Bet_Noire

Thesis

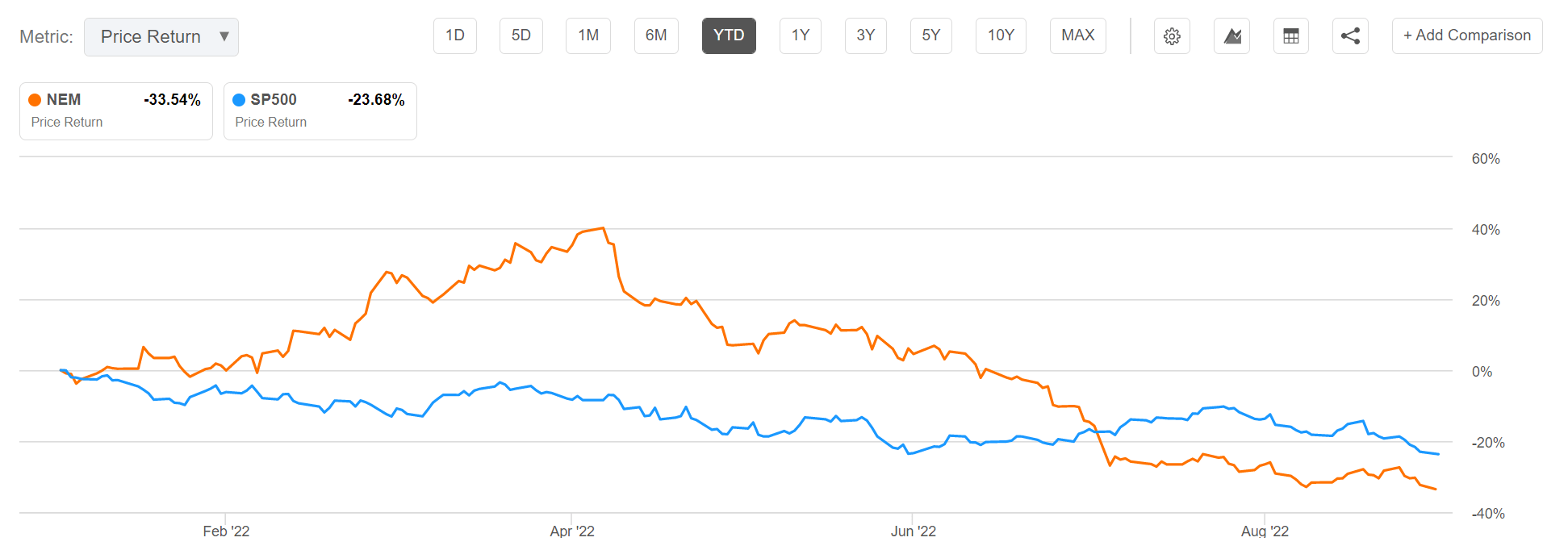

Newmont (NYSE:NEM) stock is down about 35% year to date, and down some 53% from the stock’s all-time high in March. But personally, I do not believe that the stock’s current share price weakness provides an attractive buying opportunity for investors. Gold prices recently fell to their lowest level in 2 years. And as central banks around the world continue to rise interest rates, the yellow metal’s relative attractiveness versus other ‘interest-bearing’ safe assets is under pressure.

Seeking Alpha

From an equity valuation perspective, Newmont stock is priced fairly given the company’s current earnings power, in my opinion. But if gold prices continue to fall, which is not unlikely, Newmont’s profitability could see further pressure and earnings downward revisions. And if an investor would assume 2015 lows as the most bearish downside scenario, NEM stock might still need to reprice by about -65%. Accordingly, I advise to remain on the sidelines for now.

Bad Environment For Gold

Valuations across markets are falling – with stocks down, fixed income securities down and economy-sensitive commodities such as oil down. Also, most major currencies are depreciating in value, except the US dollar. Such moves generally indicate a rush to safe-haven assets, and gold should in theory be well positioned to satisfy the demand. But this time it is different. Gold futures are down about 22% since the YTD high in March.

There is a good explanation why this is not an attractive market environment to invest in gold, and since Newmont’s profitability is closely correlated with gold prices it is neither the time to invest in NEM stock. Gold is broadly considered as a hedge against inflation. But as central banks around the world are fighting hard to tame price appreciation, they are also fighting against the attraction of the yellow metal. Investors should consider that with rising interest rates on risk-free assets such as the US treasury notes, the nothing-yielding gold becomes relatively less attractive. Or in other words, risk-free treasury notes with a greater than 5% yield offer investors an opportunity to compound their capital. While gold does not.

Margin Pressure For Newmont

But a contracting topline due to a lower gold price is not the only pressure on Newmont’s profitability. As a mining company, Newmont faces inflationary pressure from higher labour costs, energy prices and higher CAPEX from machinery replacement/investment. As a consequence, for the trailing twelve months Newmont’s gross profit has decreased to $6.3 billion versus $6.43 billion in 2021, despite higher revenues of $12.34 versus $11.5 billion respectively. Over the same time horizon, the company’s cash flow from operations has contracted by about 15%, from $4.88 billion in 2021 to $4.18 in 2022 (TTM reference).

Investors should consider that pressures to Newmont’s profitability are not likely to fade anytime soon. Notably, the hotter-than-expected CPI print for August has highlighted that inflation is still spooking the economy. But it is unlikely that investors will seek protection by rushing into gold. In fact, I believe that the yellow metal may further lose its luster, as the Federal Reserve is expected to raise the funds rate to as much as 5% in 2023.

Valuation

From an equity valuation perspective, NEM stock is arguably priced fairly. Taking analyst consensus estimates as a reference, Newmont is currently trading at a one year forward P/E of x16.6 and a P/B of x1.5. This is in line with the company’s historical 2-year average trading multiples (Source: Bloomberg EQRV).

Assuming that a stock’s yield is equal to the inverse of the P/E multiple (1/16), NEM would effectively offer a 6.25% yield, which is higher than the current 2-year treasury yield of about 4.3%.

But investing is also a relative discipline. And investors should consider, that NEM’s P/E valuation is similar to leading tech firms such as Google (GOOG), and even higher than Qualcomm’s (QCOM) or Meta Platforms’ (META). Would you feel more comfortable investing in a x16 P/E for NEM or Google? Personally, I would say Google has the advantage here, given that the tech giant has a more favorable growth outlook – in my opinion.

Conclusion

I am not necessarily bearish on Newmont, given that the valuation is acceptable versus the stock’s historical average as well as in relation to other stocks. However, as central banks around the world are fighting CPI appreciation, I do not see a rush to buy gold as an inflationary hedge. In fact, given interest materially positive interest rates on safe-haven assets such as the US treasury notes, I believe the relative attractiveness of investing in gold, and accordingly gold producing assets, is limited. My recommendation for NEM stock is ‘Hold’.

Final thought: I would be open to revisit the thesis of investing in gold and NEM, if it becomes apparent that central banks need to pivot towards a more dovish stance. Or in other words, the health of the economy (labor markets, fiscal deficits, etc.) constrain central banks’ ability to fight inflation.

Be the first to comment