Brandon Bell

Article Thesis

Around half a year ago, I wrote an article in which I argued that Occidental Petroleum (NYSE:OXY) was not a great investment, despite the bullish environment for oil companies. Other energy companies offered a way better setup, thanks to lower valuations and better balance sheets, which, in turn, allowed for larger shareholder return programs. In this article, we’ll look back at how this thesis has played out so far, and we will take a look at what the future might hold for Occidental Petroleum.

Occidental Petroleum: Getting Left In The Dust

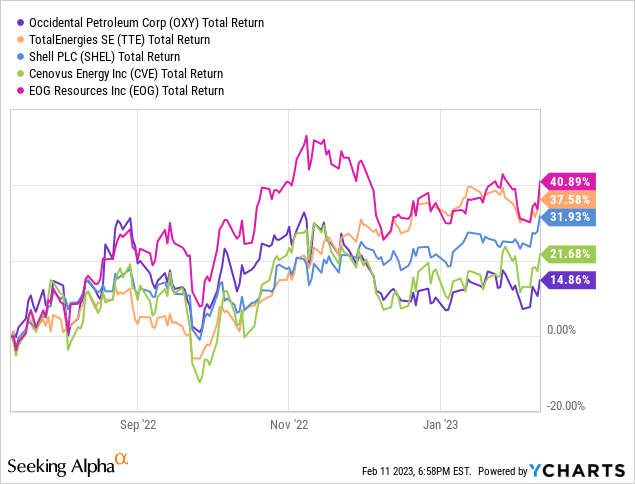

Last July, I wrote an article in which I argued that investors shouldn’t buy into Occidental Petroleum and that they should opt for better and cheaper energy stocks instead. I argued that TotalEnergies (TTE), Shell (SHEL), Cenovus Energy (CVE), and EOG Resources (EOG) would be stronger investments going forward.

So far, this thesis has played out very well:

While Occidental Petroleum’s 15% return over the last 7 months is pretty strong, the other four energy companies easily delivered better returns — the average total return over that time frame was 33% or more than twice the return that OXY has delivered so far.

There are good reasons for the outperformance of these companies versus OXY over the last seven months, mainly OXY’s too-high valuation (on a relative basis in summer 2022), its too-weak balance sheet, and its limited shareholder return potential since high debt levels forced OXY to prioritize debt reduction while that was not true for energy companies with cleaner balance sheets. Of course, things change over time, so let’s revisit OXY in order to determine whether things will likely go on in the same manner going forward, or whether OXY has a good chance of performing better on a relative basis.

OXY’s Recent Performance

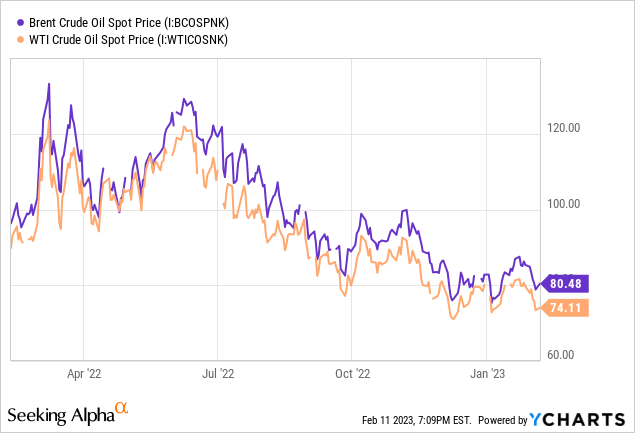

Occidental Petroleum reported its most recent quarterly results in November. During the third quarter, Occidental Petroleum naturally was able to grow its revenue, as higher average oil prices boosted its sales considerably. Average WTI and Brent prices stood at $92 during the third quarter, which is higher than the average during the fourth quarter and the average, so far, in 2023:

Crude oil prices headed downwards during the fourth quarter, and have averaged around $80 so far in 2023. While that is lower than the prices seen in 2022, crude oil prices of around $80 per barrel are still far from low in absolute terms, and generally make for a still pretty solid environment for energy companies. It is not possible to forecast precisely what oil prices might look like during the remainder of the year and beyond, but there are some factors that could result in an increase in oil prices. Right now, the market fears about a recession, which is why commodities including crude oil have headed lower in recent months. If a recession does not occur, those declines could reverse, I believe. China’s economic reopening should also be positive for crude oil prices, as additional demand is added due to more driving and flying activity in China. Last but not least, sanctions on Russia could result in lower output in the country, as Western tech and parts are not available any longer, which could increasingly lead to maintenance issues that result in lower production levels.

While Q4 and Q1 thus do look like they will be weaker than what Q3 looked like, for OXY and for other energy companies, the remainder of 2023 might be stronger again — but that’s not guaranteed, of course.

Occidental Petroleum generated operating cash flows of $4.3 billion during the third quarter, which resulted in free cash flows of $3.2 billion after accounting for $1.1 billion in capital expenditures. Occidental Petroleum’s reinvestment rate of just 26% is pretty low compared to other energy companies — depending on how one wants to interpret this, it could be a good sign or a bad sign. One could argue it’s good, as the company is focusing on the best investment opportunities while not chasing broad-based growth. But one could also argue that OXY is investing too little as it is forced to maximize free cash flows in order to pay down its massive debt load. I personally lean towards the first interpretation, seeing a high free cash flow conversion rate as a positive thing, but investors should keep an eye on production levels as low investment rates might lead to some declines going forward. A $3.2 billion quarterly free cash flow resulted in an annualized free cash flow of $12.8 billion — for a company that is currently valued at $59 billion, that’s pretty strong. When we look at OXY’s free cash flow relative to its enterprise value, which accounts for its above-average debt levels, the result is not as great, however.

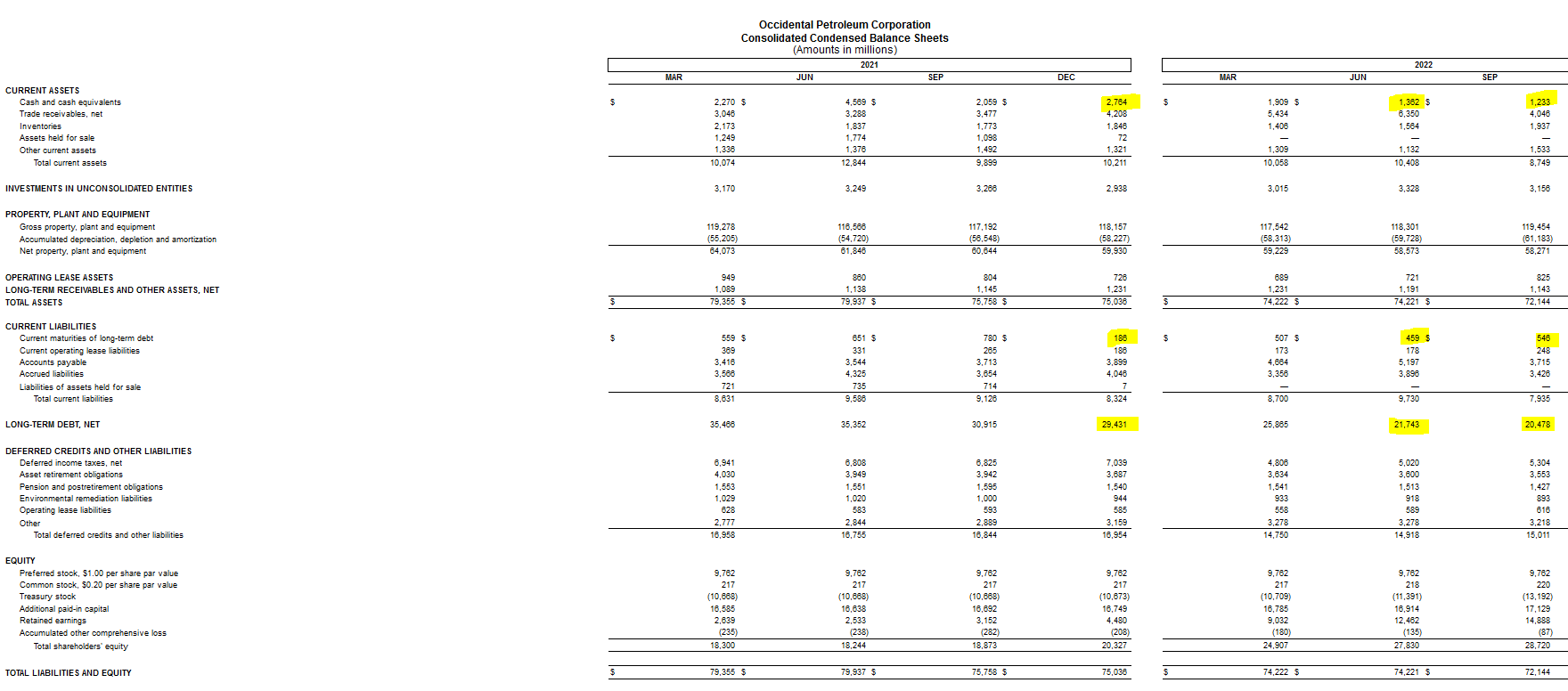

Not surprisingly, Occidental Petroleum focused on bringing down debt levels when it came to utilizing its free cash flows. The company’s filing shows its balance sheet movements over the last quarter and the last year:

OXY filing

At the end of fiscal 2021, Occidental Petroleum’s net debt totaled $26.8 billion. At the end of the second quarter of 2022, OXY’s net debt totaled $20.8 billion, while OXY’s net debt at the end of the most recent quarter totaled $19.8 billion. Occidental Petroleum has thus lowered its net debt position by $7 billion over the first three quarters of 2022, which is solid progress — but on the other hand, the net debt position still remains rather elevated, at more than 1.5x its annualized free cash flow (looking at the Q3 numbers).

High debt levels are an issue due to several reasons. First, they make a company less flexible when it comes to capital allocation — highly indebted companies have to focus on debt reduction, no matter what. Second, high debt levels pose a risk in tough times, e.g. if oil prices pull back and profits wane. Third, high debt levels lead to significant additional interest costs in a rising rates environment — more or less debt-free peers such as EOG (its net debt is equal to just 0.02x its net profit) don’t have to worry about rising rates.

While OXY has made progress in cleaning up its balance sheet, its balance sheet is still far from strong. I believe that this could remain a headwind going forward, especially if the Fed continues to increase interest rates. Eventually, those interest rate increases will impact Occidental Petroleum, as it will be forced to refinance some of its debt at higher rates, all else equal, which will lead to higher interest expenses and thus lower profits and cash flows.

Valuation Update

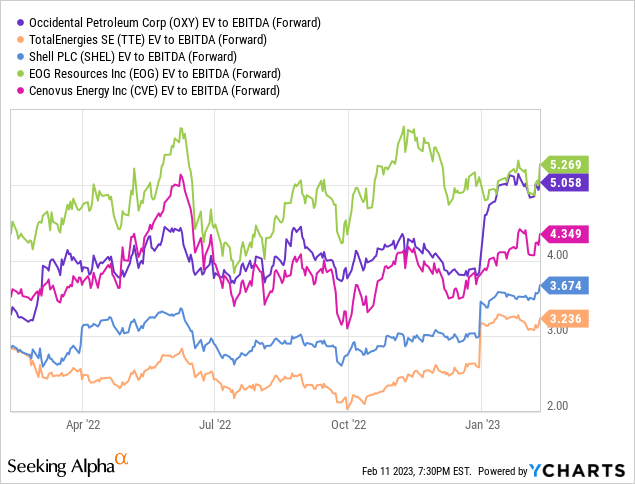

One of my original arguments for avoiding Occidental Petroleum and going with TTE, SHEL, EOG, and CVE instead, was the fact that OXY was quite pricy on a relative basis. The recent underperformance has changed that, at least to some degree:

Note: I use EV to EBITDA as it accounts for differences in net debt usage between individual companies, while that is not true when one looks at market capitalization only.

While OXY was the most expensive among these five energy companies half a year ago, it is not the second-most expensive. One could argue that OXY is more attractive than EOG today. But on the other hand, Cenovus Energy, Shell, and TotalEnergies are still far cheaper than OXY — despite their recent massive outperformance versus OXY. I thus continue to believe that OXY is not especially attractive valuation-wise. I wouldn’t be surprised to see TTE, SHEL, and CVE outperform OXY going forward, too, as they have done over the last half year.

The Buffett Factor

One of the reasons that made OXY perform well in early 2022 was the fact that Buffett’s Berkshire Hathaway (BRK.A)(BRK.B) bought Occidental Petroleum repeatedly. There was some buying by Buffett during the third quarter, but we haven’t heard anything since then. The outright takeover bid for the company that some OXY bulls have speculated on has also not materialized so far — and with Buffett being heavily into Chevron (CVX) in the recent past, it does not look like he is overly interested in buying all of Occidental Petroleum. Still, I could see the fact that Buffett bought into OXY and continues to own shares as a positive for the stock going forward. While it will likely not result in a rising stock price by itself, the Buffett factor could protect OXY’s shares on the downside, as shareholders could be more inclined to hold onto shares during a sell-off knowing that they are investing alongside Buffett’s Berkshire Hathaway. Over the last half year or so, OXY has traded in a relatively tight range around the mid-$60s — the “Buffett factor” might be part of the explanation. I thus would not be surprised to see OXY remain relatively stable even if oil prices pull back, at least unless Berkshire Hathaway starts to sell its position.

Takeaway

OXY has its fans, but balance sheet strength, shareholder return potential, and valuation matter. It is thus, I believe, not surprising to see that the energy companies that were better-positioned half a year ago have easily outperformed OXY. While OXY’s relative valuation has improved slightly, and while its balance sheet has gotten a little stronger, I continue to believe that other energy companies are better positioned from a valuation and fundamental perspective. I thus would not be surprised if OXY continues to underperform the “better” energy companies I had identified.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment