Ozgu Arslan/iStock via Getty Images

This article is an update to my previous coverage on OCUL stock which can be read here. Today, I’d like to focus on some exciting new data which Ocular Therapeutix (NASDAQ:OCUL) released this weekend for its Phase I trial in wet AMD (Age related Macular Degeneration). For readers unfamiliar with the disease, I refer you to my previous article, in which I gave a relatively detailed overview, including saying this about its prevalence:

Genentech estimates that in 2011 there were about 1.7M cases of wet AMD in the US and that 200,000 new cases are diagnosed annually in North America. It further estimates that by 2020 there would be nearly 3M cases in the US. Research and Markets estimates that there are about 4.4M wet AMD cases spread across the US, EU5 and Japan in 2020.

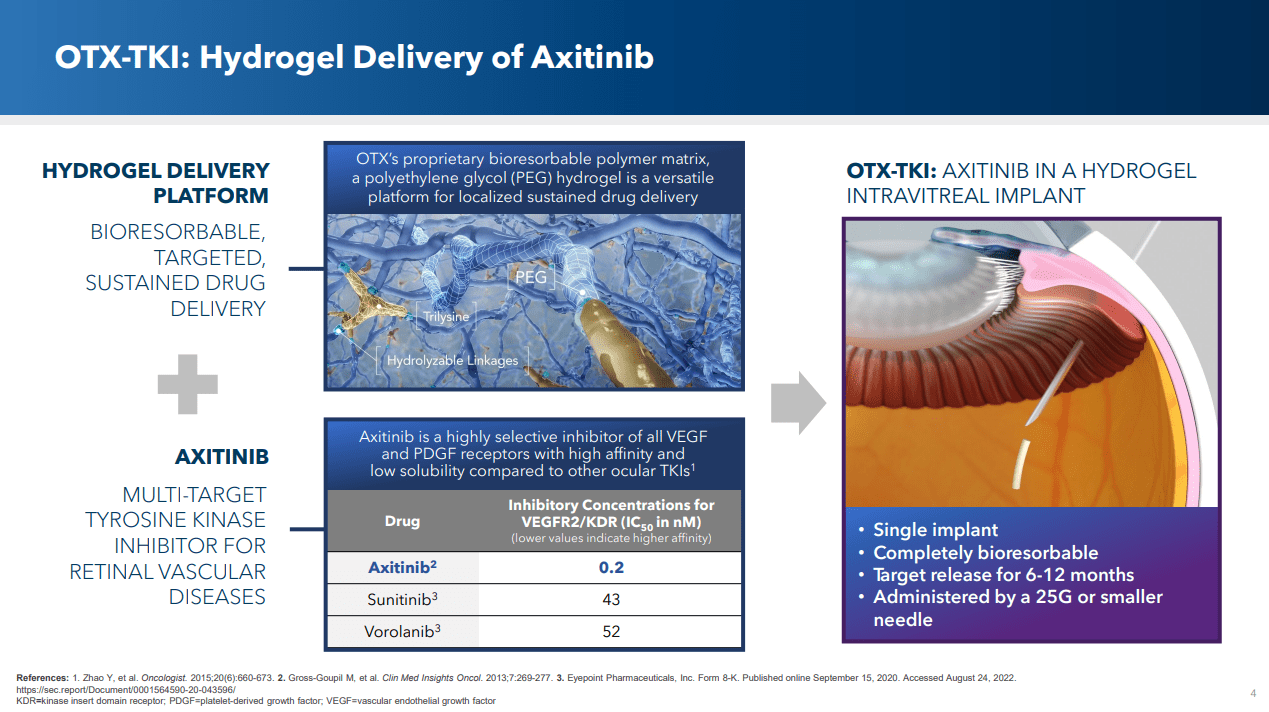

OCUL’s Candidate Treatment for Wet AMD: OTX-TKI

OTX-TKI is an intravitreal implant with a hydrogel that’s intended to deliver a tyrosine kinase inhibitor, Axitinib, whose primary mechanism of action (MOA) is through VEGF inhibition.

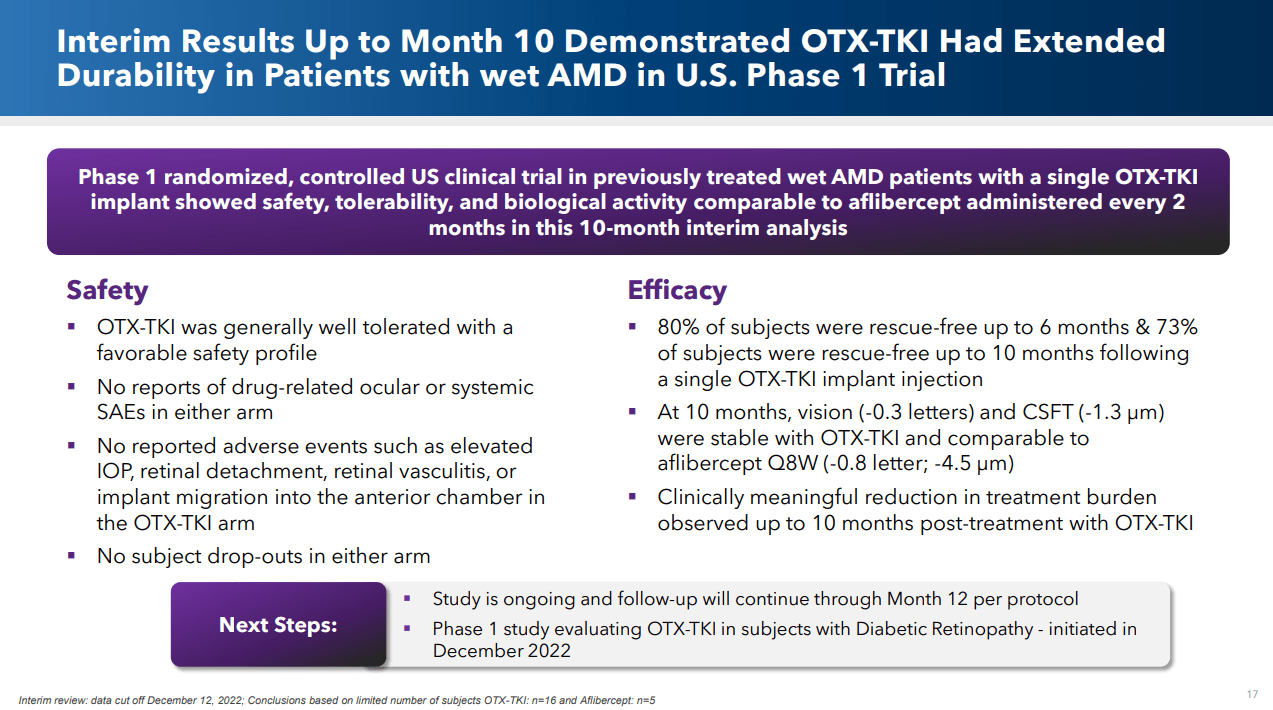

It is currently being tested in its second Phase I trial, this one being conducted in the US on patients who have no (aka controlled) fluid in the eye. The data now spans 10 months which the company summarized in this presentation. As can be seen in the slide below, the goal/hope is for treatment to be effective from somewhere between 6 and 12 months.

Corporate presentation

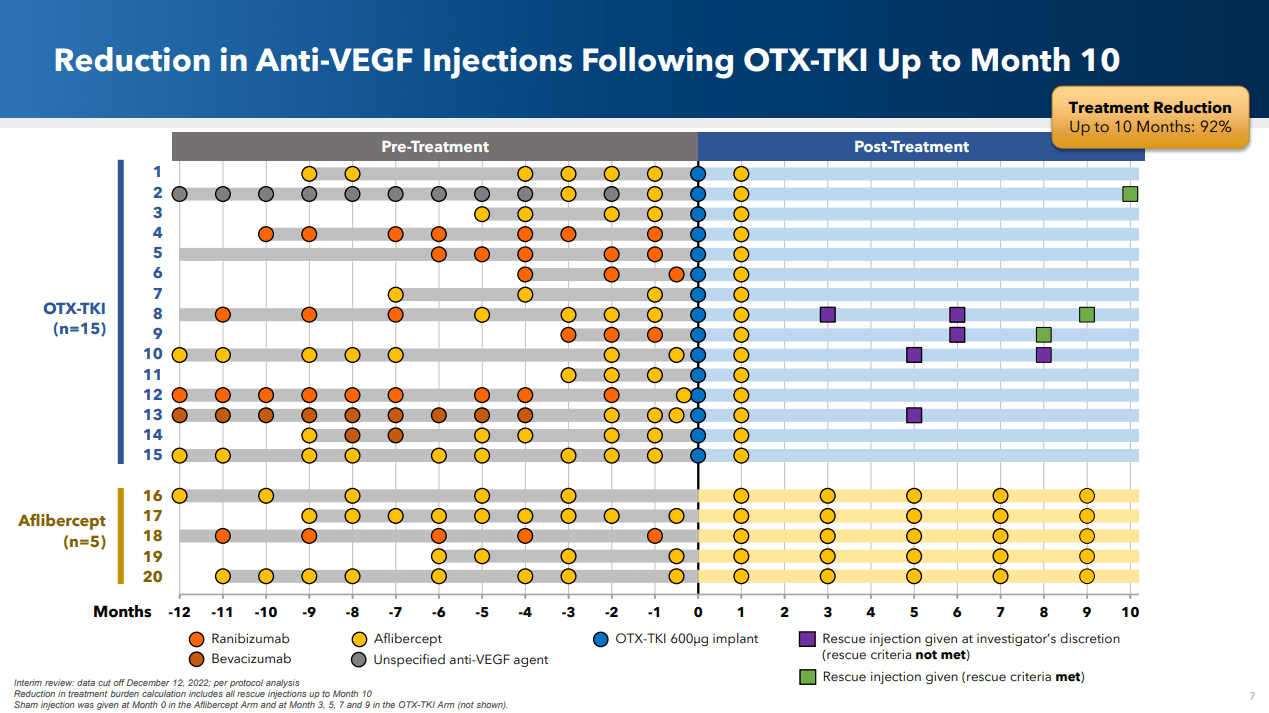

In my opinion, the pièce de résistance from the presentation is probably this slide which shows that 11 out of 15 patients (73%) were rescue-free after 10 months. (Note that the rescue squares are plotted such that the rescue occurs after the time tick on which they’re shown, which I personally find a bit confusing. So, for example, patient 2 was rescued after 10 months and thus was rescue free at 10 months.)

Corporate presentation

The lower portion of the graph shows the number of treatments that someone on the standard of care ( Aflibercept or Eylea) receives. Clearly the treatment burden is much less with OCUL’s candidate treatment than what occurs with the current standard of care (SOC). And given that we’re talking about injections into the eye, this is very significant.

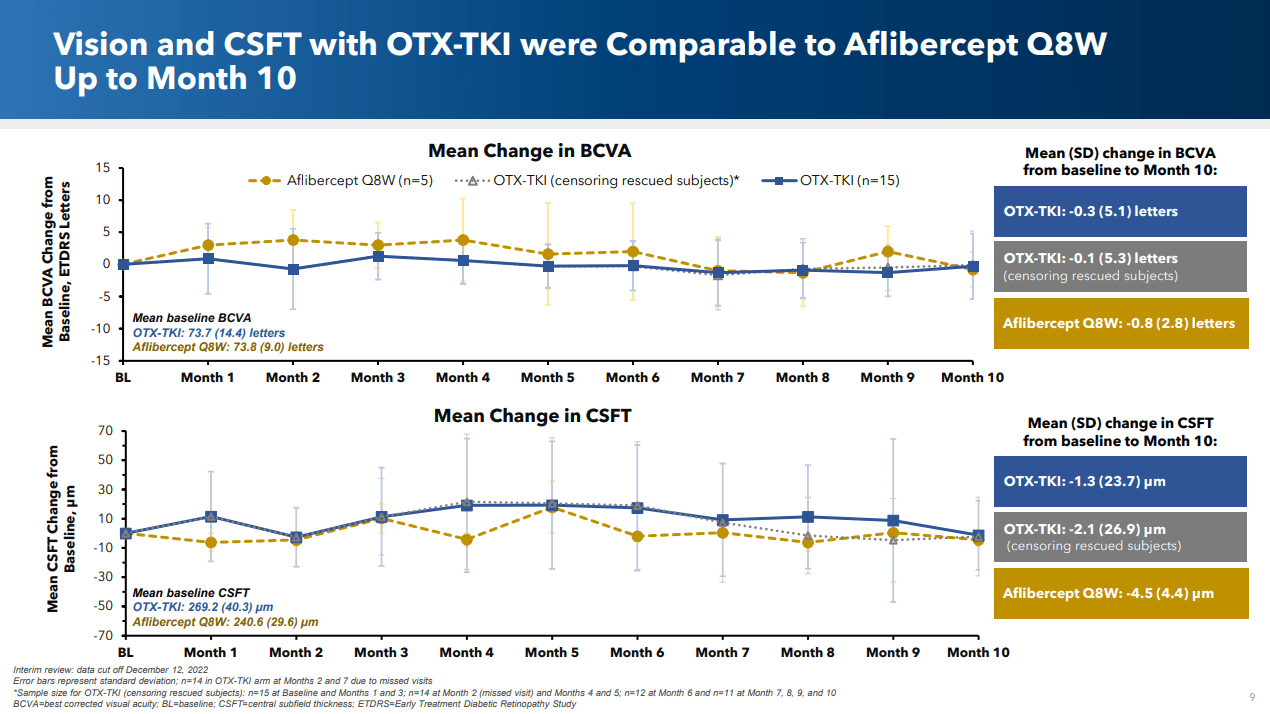

Importantly, the efficacy of the two treatments were similar, both in terms of vision and of central sub-field thickness (which is a measure of the thickness of the macula, and which can decrease as an effect of wet AMD). Indeed here’s what ChatGPT had to say about this latter point:

There is a significant correlation between the thickness of the central subfield and the presence of wet AMD. Studies have shown that patients with wet AMD tend to have thinner central subfield measurements compared to those without the condition. This is likely due to the fluid and blood accumulation associated with wet AMD, which can cause edema (swelling) and thinning of the macula.

Central subfield thickness measurement can be used as a tool for monitoring the progression of wet AMD and the effectiveness of treatment. In cases of wet AMD, treatment is aimed at slowing or halting the growth of abnormal blood vessels and preventing further vision loss. Regular monitoring of central subfield thickness can help determine whether the treatment is working and whether any changes are needed.

Here’s the slide comparing these two important metrics for OCUL’s candidate treatment vs. the SOC:

Corporate presentation

I submit that given the closely similar effectiveness, OCUL’s much easier treatment regimen will be seen very favorably by doctors and patients (important caveat: these are Phase I results and there’s much work and much that can go wrong before the product is ever commercially available).

Safety Profile

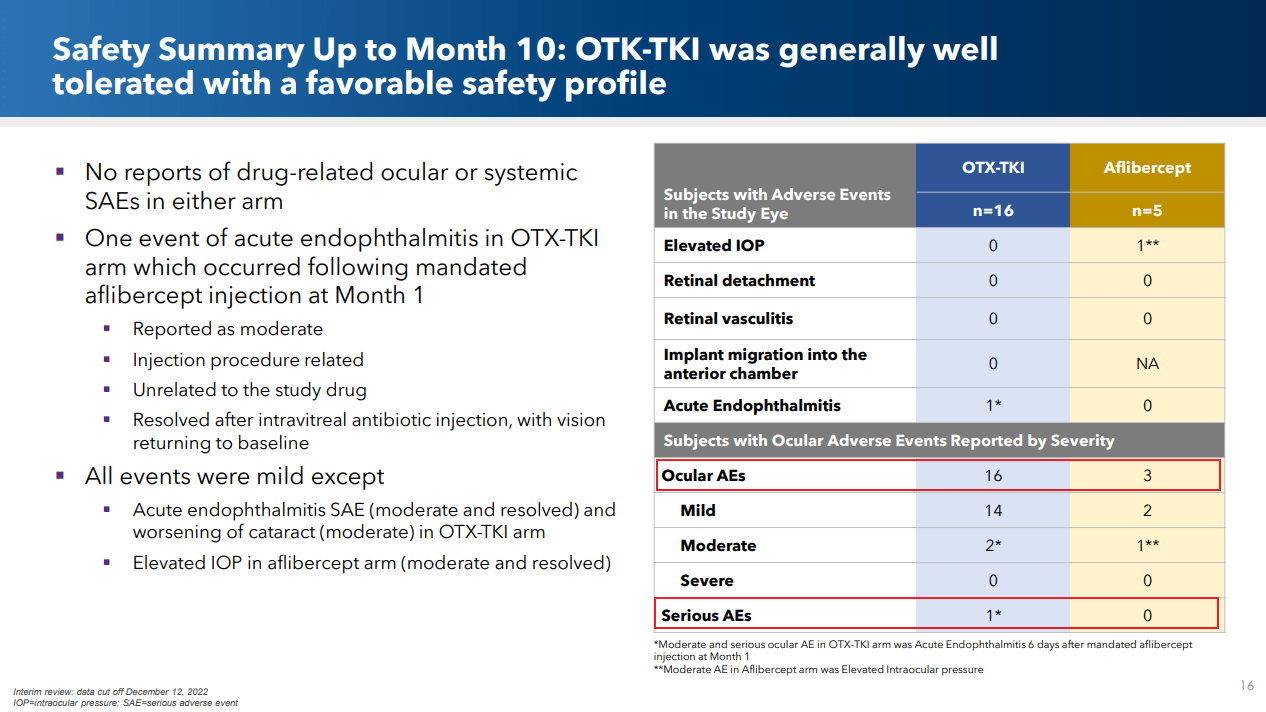

The one negative in the comparison between OTX-TKI’s performance vs. the standard of care is as it pertains to safety. Fourteen out of 16 OTX-TKI patients (88%) experienced some form of adverse events vs only 3 out of 5 (60%) for the SOC patients (though the error bars for these very small sample sizes likely overlap). OCUL makes the point that several of the adverse events came after the aflibercept injection at month 1, but they still go to this treatment’s account.

Corporate presentation

Importantly, however, there were no patient dropouts in either arm due to these adverse events.

Data Summary

OCUL ends its presentation with this slide which highlights not only the new data, but also the performance at 6 months which shows 80% of subjects were rescue-free when treated with the OTX-TKI protocol. It also highlights the fact that this same drug is now being evaluated in perhaps an easier indication, viz. diabetic retinopathy. I intend to cover this latter topic as soon as any initial data is available.

Corporate presentation

I personally am very impressed and encouraged by this data, especially given that this is a very serious and prevalent disease setting, and am considering adding to my position in the stock. But with that in mind, let’s look at a few of the important stock metrics to either temper or support this inclination.

Operating Performance

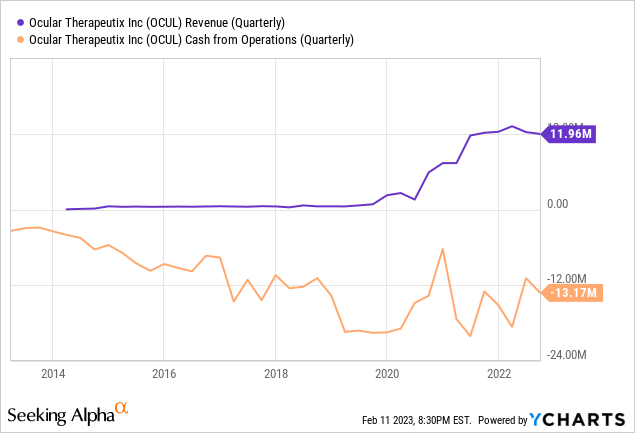

Currently the company has one commercial product, Dextenza, but despite its promise and its expanded label, financial performance has been disappointing.

The good news is that the company recognizes this, and spent a good portion of the most recent earnings call addressing it. Since it’s very important, I’m supplying a longer quote than normal to help readers understand the company’s plans to improve performance in this regard (with my emphasis):

In the third quarter, we reported net sales of DEXTENZA of $11.9 million, essentially flat year-over-year and down approximately 2% sequentially quarter-over-quarter. Relative to the potential of the opportunity and our own expectations, this represents a disappointing result and is clearly unacceptable.

We believe that there are three main reasons for DEXTENZA’s performance. The first is that our customers ASCs and HOPDs remain in a difficult situation. Since the pandemic, the majority of our customers have been chronically short of staff or recently re-staffed with generally less experienced people than they had before the pandemic.

Buy and build products like DEXTENZA a huge advantage for the ASC and HOPD when administered appropriately, do require experience back office staff and surgical staff to properly implement and administer. Understandably, in the current environment, ASCs and HOPDs are reluctant to add extra work and complexity.

The second reason is that we are in a similar position as our customers and our own ability to maintain an experienced field-based team with minimal vacancies, which we have – which have been higher than we would have liked over the past few quarters.

The final reason behind DEXTENZA’s performance has to do with changes in the reimbursement landscape for the procedure code, CPT 68841, and it is clear that volume has been impacted due to the reduction in physician payment for the insertion of DEXTENZA when our procedure or CPT code was converted from a Category III T code into a Category I code effective January 1, 2022.

[…] I’m happy to report the variable over which we believe we have the most control is the closest to being resolved. We are now nearly at full capacity in our field force with the team trained and in the field.

[…] We have had tremendous improvements in coverage and reimbursement of late and we need to get our customers comfortable giving more patients access to the benefits of DEXTENZA.

The next two elements over which we believe we can have the most control are the value proposition for DEXTENZA and the procedure code 68841 associated with insertion. Last quarter, we began issuing an off-invoice discount that was well received by our customer base as it removed the most common injection voiced by our accounts.

We also have implemented a number of strategies working with CMS in an effort to appropriately rebalance the value proposition for DEXTENZA and CPT 68841 in the future. While early in the implementation, we started the fourth quarter well with October recording the strongest monthly in-market sales ever nearing 11,500 billable units and eclipsing our previous record by more than 900 inserts.

Cash on Hand

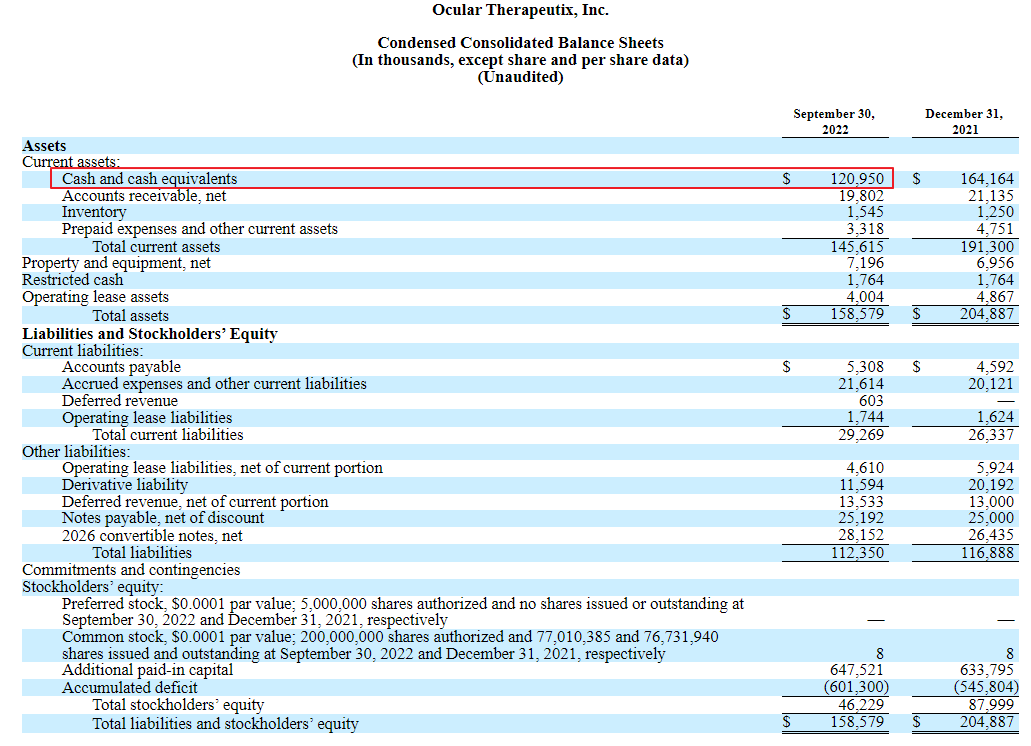

According to the most recent balance sheet, OCUL has about $121M in cash and cash equivalents on hand. It also has 77M shares outstanding which means it has about $1.57 of cash per share. With the stock trading at $3.87, the cash on hand represents about 40% of the share price. This significantly de-risks holding the stock in my opinion.

sec.gov

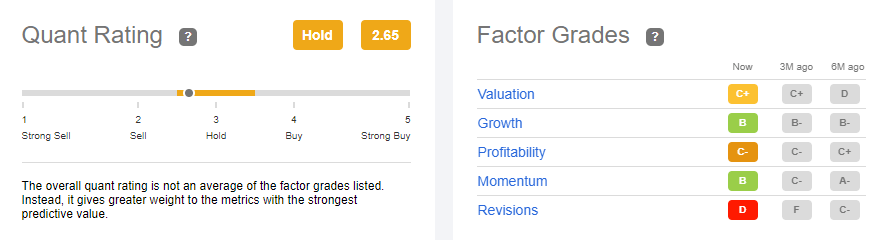

Valuation

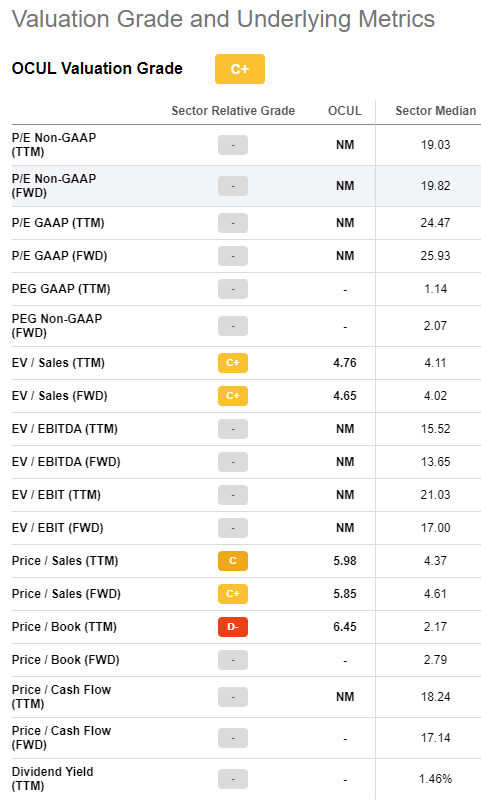

Because sales of Dextenza have been underwhelming and the company is unprofitable, OCUL receives a grade of C+ from Seeking Alpha. Here are the relevant metrics:

Seeking Alpha

Quant Ratings

Currently Seeking Alpha gives OCUL a hold rating with the worst factor grade being “Revisions”. I think we’ll see a change in sentiment with the data discussed above and I believe that will bleed through to the ratings over time. But it will be very instructive to monitor this going forward.

Seeking Alpha

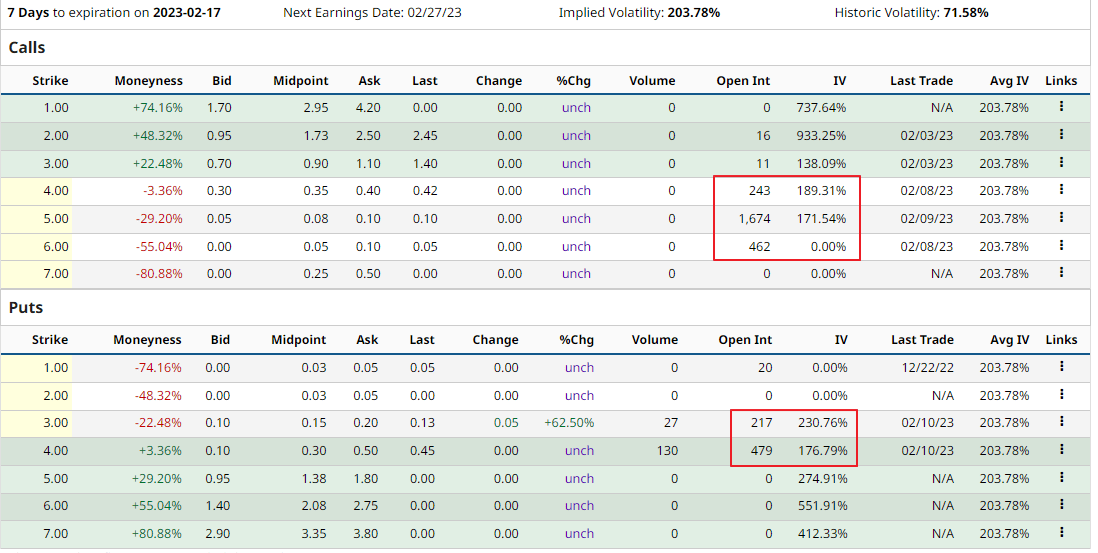

Options

OCUL trades options which sport quite high implied volatilities and which have a moderate open interest. Thus they may be suitable for smaller players to engage in strategies like covered calls or cash secured puts.

barchart.com

Risks

OCUL faces numerous risks and anyone’s position size should acknowledge these.

First, sales of the company’s only commercial product have been quite disappointing, and while the company may have plans to address this, actual results should be weighed more heavily than any plans.

Second, the very encouraging OTX-TKI results discussed herein are caveated by the fact that they occur in a Phase I study with only 15 patients in the OCUL arm of the trial. Much could change with more advanced trials involving larger numbers of patients.

The company has a decent amount of cash on hand, but if it can’t ramp up Dextenza sales and perhaps become cash flow positive, then it will likely need to raise cash to advance its pipeline.

Summary

While there are very real risks involved with owning OCUL, I’m very encouraged with the recent early stage results of OTX-TKI in wet AMD. I already hold a speculative sized position in the stock (a position which is currently underwater at today’s stock price) but I’m seriously considering averaging down based on these newly released results. In either case, I intend to continue my coverage of the company going forward.

Be the first to comment