Erik Isakson/DigitalVision via Getty Images

The Thesis

nVent Electric (NYSE: NYSE:NVT) continued to see double-digit topline growth as it entered into the first quarter of FY2024. I expect it to continue further as the company continues to execute its growth strategy including new product introduction, acquisition, and global expansion. Demand remains strong across most of the verticals including Infrastructure and Energy, which along with the benefit from positive pricing should support the company’s sales in the coming quarters. Longer-term demand, on the other hand, should be driven by AI acceleration and energy transition across the industry. Margin prospects also look promising due to strength in pricing and improved productivity. Currently, the company’s stock might appear to be at a premium, however, considering the company’s strong growth prospects, I would rate this stock a BUY.

Business Overview

nVent is a prominent company that, along with its subsidiaries, provides services related to electrical connection and protection solutions. The company provides its services mainly across North America, Europe, the Middle East, Africa, and Asia Pacific. The company mainly operates in three segments:

-

Enclosures: In this segment, the company primarily provides solutions to protect electrical as well as electronic systems in different environments.

-

Electrical & Fastening Solutions: This segment provides solutions to protect power and data infrastructure. Under this segment, the company also offers power connections, fastening solutions, cable management solutions, grounding and bonding systems, and other related products and solutions.

-

Thermal Management: This segment of the company mainly specializes in electrical heating solutions and includes products related to floor heating, heat tracing, and other thermal management products.

