BsWei/iStock via Getty Images

There are a number of proposed SEC regulation changes regarding short selling that could impact trading in Imperial Petroleum (NASDAQ:IMPP), GameStop (NYSE:GME), and other meme stocks. Could the impact of these new regulations help to stabilize trading or could the changes actually increase price volatility? Of course, the reality might be that the proposals, if enacted, could just increase paperwork requirements and add more bureaucratic regulations that really do not impact trading or investors. The SEC proposals have to do with lending of shares for short selling, reporting of short sale positions by institutional investment managers, and changing equity trade settlement from T+2 to T+1.

Current Short Sales Available Data

Before looking at the SEC proposals, we need to remember what information on short selling is already available for Investors. First, FINRA reports twice a month short interests on individual stocks. The latest reports are usually published 9 days after the reporting date. Imperial Petroleum had 9.71% short interest and GameStock had 19.54%. While these numbers are interesting, they are also rather dated. It seems that many investors are unaware of the daily reported numbers. Short sale share volumes during regular trading hours are posted by FINRA before 6:00pm for that trading day. These numbers, however, do not include pre and post regular trading hours data.

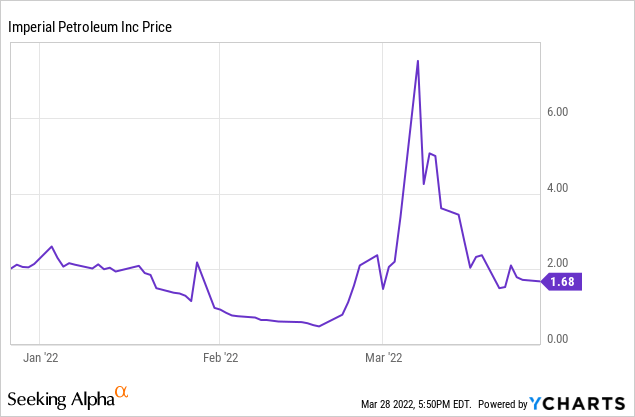

Imperial Petroleum

Short Volume//Short Exempt//Total Volume

Mar. 25 21,806,491//1,294,702//42,880,531

Mar. 24 31,300,390// 1,106,387// 56,270,292

Mar. 23 35,810,023//366,983//65,821,340

Mar. 22 8,798,131//493,331//18,786,950

Mar. 21 17,494,596//1,038,406//37,078,488

Three Month IMPP Stock Price

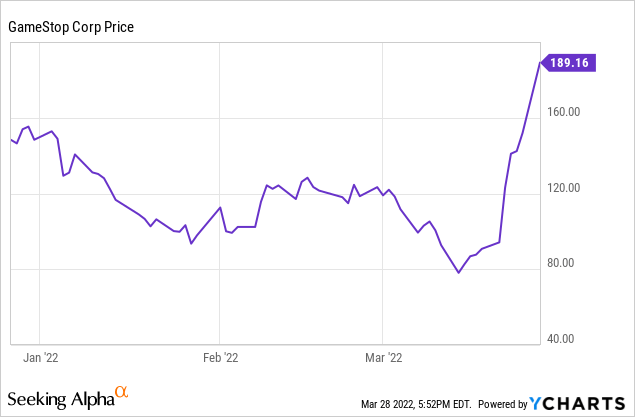

GameStop

Short Volume//Short Exempt//Total Volume

Mar. 25 3,593,380|120,678|6,530,569

Mar 24 2,439,491|41,399|4,217,003

Mar. 23 6,694,081|24,132|11,437,161

Mar. 22 3,550,458|22,976|7,213,409

Mar. 21 799,429|22,390|1,781,226

Three Month GME Stock Price

Rule 10c-1 Proposed Change

On November 18, the SEC announced a proposed change to Rule 10c-1 regarding the lending of all securities used in short selling and for settling failed deliveries. The comment period on this proposed change keeps getting extended and currently ends April 1. It could be some time before the changes actually become effective even after they are adopted because computers will need to be upgraded to reflect the changes. SEC released a 184 page document that discusses the changes. (Text of the proposal starts on page 176 of 184 pages.)

The SEC proposals focus on lending and lenders, which, of course, impacts borrowers of securities who sell short. Under the proposal, lenders of all securities (stock and debt instruments-except Repo trades) would have to file with FINRA (“RNSA”- registered national securities association – is actually used in the SEC proposal) within 15 minutes after the lending is affected details about the transaction. The required information includes borrower’s name, number of shares, all direct/indirect fees, collateral securing the loaned securities, time period, and some other detailed information.

In addition, at the end of the trading day, lenders/lending agents would have to file statements with FINRA that include securities on loan and securities available to loan for each security they own. This would even apply to insurance companies, foundations, and pension plans that lend their securities, but do not currently report to FINRA. Those lenders who currently do not report to FINRA are already pushing back on these proposals. It could mean that FINRA would be getting daily reports on their portfolio holdings, if they are required to report securities available to be loaned. Those that do not lend securities will not have to file “securities available to loan” based on my reading the proposals. (I have serious doubts that this part will actually be adopted because of lengthy court challenges.)

Currently neither FINRA or SEC get all this information. This will be a major change. The information by security will be publicly available, but details about specific lenders/borrowers will not be disclosed. Timely reporting of the transactions could significantly reduce “naked shorting” where a short seller has not arranged for borrowing securities before entering sell orders. In addition, it will be almost impossible to have more shares sold short than the number of shares outstanding under these proposals. This will most likely greatly reduce the risk of future short squeezes, in my opinion.

As many short sellers know, the fees/borrowing rates to sell short IMPP and GME shares are very high. Some brokers were charging late on March 25 almost 94% for selling short IMPP and 26.3% to short GME. Many feel that they are being ripped-off by brokerage firms. Currently this information is not being directly reported to FINRA or the SEC. Under the proposals, FINRA would be able to see the fees. It will, therefore, be able to see the difference in fees between various lenders and difference in fees for small retail transactions and for larger trades by hedge funds.

It is unclear when the public will be able to see the data and I am assuming the data would be made available on FINRA’s website, which already reports certain short sales data. (See above.)

This new transparency most likely will lower borrowing costs, especially for retail traders. As the SEC stated, “the proposal might also reduce the cost of short selling”. Customers will be able to compare fees posted by FINRA to the fees charged by their broker and may move their accounts to brokers who charge lower fees. This increased competition could, however, have a negative impact on broker’s bottom line who are currently gauging their clients.

Looking specifically at the impact on these two meme stocks, you see a large impact difference between them. Because Imperial Petroleum has a very small equity capitalization, very few, if any, investment companies, pension plans, insurance companies even own IMPP stock. Most of the lending, therefore, is at the retail level within and between brokerage firms.

At this point, we need to have a sidebar to look at selling short a very low priced stock. Since IMPP is currently selling at $1.72 many small retail traders most likely are buying IMPP shares in cash accounts instead of margin accounts. If IMPP and any other shares are bought in a margin account, the broker is allowed to lend out the shares for short sales because that authority is always (or almost always) is included in the margin agreement. In the past, the lending clause was not routinely included in cash account agreements, but now for cash accounts with zero commissions this lending clause is now usually included in cash account agreements. Of course, customers that are lending their IMPP shares to others to sell short will not actually be the ones filing the data with FINRA, it will be done by their brokerage firm.

Since GameStop currently trades at about $190 and has an equity capitalization over $14.4 billion, it does have institutional ownership of GME shares that will be impacted by this new required data filing. These institutional holders are a much more reliable and steady lenders of shares than just relying on retail brokerage account holders, which is one reason why the borrowing rate to sell GME short is so much lower than IMPP.

Proposed Rule 13f-2 & Rule 205 Changes

The next SEC announcement on February 25 actually includes two different proposals. Proposed Rule 13f-2 involves reporting short sale positions and proposed Rule 205 change involves a new buy to cover reporting requirement.

Currently there is no reporting of buying shares to cover prior short sales. Shares are just bought to cover prior short sales. This proposal would require marking “buy to cover” transactions that will allow monitoring by FINRA. (The text of 242.205 is found on page 192 of 201 pages.)

This Rule 205 change is a very straightforward, but I do see one problem. If you sell short at one broker and then later buy shares at a different broker and have them deliver those shares to cover that short position, there would be no marketing of “buy to cover”. For example, if I short the same stock at many different brokers, which I frequently do, and buy a large block of the same stock at a different broker where I had no short sales of that company, that buy order would not be marked “buy to cover” even if those purchased shares were delivered to the other brokers to cover the prior short sales.

Under the other SEC proposal, an institutional money manager will have to file Form SHO within 14 days from the end of the month if “either a gross short position in an equity security with a US dollar value of $10 million or more at the close of regular trading hours on any settlement date during the calendar month or a monthly average gross short position as a percentage of shares outstanding in the equity security of 2.5% or more”. In addition, if they hold $500,000 or more non-reporting with the SEC equity securities at the close of regular trading hours on any settlement date during the calendar month they will have to file Form SHO for that equity security. (Text for amended Part 240 starts on page 190 of 201 pages.)

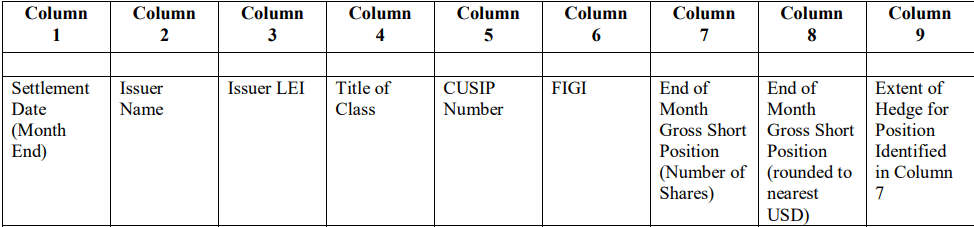

Form SHO

Table 1-Manager’s Gross Short Position Information

sec.gov (Form SHO-Table 1 (sec.gov))

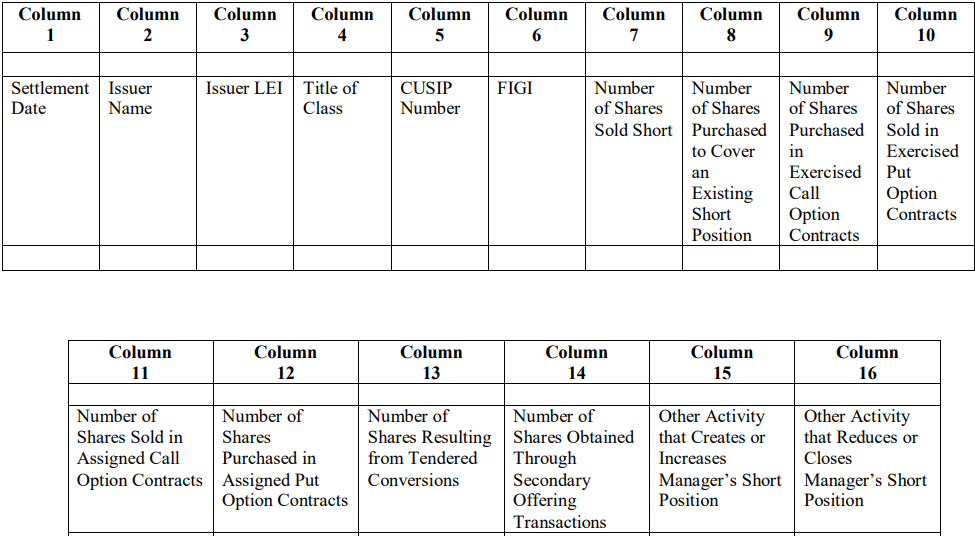

Table 2-Daily Activity Affecting Manager’s Gross Short Position During the Reporting Period

sec.gov (Form SHO Table 2 (sec.gov))

The information will be published within 30 days, but not certain specific details. While this will require a lot of data to be reported, it will be done by computers and not by some by margin clerks working with pens and paper. It is interesting to note that this rule does apply to a natural person, only institutional money managers. So if an individual investor has a position above these metrics, they do not have to file Form SHO. Another interesting note is that the new Rule 205 will enable them to easily determine column 8 “shares purchased to cover existing short position”.

Both the $10 million and 2.5% metrics could impact GME investors because of their large capitalization. I find it unlikely the $10 million metric would impact IMPP investors because it is unlikely there will be such a large short position held by an institutional money manager given their very small equity capitalization, but the 2.5% metric could trigger an institutional money manager to file Form SHO.

Amend 240.15c6-1 Settlement Cycle

This proposed SEC change may not seem that will have a critical impact on short selling, but it most likely will. It is also a lot less complex than the other proposals. On February 9, the SEC proposed changing stock settlements from T+2 to T+1 and they also stated eventually they would like T+0. (The text of amending 240.15c6-1 starts on page 244 of 247 pages.)

With one day less carrying period for short sales, brokerage firms will have less risk exposure and one less day to maintain collateral to back transactions. Some brokers, such as Robinhood (HOOD), limited trading in some meme stocks in early 2021 because of massive capital needed to back meme trades.

Another major impact on changing to T+1 is that trading settlement for stock trades would be the same as listed put/call options. This has been an issue since the 1970’s of trying to structure positions/trades for stocks and options. From my own experience of selling short a stock and either buying a call as protection or selling short a put has been a challenge to manage capital and margin requirements. Having the same T+1 settlement will make portfolio management much easier. I have been waiting for this change for over 47 years, but I may have to wait until March 31, 2024, before it becomes effective according to the SEC.

Conclusion-General Impact Of All SEC Proposals

Many retail short sellers hope that these combined SEC proposals will reduce the fees to sell short, including selling IMPP and GME short. These lower fees could encourage other retail investors to sell short as part of their investment strategy. That, however, could create a huge problem. If these retail short sellers do not have adequate capital to meet margin calls if the shorted shares soar in price, they could get automatic close-outs and may still owe additional funds. These market orders to “buy to cover” could cause stock prices to increase quickly even if there are shares available to sell short. Instead of meme long traders, you could have meme short traders who only have a very modest amount of capital and who are not able to back up their short positions with cash/securities.

I worry that lowering short selling costs for retail traders could actually increase stock volatility especially for small equity capitalized companies, such as Imperial Petroleum, unless the FINRA significantly raises the capital from $2,000 to open a margin account, which is needed to sell short, to $25,000 or even higher.

The SEC is expecting that their proposals will reduce selling short expenses, which they expect could increase fundamental research on selling short a company’s stock and that “when management knows that short sellers may be studying their firms, they are less likely to engage in inappropriate and/or value-destroying behavior”. The SEC also asserted that “short sellers also serve as valuable monitors of management”.

While most of these SEC proposals may take years before they become effective, some of them may have a negative impact on Imperial Petroleum and GameStop stock prices because there could be increased short selling in the future and there will much less risk of future stock squeezes. Therefore, I rate both IMPP and GME a sell. I would also rate most meme stocks a sell.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment