hallojulie

With the world heading into a potential global recession, investors shouldn’t expect another record return for Occidental Petroleum (NYSE:OXY). While repeating big yearly gains is statistically hard, the company could definitely rally on higher energy prices under an unlikely scenario. My investment thesis is more Neutral on the stock trading close to $60 now.

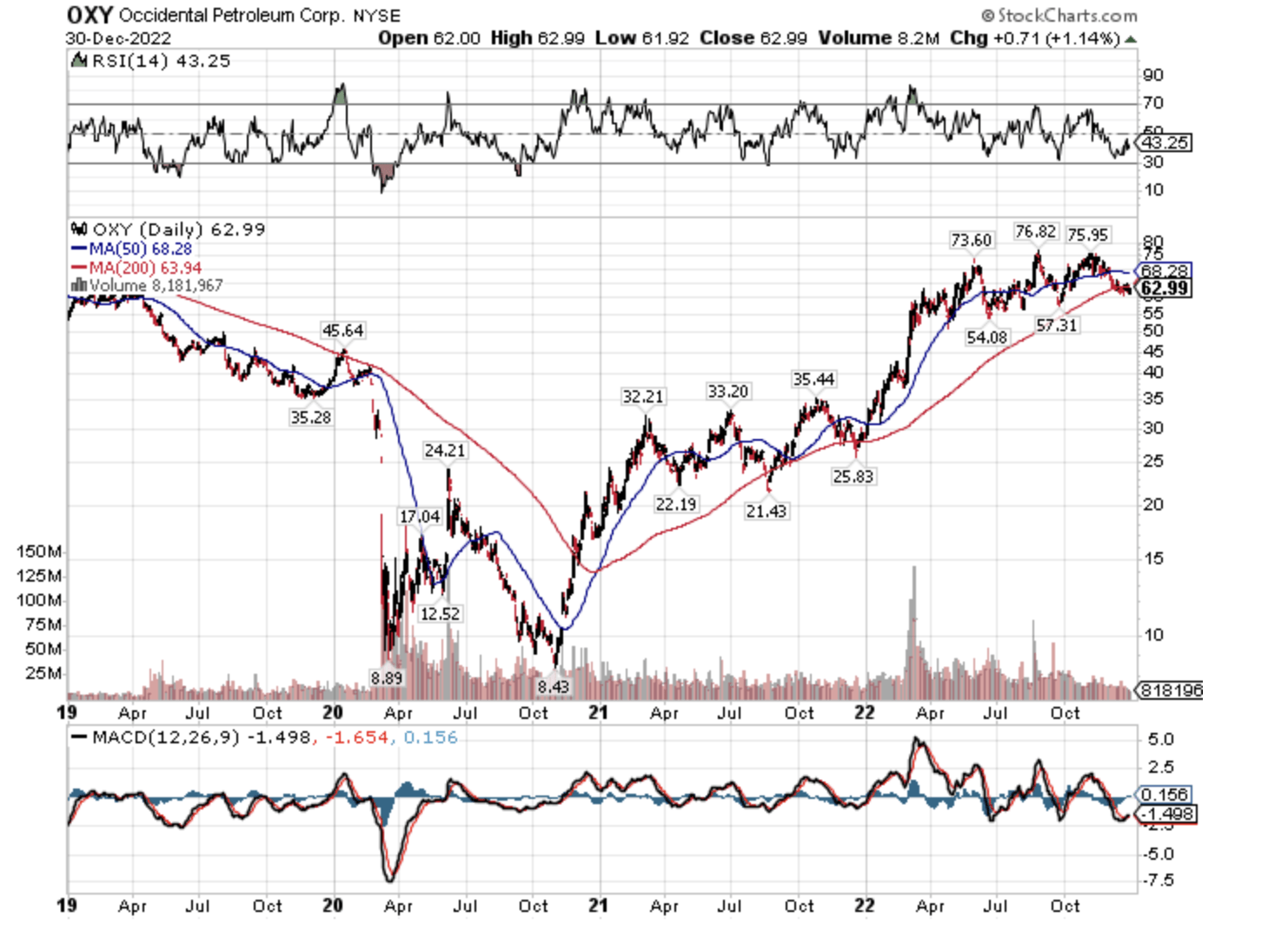

Source: StockCharts

Big 2022

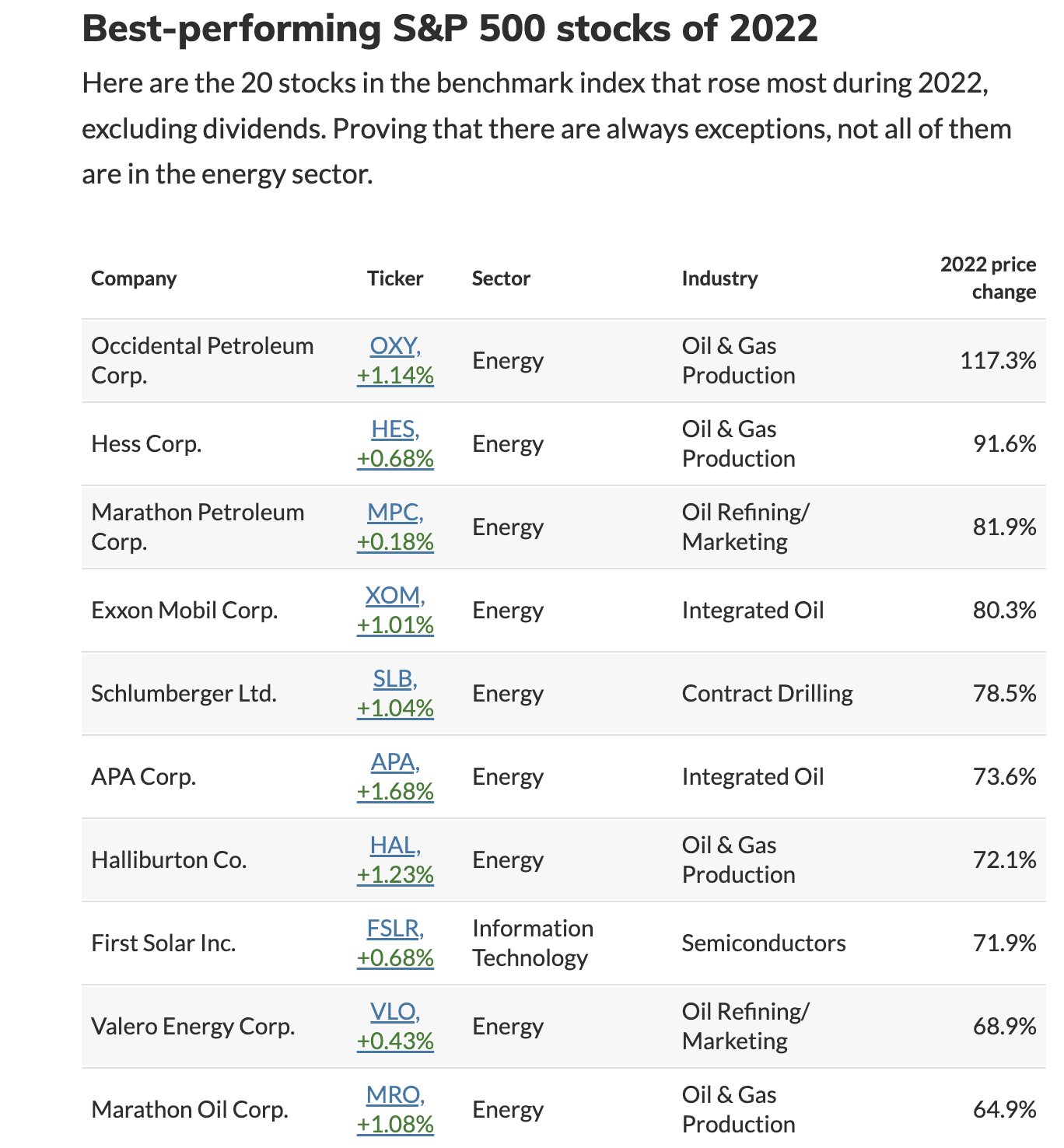

Despite the S&P 500 losing 20% last year, the energy sector had a blockbuster year. Oxy led the sector and the market with an incredible 117% gain in 2022.

Source: MarketWatch

As the table quickly highlights, all of the top performing stocks in the index were energy related enterprises. Even First Solar (FSLR) produces solar panels and most definitely isn’t in the semiconductor sector.

Oxy saw the huge gains in 2022 due in part to the stock starting the year off at only $28.75. The independent energy stock started 2021 at $17.14 and was already coming off a technically big year heading into last year.

The stock was nearly a $50 stock heading into the covid lockdowns and the economic reopening had already sent energy prices higher at the start of 2022. The ultimate final boost was the Russian invasion of Ukraine, but the stock didn’t see many gains beyond that initial rally above $60 in February.

As the charts show, Oxy needed the Russian invasion and a technically weak stock heading into 2022 in order to generate the outsized returns during last year. The stock doesn’t have this technical setup heading into 2023. In fact, the unwillingness of Warren Buffett to purchase shares above $60 doesn’t portend well for a big gain this year.

Going back a few years, Advanced Micro Devices (AMD) had multiple years of leading the S&P 500 heading into 2020. My view was that AMD was still poised to capture the title in back-to-back years due to structural shifts in the market. The positive call highlights that this negative call on Oxy is related to the fundamental setup and not any automatic prediction of a failure following a year of outsized gains.

Russian Headwind

As 2023 starts, Russia has limited territory in Ukraine. In fact, the country only controls about twice the land area as prior to the invasion of Ukraine last February.

Russia is very crucial to energy companies due to the implications on energy prices. Despite a major winter storm in the US, natural gas prices fell below $4.50 to end 2022.

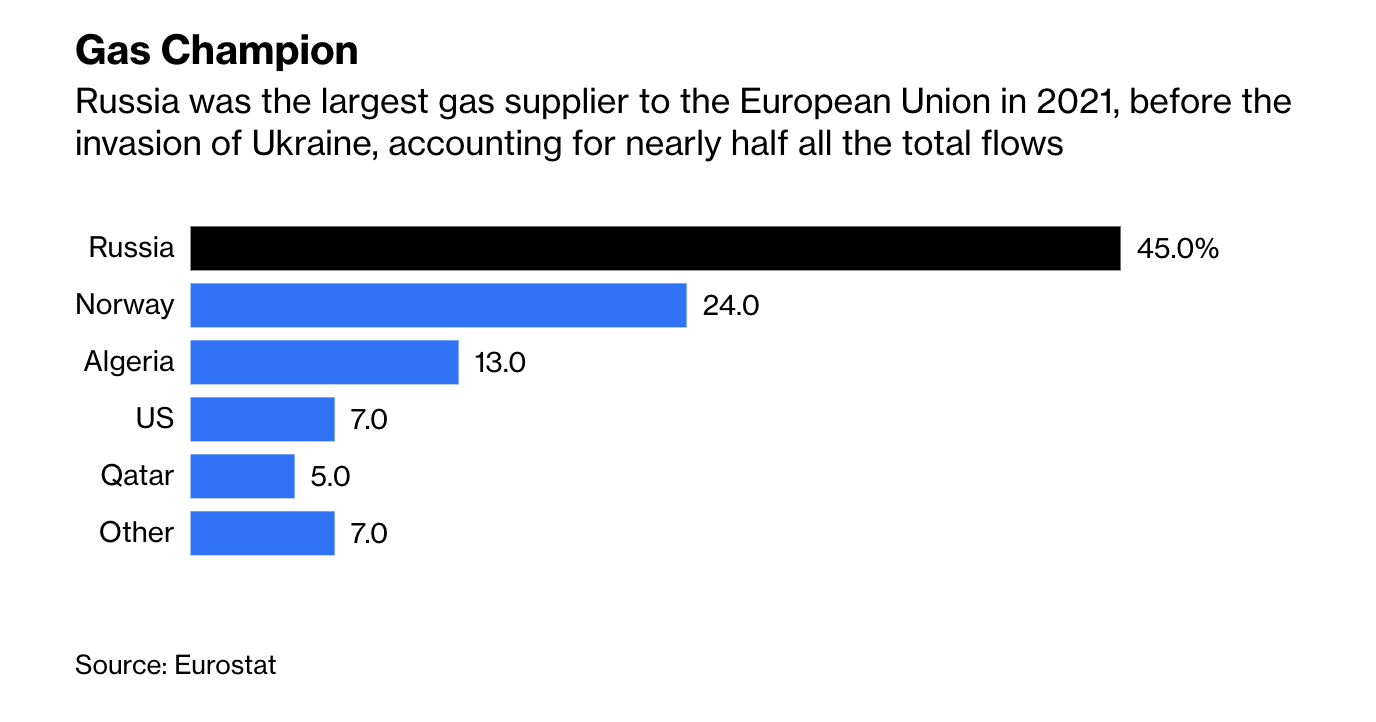

Back in 2021, Russia supplied 45% of gas used by the European Union. The U.S. has already stepped up to deliver more LNG to Europe and the IEA forecasts Europe not needing Russia gas by as early as 2025 and at the latest 2028.

Source: Bloomberg

Per Bloomberg, the view on Russian gas in European capitals is adamantly against a return of supplies to the market. The view closer to the ground probably matches this statement from Michael Kretschmer, leader of the German state of Saxony and a prominent conservative politician, on bypassing cheap Russian gas in the future:

…historically ignorant and geopolitically wrong.

Said another way, Europe is unlikely to end up passing on Russian gas, if the price is right. Besides, energy supplies are very fungible.

If Russia doesn’t send the gas back to Europe when the war is over, the country will just send more gas to China, which ultimately frees up more supplies from other destinations for Europe. After all, Russia just opened up a new field in Siberia with 1.8 trillion cubic meters of gas to feed the Power of Siberia pipeline to China with plans to build another pipeline to China.

In fact, Ukraine is likely to push some deal requiring Russia to sell gas to Europe in order to fund reconstruction. Whether this happens in 2023 or not is a big question mark with the war still ongoing, but the most likely outcome is that Russia gas becomes more of a headwind for energy prices as they ultimately find a path to the market.

Oxy traded below $40 before the invasion took place. The stock probably doesn’t fall back to those levels, but a big rally in 2023 appears highly unlikely with a positive outcome on the war in Ukraine the much more likely outcome.

Takeaway

The key investor takeaway is that Oxy remains a problematic investment in the $60s. Warren Buffett doesn’t want to buy the stock much above $60 questioning the valuation due to historical earnings based on normalized prices covered in previous research.

Oxy could definitely rally in 2023, but the upside is more likely muted after a couple of big years. Buffett bought shares at slightly lower levels, so investors shouldn’t be too bearish either. The stock is a potential buy in the mid-$50s, though the long-term EPS potential could be back in the $3s or lower considering the 2021 EPS was only $2.55.

Be the first to comment