Dilok Klaisataporn

Introduction

Even though Warren Buffett is not always right, he certainly made another great call on Occidental Petroleum (NYSE:OXY) that lead the S&P 500 during 2022 as he continued increasing his stake and as my previous article discussed, he would not get my shares too cheap. Whilst their share price is now slightly lower due to market volatility, the improvements have still continued and excitingly, as we look into 2023, this new year sees a new era of maximized shareholder returns beginning.

Coverage Summary & Ratings

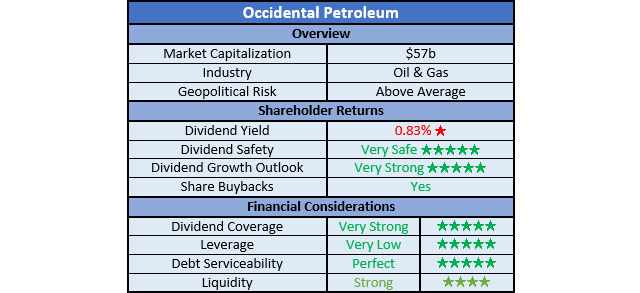

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

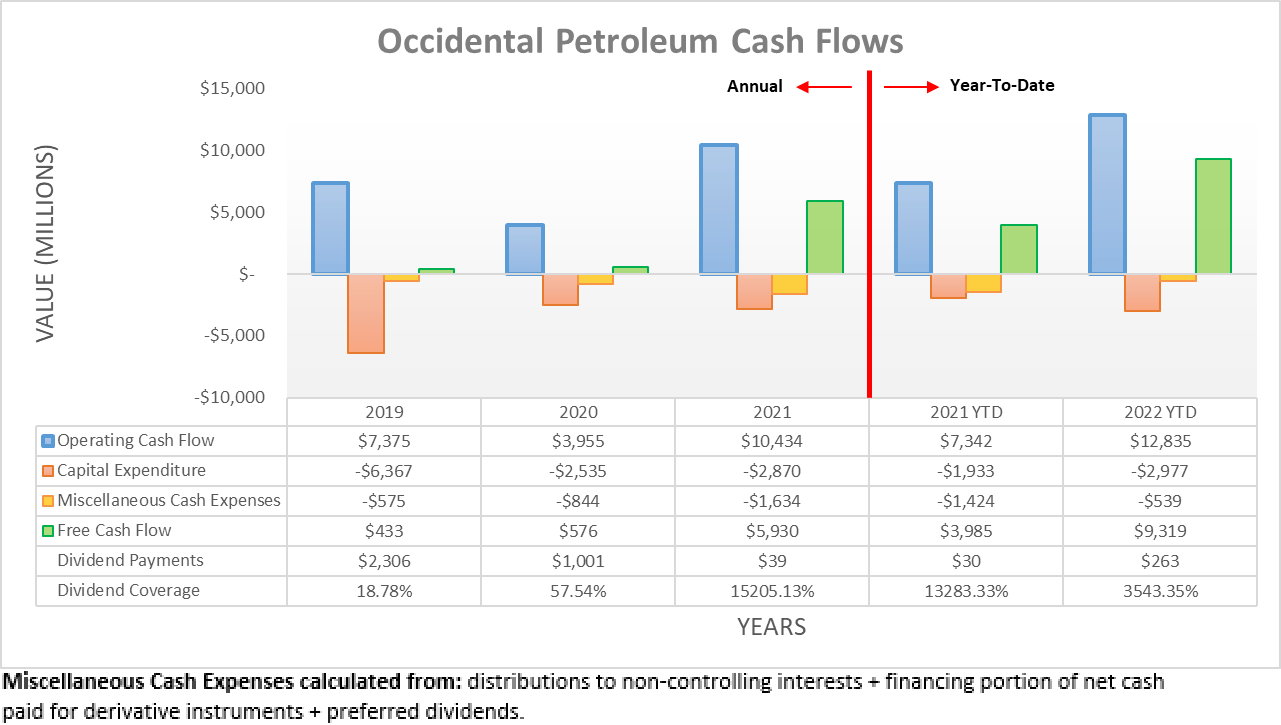

Following their record-setting cash flow performance during the first half of 2022 on the back of the booming oil and gas prices, their results continued to power onwards during the third quarter, albeit at a modestly softer pace as operating conditions softened. Regardless, this now sees their operating cash flow during the first nine months hitting a massive $12.835b, thereby up from $8.568b during the first half and thus now eclipsing even their full-year result of $10.434b during 2021. Plus, as their capital expenditure stayed modest, their free cash flow followed suit to land at an immense $9.319b across the first nine months of 2022, which even more impressively, was actually weighed down by their working capital movements.

Author

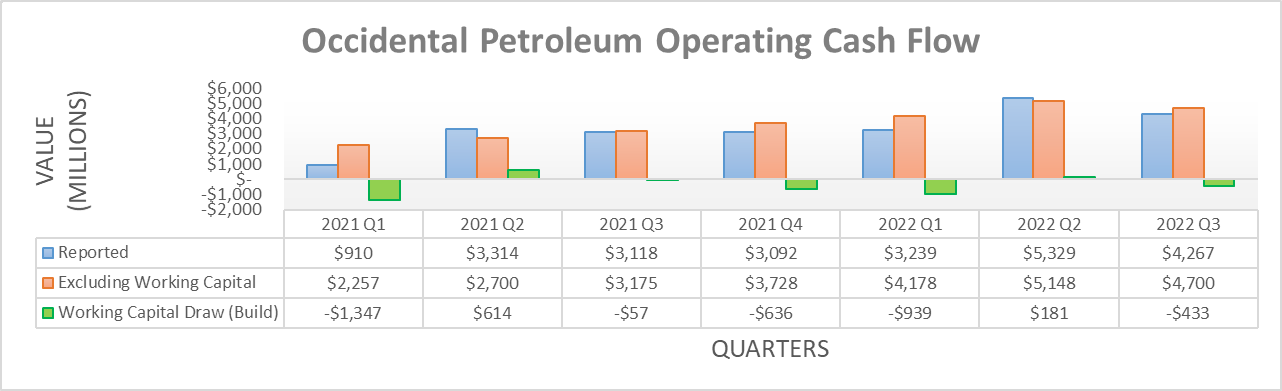

If viewed on a quarterly basis, it shows their operating cash flow and thus by extension, their free cash flow was weighed down by a working capital build again during the third quarter of 2022. Even though the second quarter saw a boost from a small $181m draw, if aggregating the first nine months, it pales compared to the builds of $939m and $433m during the first and third quarters, respectively. If excluding this headwind, their underlying free cash flow during the first nine months would have been another $1.191b higher, which equates to almost 13% on top of their reported result of $9.319b.

After spending 2021 and the start of 2022 focused upon deleveraging, they effectively achieved their net debt target following the second quarter, as my previous article discussed and thus, they ramped up their shareholder returns, mostly via share buybacks. Throughout the third quarter, these amounted to a sizeable $1.899b, which marks a much faster pace than the mere $568m that was conducted across the combined first and second quarters. Whilst positive, the more important topic is their outlook for the year ahead as the calendar has now rolled over to 2023.

Occidental Petroleum Third Quarter Of 2022 Results Presentation

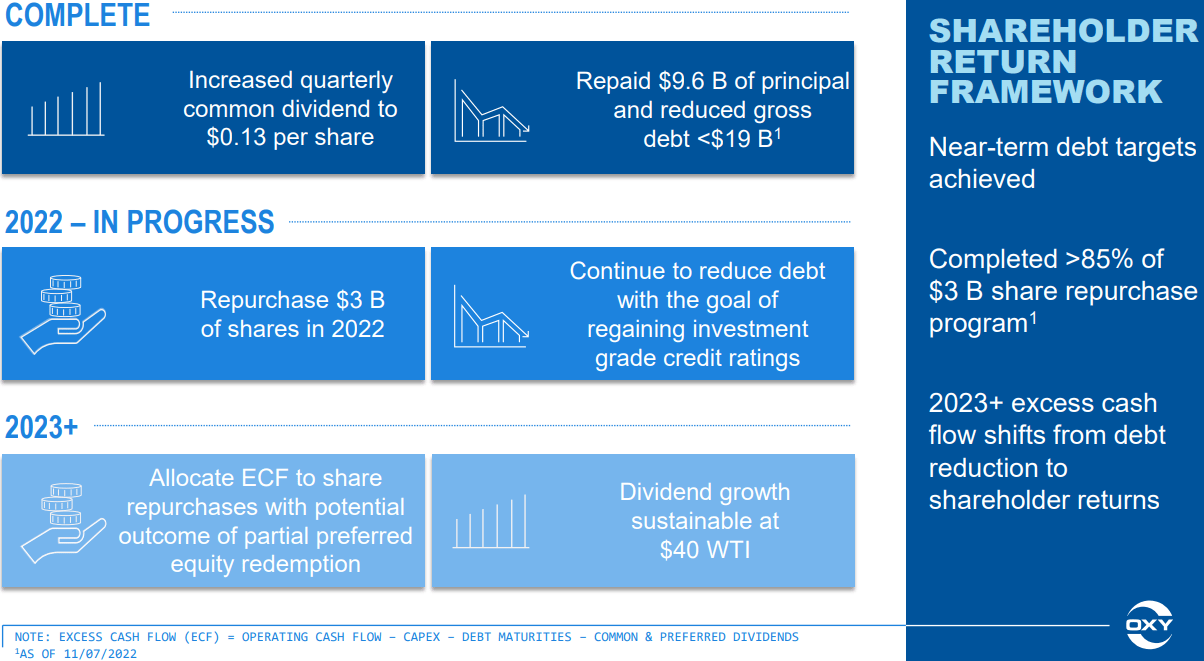

When reviewing their capital allocation strategy, it shows that beginning 2023 and beyond, they are moving to a new phase whereby they allocate all of their ECF to share buybacks. As noted at the bottom of the above slide, ECF stands for excess cash flow, which is effectively their free cash flow minus common dividend payments and debt maturities, because I already subtract preferred dividend payments from free cash flow. Unlike during 2021 and 2022, this means that deleveraging going forwards will occur at the natural pace of their debt maturities, instead of being expedited by purposely repaying debt ahead of time and thus this new relaxed pace significantly boosts their prospects for shareholder returns and creates what I view as a new era for their company.

Even though I am not normally a fan of a heavy weighting towards share buybacks over dividends, at least their shares are still sufficiently cheap, even after their market-leading rally during 2022 and without relying upon the triple-digit oil prices of 2022. If comparing their current market capitalization of approximately $57b against their free cash flow of $5.93b during 2021, it still sees a very high free cash flow yield that is slightly above 10%. As 2021 was largely unaffected by geopolitical events nor extreme supply imbalances, I feel that it represents a suitable middle-of-the-road basis that should be utilized given the mixed outlook for their operating conditions.

The most obvious issue on the horizon is the uncertain outlook for oil prices during 2023 with competing views only making the job more difficult for investors. Whilst oil prices are never certain by nature, they are facing never-before-seen geopolitical implications from the Russia-Ukraine war that is quickly approaching the one-year mark. Apart from the continued loss of life, it also continues playing a role in moving oil prices, especially following the 5th of December 2022 European ban on seaborne oil from Russia. Initially, it appears the drop off in Russian exports should have a material benefit but until more time elapses, uncertainty prevails.

Whilst this sets a bullish tone for oil prices, central banks have been rapidly tightening monetary policy to fight inflation and thus as a result, many investors are worried about a recession. Even if not forthcoming, weaker economic conditions still appear more likely than not and thus, these obviously stand to weigh upon oil and gas prices, particularly the former. Ultimately, no one can necessarily tell exactly how these competing forces will intersect, although with OPEC managing their supply in the market, it reduces the risk of a severe downturn for oil companies, thereby making their 2021 results a suitable basis point that were neither too strong nor too weak. Plus, their capital expenditure is likely to remain steady and modest into 2023, as per the commentary from management included below.

“Finally, we understand that there’s a high level of interest in our 2023 capital and activity plans, which we will communicate on our next call once our plans are finalized and approved by the Board. As we formulate our plans for 2023, we will focus on retaining a high degree of flexibility in our capital and spending plans, allowing us to adapt and maximize opportunities in a changing macro environment as we do each year.”

– Occidental Petroleum Q3 2022 Conference Call.

Author

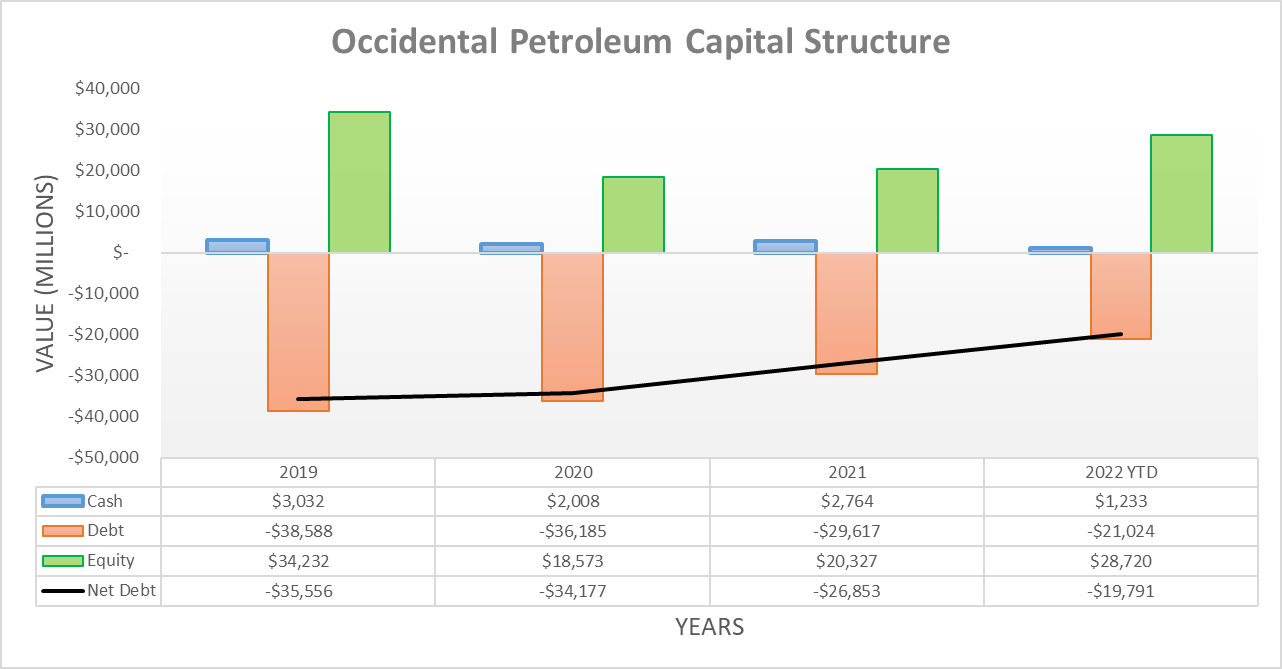

The third quarter of 2022 marked another period of deleveraging, as their net debt slides lower to $19.791b and thus down a little more than $1b versus its previous level of $20.84b following the second quarter. As for the recently ended fourth quarter, when its results land this should broadly continue, as oil and gas prices remained strong historically speaking, despite softening from earlier in the year. When looking ahead into 2023 and beyond, their net debt should progressively continue decreasing as the quarters and years roll past and future debt maturities arise, given their new relaxed deleveraging pace.

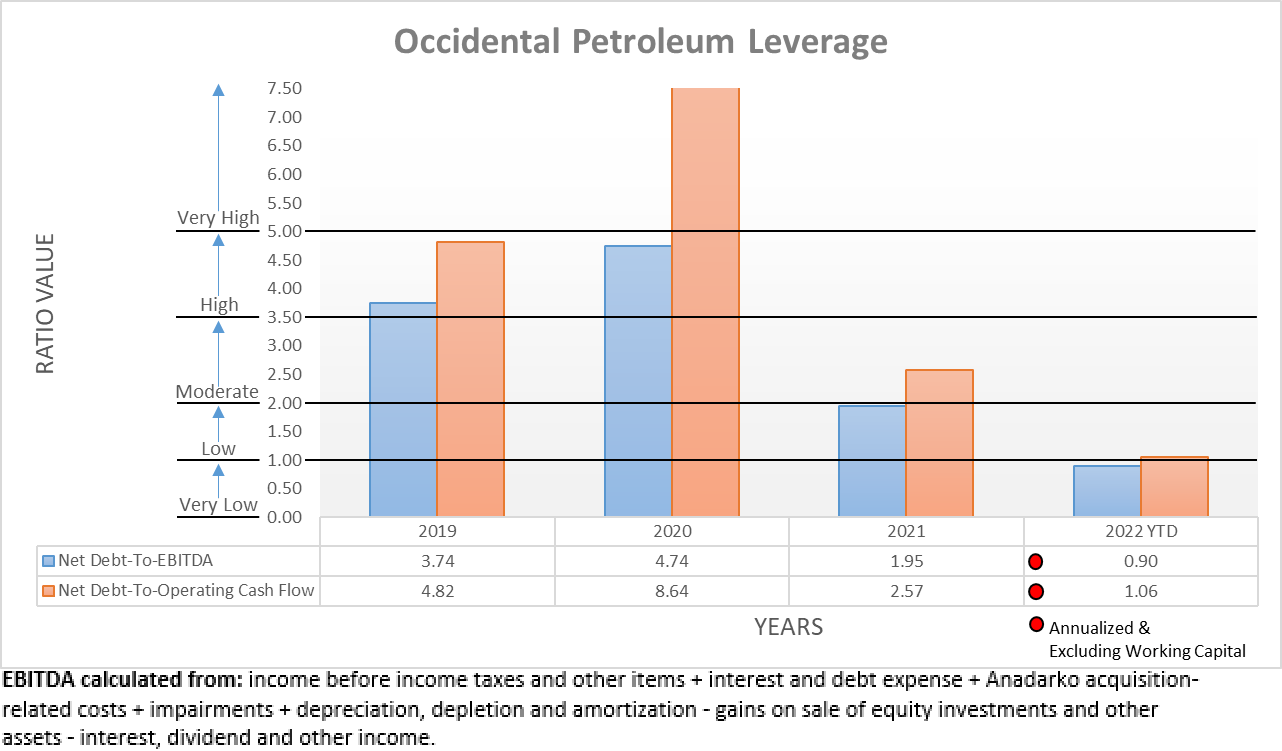

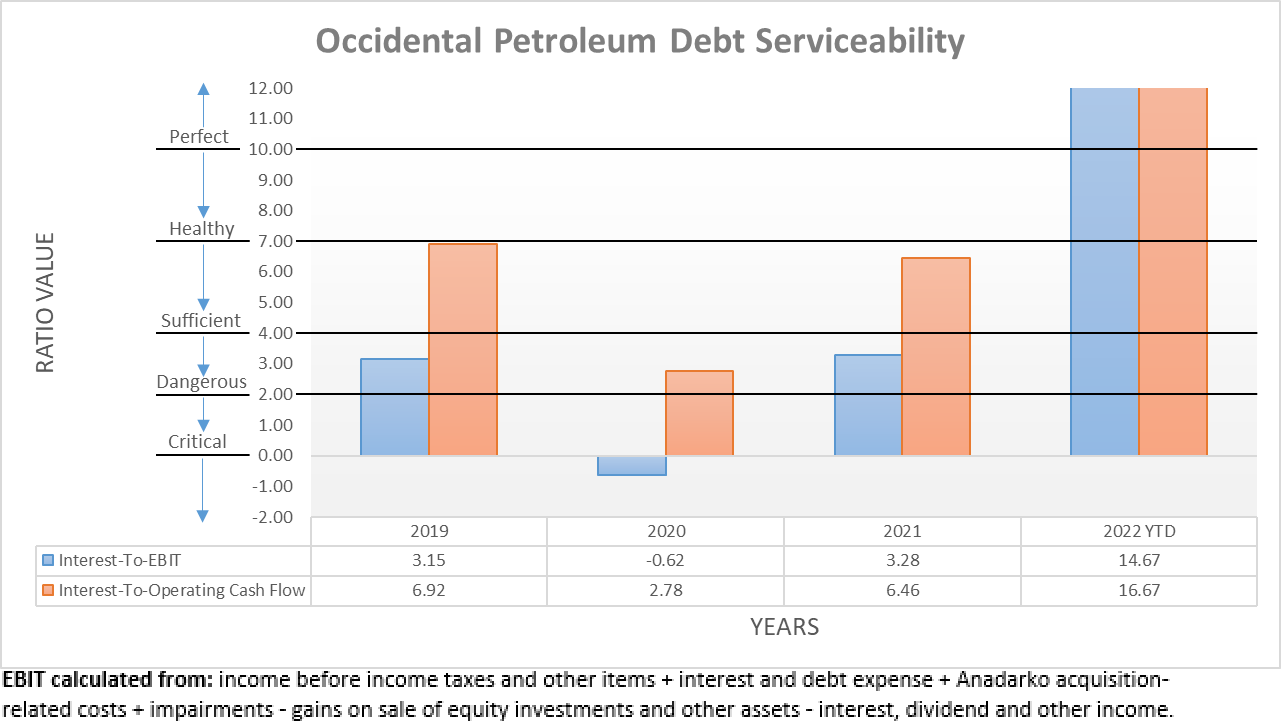

Since only one quarter has elapsed since the previous analysis and their net debt only saw a modest change, it would be redundant to reassess their leverage or debt serviceability in detail, especially since their outlook for 2023 was the far more important topic. That said, their subsequently discussed liquidity remains important because its associated debt maturity profile plays a role in determining their shareholder returns.

The two relevant graphs are still included below to provide context for any new readers, which on the first account show their leverage is once again very low with a net debt-to-EBITDA of 0.90. Whilst their accompanying net debt-to-operating cash flow of 1.06 is slightly above the applicable threshold of 1.00, it should fall beneath this point in the coming year as their net debt slides lower. On the second account, it also shows their debt serviceability is perfect with interest coverage of 14.67 when compared against their EBIT, or a similar 16.67 when compared against their operating cash flow. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

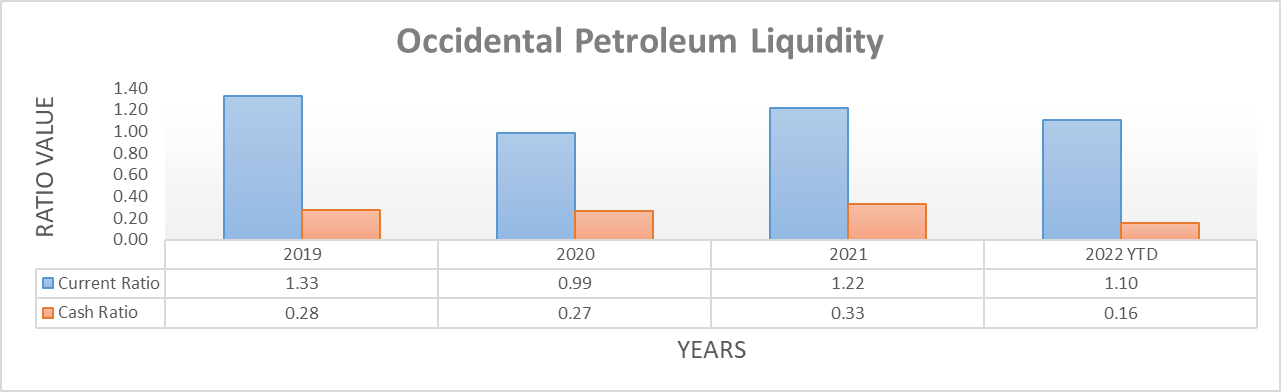

The third quarter of 2022 saw their liquidity track broadly sideways, which was not surprising nor negative. Both their respective current and cash ratios clocked small increases to 1.10 and 0.16 versus their previous respective results of 1.07 and 0.14 following the second quarter. Thanks to their immense free cash flow and now far healthier financial position, debt maturities and credit facility availability no longer pose a risk but at the same time, the former still influences their shareholder returns given their aforementioned excess cash flow.

Alas, they only release a breakdown of their debt maturity profile with their fourth-quarter results each year but thankfully, a reasonably accurate judgment can still be formed with other data provided. Their balance sheets following the third quarter of 2022 shows $546m of debt listed as a current liability, thereby meaning its maturity is within the next twelve months and thus during either the fourth quarter of 2022 or the first nine months of 2023. If looking back at their 2021 10-K that last provided their full debt structure, there were zero maturities during the fourth quarter of 2023.

Since they have been deleveraging and rapidly repaying debt since this was published, it stands to reason that no new debt was issued with such a short-term maturity or if so, it should only be immaterial. When wrapped together, this strongly implies there should be very few debt maturities during 2023 and thereby only represent a relatively modest factor given the volatility brought about due to oil and gas prices. As a result, their shareholders should see almost the entirety of their free cash flow returned in the year ahead, mostly via share buybacks.

Conclusion

After fighting to restore financial health, this new year sees a new era of maximized shareholder returns beginning given their move to a new relaxed pace of deleveraging. When combined with the very desirable value offered by their double-digit free cash flow yield, I suspect this will help support their share price, regardless of the economic risks and thus, I still believe that a strong buy rating is appropriate. If not for this double-digit free cash flow yield arising from their middle-of-the-road 2021 results, my rating would have been downgraded in light of the gloomy economic outlook.

Notes: Unless specified otherwise, all figures in this article were taken from Occidental Petroleum’s SEC filings, all calculated figures were performed by the author.

Be the first to comment