piranka

Investment Thesis: With rising customer demand and a low EV/EBITDA ratio, I take a bullish view on NortonLifeLock at this point in time.

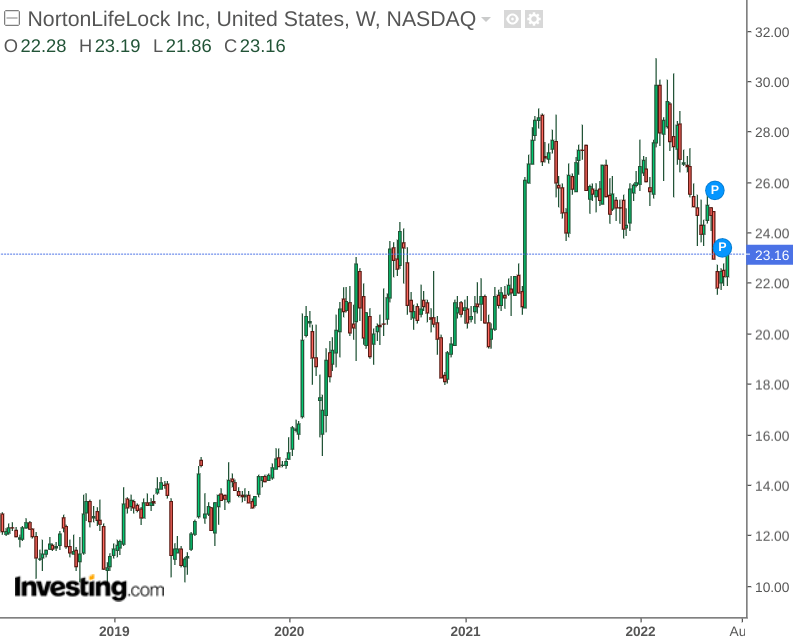

NortonLifeLock Inc. (NASDAQ:NLOK) is a leading company in the computer security space. With concerns over cyber safety having become magnified due to the COVID-19 pandemic and the increase in remote working, we can see that the stock saw significant growth in 2020 and 2021 before seeing consolidation this year:

investing.com

The purpose of this article is to determine whether NortonLifeLock could have room for upside given the recent consolidation.

Performance

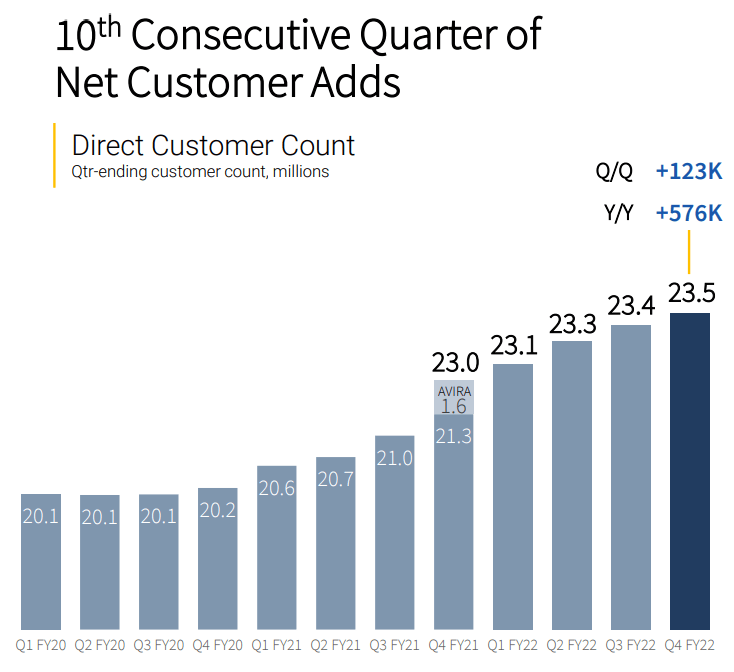

In order to get a better overview of customer and revenue growth for the company, three months ended data from September 2018 to the present for direct customer count, direct average revenue per user, and direct customer revenues were collated and averaged by year. The quarterly data and relevant calculations conducted using SQL can be found here.

In averaging the figures for each year, the following figures were calculated:

| Year | Direct customer count | Direct average revenue per user | Direct customer revenues |

| 2018 | 20.6 | 8.74 | 541.5 |

| 2019 | 20.17 | 8.85 | 551.33 |

| 2020 | 20.4 | 9.05 | 551.5 |

| 2021 | 22.76 | 8.89 | 604 |

| 2022 | 23.5 | 8.9 | 627 |

Source: Figures calculated by author using SQL.

As we can see, NortonLifeLock has seen long-term growth across these metrics – with direct customer revenues up by 15% compared to the average figure for 2018.

Additionally, while direct average revenue per user is down slightly from 2020 levels – there has been a slight rise of nearly 2% from 2018 along with growth of 14% in direct customer count from 2018.

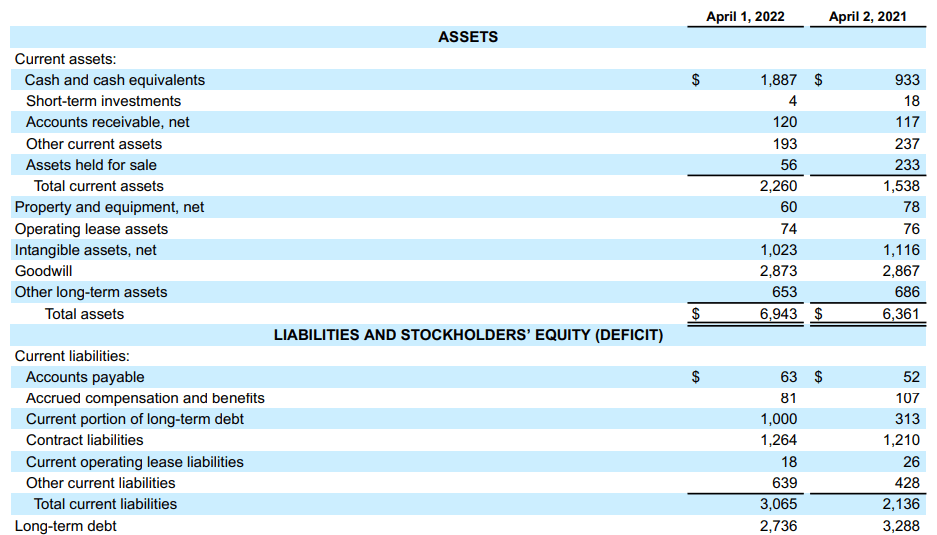

When looking at balance sheet data for the most recent quarter as compared to last year, we can see that cash and cash equivalents has doubled over the period while long-term debt is down by 16%.

NortonLifeLock Financial Results Q4 2022

In addition, net income per share is up by over 50% from $0.92 in April 2021 to $1.41 in April of this year.

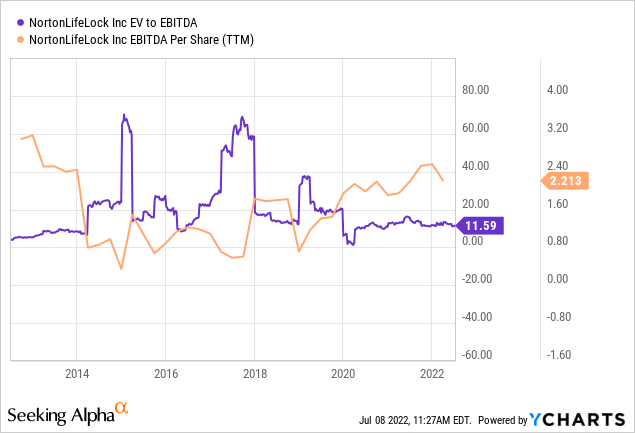

When looking at the company’s P/E ratio, we can see that EBITDA per share has seen a strong upward trajectory since 2018, while the EV/EBITDA ratio is still significantly below levels seen pre-2020.

ycharts.com

In this regard, there is a strong possibility that we could see a rebound in upside going forward if revenue growth continues from here.

Looking Forward

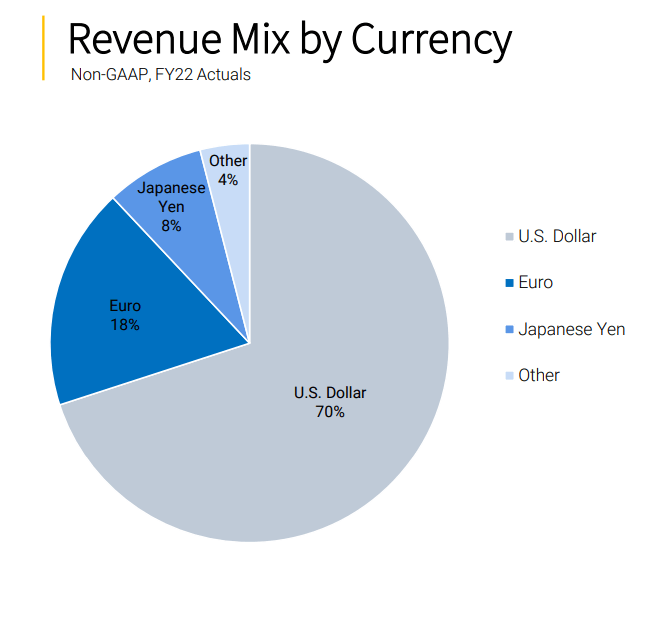

From a macroeconomic standpoint, while NortonLifeLock could potentially see some downside in the short-term if overall market sentiment continues to be bearish, a strong U.S. dollar means that the company’s risk of foreign exchange loss is limited:

NortonLifeLock Fiscal Year 2022 Q4 Earnings

Notwithstanding that growth in average revenue per user has been stable and customer revenues as a whole has continued to rise, one potential concern for investors going forward could be regulatory resistance to the company’s $8.6 billion purchase of Avast (AVST). It is coming under fire in the United Kingdom as a result of concerns that the deal could prove to be anti-competitive and ultimately lead to higher prices for consumers as a whole.

Should we see a situation where the merger ultimately does not go through later this year, I anticipate the stock could see further downside.

NortonLifeLock Fiscal 2022 Q4 Earnings

With that being said, I take the view that NortonLifeLock has a strong position in its own right. Given that this has been the 10th consecutive quarter of direct customer growth for the company, the company is likely to be able to sustain such growth going forward.

Conclusion

To conclude, NortonLifeLock has continued to show strong revenue growth in spite of recent macroeconomic pressures, and I anticipate that as computer security continues to become more of a concern given the increase in remote working – market demand can be expected to grow accordingly.

Given that the stock seems to be trading at an attractive price on an EV/EBITDA basis, I take a bullish view on the stock at this point in time.

Additional disclosure: This article is written on an “as is” basis and without warranty. The content represents my opinion only and in no way constitutes professional investment advice. It is the responsibility of the reader to conduct their due diligence and seek investment advice from a licensed professional before making any investment decisions. The author disclaims all liability for any actions taken based on the information contained in this article.

Be the first to comment