Last Quarter Performance

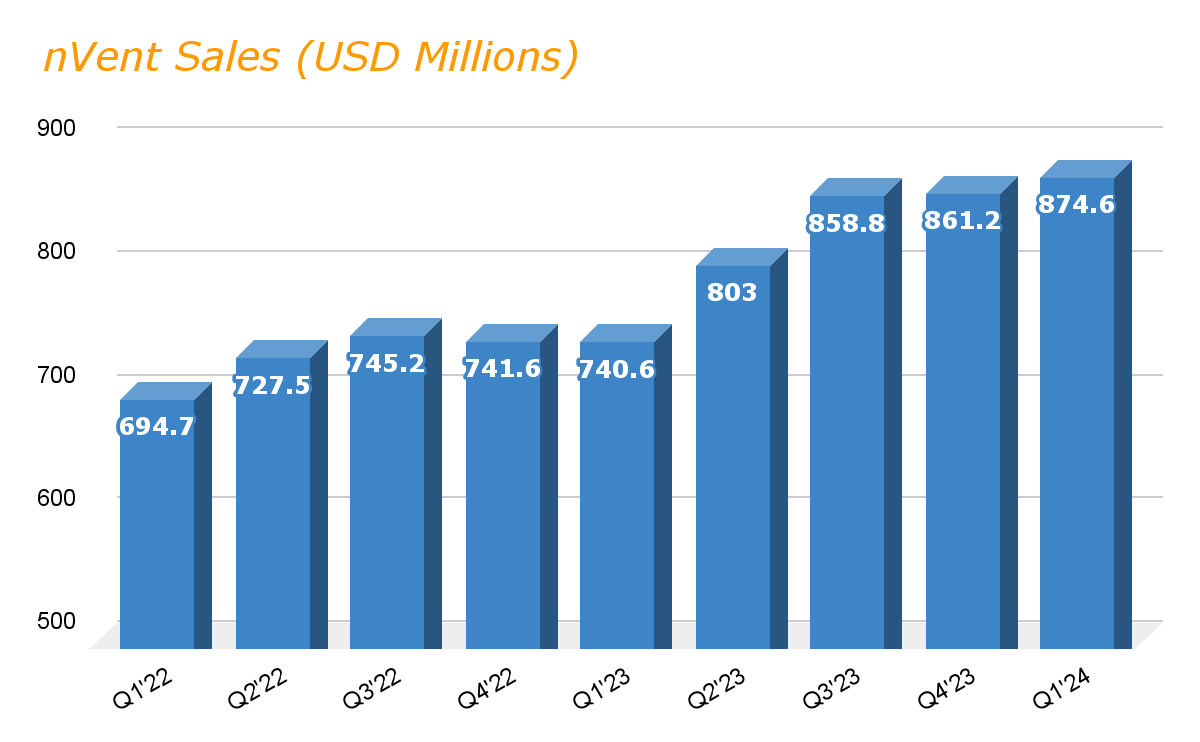

The company continued its strong performance as it continued to benefit from strong AI-accelerated demand for the company’s data solutions offerings. As the company entered into the first quarter of 2024, its topline reported on May 3rd climbed by approximately 18.1% to $875 million versus the prior-year quarter. This strong growth was primarily a result of 42% year-on-year growth in the Electrical & Fastening segment sales, which largely benefited from ECM acquisition contribution, however, the segment’s organic sales were down 3% due to weak volumes. Enclosures, the company’s largest segment by sales, was up approximately 13% to $440 million due to strength across volumes and pricing primarily in the North American region, which led the growth. Finally, the Thermal Management segment was down 1% as the impact from weak volumes offsets positive pricing.

NVT consolidated sales (Research Wise)

Strong topline growth also benefited the company’s margin, as the company’s consolidated segment margin expanded 200 bps to 22% during the last quarter. The growth was largely driven by margin expansion in the Enclosures and the Thermal segment which expanded 50 bps and 80 bps respectively during the quarters, primarily due to benefits from strong execution, favorable mix, and strong topline growth in the Enclosures segment during the first quarter of 2024.

The company’s bottom-line performance was also good, thanks to strong margin growth during the last quarter of 2024. The company reported its EPS at $0.78 during the quarter, up approximately 15% year-on-year, beating the consensus estimates by $0.04. The company’s cash position is also good, as it ended the quarter with $211 million of cash in hand.

Outlook

As the company entered 2024, it continued to execute on its growth strategy that is mainly focused on new products, global expansion, and acquisitions, which benefited the company’s top line in the last quarter. In my opinion, the strong execution of this growth strategy with a focus on high-growth verticals along with strong pricing should continue to drive the company’s revenue in the coming quarters. During the last quarter, the company significantly benefitted from the introduction of new innovative products. So far, the company has launched 17 new products in the last quarter, which should also support the company’s sales across all the regions as the sellout through its key distribution partners remained positive.

Apart from these, the growth prospects look promising across most of the verticals that the company operates in. I expect the infrastructure vertical should continue its strong growth further in 2024 and beyond due to benefits from the electrification and digitalization trends. Also, AI-driven demand for the company’s Data Solutions, primarily in the company’s liquid cooling solutions, should boost the company sales in 2024. The Energy vertical is also expected to grow significantly as we move forward due to strong energy transition growth, particularly in LNG, carbon capture, clean fuels, and hydrogen, which should further benefit the company’s sales in the coming quarter, leading to another good year for the company. The Commercial vertical, however, should deliver modest growth due to softness in the Residential end market.

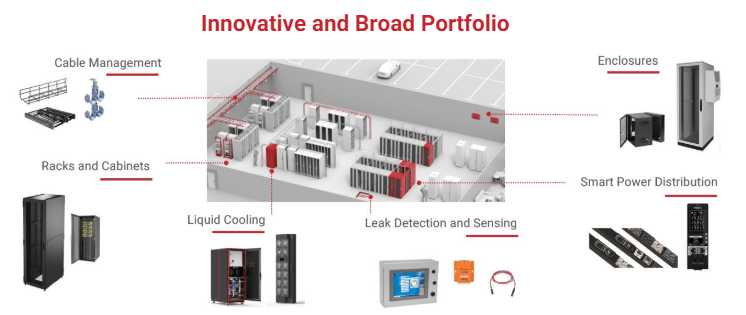

While the company is expected to continue its growth in the near term, the company is well-positioned to grow in the longer term as well as the investment in the data center infrastructure continues to grow notably due to the acceleration of AI. With the technology shift to the new AI chips, efficient liquid cooling is becoming essential as it can save up to energy and power consumption. Currently, only about 5% of the data centers are liquid-cooled, and in my opinion, this number should grow significantly in the coming years, which should benefit the company due to its leading position in this space and a broad range of solutions including liquid to air, air to liquid, liquid to liquid.

AI driving demand for Data Solutions (Company presentation)

Apart from this, the company has developed technical application expertise as well as manufacturing and supply chain capabilities, which along with the company’s ability to manufacture at scales position the company strongly to grow in this rapidly growing space. Furthermore, the company is also building various standard products to drive adoption and scale via its distribution channel. And, as cooling remains an important and growing area of the company, accounting for approximately 50% of the data solution business, the company is setting up new space to expand its liquid cooling capacity, which is expected to come online in the latter half of the year enabling the company to expand its capacity four-fold, which should boost the company’s sales in the longer term.

Data Solutions stats (Company Presentation)

Finally, strategic M&As remain an important part of the company’s growth strategy. The company’s financial position is also good as, it currently has a net debt-to-EBITDA ratio of 1.9 times, well below the target range of 2.0-2.5x. The company is also generating a decent amount of cash flow, which should support the company’s strategic acquisition in the future.

Valuation

In the past few quarters, the company’s top line and margin have expanded notably, leading to significant bottom-line growth and the company’s stock has climbed by more than 60% in the past year. Currently, the company’s stock is trading at a forward P/E ratio of 23.95, based on the FY24 EPS estimates of $3.27, which appears to be at a premium to its five-year average forward P/E, which is currently at 16.23.

NVT’s EPS estimates (Seeking Alpha)

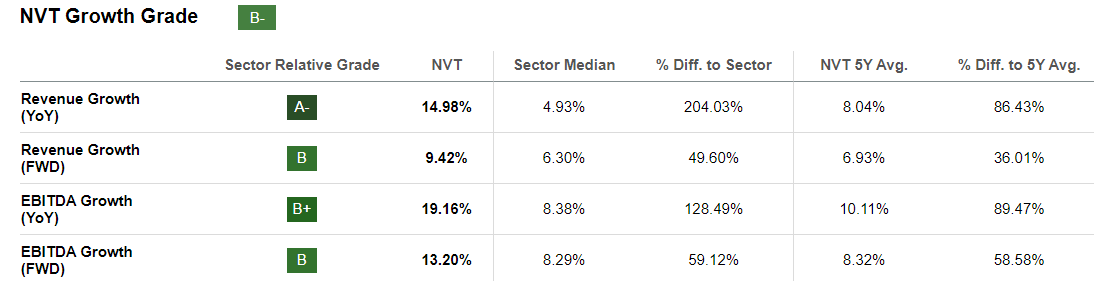

I am expecting the company topline to continue to grow further as the demand environment across most of the market verticals remains strong, primarily due to AI-driven demand and energy transition projects. Pricing is also showing strength primarily in the North American region, which should benefit the company’s margin going forward. As we can see in the chart below, the company’s forward EBITDA is anticipated to grow 13.2% as compared to the single-digit topline growth. This should result in bottom-line expansion in the coming quarter, which should lead to an improved valuation in the future.

NVT’s growth grade (Seeking Alpha)

Risk

The company’s margin has grown significantly in the last few years as the company’s volume also continued to grow. As the company entered 2024, the company saw notable overall margin growth, but a margin decline in its Electrical segment, sales of which, jumped by over 40% during the quarter due to contributions from the acquisition. Among all the demand growth drivers, Strategic M&A remains an important part of the company’s growth in the future. My thesis is built upon that the company will continue to benefit from healthy demand across its verticals, as well as benefit from acquisitions. However, if the profitability remains weak in the acquisition contribution, the overall margin and bottom line might be impacted negatively, which could deteriorate the company’s valuation, leading to poor stock performance in the future.

Conclusion

As we discussed, the company’s stock is currently trading at a premium to its historical averages. The company’s topline should continue is well positioned to continue growing further in 2024 as the demand environment remains good in most of the market verticals. Prices are also positive, which should support the company’s margins in the coming quarter as volume continues to grow. The long term also looks promising due to the expected rise in demand for the company’s product in Data centers, which is being driven by AI acceleration. While the company’s stocks appear to be at a slightly higher valuation, the company’s growth prospects are good, which should benefit its margin as well as the bottom line, which makes the current stock valuation reasonable to me. Therefore, I would recommend to “buy” this stock

Be the first to comment