Editor’s note: Seeking Alpha is proud to welcome Nathaniel Petruska as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

imaginima

Occidental Petroleum (NYSE:OXY) is an American company engaged in international hydrocarbon exploration, petrochemical manufacturing, and building up low-carbon technologies. The stock is currently trading at a bargain and investors should up shares due to overwhelmingly positive macroeconomic factors that will surge oil prices in the long term providing higher profits for a business that is currently undervalued.

Business Model

OXY 10K, 2021

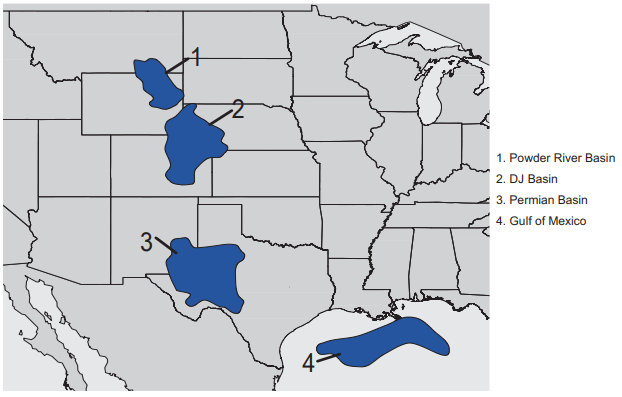

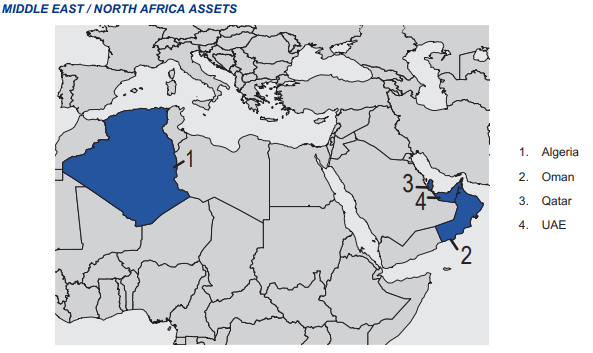

Occidental is an international energy company with assets primarily in the United States, the Middle East, and North Africa. They are one of the largest oil producers in the U.S., including a leading producer in the Permian and D.J. basins and the offshore Gulf of Mexico. Occidental’s principal businesses consist of three reporting segments: oil and gas, chemical and midstream, and marketing.

OXY 10K, 2021

Occidental primarily conducts its exploration and production activities in the United States, the Middle East, and North Africa. Within the U. S., Occidental operates in Texas, New Mexico, and Colorado and offshore in the Gulf of Mexico. Internationally, Occidental mostly operates in Oman, United Arab Emirates (UAE), and Algeria. Occidental’s competitive edge depends on sustaining production in a cost-efficient way through developing both conventional and unconventional fields and utilizing primary and enhanced oil recovery (EOR) methods in regions where Occidental has the advantage.

The above information was gathered from Occidental Petroleum’s annual filing.

Macro Environment

There are some powerful macroeconomic forces at play that paint a bullish picture for oil in the long term, which Occidental’s top line will directly benefit from. Many of these conditions have either already occurred, will most assuredly happen in the near future, or high probability that favors a bullish stance with little downside risk. Since commodities are volatile, picking an undervalued company that would generate increased revenues from this thesis is paramount. Occidental Petroleum is one of the most promising in this regard.

Ukraine-Russian Conflict

Many nations have committed to stopping or drastically reducing their oil and gas imports in the wake of Russia’s invasion of Ukraine. E.U. countries have stopped Russian oil shipments by sea, and refined oil products will no longer be imported starting in February 2023. Additionally, all imports of Russian oil have been halted in the U.S. By the end of this year, and the U.K. has committed to completely stopping all imports of Russian oil. A barrel of Russian crude oil cannot exceed $60 a barrel thanks to a ceiling on oil prices endorsed by Western allies, namely G7, Australia, and 27 E.U. counties. In March, the E.U. said that within a year, it would reduce its reliance on Russian gas imports by two-thirds. The U.K. had been importing limited amounts of Russian gas, but it has halted operations entirely. Prime Minister Alexander Novak replied that Russia wouldn’t sell oil to countries that adopt the price cap, predicting an oil-supply deficit as soon as this year. This has been restated as recently as last week when he reiterated Russia reducing their production by up to 700k barrels per day, which is about 7% of their daily output, by early next year.

Ukraine’s conflict has worsened the energy and cost of living crises in the E.U. Many European nations are anticipated to experience a recession throughout the winter due to rising inflation and significant tightening in monetary policy. The U.S. cannot meet the E.U.’s demand for higher oil imports, despite them exacerbating the situation by banning Russian oil at such a critical time.

American Government

The White House and U.S. oil businesses are at odds as several corporations make record profits from higher prices despite pumping less crude than before the COVID outbreak, leaving American consumers with skyrocketing fuel prices. Part of the problem is the conflict in Ukraine. President Biden has asked the U.S. oil industry to increase its output. However, the industry is hesitant, given this administration’s history of opposition to fossil fuels and the possibility that additional drilling won’t be profitable in the long run. With less investment in oil exploration, the American oil industry has most likely reached its production cap.

Since President Biden assumed office, the amount of oil in the Strategic Petroleum Reserve (SPR) has decreased by over a third. This caused the emergency oil stockpile to reach its lowest level since June 1984, when the U.S. economy and energy consumption were far less than they are now. According to a senior administration official, the Energy Department intends to acquire up to 3 million barrels of oil for the SPR that will be delivered in February. According to the official, the buyback would test a novel strategy for buying back the oil at a set price and acknowledged that filling the SPR would take months or years to refill to previous levels. Refilling the SPR would have two effects: no longer artificially suppressing oil prices and slowly pulling from the oil production that is already stretched thin, raising the price of oil. To showcase this, according to 2021 statistics, the U.S. continued to import crude oil and petroleum products from other nations to meet local demand for petroleum and to service global markets.

To add to this, U.S. oil production growth is slowing down. The shale revolution is no longer in the boom it once was and may never return to the levels we’ve seen. On the surface, U.S. output looks good; it has rebounded from a low of 9.7 million BPD (barrels per day) in May 2020 to 12.3 million BPD this September, with this year’s high still below the pre-pandemic record of 13 million BPD reached in late 2019. Moreover, oil production in the country has not continued to increase. Instead, it maintains its production peak showing no additional growth in its future.

OPEC+

OPEC+ cuts daily output by 2 million barrels a day. This amounts to approximately 2% of the world’s daily oil production. Combined, OPEC+ produces more than half of the world’s crude oil. Its two most significant producers in the organization, Russia and Saudi Arabia, have grown closer in recent years through this alliance. As of November 29, OPEC+ said it would not increase production and maintain its current trajectory. They want to support a healthy oil price, despite concerns about an oil supply shortage since the E.U. is cutting Russian oil. These moves show that OPEC+ will support higher crude prices. They will not let the levels drop too far, providing another bullish case for oil.

Several OPEC countries, including Saudi Arabia’s energy minister Prince Abdulaziz bin Salman, have raised the possibility of another output cut soon. Delegates from OPEC have stated that output targets may increase early next year. Oil prices may drop into the lower $60s due to worries about a worldwide recession and rising inflation rates. The alliance’s next meeting is scheduled for June 4, after which it will evaluate its productivity. However, OPEC declared that it was prepared “to meet at any time and take immediate additional measures to address market developments” if necessary.

China Lockdowns

China lockdowns appear to be easing due to protests that are occurring due to the Chinese ‘zero-COVID’ policy. China is stuck between a rock and a hard place; they do not have developed COVID-19 vaccines available for the public due to their refusal to use western medicine. Their economy has been locked down for most of 2022, which has allowed oil to breathe after its surge earlier this year. Analysts determined that travel has been down approximately 67% for most of the year compared to 2019. Now, when China inevitably agrees to loosen its policy and allow its economy to function normally, possibly even allowing its people to utilize western medicines, oil prices will see a drastic price hike. This has been estimated to boost global oil consumption by more than 1 million BPD. In the near term, China will go through a wave of infections, hurting short-term oil consumption. These issues should abate by late 2023, causing a sharp J-curve in oil prices.

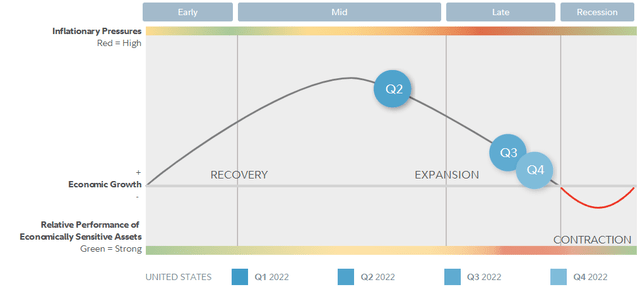

Economic Cycle

Economic Cycle, Fidelity

Supply chain issues have been getting a lot better in 2022, which has caused an oversupply and overordering for retailers. Typically, in late economic cycles, there is an oversupply of goods with less demand. Commodity prices have continued to be elevated, as is typical in this phase; however, demand destruction usually takes care of this issue when the recession hits. Even though this is seen with the recent fall in oil prices, this specific situation for oil is an outlier to typical expectations.

Elevated inflation rates will continue for years to come. Even though they have seemed to reverse course, 7.1% CPI is not acceptable for long-term economic well-being. The longer inflation is elevated above the 2% FED target, the more entrenched it will be and the more challenging it will be to correct. With this problem comes the strength of investing in commodities during inflationary periods. Even if inflation does not remain at current levels, it will be entrenched for years. Any increased inflation above the 2% target rate supports businesses that make a living on commodities, making OXY a perfect inflation hedge.

Management Team

When doing company evaluations, it’s essential to consider the management team running the company an investor is interested in. Vicki Hollub has been the CEO since April 2016, specifically chosen based on her “strong track record of successfully growing our domestic oil and gas business profitably and efficiently,” stated the previous CEO. A published Forbes article wrote that in the past, the CEO’s focus on high-producing oil fields had made the company more focused and “poised to gusher cash for the next half-century.”

All the other leadership bios from Occidental’s team can be read here.

Hollub has been very adamant about acting in the shareholder’s best interests. She is aggressively paying off debt and returning profits back to shareholders. Through share buybacks and dividends. The company will be able to accelerate share buybacks in 2023, which would spur pay downs in its preferred shares, analysts at J.P. Morgan stated. This is a significant priority for the management team. They also want to reduce their gross debt to $15 billion to normalize their balance sheet after buying Anadarko Petroleum in 2019.

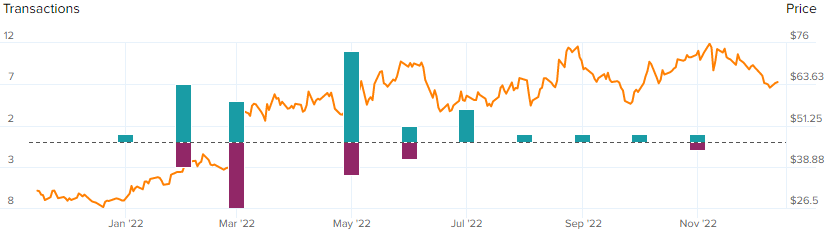

Insider Actions

TipRanks/OXY

In addition to the CEO acting in shareholders’ best interests, analyzing insider transactions is another important part of building investors’ trust in the company. The insider transactions of the leadership within the company have been positive throughout this year showing that they believe the company will experience growth in the future and the current share price, indicated by the orange line, is currently undervalued.

Valuation

Author’s calculations

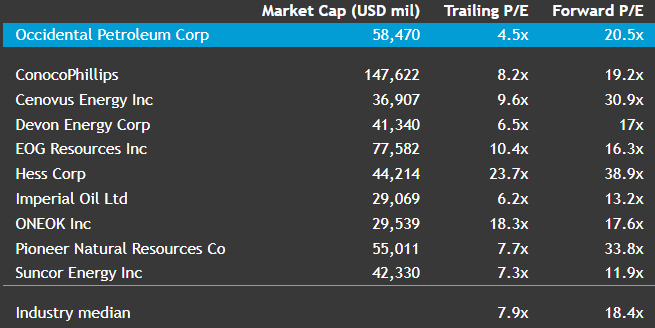

The above is the worst-case valuation utilizing a DCF model, still yielding 13% annual growth. Assumptions for this valuation include EPS staying around the same TTM value of $9.95 with an annualized growth rate of 11%, a discount rate of 10%, and a margin of safety of 10%. Instead of using the risk-free discount rate, I chose 10% because as individual investors we shoot to beat the S&P returns if we want to invest in individual companies. The discount rate of 10% reflects the stability of the projected cashflows, especially taking into account the macro factors. You would be hard-pressed to find a company like this with a deeper margin of safety, even if it is preferable. The PE ratio used in this model is 6.95, but in reality, the PE ratio should be closer to 10 since these are multi-year lows, and the average PE of the industry is about 3.5x higher than that. If compared to the industry mean for forward PE, shown in the chart to the lower right, 10 is very conservative.

valueinvesting.io/OXY

Even if PE only reached 10 over the next 5 years, that would yield a beautiful CAGR of 22% to the shareholder. On the more optimistic end of the spectrum, the investor can assume a 20% growth rate, yielding a 31% return rate each year. This seems aggressive, but over the last 3 years, revenue has grown by 27% annually, shown in the chart below. Maybe this is due to 2020 being a massive low for oil to 2022 being a massive growth per barrel price. Since 2018, Occidental has averaged an 11% annualized growth in revenue, even though this considers pre-Anadarko revenue. The chart to the right has Occidental’s peers listed with their forward PE of 10, showing this consideration is still very conservative.

GuruFocus/OXY

Technical Analysis

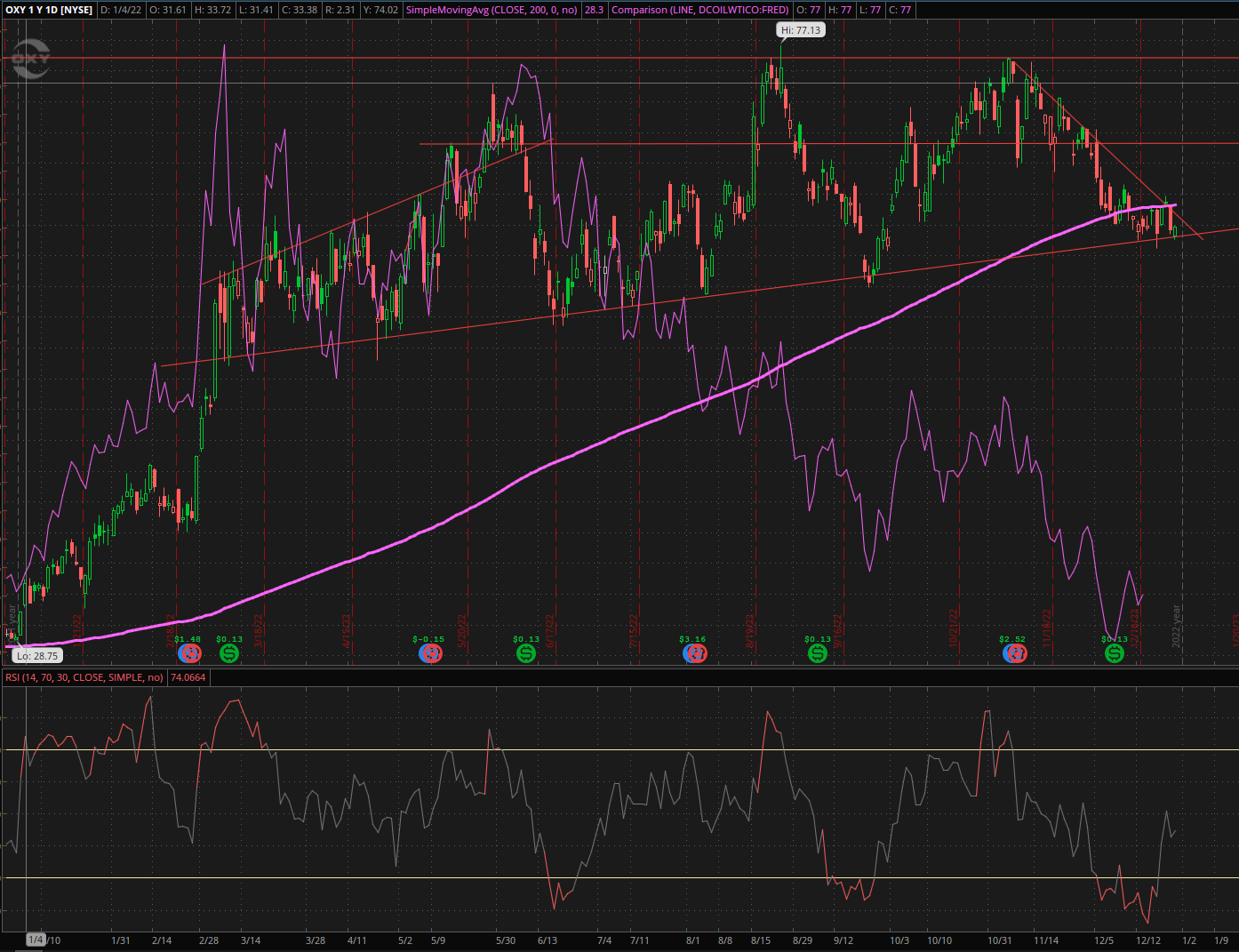

Based on historical trends, I believe it would be a great time to load up on shares now for the ride-up retesting $75 again, where investors can reduce their exposure. The floor has been maintained this past year, and while comparing the thin purple line (WTI prices) with how it reacted to prices in the past, OXY looks ready to take off with any oil price increases. Compared to the WTI prices, it has held up well even with the recent oil price reductions. If there is another gain like earlier this year, it would easily blow through the $75 cap that has been held throughout 2022.

Author’s calculations

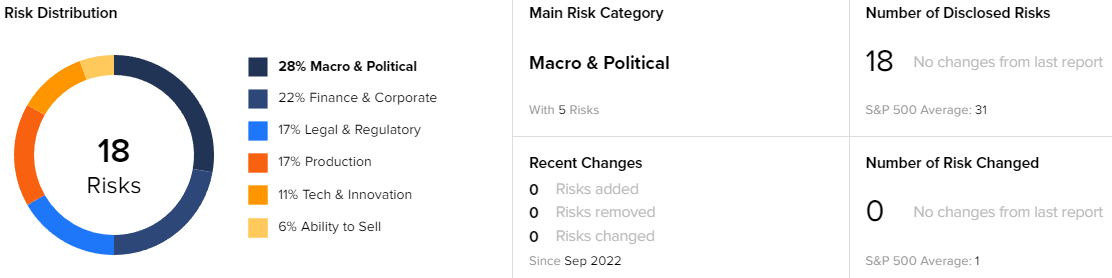

Risks

TipRanks/OXY

Overall, these are the risks investors should be aware of:

- The actions of the government and any political unrest may have an impact on Occidental’s business outcomes.

- Changes in regulations related to greenhouse gas emissions and other air pollutants, as well as the overall impact of climate change, may negatively affect Occidental’s operations or results.

- Fluctuations in global and local commodity prices can significantly impact Occidental’s business outcomes.

- Occidental’s high debt levels may make it more susceptible to economic challenges and negative developments in its industry. Any declines in Occidental’s credit ratings or increases in interest rates may also negatively affect its access to capital and the cost of borrowing.

Occidental’s results are sensitive to oil, NGL, and natural gas price fluctuations. Price changes at current global prices and production levels affect Occidental’s budgeted 2022 annual pre-tax income by approximately $200 million for a $1 per barrel change in oil prices and roughly $30 million for a $1 per barrel shift in NGL prices. If domestic natural gas prices vary by $0.10 per Mcf, it would have an estimated annual effect on Occidental’s budgeted 2022 pre-tax income of approximately $40 million. It is important to note that Occidental will continue to be profitable while the price per barrel of oil is over $40. Therefore, even if oil prices decline significantly from their current prices, the company’s oil and gas division will continue to profit.

One major fundamental risk Occidental has is its working capital turnover. So for every dollar of working capital, OXY produces $44.63 in revenue. Let’s look at OXY’s peers: ConocoPhillips (COP) is 11.63, Exxon Mobil (XOM) is 2, and VAALCO Energy (EGY) is 2.07. So relatively, 44.63 is extremely high, which might mean it doesn’t have enough capital available to support its sales growth. It could also be that the accounts payable are too high and OXY is struggling to pay them as they are due. Keep in mind, from mid-2020 until mid-2022 this metric has increased quarter over quarter, but in September it decreased substantially. Accounts payable must be observed as we head into the future to ensure nothing more serious is happening.

Conclusion

Overall, considering the macroeconomic factors, oil will be a very profitable play for long-term value investors. Instead of directly investing in the commodities, a more beneficial plan would be to utilize a company that generates profits that are currently undervalued based on the expected returns an investor wants to achieve. Occidental Petroleum fits these needs and purchasing the stock at current prices should have tremendous upside if investors have a 5- to 10-year horizon.

Be the first to comment