Sakorn Sukkasemsakorn

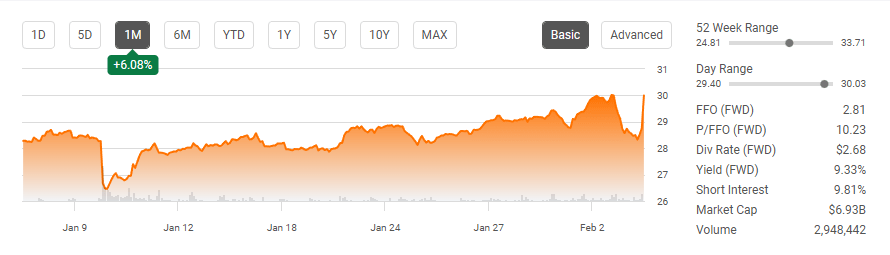

I just finished reading through Omega Healthcare Investors (NYSE:OHI) Q4 2022 and full-year 2022 results, and my investment thesis hasn’t changed. It’s going on three years since the pandemic started, and Seeking Alpha contributors and members still question OHI’s ability to maintain the current dividend. Things aren’t perfect, and OHI has faced adversity since 2020, but come 2/15/23, its 12th quarterly dividend will be paid in full since the pandemic started. The market seems to have digested earnings rather well, as OHI is up 11.32% since 1/10/23 and bounced 5.93% since earnings were released. Nobody can accurately predict what will unfold in the future, and we must make the best decisions with the information we have today. Another dividend payment is incoming, and another earnings conference call has concluded without a reduction to the dividend. I feel strongly that if the board was going to reduce the dividend, it would have occurred already. Unless something unforeseen occurs, the commentary from senior leadership on the earnings call makes me believe that the high-yielding dividend is safe and that the projected dip in funds available for distribution (FAD) in Q1 will be a one-time occurrence and return to a FAD run rate that exceeds the dividend in the fiscal year of 2023.

Seeking Alpha

Management spoke specifically about the dividend and gave no indication that the dividend was in danger

The main reason I have been invested in OHI is for the dividend. When you’re being paid a dividend with a yield that fluctuates between 7.5% – 10%, the powers of compounding can truly be remarkable over an extended period. On the Q4 2022 conference call, Taylor Pickett (OHI CEO) wasted no time discussing the dividend. OHI generated $0.70 of adjusted funds from operations (AFFO) per share, and the FAD in Q4 2022 was also $0.70 on a per-share basis. The current quarterly dividend of $0.67 per share has a 92% payout ratio from AFFO and is 96% of FAD. In 2022, OHI generated $2.77 of FAD, which exceeded the annualized dividend of $2.68 per share by $0.09. Mr. Pickett briefly touched on operator restructurings and indicated that OHI is projecting that the FAD in Q1 2023 will be less than $0.67, but OHI will return to a run rate that exceeds the dividend in 2023 as the current restructurings are resolved.

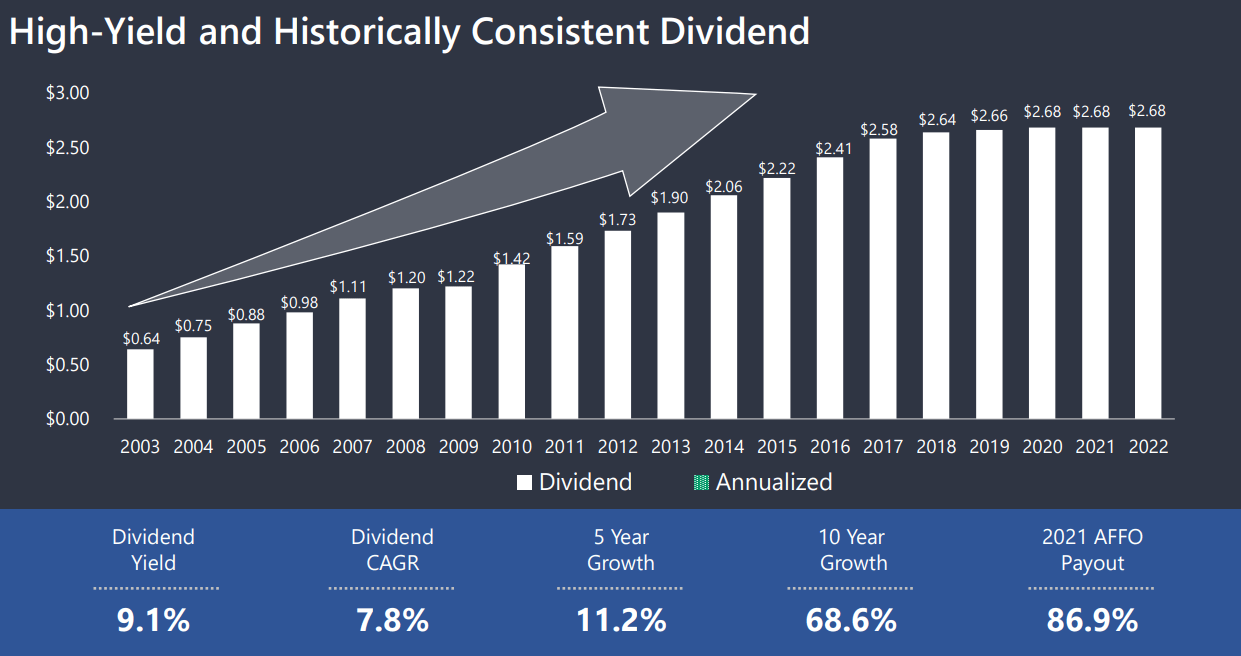

Mr. Pickett was pressed on this in the Q&A by Jonathan Hughes of Raymond James as to the board’s comfort level of maintaining the current dividend. Mr. Pickett stated that he could only speak to his comfort level, but based on the commentary from Bob Stephenson (OHI’s CFO) and connecting the dots between what is occurring from Q1 2023 through Q2 2023, he has a high level of comfort regarding the current dividend level. He added that with Agemo coming back on and the transition of the 2.4% operator, these are significant moving parts to help deliver a “comfortable FAD” from a dividend perspective. I can only make decisions based on the information I have, and the Q4 2022 conference call is the latest commentary surrounding the dividend. Nothing in the call would make me feel the dividend would be reduced, especially since the Q1 dividend will be paid on 2/15/23, and OHI won’t go ex-dividend again until around 5/15/23. Management is fully aware that the dividend is a main investment driver for shareholders, and they are going to do everything they can to protect the dividend and not have to change the wording again on the slide below from historically consistent dividend.

OHI

A real example of how compounding OHI’s dividend would have worked out

In the first account, I purchased 163 shares of OHI. I purchased 100 shares in the fall of 2017 at $31.50 per share, then another 63 shares in January 2018 at $27.38 per share. My average out-of-pocket price per share is $29.91 prior to incorporating dividends. I have received 21 dividends since my initial investment, which has generated $2,749.59 of income and added 84.62 additional shares to my investment. My total amount of shares and income generated from the shares have increased by 51.91%. So far, my initial investment is up 52.37%, and I am generating an additional $225.94 in projected annualized dividend income.

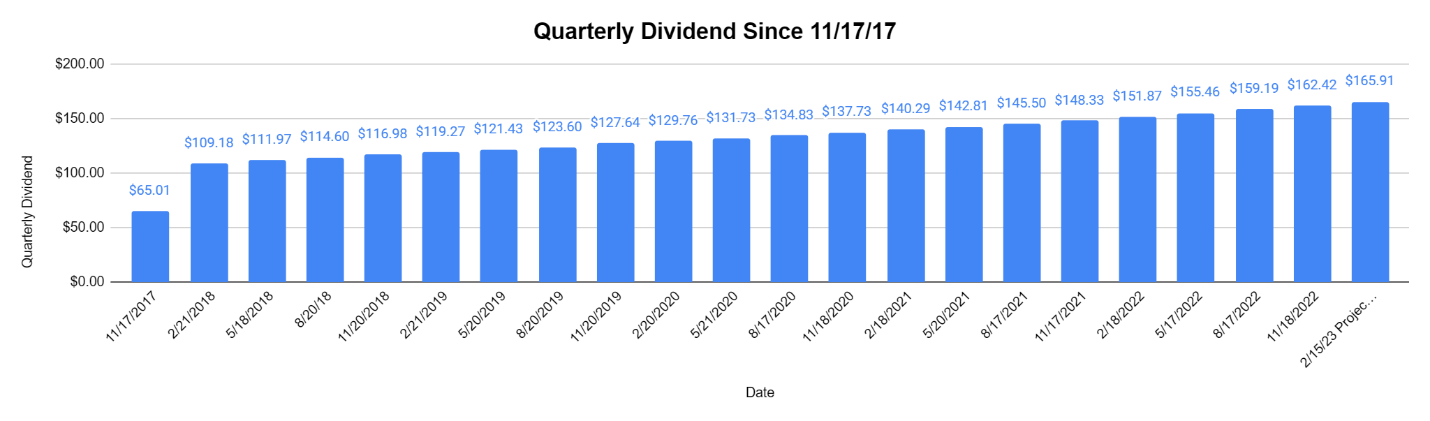

The next dividend is right around the corner, and I am expecting to generate $165.91, which will be reinvested. OHI is a REIT that I plan on holding for decades to come unless something changes within my investment thesis toward OHI. The dividend snowball is slowly growing, but each quarter additional income is generated. There is a large bump in my second dividend payment as I had dollar cost averaged before the ex-dividend date. Based on the $165.91 projected dividend coming on February 15, my quarterly dividend income over the previous 20 quarters has grown by $56.73, or 51.96%. This will continue to grow quicker and quicker over the years, and eventually, if OHI gets back to dividend growth, the powers of compounding will only intensify.

Steven Fiorillo

OHI had a descent 2022 and made significant headway on restructurings

In Q4, OHI generated $47 million in net income, $177 million in AFFO, and $171 million in FAD. OHI completed $89 million in acquisitions and funded $15 million in capital renovations and construction-in-progress projects. OHI sold 33 facilities for $321 million in cash, generating a $180 million gain. In the fiscal year of 2022, OHI generated $439 million of net income, $730 million in AFFO, and $678 million in FAD. They completed $238 million in acquisitions, invested $96 million in three new loans, and funded $70 million worth of capital renovation and construction in progress projects. OHI repurchased five million shares for $142 million and sold 77 facilities for $759 million in cash, generating a $360 million gain.

OHI made a substantial amount of progress in its portfolio restructurings over the year. The restructuring of Agemo concluded in Q4. All 22 facilities were sold to third parties for $366 million. The remaining portfolio consisting of 11 facilities in Kentucky and 18 facilities in Tennessee are contractually obligated to resume rent and interest in April of 2023 in the amount of $27.9 million per annum. The master lease has been extended from December 31, 2030, to December 31, 2036. LaVie, which is OHI’s largest tenant, paid its rent through 2022 but anticipates that liquidity issues will materialize. As part of the restructuring to mitigate risk, OHI divested 11 facilities to a third party for a gross sales price of $130 million. Healthcare Homes is OHI’s largest UK operator, with 42 care homes. OHI has agreed to allow up to four months of rent deferral from January 2023 through April 2023. OHI restructured the Maplewood contract, which consisted of 17 high-end senior housing facilities located in the Northeast region of the United States. OHI agreed to defer rent escalators through year-end 2025, defer interest payments due on secured credit facility by permitting payment-in-kind until cash flow permits future payments anticipated to begin in 2024, and increase the secured credit facility by $13 million to support near-term liquidity needs.

An existing operator representing 2.4% of OHI’s contractual rent, which has remained unidentified, has failed to pay full contractual rent since March. OHI has utilized the security deposit of $2 million to offset a portion of this rent. OHI and the operator are in talks to transition this portfolio to a third-party sometime during the first quarter of 2023. Another unidentified operator representing 2.2% of OHI’s rent has been making partial rent payments since Q2. OHI has been tapping the $5.4 million security deposit to offset shortfalls. OHI has discussed potential sales of the portfolio with the operator.

OHI

OHI has been on top of its portfolio throughout the pandemic and worked with providers to meet their obligations. When you’re a long-term investor, sometimes there are extended periods of adversity, and things don’t go right every year. I want to be invested in a management team that can solve issues, not just reap the rewards when things are going well. I have to take management at face value that while investors will see a dip in FAD in Q1, the total 2023 FAD will exceed the annual dividend. Management has been actively trimming locations, making new investments, and restructuring agreements to ensure that OHI makes it out to the other side. I think senior leadership has earned the trust of shareholders, and while the share price may not be where some would like to see it, there is no reason significant appreciation can’t occur in the back half of 2023 when the restructurings are finalized.

Conclusion

Once again, there was no discussion leading to an indication of a dividend cut after the Q4 2022 results were released. OHI is doing its part to maintain the dividend while providing a roadmap of what to expect in the coming quarters. In 2022, OHI delivered an additional $0.09 in FAD than was paid from the dividend, and expects 2023’s FAD to exceed the annual dividend despite a blip in Q1. OHI’s dividend has been maintained for three years since the pandemic without a reduction, and the CEO reaffirmed that he is comfortable with OHI’s ability to deliver the current dividend to shareholders. Anyone who still believes that OHI will need to cut the dividend should read the earnings report carefully, as that is currently not the situation. I think OHI is a strong buy here as the market received the earnings report well, the yield is almost 10%, and investors could see capital appreciation in 2023 as the remaining restructurings are completed.

Be the first to comment