littleny

As the market continues to rebound healthily this year, stock-picking remains of the essence. Pick the right growth names to invest in and be rewarded handsomely for careful stock selection, and avoid value traps and washed-up legacy names that are sitting on bloated valuations.

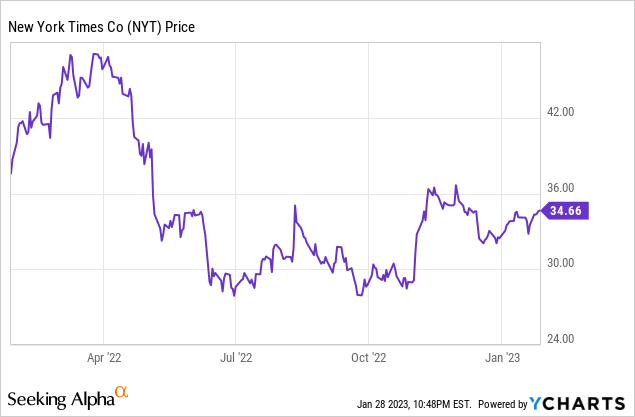

The New York Times (NYSE:NYT) sits high on my list of stocks to avoid. Up 5% this year and down only a relatively modest ~15% over the past twelve months while the rest of the stock market has cratered, I think this vaunted journalism brand is sitting on a pepped-up valuation with very little to show for it.

I remain bearish on the New York Times, and especially as so many better rebound opportunities are floating around in today’s market, I think there is no clear incentive to stay invested in this name. While I think the Times will continue to be a respected, quality journalism brand for years to come (though many would also say that the Times’ political content and its left-leaning bias have also alienated some of its reader base), I don’t see a path for its stock to continue appreciating.

As a reminder, here are what I believe to be the key red flags for the New York Times:

- Organic growth is faltering. Digital revenue growth is currently only held up by the acquisition of the Athletic, and the pace of subscriber additions is paling in comparison to 2020, which was a super-cycle year for news (COVID plus a presidential election). To boost its growth, the Times has turned to acquiring several different companies. Moreover, growth in digital is hardly enough to offset declines in print and advertising.

- Losing focus? The acquisition of The Athletic makes sense. But the addition of Wordle only has a loose connection to the Times’ long-standing history of crossword puzzles. It has become apparent that The New York Times is primarily interested in purchasing companies to keep up digital subscriber growth numbers at any cost, even when large purchases like The Athletic are dilutive to the bottom line. In my view, management is spreading itself too thin in trying to form a conglomerate of different news brands and games.

- Will people continue to pay for the news? The internet and a variety of applications are now serving up news for free. Social media applications like Twitter and Instagram now somewhat function as a news-absorption channel for many younger users. Looking ahead to the future, the concept of paying for news may cease to become mainstream.

- Inflation is a real profit killer for The Times. Unfortunately, we are already in an age where lots of news is available for free (or consumed in other ways, such as via social media) – so the thought of raising prices is unthinkable. In fact, The Times’ chief tactic for attracting new subscribers is via lowball introductory offers, such as $1/week for four weeks. At the same time, inflationary wage pressure means that The Times is having to shell out a lot more to keep its newsroom staff afloat. This exploding cost burden, plus the losses at recently acquired companies, is eroding The Times’ profit margins. Avoid this stock: I think the upcoming earnings cycle in early February (the company will report results on February 8) will give the stock a long-overdue walloping.

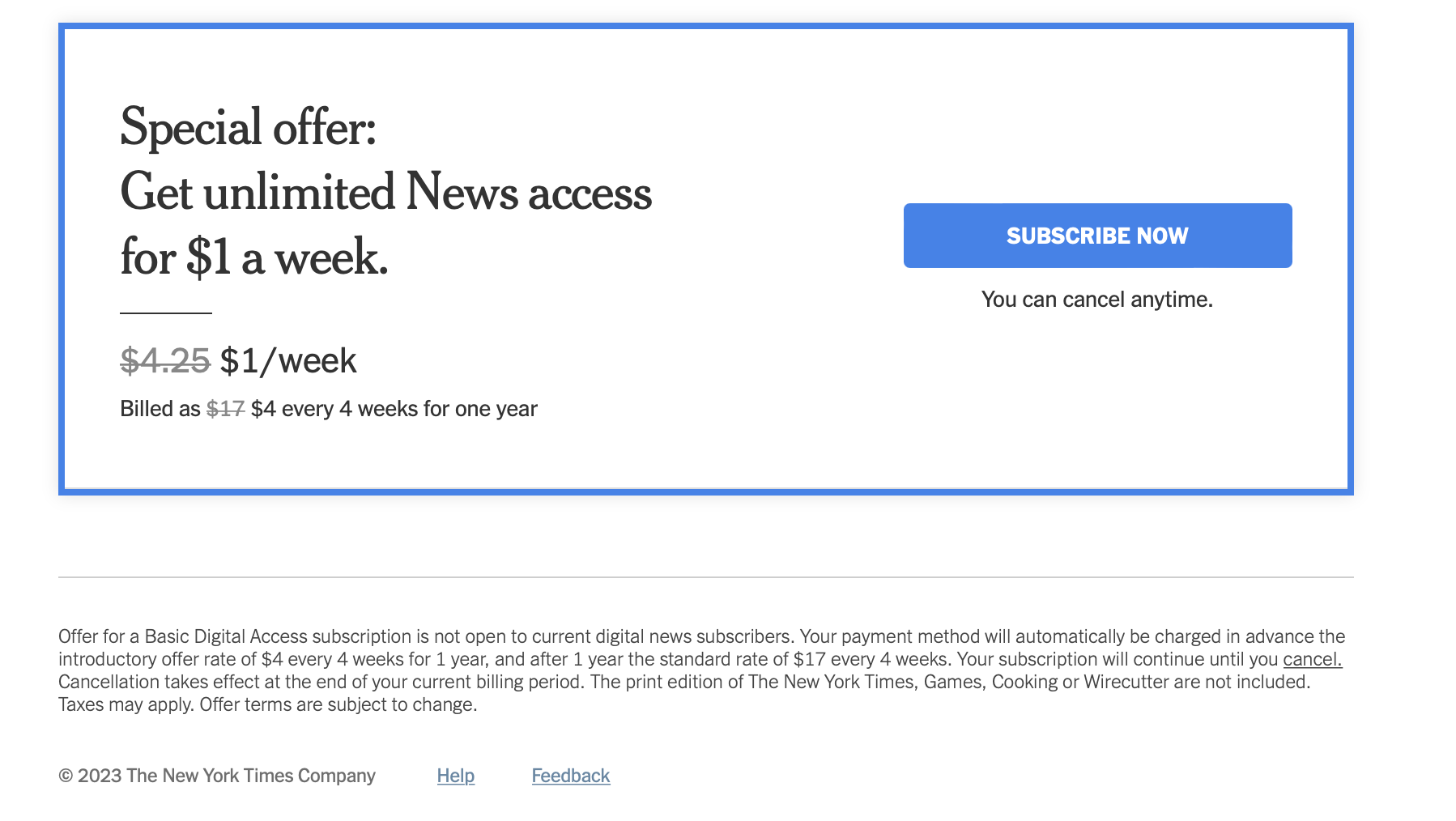

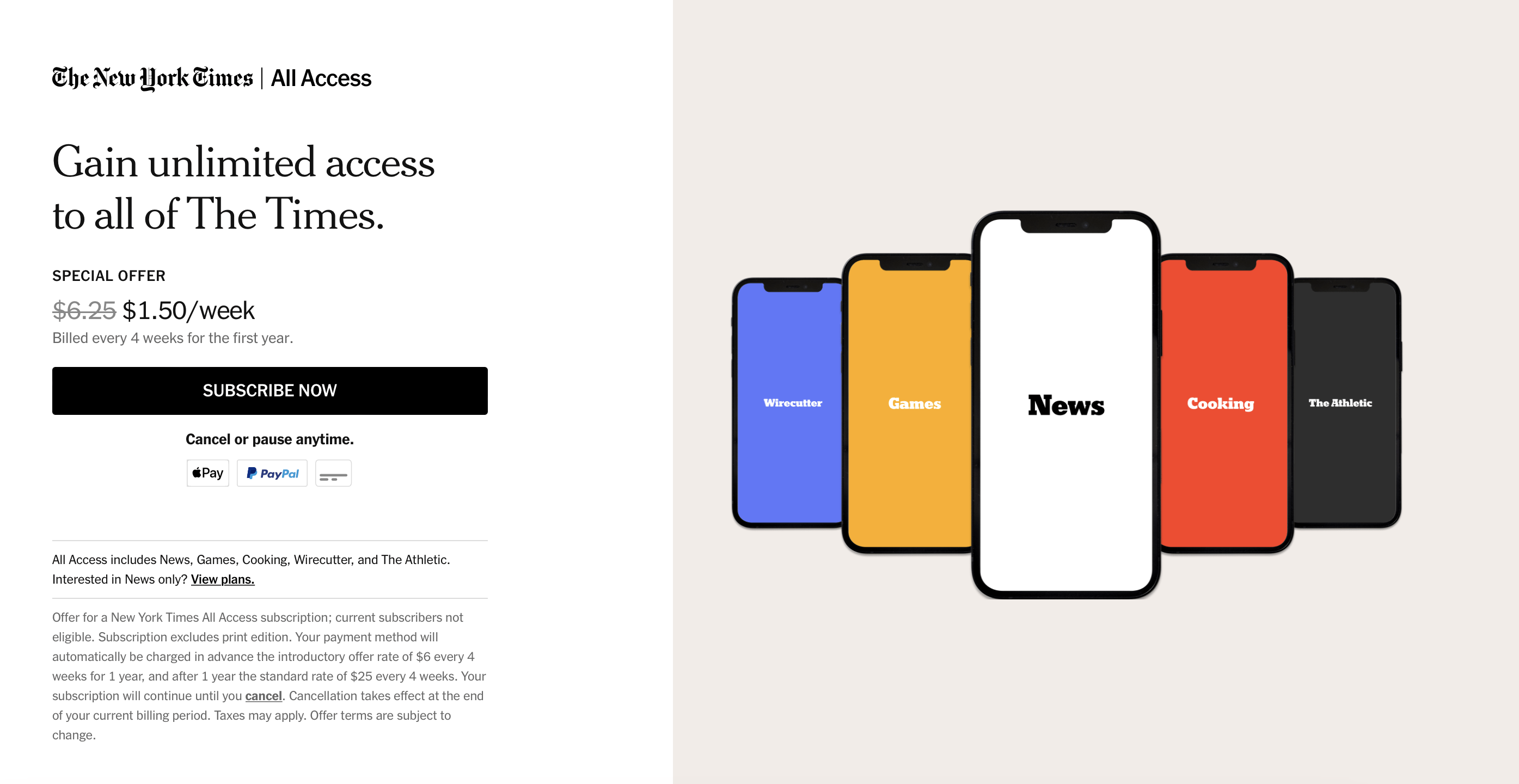

Aggressive customer acquisition offers

Let’s dive into the last point on discounts in a bit more color. Almost every subscription service has a discounted or free trial period: but where the New York Times is unique is that its discount periods frequently last for one year.

The snapshots below show the offers that the Times is currently displaying. Users can sign up for news-only digital access for $1/week for a full year:

New York Times news offer (NYT.com)

An All-Access subscription isn’t that much more expensive when discounted, either, running at only $1.50/week:

New York Times all-access offer (NYT.com)

Note additionally that these discounts aren’t too difficult to abuse by users who switch to a different email account when the trial period is over.

Financials don’t support valuation

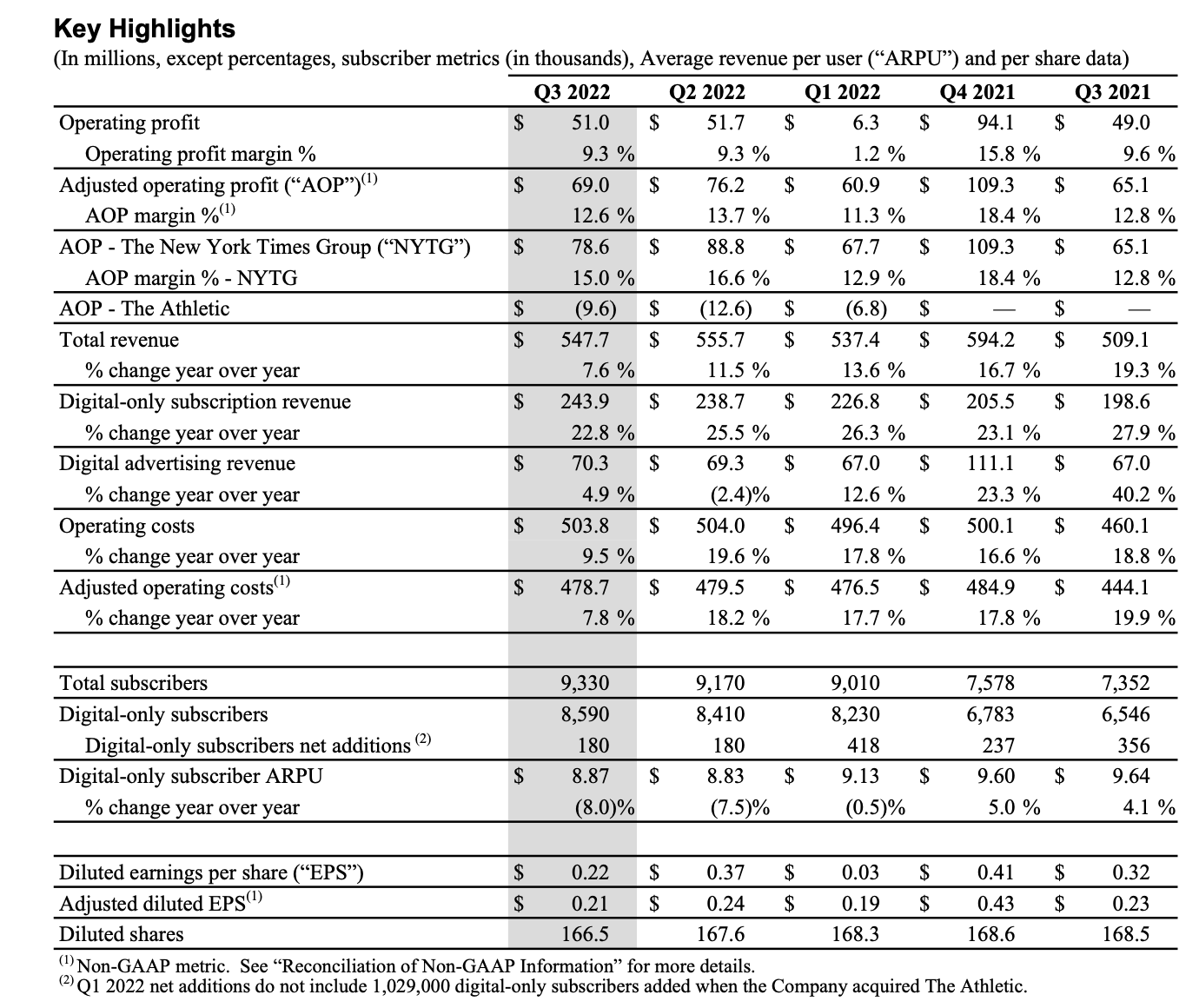

The New York Times often touts its subscriber additions. The company added 180k net-new digital subscribers in Q3, and subscribers grew 31% y/y to 8.59 million (driven in part by the inclusion of the Athletic’s subscribers, which brought in 1.1 million subscribers in Q1):

New York Times Q3 highlights (New York Times Q3 earnings release)

But digital revenue growth of 23% y/y (again, helped in part by the acquisition of The Athletic which had no prior-year comp) fell short of overall subscriber growth, and total revenue growth of only 7.6% y/y (pulled down by declines in print subscriptions and print advertising) fell even shorter still.

The key message here: don’t focus on subscription adds when a lot of these subscriptions are being drawn in at very low, discounted prices. Revenue growth is still quite stagnant, and that’s what really matters.

In the long run, the company’s strategy is to drive more bundled offers that increase customer subscription values. Per CEO Meredith Kopit Levien’s remarks on the Q3 earnings call:

Leveraging the whole of our portfolio to drive the bundle is our priority over the coming quarters. As we do that, we’ll be taking measures to further open up The Athletic’s hard paywall to substantially increase awareness and free sampling of The Athletic in order to build a large, sustainable audience funnel. We expect that this will result in slower additions of subscribers on a standalone basis for some time, as it did in the third quarter. Our ambition here is to become one of the leading players in global sports journalism, and we’re confident that in doing so, we’ll create significant value for shareholders.

Notably, we continued to see higher engagement among bundle subscribers, with 10% to 20% more bundle subscribers engaging each week than news-only subscribers. This is true across the entire base and among cohorts of bundle subscribers who are in their first few months with us – an encouraging sign given the strong relationship we have seen between subscriber engagement and retention.

As a result of the efforts I’ve just described, The Times crossed an important milestone in the quarter: We now have more than 1 million bundle subscribers – discernable momentum on a key element of our strategy to drive revenue, profit, and shareholder value. The Times now has more than 9.3 million subscribers, with 10.8 million subscriptions, well on our way to our next mile marker of 15 million subscribers by 2027.”

This bundle benefit has not yet driven ARPU growth, however. Digital subscription ARPU in Q3 was $8.87, flat to Q2 but declining -8% y/y – reflective of the company’s aggressive discounting strategy.

And we should be mindful of a slow decay in operating margins as well. Operating costs grew 9.5% y/y in Q3 to $503.8 million, two points faster than revenue growth – pushing down operating margins to 12.6%, a 20bps reduction y/y and a 110bps sequential reduction. Put more simply: it’s not getting any cheaper to produce high-quality journalism, even if consumers’ willingness to pay for it is declining.

Valuation and key takeaways

At current share prices near $35, the New York Times is trading at a forward P/E of 32x against Wall Street’s consensus EPS expectations of $1.08 for FY23 (data from Yahoo Finance). This premium valuation baffles me: why pay a bloated P/E for a legacy company that is barely growing its top line and is facing notable margin pressure?

Stay away from this stock at all costs.

Be the first to comment