Justin Sullivan

I was adamant about Nvidia (NASDAQ:NVDA) being grossly overbought towards the end of the bull market last year. Nvidia was one of the primary examples I used to outline how overvalued the market was in November 2021 in my “Epic Drop Is Coming” article. Remarkably, Nvidia had a market cap of around $800 billion and was trading at approximately 100 times TTM earnings and roughly 40 times TTM sales. However, now that the stock is down by nearly 70% from its highs, Nvidia looks much more attractive. The chip giant is going through a challenging period and experiencing an earnings decline.

However, Nvidia is primarily facing transitory issues that should not impact the company’s long-term revenue growth and earnings potential. The company’s gaming segment should rebound after the economic slowdown, enabling gaming revenues to recover and grow again. Moreover, Nvidia’s data center business continues to boom, and the company has promising AI, automotive, and other secondary segments. Nvidia’s drop has been epic, and the stock is significantly cheaper than it’s been in a long time. With its stock price heading for $100, Nvidia is closing in on a 20 times forward earnings valuation, making the stock a solid intermediate to long-term buy around current levels.

Nvidia’s Technical Blueprint

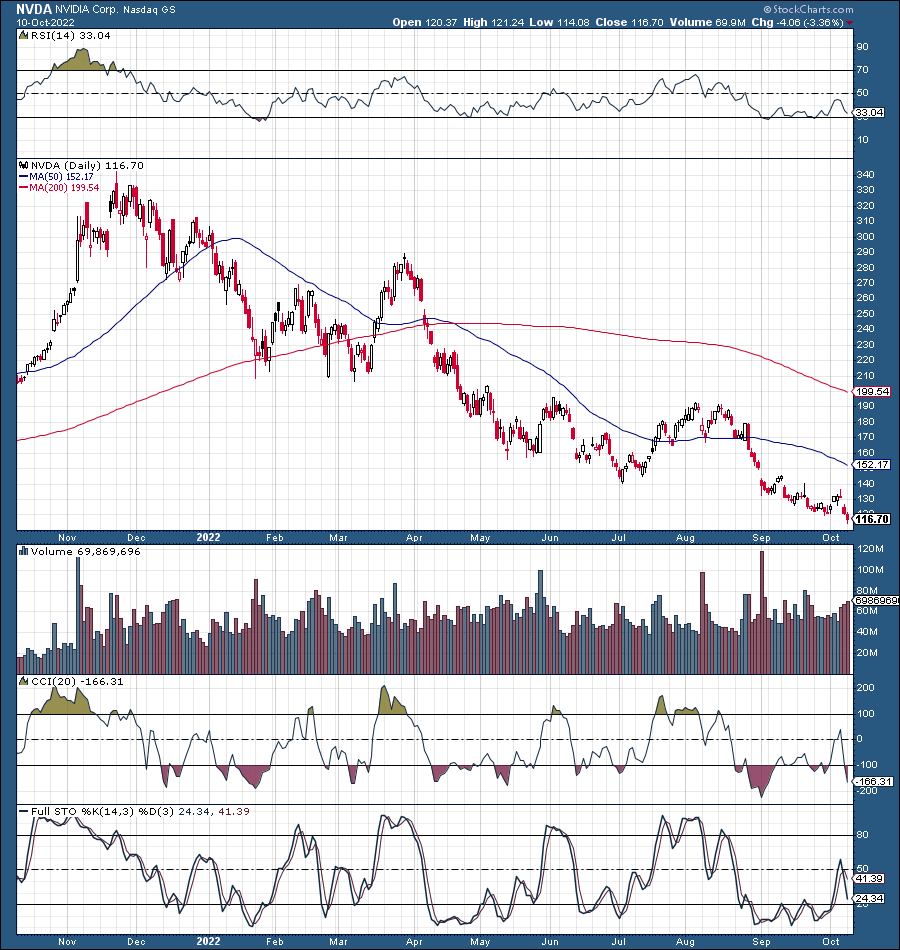

1-Year Chart

NVDA (StockCharts.com)

We see Nvidia’s blowoff top last November, and the stock still has not found a bottom nearly a year later. I’ve mentioned the $100-120 range as an attractive buy-in zone in prior analyses. With the stock at around $115, I still think this level is a good buy-in point. While Nvidia could temporarily drop below $100, the stock will not likely remain below par for long. We see the RSI bouncing around 30 here, illustrating oversold market conditions. While the bottom has not been confirmed yet, it may be close, and this may be an appropriate point to begin accumulating Nvidia shares now.

What Separates Nvidia From Others

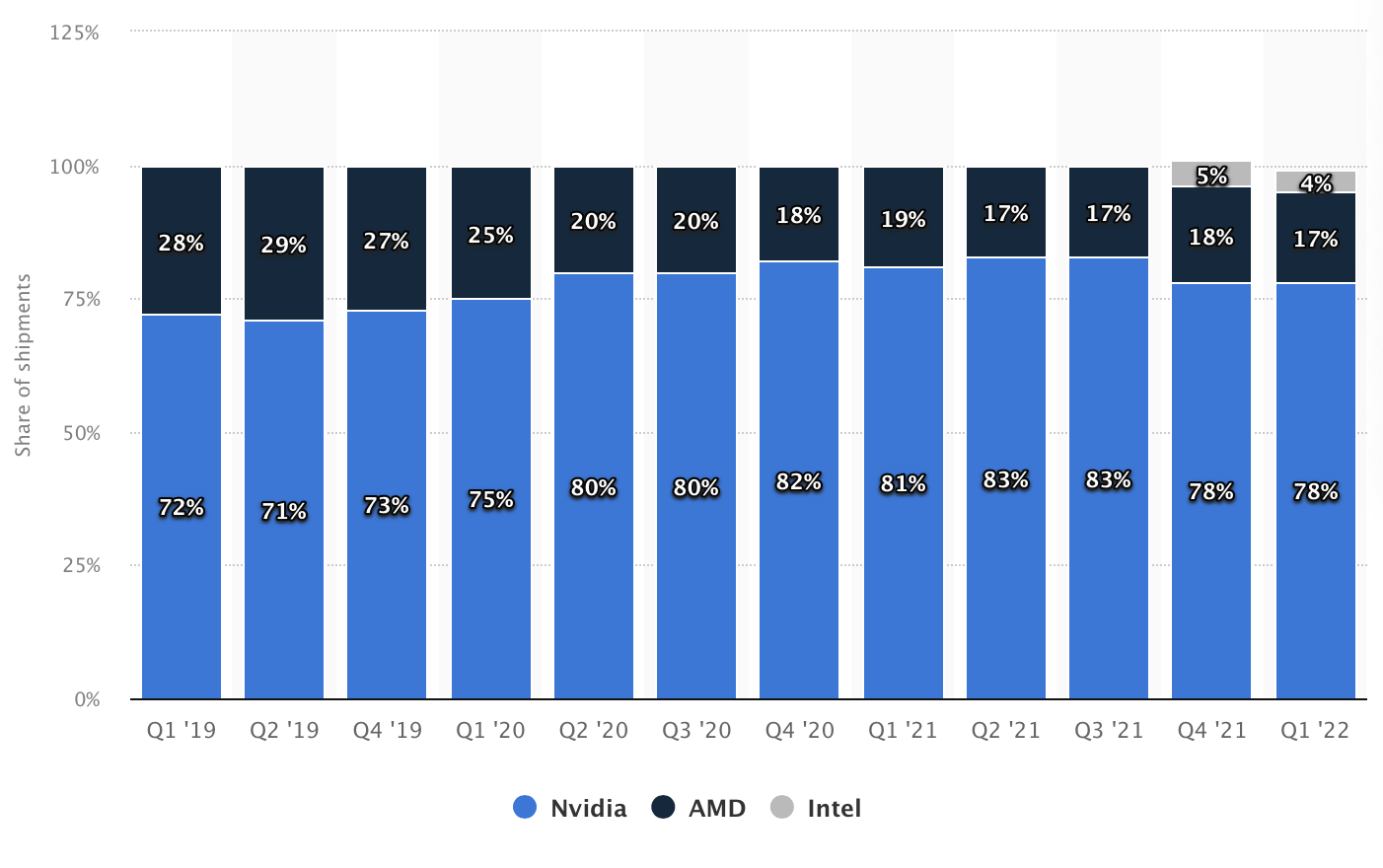

While Advanced Micro Devices (AMD) makes excellent graphics cards, the top discrete GPU maker is Nvidia. AMD’s GPUs may be more affordable, but many gamers still prefer Nvidia to power the heart of their PC.

Discrete GPU Market

Discrete GPU market (Statista.com)

Nvidia still controls nearly 80% of the discrete GPU market. Despite Intel’s (INTC) recent entry into the high-end graphics market, Nvidia will likely remain the dominant leader in this space as we advance. Nvidia’s GPUs remain the industry’s gold standard, which will probably not change soon.

One of the reasons why Nvidia’s stock is down so much is due to the company’s gaming revenue decline of 33% YoY. However, gaming revenues crashed for several reasons, and the phenomenon is transitory. Nvidia still has the top products in the market, and its gaming unit will likely make a massive comeback once market conditions normalize and the slowdown ends.

Some of the reasons for the drop in gaming revenues include:

- The coronavirus effect – Nvidia’s gaming unit experienced increased demand during the coronavirus lockdowns.

- The video card shortage – As demand increased for GPUs, prices rose significantly. There was a GPU shortage recently, and Nvidia’s revenues increased substantially due to higher prices. Now that there is a GPU surplus, prices are going through a transitory decline, leading to lower sales for Nvidia.

- The decline in cryptocurrency mining demand – Many of Nvidia’s gaming GPUs went towards cryptocurrency mining. However, now that Ethereum and other networks are moving away from GPU mining, Nvidia faces decreased demand for some of its products.

- The overall economic slowdown – The global economy is in a slowdown. Therefore, it’s normal seeing less demand for gaming products. Moreover, the effect is compounding as GPU prices drop below MSRP.

- The Takeaway – We see that the factors responsible for the drop in gaming revenues are transitory. It is not like Nvidia began making inferior products or someone began producing better GPUs. Nvidia remains the dominant market leader in the discrete GPU segment, which probably won’t change soon. Therefore, as the global economy gets back on track, gaming revenues should improve, GPU prices should rise, and Nvidia’s gaming revenues should increase significantly in the coming years.

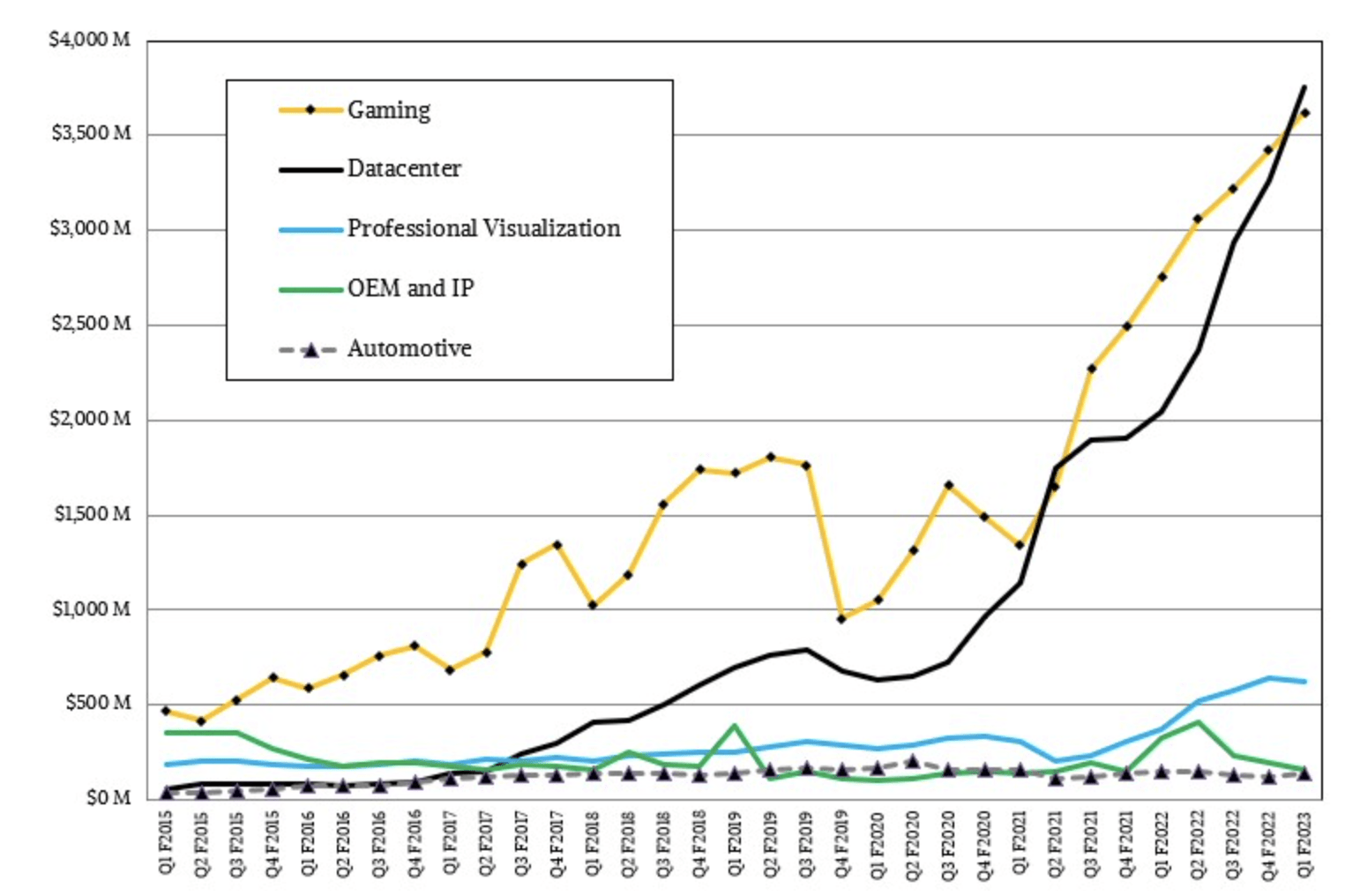

It’s Not All About Gaming Anymore

We often see Nvidia as a gaming company, but it is much more than that now. Last quarter’s preliminary results illustrated that gaming revenue of $2.04 billion was dwarfed by the company’s data center revenue which came in at $3.81 billion last quarter, up by a whopping 61% YoY.

Revenue by Segment

Nvidia revenues (nextplatform.com)

We recently saw data center revenues taking over gaming as the top revenue-producing sector. We should continue seeing robust gains in data center revenues as Nvidia continues its expansion in the industry. Moreover, we should see a significant rebound in gaming revenues in the coming years. Additionally, Nvidia has promising projects in automotive, AI, and other segments that should contribute to the company’s overall revenue stream much more as the company advances.

Nvidia: Valuation Perspective

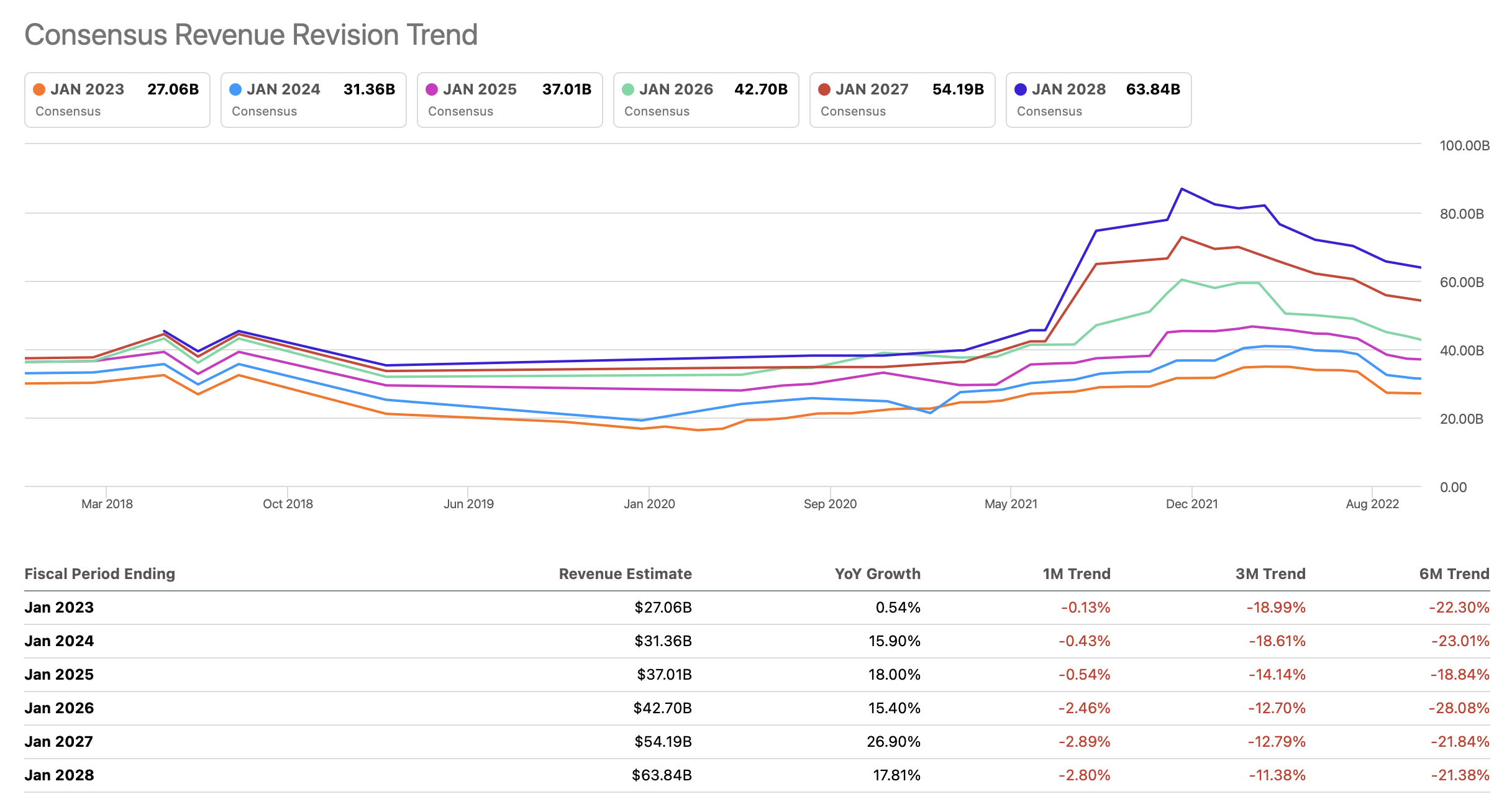

Due to the declining gaming revenue, the broad market slowdown, and other factors, Nvidia’s revenues and earnings expectations have been adjusted lower considerably in recent months.

Revenue Revisions

Revenue revisions (SeekingAlpha.com)

Consensus revenue estimates have been brought down by around 20% in future years over the last six months.

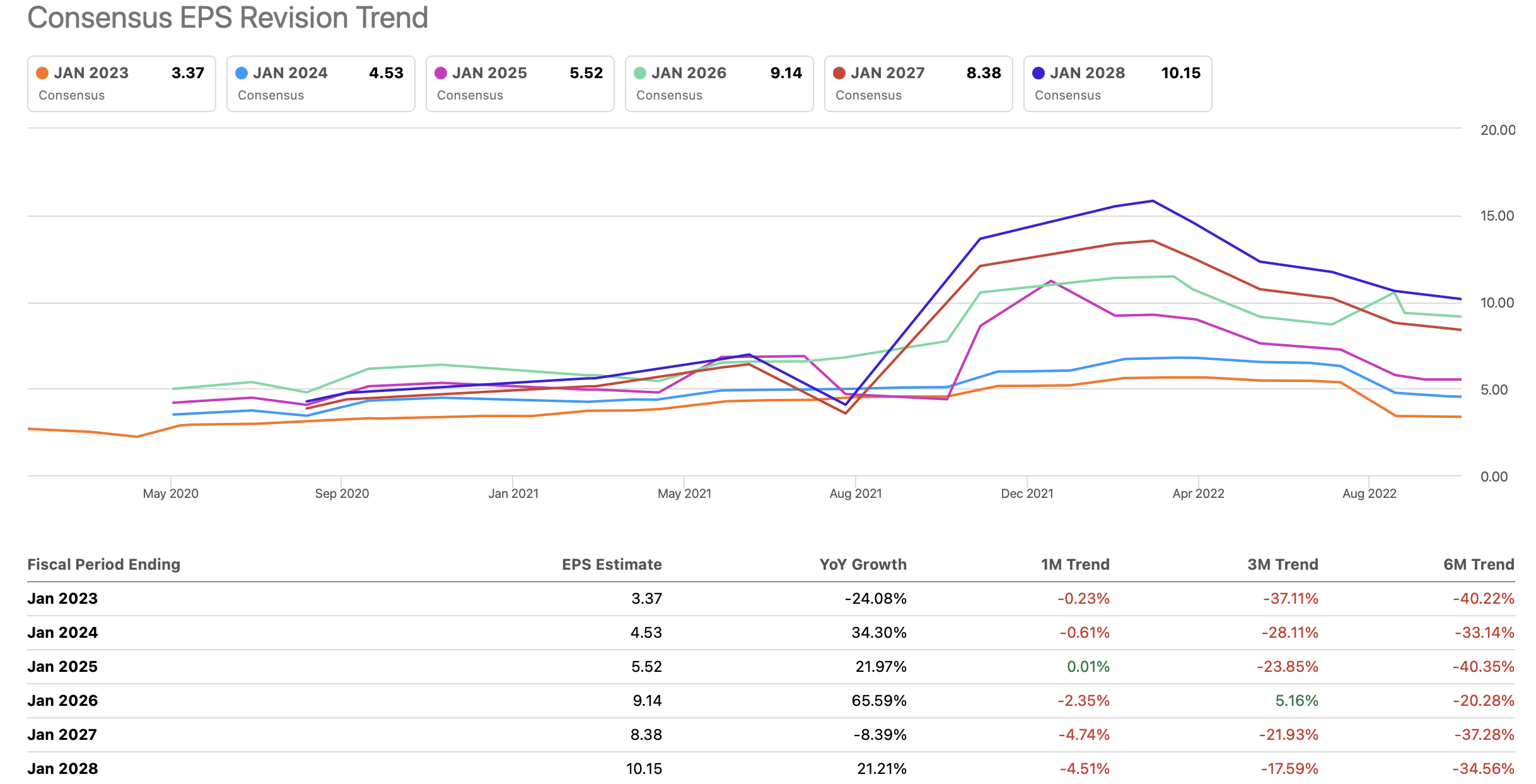

EPS Revisions

EPS revisions (SeekingAlpha.com )

EPS revisions illustrate that consensus EPS forecasts have been lowered by 20-40% for future years over the last six months. While EPS and revenue estimates may have been optimistic when Nvidia was around its highs, we may be seeing overly pessimistic estimates with Nvidia around its lows now. It is possible that just as analysts got ahead of themselves at the height of the bull market, analysts may be lowballing Nvidia’s estimates today. However, even if we look at the current depressed consensus estimates, Nvidia’s valuation is approaching 20 times forward earnings estimates.

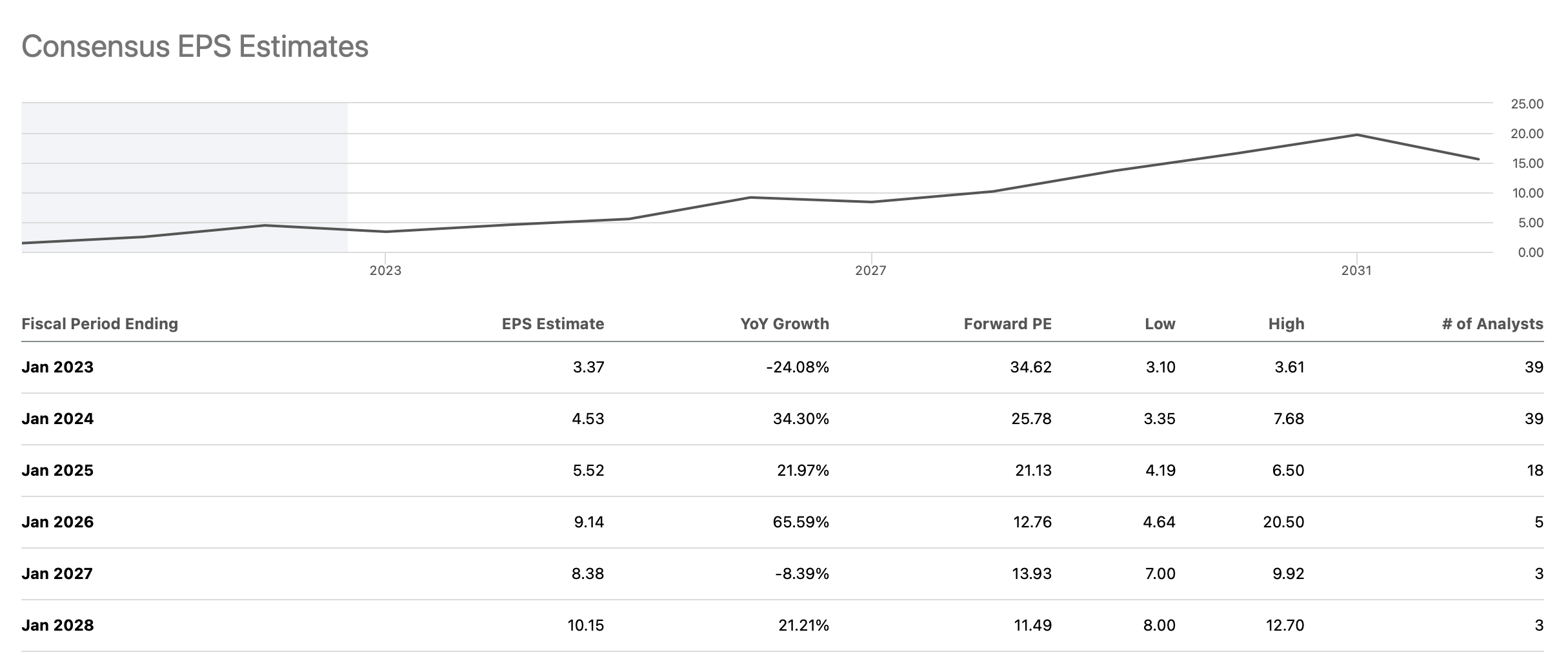

EPS Estimates

EPS estimates (SeekingAlpha.com)

Next year (fiscal 2024), Nvidia should earn about $4.53 in EPS (consensus estimate). My 2023 (fiscal 2024) EPS estimate is closer to $5, but in either case, Nvidia is approaching a 20-forward P/E multiple. If we implement my $5 EPS target, Nvidia is trading at approximately 22.8 times forward earnings, and if the stock hits my buy-in target of $100, its forward P/E ratio will be around 20. When was the last time we saw Nvidia trading at a P/E ratio of 20 or below?

I understand some people may be saying that we will see further deterioration in earnings estimates, but any downside should be transitory and limited, in my view.

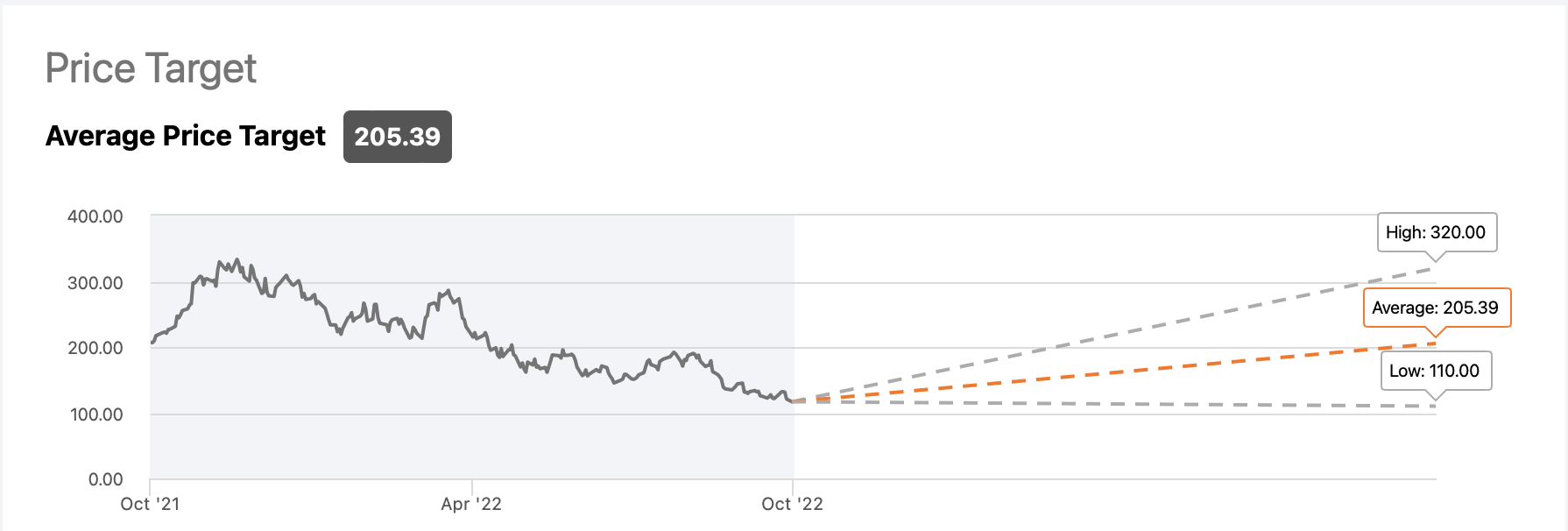

Wall St.’s Price Targets

Price targets (SeekingAlpha.com )

Wall St.’s average 1-year price target on Nvidia’s stock is $205, roughly 80% above its current level. Moreover, the low-end price target is $110, approximately where the stock is trading today. On the other hand, the higher-end price target is at $320, roughly 180% above Nvidia’s price today. I am not expecting the stock to return 180% over the next 12 months, but here is what Nvidia’s financials could look like as we advance:

| Year (fiscal) | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue Bs | $27 | $32 | $38 | $45 | $54 | $65 |

| Revenue growth | 1% | 18.5% | 19% | 18.4% | 20% | 20% |

| EPS | $3.40 | $5 | $6.50 | $10 | $12.50 | $15 |

| Forward P/E ratio | 20 | 23 | 24 | 25 | 25 | 25 |

| Stock price | $100 | $150 | $240 | $313 | $375 | $450 |

Source: The Financial Prophet

The Bottom Line

It will be difficult not to see Nvidia increase substantially as the company’s earnings improve in the coming years. As the company’s profits straighten out, even a relatively low forward P/E multiple of 25 or below should enable shares to move significantly higher as we advance. Thus, the stock could appreciate by 100-200% over the next few years. Despite the likelihood of near-term volatility, Nvidia is a solid long-term investment, and the company’s stock should be considerably higher several years from now.

Risks to Nvidia

While I am bullish on Nvidia in the intermediate and longer-term, technically, we are still in a bear market. Therefore, we may see the stock bottom out at a lower level. In a bearish-case scenario, Nvidia may find its base around the $120 level. However, near-term declines should be transitory and not affect my stock’s intermediate/long-term price target. Additionally, Nvidia could face increased competition in the GPU sector and other areas the company operates in.

Moreover, the company could face margin pressure due to higher costs associated with inflation, leading to decreased profitability. Ultimately, the company could deliver less growth and worse EPS than my estimated forecast. Investors should scrutinize these and other risks before investing in Nvidia.

Be the first to comment