Ivan Pantic/E+ via Getty Images

“If you have wealth without liquidity, you’re still in bondage. If you have capital without currency, you’re still in bondage. Liquidity equals freedom.” – Hendrith Vanlon Smith, Jr.

Today’s piece is on a well-known name. After failing to sell itself in whole, the company is planning to split itself into two separate companies. The sell-off of the shares, thanks to the lack of a buyout, appears to be a trading opportunity given reasonable valuations. An analysis follows below.

Seeking Alpha

Company Overview:

NCR Corporation (NYSE:NCR) is an Atlanta based provider of automated teller machines, as well as services and software to the banking, retail, and restaurant verticals that include payment processing, self-checkout (SCO), and point-of-sale (POS) terminals. In September 2022, the company announced its intention to split into two companies: one focused on digital commerce and the other on ATMs, culminating a seven-month strategic review to enhance shareholder value. NCR was founded in 1884, initially went public in 1925, was acquired by AT&T (T) in 1991 and spun out in 1996 at ~$17.50 a share (on a when issued basis, adjusted for a 2-for-1 split). Shares of NCR trade for just under $23.00 a share, equating to a market cap slightly over $3 billion.

Current Reporting Segments

The company currently operates through five reporting segments: Retail, Hospitality, Digital Banking, Payments & Network, and Self-Service Banking. The first three segments will remain with NCR “Commerce Co” while Payments & Network and Self-Service Banking will be spun out as a separate publicly traded entity (“ATM Spin Co”) to existing NCR shareholders. The separation is expected to transpire near the end of 2023.

Retail offers POS, payment processing, inventory management, fraud and loss prevention, loyalty, and customer engagement solutions, as well as bar-code scanners and self-checkout terminals to retailers throughout the world. For the nine months ending September 30, 2022 (YTD22), Retail generated Adj. EBITDA of $299 million on revenue of $1.68 billion, comprising 29% of the company’s total topline. These metrics were down 7% and up 4% (respectively) versus the prior-year period.

Hospitality provides many of the solutions as its Retail counterpart, with an additional focus on ordering tablets for table-service, quick-service, and fast casual restaurants. It accounted for YTD22 Adj. EBITDA of $138 million on revenue of $687 million, representing 12% of total revenue plus 16% and 11% improvements over the YTD21, respectively.

Digital Banking offers financial institutions account opening, account management, transaction processing, and imaging solutions through software licenses and cloud service subscriptions. It was responsible for YTD22 Adj. EBITDA of $172 million on revenue of $404 million, or 7% of the NCR’s total topline, as well as 7% and 6% increases over YTD21.

Payments & Network provides financial institutions, fintechs, and neo-banks cash withdrawal and deposit access to their customers through its ATM network. It generated YTD22 Adj. EBITDA of $309 million on revenue of $967 million, representing 17% of NCR’s topline and 132% and 154% improvements over YTD21 (respectively), which were a result of its $2.5 billion (enterprise value) acquisition of ATM operator Cardtronics in 2Q21.

Self-Service Banking includes the sale and installation of ATM hardware and software to financial institutions and other businesses. The segment provided YTD22 Adj. EBITDA of $404 million on revenue of $1.93 billion, making it the largest contributor to the company’s topline at 33%. These metrics represented a 6% decrease and a 1% increase over the prior-year period, respectively.

Everything else that doesn’t add to (or adds over) 100% is netted out by two NCR categories: Corporate and Other; and Eliminations.

Separation Rationale and Share Price Performance

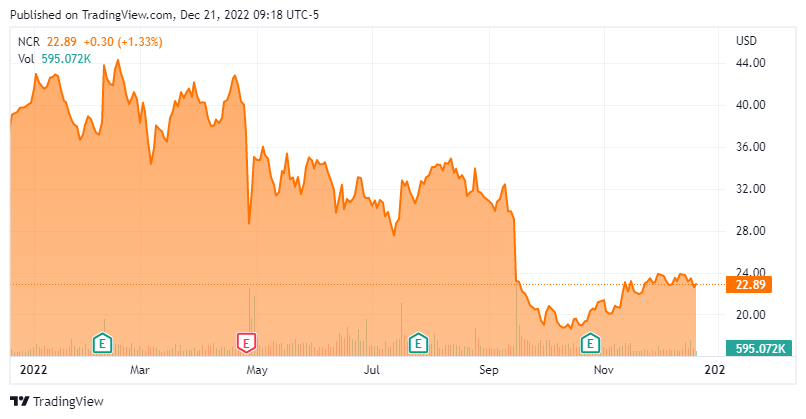

A beneficiary of the $4 trillion plus of pandemic-related aid packages, shares of NCR traded to an all-time high of $50.00 (after giving effect to its Teradata spinoff in 2007) in May 2021. However, as inflation fears began morphing into reality in early 2022, the market refocused on the fact that the company had grown its topline at a stagnate 2.5% CAGR (2012-2021) and its stock retreated back to the high-30s in Feb 2022, at which point management made the ‘seeking strategic alternatives’ announcement, sparking a one-day 14% rally to $43.78 a share.

In September 2022, the results of that review were to split the company in two, sold to its shareholder base as creating two best-in-class companies. ATM Spin Co will be the leading ATM-as-a-service provider and ATM network business worldwide. Commerce Co will continue to be a leading digital commerce business for retail, hospitality, and digital banking. Each concern will (supposedly) benefit from respective tailored capital allocation strategies with ATM Spin Co providing stable cash flows that would be returned to investors (presumably through dividends), while Commerce Co will look to grow through reinvestment of its cash flows. These differing strategies will attract distinct shareholder bases and drive value.

Once this strategic determination was announced, shareholders took it as a failure by management to find a suitor for its slow-growth concern. They did not see any value add from this move but rather dyssynergies: the split entities share customers and would now require duplication of corporate overhead. As such, the market voted thumbs down, selling shares of NCR down 20% in the subsequent trading session (September 16, 2022) to $23.20.

3Q22 Earnings & Outlook

The question now becomes whether the market’s response to NCR’s split announcement amounts to an overreaction. Some clue was provided by the company’s 3Q22 financial report of October 25, 2022 in which NCR posted earnings of $0.80 a share (non-GAAP) and Adj. EBITDA of $380 million on revenue of $1.97 billion as compared to $0.69 a share (non-GAAP) and Adj. EBITDA of $352 million on revenue of $1.90 billion, representing improvements of 16%, 8%, and 4%, respectively. The metrics look even better on a constant-currency basis: up 40%, 15%, and 18%, respectively. Recurring revenue increased 3% (7% on a constant currency basis) to $1.22 billion, or 62% of total. Non-GAAP gross margin fell 200 basis points to 26.7% as currency contributed 150 basis points of headwind. Adj. EBITDA margin expanded 80 basis points year over year to 19.3%. The improvements were more or less across all five operating segments on a constant currency basis with only Self-Service Banking unable to generate double-digit year-over-year growth in either revenue (up 6%) or Adj. EBITDA (up 1%).

The non-GAAP bottom line beat Street consensus by $0.02 a share while the topline was $30 million shy.

Management did provide FY22 guidance in April, expecting non-GAAP earnings in the range of $2.70 to $3.20 a share and $1.45 billion of Adj. EBITDA (based on a range midpoint) on revenue of $8.0 billion. Instead of readjusting those metrics, it said that short of the unforeseen strength in the dollar, these forecasts would still be in play. NCR also stated that it expects somewhat of a repeat of 3Q22 in 4Q22.

Balance Sheet & Analyst Commentary:

Management did not make any forecasts specific to FY23, only to say that it expects to generate anywhere from $500 million to $800 million in free cash flow between the end of 3Q22 and separation (YE23). That said, the company has experienced negative $38 million of free cash flow in YTD22 as supply chain challenges have resulted in uneven revenue generation, necessitating an investment in working capital. However, management expects that dynamic to abate significantly over the upcoming quarters. Net leverage, currently at 3.9 – debt of $5.7 billion and cash of $434 million – should improve over FY23 as the company anticipates using ~$450 million of its expected free cash flow to pay down debt. NCR does not pay a dividend and has not repurchased shares in 2022, although management indicated that some of its future free cash flow could be earmarked for buybacks.

Analysts were not that sanguine on the quarter, citing factors beyond the company’s control (such as currency and a poor macro backdrop) as reasons to be less bullish. Specifically, Morgan Stanley (MS) – who had downgraded the stock from an outperform to a hold just after the separation announcement – lowered its price target from $27 to $24 a share. Stephens maintained an outperform rating but lowered its price objective from $38 to $28 and then raised that to $32 two weeks ago. D.A. Davidson reiterated a buy but reduced its price target from $45 to $35. Royal Bank of Canada lowered its price target back in April from $54 to $44.

On average, they expect the company to earn $0.80 a share (non-GAAP) on revenue of $2.0 billion in 4Q22, bringing FY22 expectations to $2.59 a share (non-GAAP) on revenue of $7.85 billion. Analysts then anticipate NCR earning $3.03 a share (non-GAAP) on revenue of $8.08 billion, representing improvements of 17% and 3%, respectively.

Board member Joseph Reece thought that the company’s current outlook versus price warranted an investment, buying 5,000 shares at $20.82 on November 9, 2022.

Verdict:

Mr. Reece likely noticed an opportunity to invest in a company trading at a 7.2 PE ratio on FY23E earnings with bottom line growth projected at 17%. Price-to-FY23E sales of under 0.4 also likely caught his eye.

That said, with the separation still 13 months off, there will be continuing uncertainty as to whether NCR’s management can unlock any value from this move. For the avoidance of doubt, the company did provide some financial statement metrics for the separate companies, but no one yet seems convinced as to the soundness of this move. However, that pessimism is priced in, and with a long window for the company to still be acquired pre-split, there exists the possibility of a significant upside. With the stock down over 50% from its all-time high, reasonable valuations – especially considering its current bottom line growth prospects for FY23 – and good option liquidity make NCR a solid covered call candidate.

“Cash is King. Information is his twin.” – Sotero M Lopez II

Be the first to comment