{kind=link}

Fundamental Forecast for the US Dollar: Neutral

- Despite a disappointing headline figure, the September US NFP report was another milestone on the road to the Fed tapering asset purchases.

- Hawkish expectations for the Federal Reserve per bond and rates markets are now the most aggressive they’ve been all year.

- According to the IG Client Sentiment Index, the US Dollar has a mixed bias heading into mid-October.

US Dollar Weathering Mixed Data

The first full week of October produced modest gains for the US Dollar (via the DXY Index) after good data releases earlier in the week were undercut by a disappointing September US NFP report on Friday. The DXY Index gained a mere +0.04%, led by a stronger USD/JPY that gained +1.03%. A weaker EUR/USD, which fell by -0.19%, was offset by a stronger GBP/USD, which added +0.50%. Nevertheless, bond and rates markets are now discounting their most aggressive hawkish expectations of the Federal Reserve since the start of the coronavirus pandemic.

US Economic Calendar Eyes Second Half of Week

The middle of October will produce another busy docket of event risk based out of the US. After the September US NFP report, several Federal Reserve speakers will be in focus, as well as three ‘high’ rated events that typically produce a significant volatility in FX markets. All of the significant economic data are due in the second half of the week.

- On Wednesday, October 13,weekly US MBA mortgage applications and the September US inflation report (CPI) will be released in the morning, while the September FOMC meeting minutes and a speech by Fed Governor Lael Brainard will in the afternoon.

- On Thursday, October 14, Fed Governor Michelle Bowman will deliver a speech in the morning ahead of the releases of the weekly US jobless claims figures, the September US produce price index (PPI), and a speech from Atlanta Fed President Raphael Bostic. In the afternoon, Richmond Fed President Tom Barkin will deliver remarks and the September US budget statement will be released.

- On Friday, October 15, the September US retail sales report, the preliminary October US Michigan consumer sentiment survey, and the August US business inventories report will be released. In the afternoon, NY Fed President John Williams will give a speech.

Atlanta Fed GDPNow 3Q’21 Growth Estimate (October 8, 2021) (Chart 1)

Based on the data received thus far about 3Q’21, the Atlanta Fed GDPNow growth forecast is now at its lowest expectation of the quarter at +1.3% annualized. This was due to “an increase in the nowcast of third-quarter real gross private domestic investment growth from +10.5% to +10.7% was offset by a decrease in the nowcast of third-quarter real personal consumption expenditures growth from +1.1% to +1.0%.”

The next update to the 3Q’21 Atlanta Fed GDPNow growth forecast is due on Friday, October 15.

For full US economic data forecasts, view the DailyFX economic calendar.

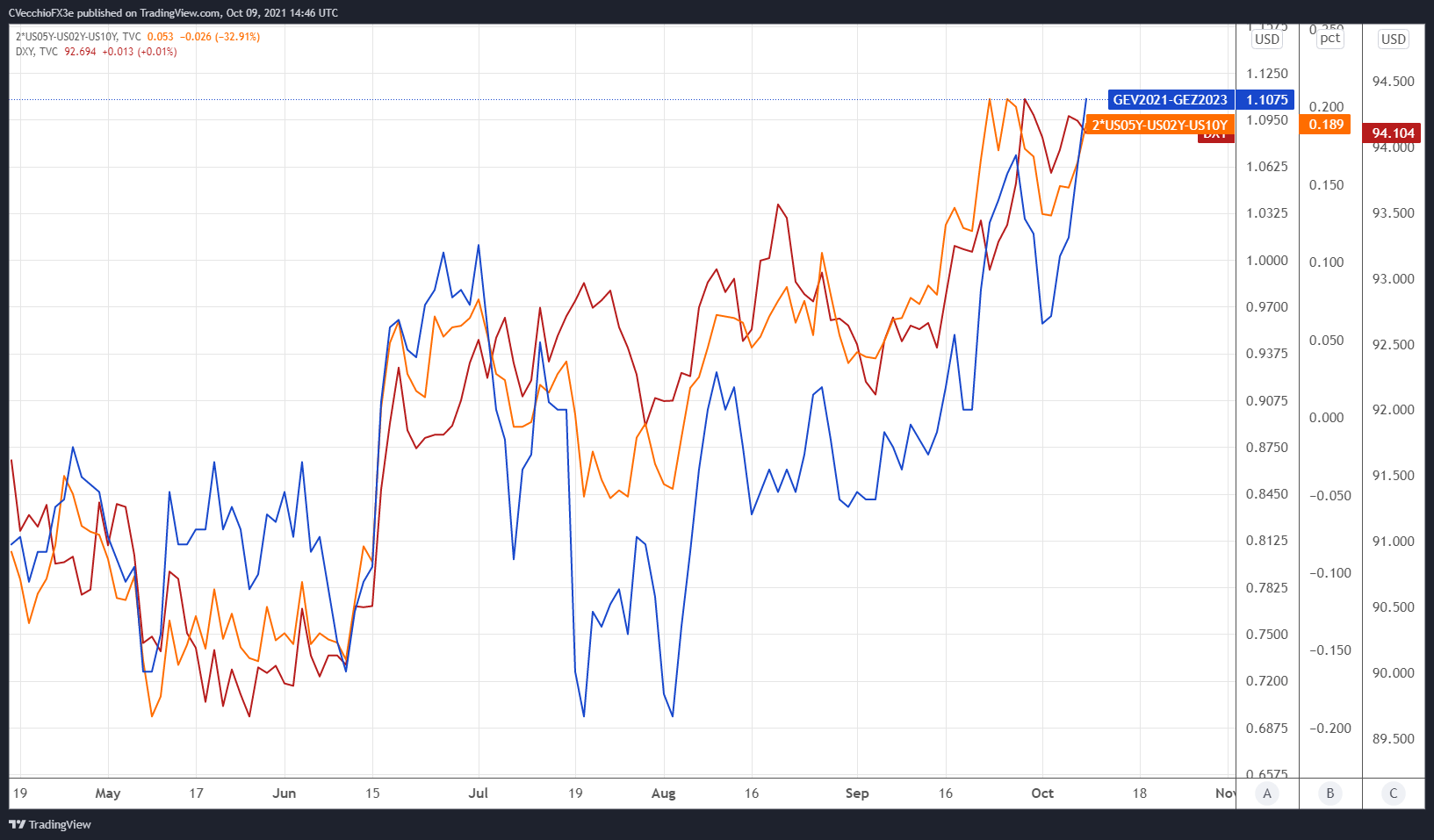

Hawkish Fed Still Expected After September US NFP

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 2 below showcases the difference in borrowing costs – the spread – for the October 2021 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (October 2021-DECEMBER 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Chart (April 2021 to October 2021) (Chart 2)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

As has been the case for several weeks now, continually elevated Eurodollar spreads alongside action in the US yield are consistent with the 2013/2014 period that suggests a more hawkish Fed is soon to arrive.

There are 111-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly recently reached its widest spread since the Fed taper talk began in June (and its widest spread of all of 2021). Moreover, consistent with recent chatter from FOMC officials, the first rate hike looks increasingly likely to arrive in late-2022.

US Treasury Yield Curve (1-year to 30-years) (October 2019 to October 2021) (Chart 3)

Historically speaking, the combined impact of rising US Treasury yields – particularly as intermediate rates outpace short-end and long-end rates – alongside elevated Fed rate hike odds has produced a more favorable trading environment for the US Dollar.

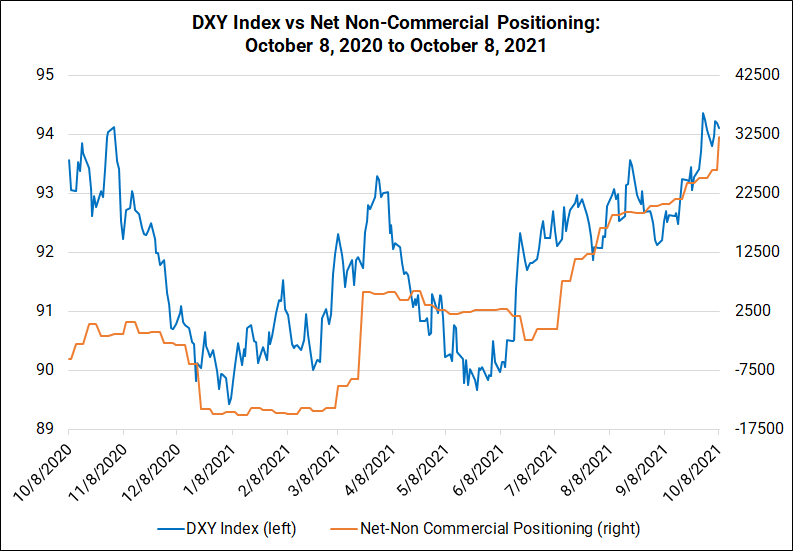

CFTC COT US Dollar Futures Positioning (October 2020 to October 2021) (Chart 4)

Finally, looking at positioning, according to the CFTC’s COT for the week ended October 5, speculators increased their net-long US Dollar positions to 32,006 contracts from 26,443 contracts. Net-long US Dollar positioning continues to hold near its highest level since the last week of November 2019.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment