bymuratdeniz

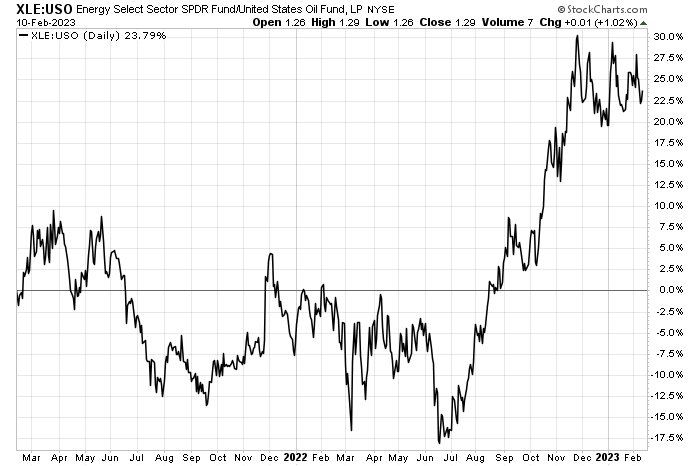

Last year, I wrote a lot about how energy equities were outpacing the move in oil during the middle of the year. Recall how WTI climbed well into the triple digits on geopolitical fears. The Energy sector ETF (XLE) managed to continue higher even after oil peaked. That was a powerful relative strength trend for oil stocks, but now we see a pause in the trend.

The XLE vs USO chart is key for energy investors to monitor – a breakdown below the late 2022 low on the chart below would portend a further pullback in big-cap Energy sector names. Until then, though, I see the pattern as a bullish continuation feature.

Let’s dig into one domestic player with operations around the world.

Energy Equities Steady Vs Oil Lately

Stockcharts.com

According to Bank of America Global Research, Occidental Petroleum (NYSE:OXY) is an oil-levered multinational organization whose principal business segments are oil & gas and chemicals. The oil and gas segment explores for, develops, produces, and markets crude oil and natural gas primarily in the US Permian Basin, Latin America, and the Middle East/North Africa. The chemicals segment manufactures and markets basic chemicals, vinyls, and performance chemicals.

The Houston-based $59 billion market cap Oil, Gas, and Consumable Fuels industry company within the Energy sector trades at a low 5.5 trailing 12-month GAAP price-to-earnings ratio and pays a small 0.8% dividend yield, according to The Wall Street Journal. Ahead of earnings, OXY has a notable 5.4% short interest for such a large firm.

A major tailwind for so many oil & gas companies right now are shareholder accretive activities. Chevron announced a gangbusters stock buyback program last month, and Occidental’s CEO recently said buybacks take priority over production growth right now. I like that from a stock performance standpoint. Another gradual bullish factor in 2023 is China’s reopening, but the rebound has been slow to materialize so far. Finally, volatility could hit later this month when 13F filings are announced – will Berkshire Hathaway keep buying? Recent announcements have led to share price upside.

The major risk for OXY is a further pullback in oil & gas prices, and recent price action in both areas has been unimpressive, but WTI is holding onto the low $70s. In the upcoming earnings report, I will be watching what capex plans the management team has as well as how free cash flow verifies (within the minor Q3 earnings miss, free cash flow was a tad light against BofA’s call).

On valuation, analysts at BofA see earnings having risen tremendously in 2022, but per-share profits are then expected to moderate to under $10 this year with a further drop in 2024. We can use a high-single-digits earnings dollar figure to determine the overall valuation. The Bloomberg consensus forecast is less sanguine compared to BofA’s outlook. Dividends, meanwhile, are expected to rise at a steadier rate, but the yield should remain modest on this oil name.

Despite the tepid earnings growth expectation, OXY trades at an EV/EBITDA ratio about half that of the broad market it trades at a very cheap 5x 2022 free cash flow. Even if we normalized that to the 2022 and 2024 rate, it’s still just about an 8x FCF multiple. Profitability is obviously extraordinarily strong for OXY right now. Moreover, if we apply a 12x P/E on $7 of earnings, the stock is decently undervalued.

Occidental: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Monday, February 27 AMC with a conference call the following afternoon. You can listen live here. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

Wall Street Horizon

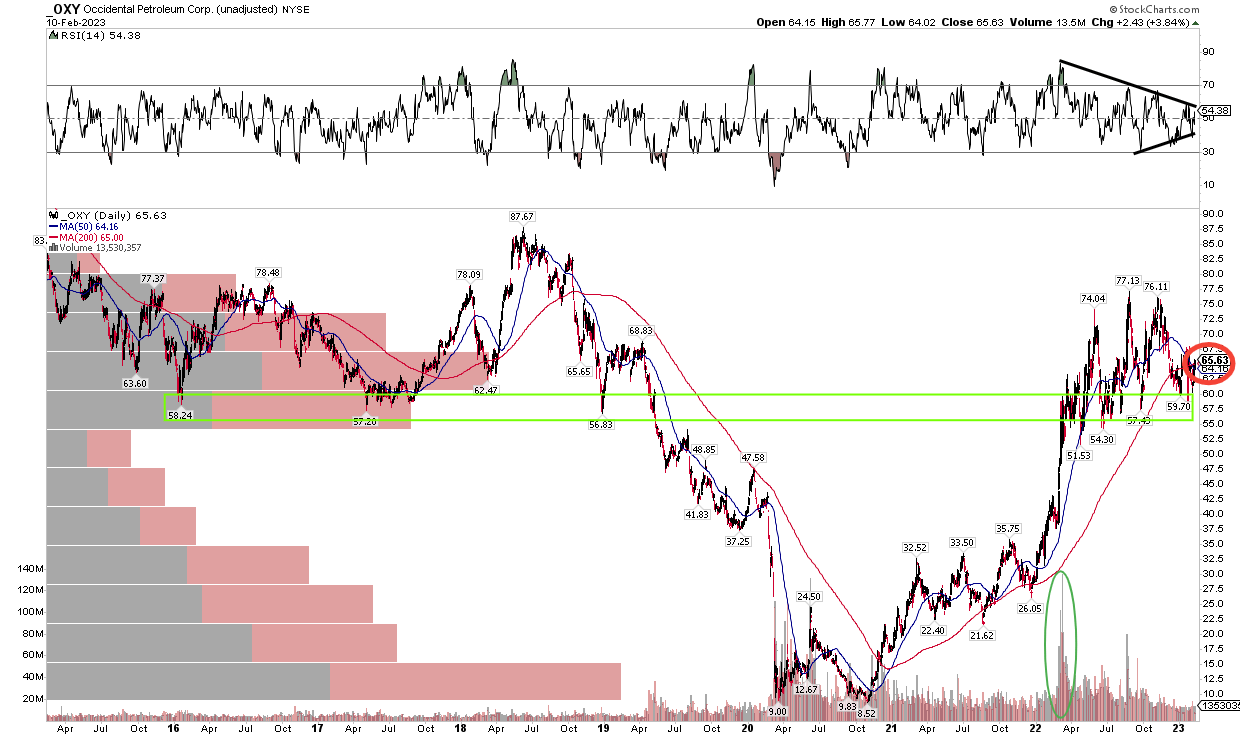

The Technical Take

With a solid valuation and the thumbs-up from good ole Uncle Warren, how does the chart look? Notice in the graph below that shares are holding important support in the mid to high $50s. At the same time, the RSI momentum indicator is in consolidation mode, so we could see a sizable move shortly – perhaps after the Q4 earnings report. Often, momentum leads price, so keep your eye on how that RSI consolidation resolves.

Also interesting is what’s going on with OXY’s volume – I see significant volume by price right where the stock trades at now. So, the presumption is this area should be supportive due to the previous congestion that we have seen. Also, there was a massive volume spike in early 2022 when shares soared, a bullish signal.

Long here with a stop under $54 looks like a favorable risk/reward.

OXY: RSI Consolidation, Shares Holding Support

Stockcharts.com

The Bottom Line

OXY has come a long way in the last year, but it still trades at a very favorable free cash flow multiple. With oil prices holding in the $70s and natural gas prices hopefully finding a floor after a mild winter, OXY’s diversified operations should be in a good spot to continue to spit off cash and reward shareholders with buybacks and debt repayments.

Be the first to comment