Jan/iStock via Getty Images

Introduction

The NWF Group (OTCPK:NWFFF) is a UK-based fuel distributor and animal feed manufacturer and distributor, while its third division, Food, takes care of storage and distribution of third party goods. The company is currently trading at 7 times free cash flow while its balance sheet contains a net cash position which is used to pursue accretive M&A. NWF currently pays a 3% dividend yield, using a 20% payout ratio.

Yahoo Finance

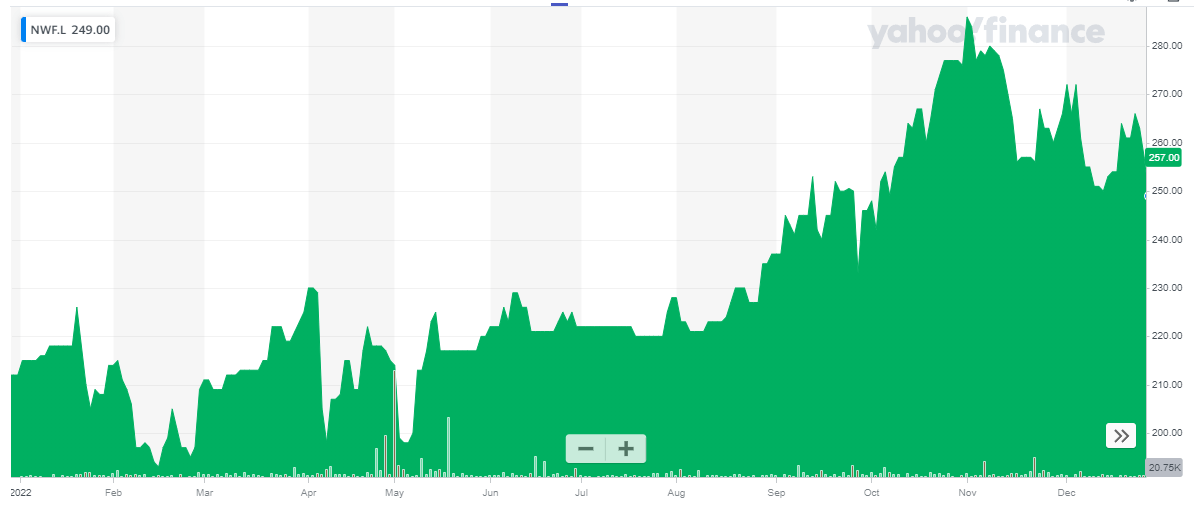

NWF’s primary listing is on the London Stock Exchange where it’s trading with NWF as its ticker symbol. The average daily volume in London is just over 40,000 shares per day for a total dollar volume of approximately US$125,000 per day.

Unfortunately NWF’s website contains a few download-only links, but you can find all relevant financial information and documentation here.

A background story of the company and its recent FY 2022 results

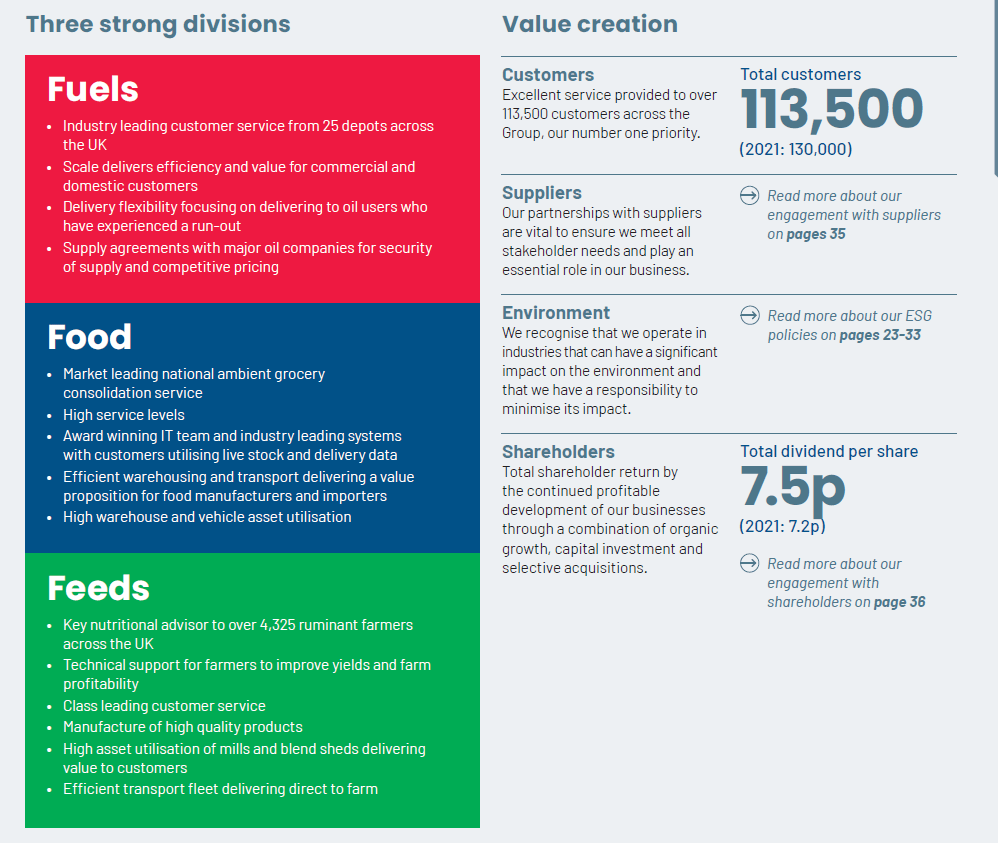

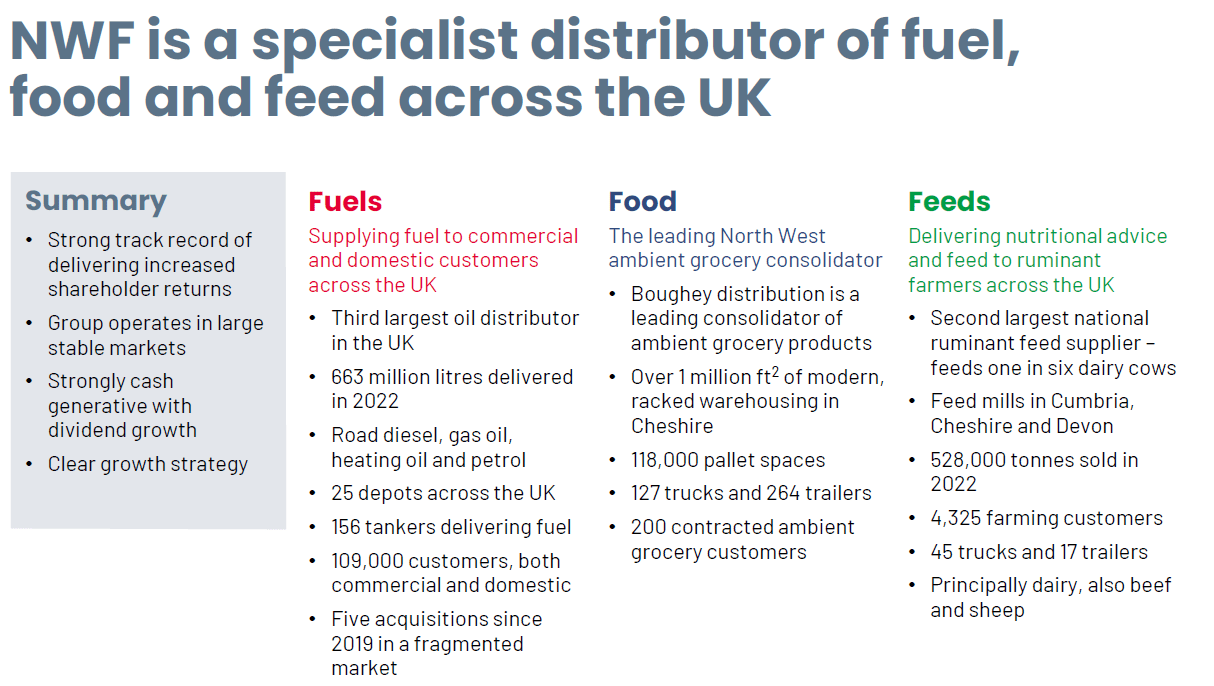

NWF Group offers exposure to fuel and food storage and distribution in the United Kingdom. The company serves in excess of 100,000 customers from its empire of 25 fuel depots (and increasing) and in the most recently completed financial year (FY 2022, which ended in May), about 663 million liters of fuel were distributed. This division generated an operating profit of 17.2M GBP on a revenue of 621M GBP.

NWF Group Investor Relations

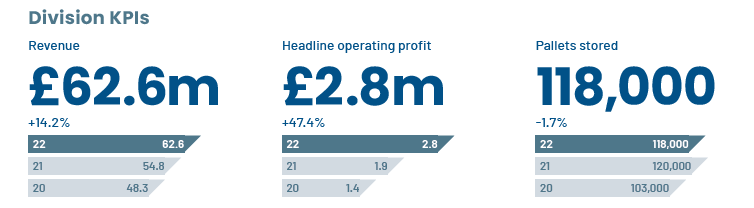

The food division is interesting. NWF does not produce food but rather provides storage for third parties and with its 264 trailers, it also plays a role in the distribution of those stored goods to their final destination. The warehouses can store a total of 135,000 pallets and the occupancy ratios have been consistently close to 90% in the past few years. This division generated a total revenue of just under 63M GBP in FY 2022, and this resulted in an operating profit of 2.8M GBP. The margins are indeed