Wachiwit

After the market closes on Thursday, Jan. 19, the management team at streaming giant Netflix (NASDAQ:NFLX) is expected to report financial results covering the fourth quarter of the company’s 2022 fiscal year. Leading up to that time, management has offered a relatively tempered forecast. But analysts seem to be more optimistic. Truth be told, there might be some good rationale behind analysts’ views, but this also creates a risk that the company could underdeliver relative to what’s anticipated. In the long run, I fully suspect that Netflix will prove to be a decent opportunity for investors. But when you factor in these short-term problems with how shares are already priced, I just can’t get behind it from a bullish perspective.

Divergent expectations

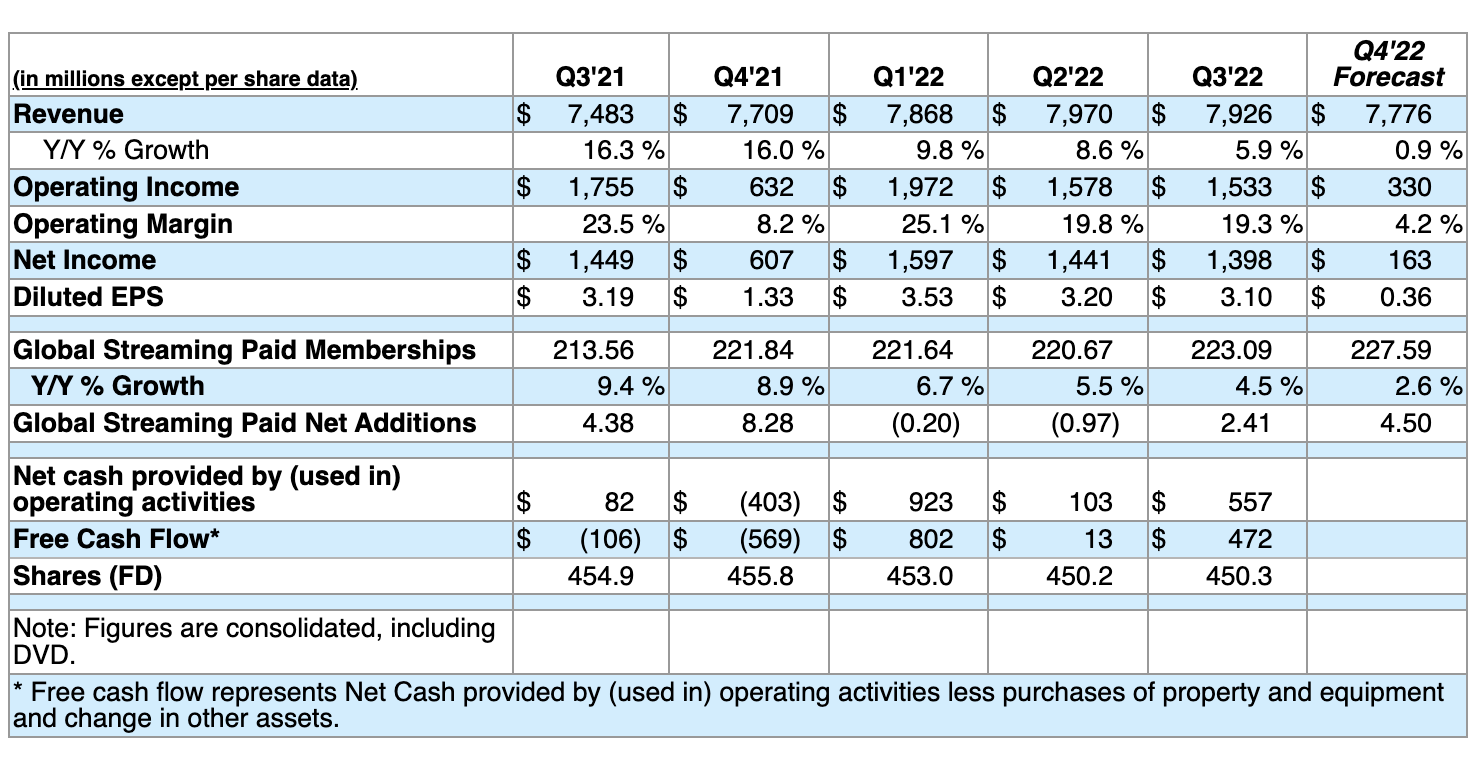

When management reported financial results for the company for the third quarter of its 2022 fiscal year last year, the company had both positive developments and negative developments. The most notable positive was the fact that overall subscriber numbers reported by the enterprise came in far higher than previously anticipated. Leading up to the earnings release, the company said that it would only have net additions for its global paid memberships of around 1 million.

The company ended up delivering 2.4 million net additions. This followed two quarters of weakness, some of which was driven by its exit from Russia. So for those who were already bullish about the company, it could be described as something of a boon. Even so, management did point to some concerns when it comes to the final quarter of the year.

Netflix

For starters, revenue has currently been forecasted at $7.776 billion. This would represent a year-over-year increase of only 0.9% compared to the $7.709 billion reported in the final quarter of 2021 and would come in spite of the fact that the firm is currently forecasting an additional 4.5 million net additions to its service for the quarter, bringing total membership to 227.59 million compared to the 221.84 million reported the same time one year earlier. The massive disconnect between expected revenue growth and net additions should be driven almost entirely by foreign currency fluctuations. To illustrate this, consider that revenue growth would have been around 9% on a constant currency basis.

You see, in its conference call for the third quarter, the company said that it anticipates around $1 billion in drag on revenue and $800 million in drag on operating profits coming from foreign currency fluctuations for the 2022 fiscal year in its entirety. The vast majority of this is expected to impact the company’s fourth quarter results. This all stems from a strengthening of the U.S. dollar. Interestingly though, the picture might not be so depressing. When management made this prognostication, the date in question was Oct. 18, 2022. From that point through the end of the year, the U.S. Dollar Index dropped 7.6%, with the decline through today being around 8.6%.

CNBC

The plunge in the dollar started occurring around early November and extended through the present day. This might be why analysts are currently more upbeat about the company than management was back then. At present, analysts think that revenue should come in at around $7.85 billion. Their expectations don’t stop on the top line. They also extend to the bottom line. The most recent forecast provided by management called for earnings per share for the final quarter to be around $0.36. This compares to the $1.33 per share reported one year earlier and would translate to net income of only $163 million.

Analysts, meanwhile, are currently forecasting earnings per share of $0.50, with that number growing to $0.54 per share on an adjusted basis. If the company does deliver on this, it could mean a nice bit of upside for shareholders in the near term. But it also creates expectations that might not be possible to meet. In addition to looking at earnings, investors should also pay attention to other profitability metrics.

Although no forecast has been provided by management, it would be wise when data is reported to compare both operating cash flow and EBITDA to what they were in the final quarter of 2021. For that period, these numbers totaled negative $403 million and $795.08 million, respectively. All of these metrics combined will prove instrumental in determining which direction shares move.

This uncertainty creates a certain amount of risk heading into earnings. But it also creates a certain amount of upside potential. When facing a situation like this though, I like to focus more on the long term and ask myself whether the company makes sense to buy into in general, not whether I can make a quick buck based on earnings. As I mentioned already, I suspect that Netflix will do just fine for itself in the long run. Having said that, I don’t think it’s the best player in this space to be invested in. Not by a long shot. Because of the nature of the firm’s net income and operating cash flow metrics, I have long viewed EBITDA as the most important metric for investors when it comes to this particular business.

Author – SEC EDGAR Data

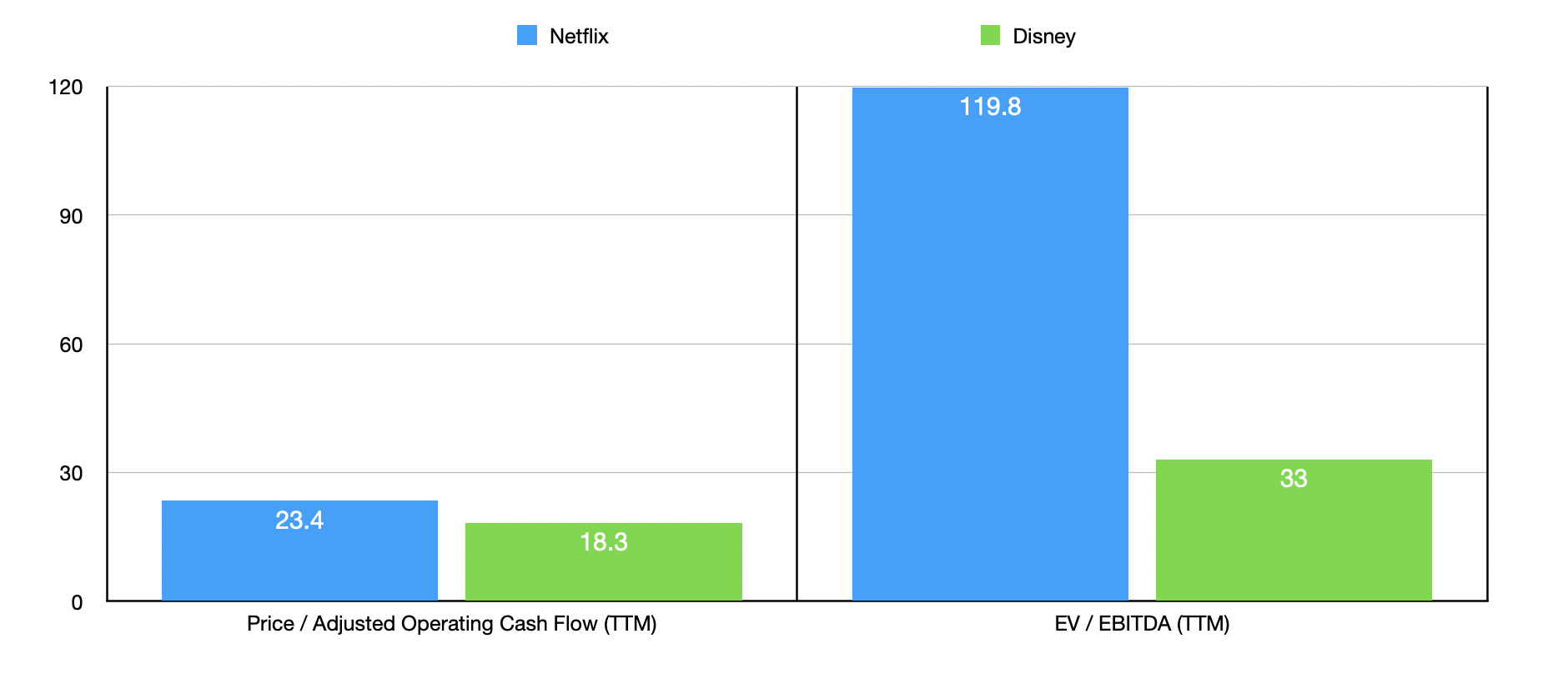

On a trailing 12-month basis ending in the third quarter, this figure came in at $6.54 billion. With an EV to EBITDA multiple of 23.4 right now, the company certainly does not look cheap. Not a pure play in the streaming market, there’s no denying that entertainment conglomerate The Walt Disney Company (DIS) is now the industry leader. By comparison, using the data from its most recently completed fiscal year, the company is trading at an EV to EBITDA multiple of 18.3. Even if we use the trailing 12-month operating cash flow data for both companies, the disparity is significant.

Disney is currently trading at a price to adjusted operating cash flow multiple of 33 while Netflix is trading at a multiple of 119.8. Although investors might argue that foreign currency troubles might be weighing only temporarily on Netflix, keep in mind that Disney has its own problems such as its theme parks and theatrical distribution operations that are only now just fully recovering from the pandemic.

Takeaway

Given what data is available to me, I believe it’s very possible that Netflix will have a better quarter than what management previously guided. This could be great for shareholders, especially if the company can beat the expectations set by analysts. But it also brings with it a certain amount of risk. Thinking about the picture long term, I suspect that the company will do just fine. But for those who want a truly high-quality operator with exposure to this space and that is experiencing even more rapid growth than Netflix has, there’s no denying that Disney is the better play and can be purchased at a far better price.

Be the first to comment