cyano66

Streaming company Netflix, Inc. (NASDAQ:NFLX) blew away expectations by adding 7.66M subscribers to its streaming platform in the fourth quarter, beating its own as well as market expectations. Netflix’s Q4 2022 earnings sheet sent shares soaring on Friday, but I believe that investors are overreacting to the firm’s subscriber gains because subscriber growth is not translating into revenue growth for Netflix. Another key issue is that despite strong overall subscriber gains in the fourth quarter, the majority of such gains once again came from lower value markets in the Asia-Pacific and Latin America, where the average revenue per membership is about half of what it is in the US/Canada market!

Netflix beats subscriber expectations but still grows mainly in low value markets

After two quarters of major subscriber losses in Q1 2022 and Q2 2022, the fourth quarter turned out to generate significant subscriber gains for the streaming company. Netflix added 7.66M subscribers globally, including 910 thousand in the US/Canada market – which remains from an average revenue per membership and monetization perspective the most lucrative market for Netflix – 3.20M in Europe, Middle East and Africa (EMEA), 1.76M in Latin America and 1.80M in the Asia-Pacific region. The Asia-Pacific segment has been the fastest-growing business for Netflix in 2022. Netflix guided for 4.5M paid subscriber net-adds while the market expected 4.6M new subscribers.

The streaming company ended the fourth quarter with 230.75M subscribers, meaning Netflix added a total of 8.91M new subscribers through its platform in FY 2022.

Despite solid subscriber gains in Q4’22, I believe the problem with Netflix is that the majority of the growth in subscribers once again occurred in markets with low subscriber values, such as the Asia-Pacific or Latin America. Netflix gained 5.39M new subscribers just in the Asia-Pacific region in FY 2022, implying that the region was responsible for 61% of Netflix’s total subscriber growth. Latin America added 1.74M subscribers on a net basis in FY 2022, representing a share of 20% of subscriber growth. A subscriber in Asia-Pacific is worth $7.69 for Netflix (on a monthly basis) while a subscriber based in Latin America has a membership value of $8.30… which is about half than what a subscriber in the U.S./Canada is worth to Netflix ($16.23 per user).

|

in millions |

Q4’21 |

Q1’22 |

Q2’22 |

Q3’22 |

Q4’22 |

|

UCAN |

|||||

|

Paid Memberships |

75.22 |

74.58 |

73.28 |

73.39 |

74.30 |

|

Paid Net Additions |

1.19 |

-0.64 |

-1.30 |

0.1 |

0.91 |

|

Average Revenue Per Membership ($) |

$14.78 |

$14.91 |

$15.95 |

$16.37 |

$16.23 |

|

EMEA |

|||||

|

Paid Memberships |

74.04 |

73.73 |

72.97 |

73.53 |

76.73 |

|

Paid Net Additions |

3.54 |

-0.30 |

-0.77 |

0.57 |

3.20 |

|

Average Revenue Per Membership ($) |

$11.64 |

$11.56 |

$11.17 |

$10.81 |

$10.43 |

|

LATAM |

|||||

|

Paid Memberships |

39.96 |

39.61 |

39.62 |

39.94 |

41.70 |

|

Paid Net Additions |

0.97 |

-0.35 |

0.01 |

0.31 |

1.76 |

|

Average Revenue Per Membership ($) |

$8.14 |

$8.37 |

$8.67 |

$8.58 |

$8.30 |

|

APAC |

|||||

|

Paid Memberships |

32.63 |

33.72 |

34.80 |

36.23 |

38.02 |

|

Paid Net Additions |

2.58 |

1.09 |

1.08 |

1.43 |

1.80 |

|

Average Revenue Per Membership ($) |

$9.26 |

$9.21 |

$8.83 |

$8.34 |

$7.69 |

(Source: Author.)

Revenue growth concerns

The problem with Netflix’s results for the fourth quarter is that strong subscriber gains did not translate to strong revenue gains for the streaming company, for reasons explained above.

Despite adding 7.66M subscribers in just the last quarter, Netflix’s total revenue growth was only 1.9%, and it marked a serious slowdown from 16.0% growth rate in Q4’21. The fact of the matter is that revenue growth in the streaming market is increasingly hard to come by because most large media companies now have rolled out their own streaming offers and the streaming market as a whole has become saturated.

Netflix’s CEO is stepping down

In other news, Netflix announced that its CEO Reed Hastings would step down as co-CEO and move over to the executive chairman position. The market did not take the announcement in a negative way: shares of Netflix soared 9% after earnings.

Netflix has two pathways to grow revenues

Netflix got into the advertising business in the fourth quarter by rolling out an ad-supported subscription plan in 12 countries which costs subscribers $6.99 per month… which is about a third less than the lowest-priced tier without ads. Netflix has said it is optimistic about the launch and that it plans to grow the ad business into a significant revenue line (representing 10% or more of consolidated revenues). Netflix is so far not seeing subscribers down-grading their subscription plans, but it may be too early to judge the success of the ad business. I indicated that there is a cannibalization risk for Netflix by introducing an ad-supported tier.

The second revenue opportunity relates to a proposed crackdown on password-sharing. Apparently, up to 100M households use this practice, which is costing Netflix billions of dollars in annual revenues. If Netflix finds a way to charge customers extra for adding non-household members to a subscription plan, I could see Netflix reinvigorate its sales growth going forward.

Outlook for Q1’23 and Netflix’s valuation

Netflix has said that it will no longer issue subscriber forecasts because the streaming company wants to focus on revenue and operating income growth going forward. However, Netflix did issue a revenue projection for its first fiscal quarter of 2023 which calls for 4% year-over-year growth. For FY 2023, investors must expect Netflix to generate only single-digit topline growth.

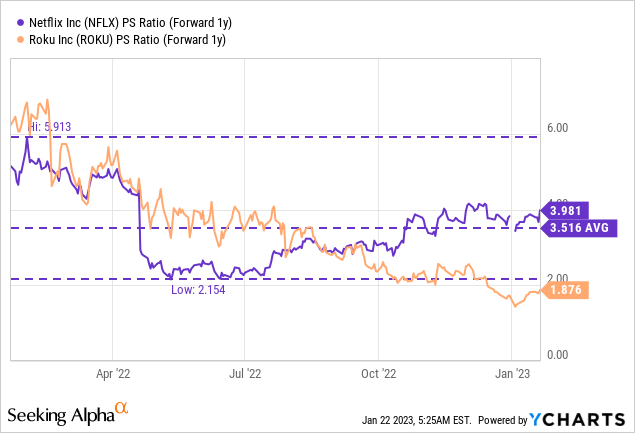

While Netflix reported a strong fourth quarter regarding global net subscriber additions, I believe the streaming company remains overvalued based off of revenues. Netflix’s revenue growth is moderating hard and although the high absolute number of net-adds in Q4’22 is a positive sign, it didn’t translate into nearly as strong revenue growth. Based off of revenues, Netflix is valued at 3.98 X revenues, more than twice as much as Roku, Inc. (ROKU). Shares of Netflix are also trading above their 1-year average P/S ratio of 3.52 X.

Risks with Netflix

The biggest commercial risk for Netflix is increasing competition in the streaming market accompanied by slowing topline growth, which could weigh on the company’s still high valuation factor. I also see a potential risk with Netflix’s new ad-supported tier resulting in subscribers down-grading their subscription plans longer term and, therefore, Netflix driving, at least to a certain extent, the cannibalization of its own subscriber base.

Final thoughts

Netflix’s Q4 2022 subscriber gains, although much better than expectations, were solid but, in my opinion, Netflix represents a bull trap here because robust subscriber growth has not translated to strong revenue growth. The 1.9% year-over-year revenue growth rate was actually quite disappointing.

Netflix faces stiff competition from a variety of media companies that are now running their own streaming offers, and the move to ad-supported format is not yet proven to be a success. The fourth quarter is also typically a good quarter for streaming companies due to the inclusion of a major holiday period and timed new releases of movies/series. I believe that the risk profile, given Netflix’s high valuation based off of revenues, remains unattractive, and I see more downside for the stock in FY 2023 than upside!

Be the first to comment