pretty low as well but NWF is getting better at expanding its margins. On a YoY comparison, the operating profit increased by 47% while the revenue increased by just 14%. And compared to FY 2020, the revenue increased by 50% while the operating profit has doubled. So there clearly is some progress.

NWF Group Investor Relations

The third division is the animal feed division. The total revenue there was almost 200M GBP but the margins are razor-thin there with an operating profit of just 1.8M GBP which means the operating margin is less than 1%.

NWF Group Investor Relations

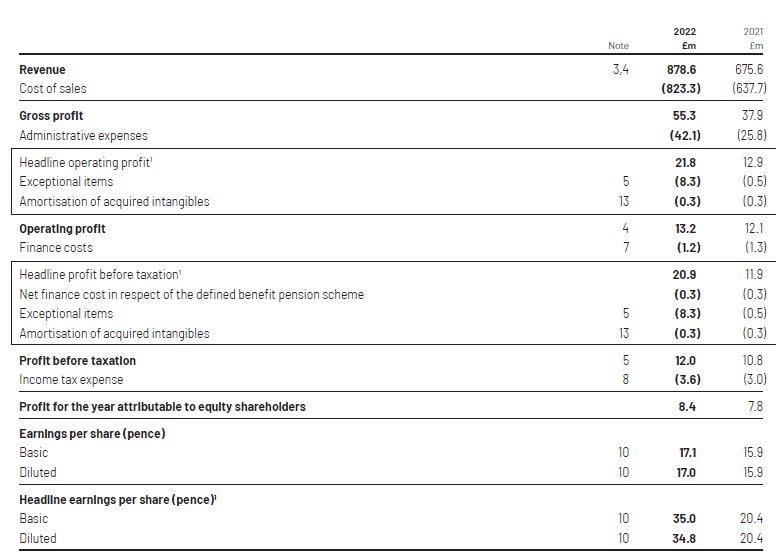

During FY 2022, the total revenue generated by NWF was almost 879M GBP which resulted in a 50% increase in the gross profit. As the administrative expenses increased as well and as there were a bunch of exceptional items recorded during the year, the reported operating profit was just 13.2M GBP, an increase of less than 10% compared to the previous financial year. However, as you can see below, the adjusted operating profit was 21.8M GBP, an increase of almost 70% compared to the previous financial year.

NWF Group Investor Relations

The reported net income was just 8.4M GBP for an EPS of 17.1 pence per share but the underlying EPS was actually 35 pence, an increase of almost 75% compared to the previous financial year.

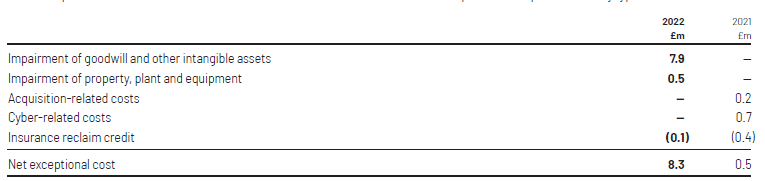

It’s quite interesting to note that virtually the entire ‘exceptional item’ cost was related to impairment charges. As you can see below, the total impairment charges were 8.4M GBP, partially offset by a 0.1M GBP insurance claim credit.

NWF Group Investor Relations

This means the free cash flow result should be more in line with the normalized net income (excluding the exceptional items).

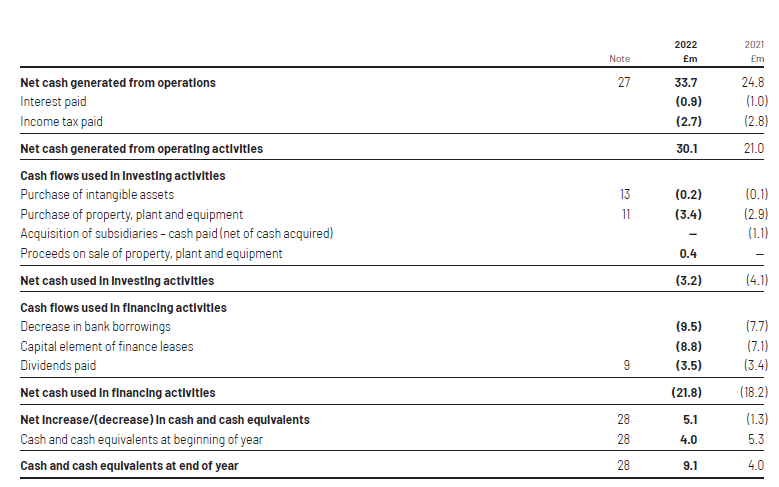

The company reported a “net cash generated from operating activities” of 30.1M GBP, but I wanted to dig deeper into where the starting point of 33.7M GBP was actually coming from.

NWF Group Investor Relations

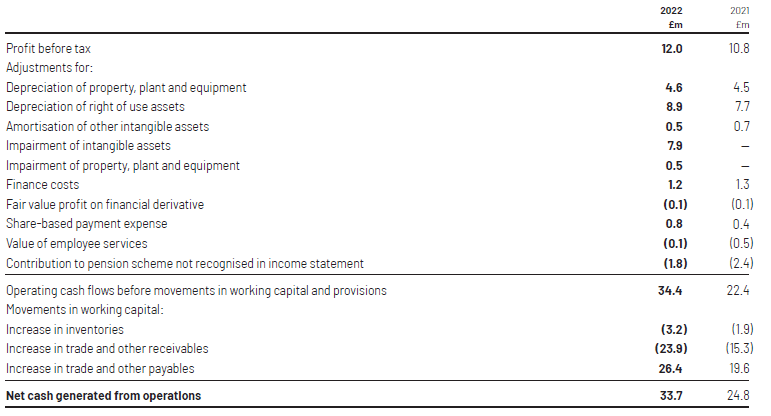

Fortunately the footnotes to the financial statements provide a good breakdown. We see the total operating cash flow before changes in the working capital position but after taking the 1.8M GBP pension payments into account was actually 34.4M GBP. This means the total adjusted operating cash flow wasn’t 30.1M GBP (as shown above), but 30.8M GBP.

NWF Group Investor Relations

The difference is small enough to not have a noticeable impact but I like to work with numbers that are adjusted for working capital changes. The company also had to pay 8.8M GBP in lease payments which means the adjusted operating cash flow was 22M GBP.

The total capex was 3.6M GBP (including 0.2M GBP spent on the investment in intangibles) which means the underlying free cash flow was approximately 18.4M GBP. Considering there are 49.1M shares outstanding, the underlying free cash flow result per share was approximately 37.5 pence per share. That’s even slightly higher than the underlying net income per share of 35 pence, mainly because the total capex of 3.6M GBP was approximately 1M GBP lower than the depreciation and amortization expenses.

NWF Group will pay a dividend of 7.5 pence per share which will cost the company about 3.7M GBP. This means the payout ratio is just around 20% and 80% of the cash is retained within the company and will be used for further M&A opportunities.

As of the end of September, NWF was running a very clean balance sheet. There was approximately 9.1M GBP in cash and no debt, which means that the company had about 18 pence per share in net cash.

What can we expect going forward?

In a recent trading update, the company sounded pretty upbeat. In its first semester (which ended on Nov. 30, so we should see detailed financial results within the next month or so), trading “has been strong” and in the fuels division the stronger margins have been sufficient to offset lower volumes. While the fall weather was pretty nice in the UK, resulting in a lower demand for heating oil, Europe experienced a cold snap in December so I would expect NWF to have had a good start of the second semester.

In the food division, NWF mentioned trading remained strong as well, while storage capacity utilization was described as “good” and the demand “has been stable.”

M&A also remains an important element in NWF’s growth strategy. Earlier in the current financial year, NWF acquired Sweetfuels limited for 10M GBP in cash. Sweetfuels is a fuel distributor with about 20 million liters of fuel being sold on an annual basis. The company’s EBITDA in the most recent financial year (2021) was 1.3M GBP so if NWF indeed paid just under 8 times the EBITDA (before any potential synergy benefits), the acquisition appears to be pretty decent.

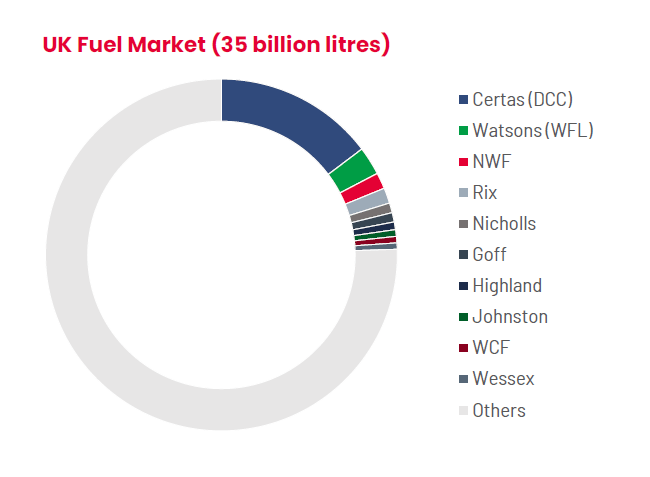

The fuel distribution market still is very fragmented in the UK (see below) and NWF is undoubtedly continuing its quest for bolt-on acquisitions to further expand its reach and perhaps unlock synergy benefits. And despite this acquisition, NWF will likely still have a positive net cash position as of the end of its first semester.

NWF Group Investor Relations

Investment thesis

With a current market capitalization of just under 125M GBP and an enterprise value of approximately 115M GBP, NWF is trading at just 4.5 times its EBITDA (excluding leases). Including lease liabilities, the EV/EBITDA would be even lower as the total amount of lease liabilities (just under 30M GBP) represents just about 3.5 times the annual lease payments.

While the sectors NWF is active in aren’t the easiest, I admire the company’s focus on free cash flow and strengthening its position by completing attractive bolt-on acquisitions. Even if we would use a multiple of 5.5 times the EBITDA of 28M GBP (including the Sweetfuels contribution) and assume the year-end net cash will remain unchanged at approximately 10M GBP, the stock should be valued at 335 pence per share versus the 249 pence it is currently trading at. And for every 0.5 you would add to that multiple, the fair value would increase by 28 pence per share.

I currently have no position in NWF but I may initiate a small speculative position before the H1 results are published.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment