Bill Oxford/E+ via Getty Images

Tredegar Corporation (NYSE:TG) recently reported that the Internet of Things revolution could represent a growth driver for one of its business segments. Management also announced that new ERP software may be installed to enhance efficiency in some of the company’s manufacturing plants. Besides, manufacturing capacity could increase thanks to more capex. There are obvious risks from exposure to operations in Brazil, where competition appears to become global, as well as the increase in the price of raw materials. With that, I believe that Tredegar Corporation remains undervalued.

Tredegar

Headquartered in Richmond, Tredegar is a manufacturer and distributor of polyethylene, polyester, and aluminum.

Tredegar has a total of 10 production plants, almost all of them in the United States, except two plants that are located in China and Brazil. The aluminum segment, in charge of the Aluminum Extrusions subsidiary, is the area with the most plants assigned, five plants located in Utah, Michigan, Georgia, Indiana, and Tennessee.

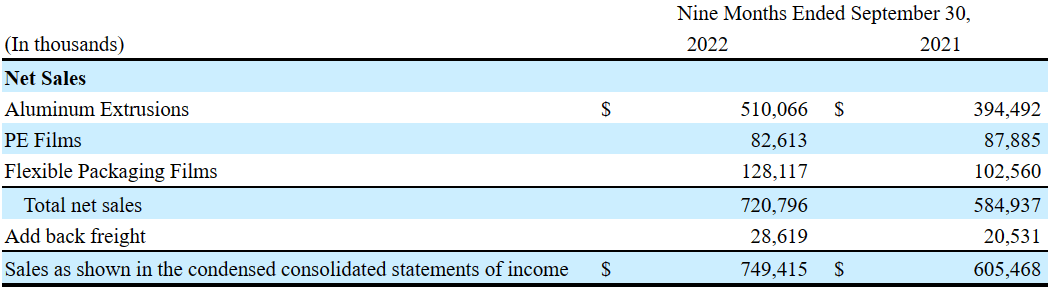

Polyethylene, polyester, and aluminum represent Tredegar’s business segments, intended for different clients, for industrial utilities and home construction. In the nine months ended September 30, 2022, most of the company’s revenue came from aluminum extrusions.

Source: 10-Q

It is interesting to understand the greatest value of the company’s business segments in the extrusion process that the company offers to its customers. Extrusion is a complex industrial process whose purpose is the malleability and design of parts through casting under pressure, in this case aluminum. In this sense, by having the possibility of adapting its parts to the needs of its clients, whether for the construction of residential settlements or industrial establishments, or equipment and machinery, as well as electrical networks, Tredegar can offer a personalized, high-quality service.

Balance Sheet

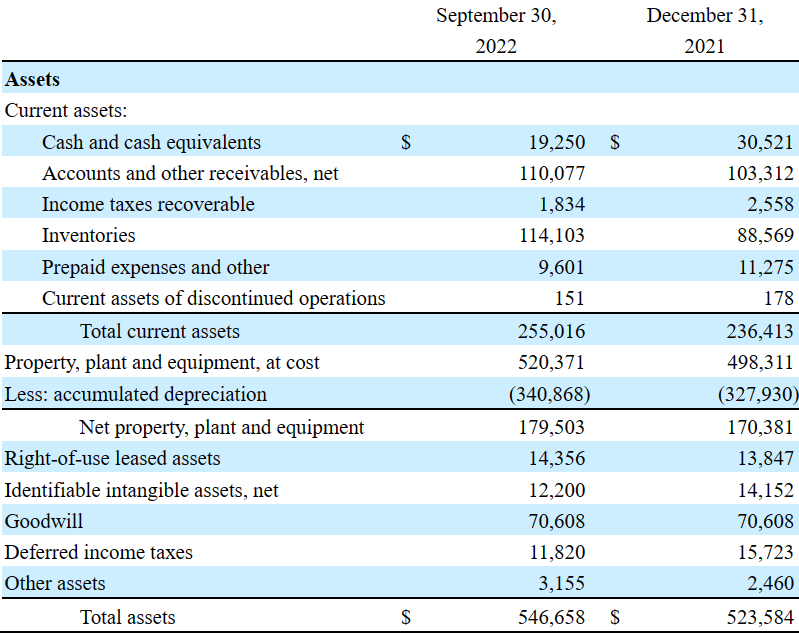

As of September 30, 2022, Tredegar reported cash of $19.250 million along with accounts of $110.077 million. Inventories were worth $114.103 million, and total current assets were equal to $255.016 million. The total current assets/current liabilities ratio is larger than one, so I am really not afraid of Tredegar’s liquidity.

With net property of $179.503 million and goodwill of $70.608 million, total assets stand at $546.658 million. With an asset/liability ratio around 1x-2x, I really believe that the balance sheet stands in good shape.

Source: 10-Q

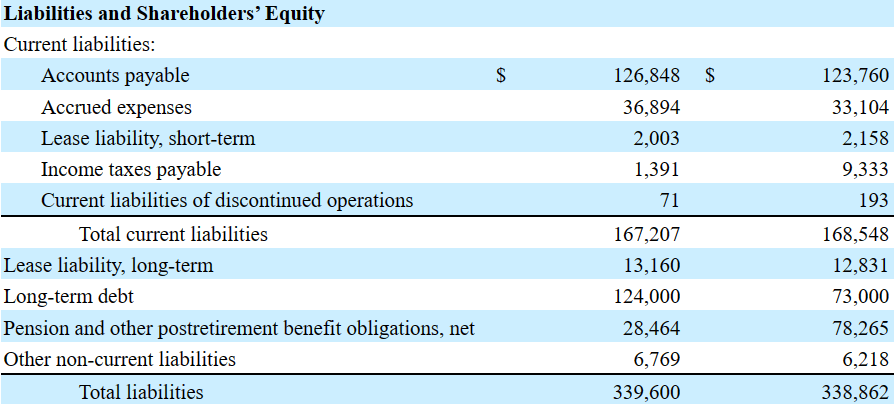

Regarding the liabilities, Tredegar reported accounts payable worth $126.848 million, with accrued expenses of $36.894 million and total current liabilities of $167.207 million. With lease liabilities worth $13.160 million, long term debt of around $124 million, and pension and other postretirement benefit obligations of $28.464 million, total liabilities are equal to $339.600 million.

Source: 10-Q

Considering that 2024 EBITDA is expected to be close to $101 million, I don’t believe that the total amount of long-term debt or total liabilities are that large. In my view, most investors will likely not be afraid of the company’s leverage.

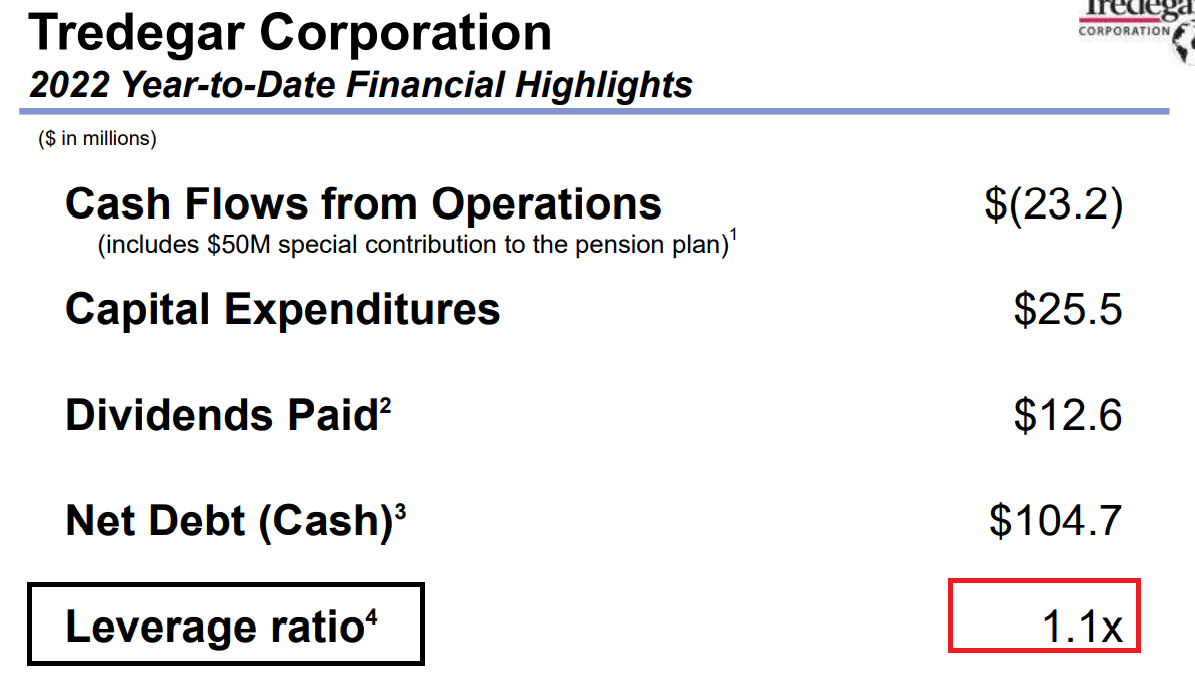

Source: Investor Presentation

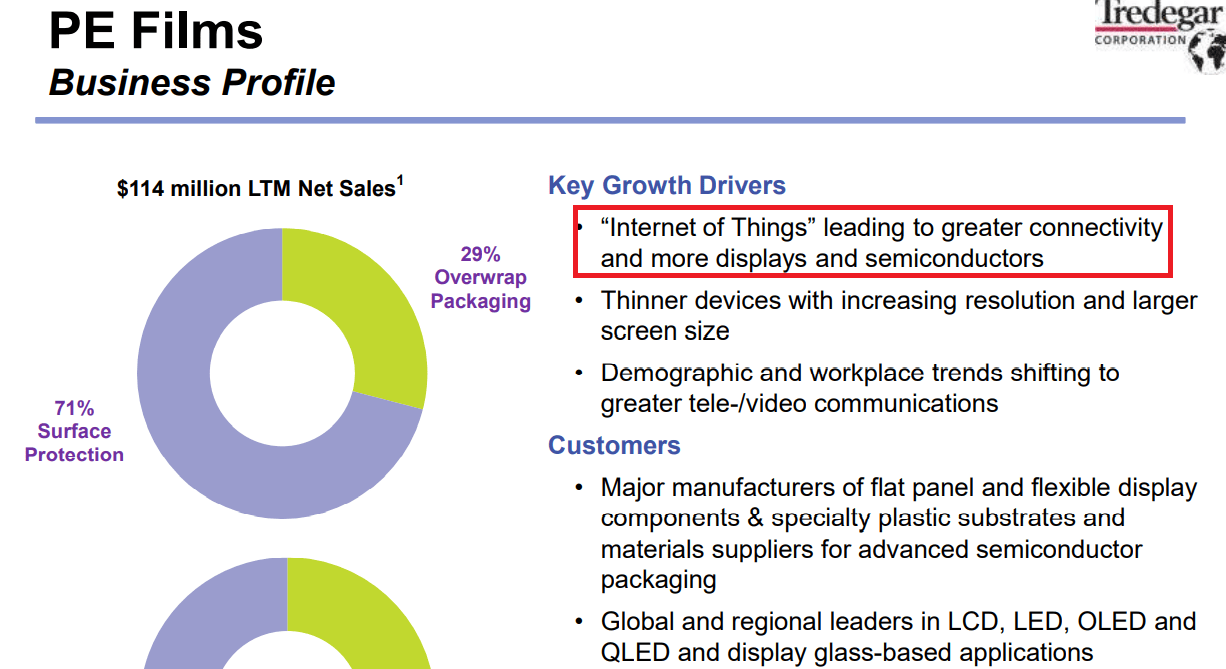

Growth Drivers Like The Internet Of Things And New Enterprise Resource Planning Systems Could Lead To A Valuation Of $19.89 Per Share And An IRR Of 7%

The foremost reason to write about Tredegar is the fact that the Internet of Things revolution may lead to significant sales growth of the company’s PE films business model. Management pointed it out in the last quarterly report. If LCD, LED, and OLED manufacturers show more demand for Tredegar’s products, revenue growth will likely trend north.

Source: Investor Presentation

I also believe that Tredegar’s plant located in Guangzhou, China, which operates with the PE Films business model, may help enhance FCF generation. Let’s keep in mind that China offers lower cost of material and labor than the United States. Besides, the plant offers the accessibility of direct sales in the Chinese market.

I am quite optimistic about the new capital expenditures plans for Bonnell Aluminum and the new ERPs that the managers intend to install. In my view, if the new software brings efficiency to the manufacturing facilities, investors will likely see free cash flow expansion.

Capital expenditures for Bonnell Aluminum are projected to be $30 million in 2022, including $15 million for new enterprise resource planning and manufacturing execution systems, $6 million for infrastructure upgrades at the facilities located in Niles, Michigan, Carthage, Tennessee and Newnan, Georgia and $3 million for other strategic projects. The ERP/MES project is expected to cost $28 million over a two-year time span. In addition to strategic projects, approximately $6 million will be required to support continuity of current operations. Source: 10-Q

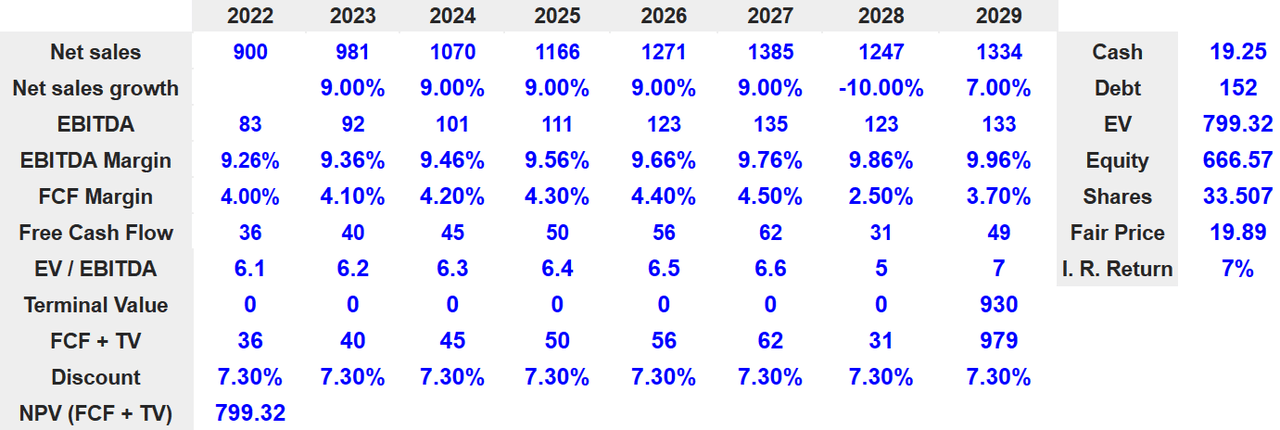

I expect the following results for 2029. Net sales would be close to $1.334 million with a net sales growth of 7%. In addition to 2029 EBITDA of $133 million together with an EBITDA margin of 9.96%, 2029 free cash flow would stand at $49 million with an FCF margin of 3.70%. I believe that my figures are quite conservative.

Source. Bersit’s DCF Model

With an EV/EBITDA multiple of 7x, I obtained a 2029 terminal value of $930 million. If we sum the future free cash flow, and also discount the terminal value with a WACC of 7.3%, the implied enterprise value would stand at $799.32 million.

With cash of $19.25 million and debt and pension obligations of $152 million, equity stands at close to $666.57 million. Finally, if we assume a share count of 33.507 million, the fair price would stand at $19.89 with an internal rate of return of 7%.

Risks Could Lead To A Valuation Of $8.2 Per Share

Tredegar, through its subsidiary Flexible Packaging Films, dedicated to the production of polyester-based films, has a production plant that also functions as a technical operations center. This segment also has a plant located in São Paulo, Brazil. This plant, although it means the positioning of the corporation in the South American market, has lately brought some problems to the company. Due to the transformations that the regional market has undergone, the devaluation of national currencies, the appearance of competitors with cheaper costs, the sale of products at a lower market price, and the regulations of the Brazilian government, the company considers that the market has become a market of global competition. This, of course, radically changes development strategies in the country as well as the entire region. Finally, there is the fact that Tredegar is exposed to the currency in Brazil.

Flexible Packaging Films is exposed to foreign exchange translation risk because almost 90% of the sales of Flexible Packaging Films business unit in Brazil and substantially all of its related raw material costs are quoted or priced in the U.S. Dollars while its variable conversion, fixed conversion and sales, general and administrative costs before D&A are quoted or priced in Brazilian Real. Source: 10-Q

In addition to these risk factors and the current complications of its operations via industrial plants in Brazil and South America, we can add some other typical factors of the area in which its business model is specialized. For example, the variation in the prices of raw materials and their transportation, the inability to attract new customers, or changes in the demand for the parts produced by the company.

Also, it should be noted that Tredegar does not seem to detail future objectives regarding environmental matters, putting the company’s operations at risk not only due to the social and political climate and its trends, but mainly due to the difficulty it may have to adapt to future regulations in the United States in relation to the impact on the ecosystem.

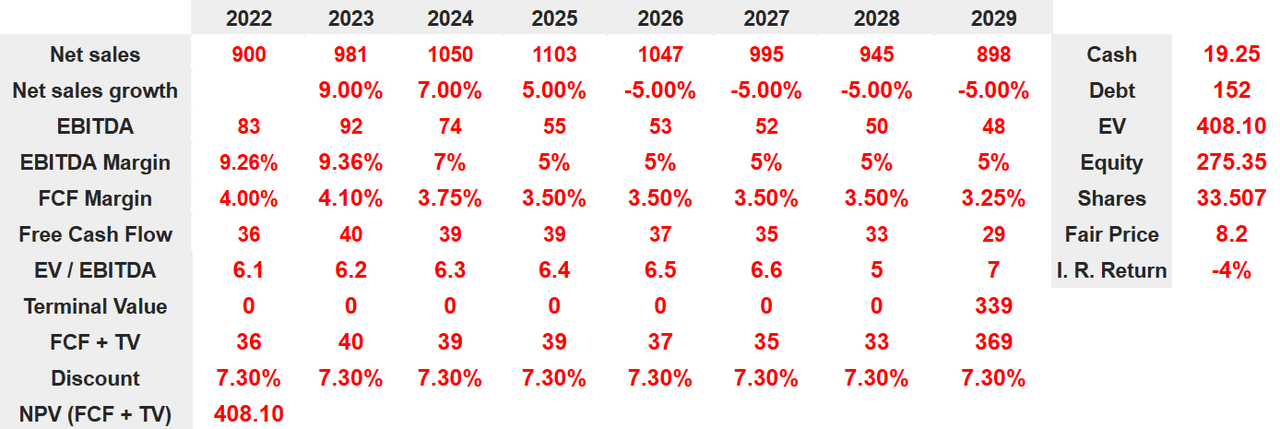

Under the previous conditions, I included 2029 net sales of $898 million with net sales growth of -5%. EBITDA will likely be around $48 million with an EBITDA margin of 5%. Free cash flow may be close to $29 million together with an FCF margin of 3.25%.

With an EV/EBITDA of 7.05x and a discount of 7.305%, the implied enterprise value would stand at $408.10 million. Equity would stand at $275.35 million, and the fair price could be close to $8.2 per share with an IRR of -5%.

Source. Bersit’s DCF Model

Conclusion

Tredegar recently identified the Internet of Things revolution as a growth driver for the company’s PE Films business segment. Management also expects to invest in new ERPs, which may bring further efficiency in some of the company’s aluminum plants. Finally, management also announced several infrastructure upgrades, which would bring new capacity, and may enhance sales growth. I do see some risks from changing market conditions, exposure to Brazilian currency, and rising global competition in South America. With that, I believe that the current market price is below Tredegar’s fair price.

Be the first to comment