IherPhoto

I don’t typically discuss defense companies, but the segment has grown to about 10% of my portfolio holdings. The five defense stocks I own are Lockheed Martin (LMT), General Dynamics (GD), Raytheon (RTX), Northrop Grumman (NOC), and Spirit AeroSystems (SPR). Each of these companies is appealing for its unique reasons. Still, they also have a significant bullish factor that should contribute to higher revenue growth and substantially higher-than-expected profitability in future years. Therefore, the stocks of these top defense companies should appreciate considerably as we advance.

It’s Not Just a War in Ukraine

The war in Ukraine is not just a war in Ukraine. It is a barbaric invasion of a peaceful nation that’s led to devastation not seen since World War Two. Unfortunately for Ukraine, a proxy war is being waged on its land with no end in sight. The West sends more and more munitions to help Ukraine, which should draw out this conflict which may last for years, decades even. The U.S. has already provided around $50 billion in military aid (officially) and will probably give much more before this war is over.

Moreover, it’s not just Ukraine or Eastern Europe, everyone wants better defense capabilities now, and that trend is likely to continue. More countries are spending more significant portions of their GDPs on increasing their defense capacities and military presence. Additionally, with Russia’s belligerent actions, more governments are taking a stricter stance against the rogue nation by ordering more advanced military technologies from top U.S. defense contractors.

Market participants may be underappreciating the seriousness of the current geopolitical atmosphere. Moreover, many analysts could be behind the curve regarding future revenue growth and earnings potential for top U.S. defense companies in the coming years. My top five defense stocks are relatively cheap, recently had significant corrections, and should appreciate considerably as we advance.

1. Lockheed Martin

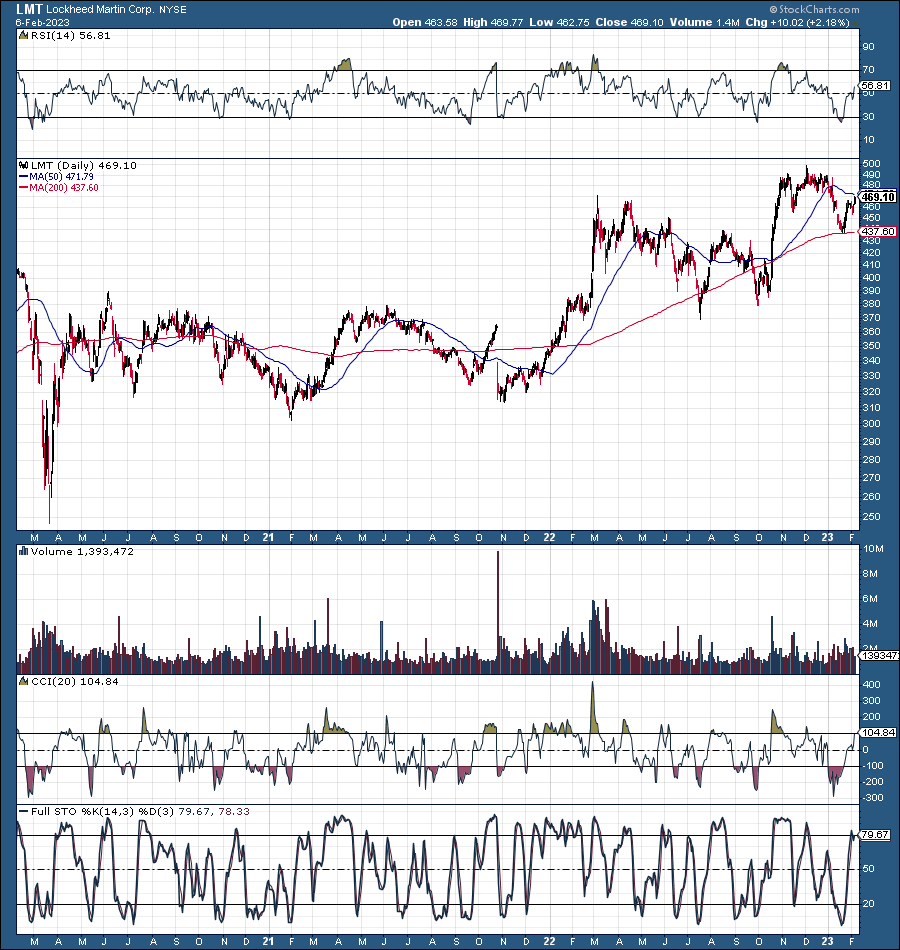

LMT (StockCharts.com)

Do you know what has shown great success in Ukraine? Lockheed’s HIMARS is likely the single most important weapons system to help turn the tide of war in Ukraine’s favor. Therefore, the Ukrainian people are likely grateful, but they need more, not just HIMARS. Lockheed is a giant defense contractor with a market cap of about $120 billion. The company makes everything from armored vehicles to planes, helicopters, battleships, and much more. I am amazed that one defense company produces this much diversified military hardware, which is truly impressive.

The consensus estimate on the street is for roughly $66 billion in revenues this year, and the company should provide about $27 in EPS. Therefore, Lockheed is trading at only around 17 times this year’s EPS. While this may not be cheap, some analysts may need to consider how much additional spending may go to top hardware producers like Lockheed and others. Therefore, Lockheed and other op U.S. contractors could outperform the downbeat estimates in the coming quarters and years.

Also, LMT’s chart is quite constructive. The stock has roughly doubled from the 2020 bottom, and after a prolonged (2-year) consolidation phase, LMT can continue moving higher in future years. Many nations can look to Lockheed to advance their safety needs in this volatile and unpredictable geopolitical environment.

2. Raytheon

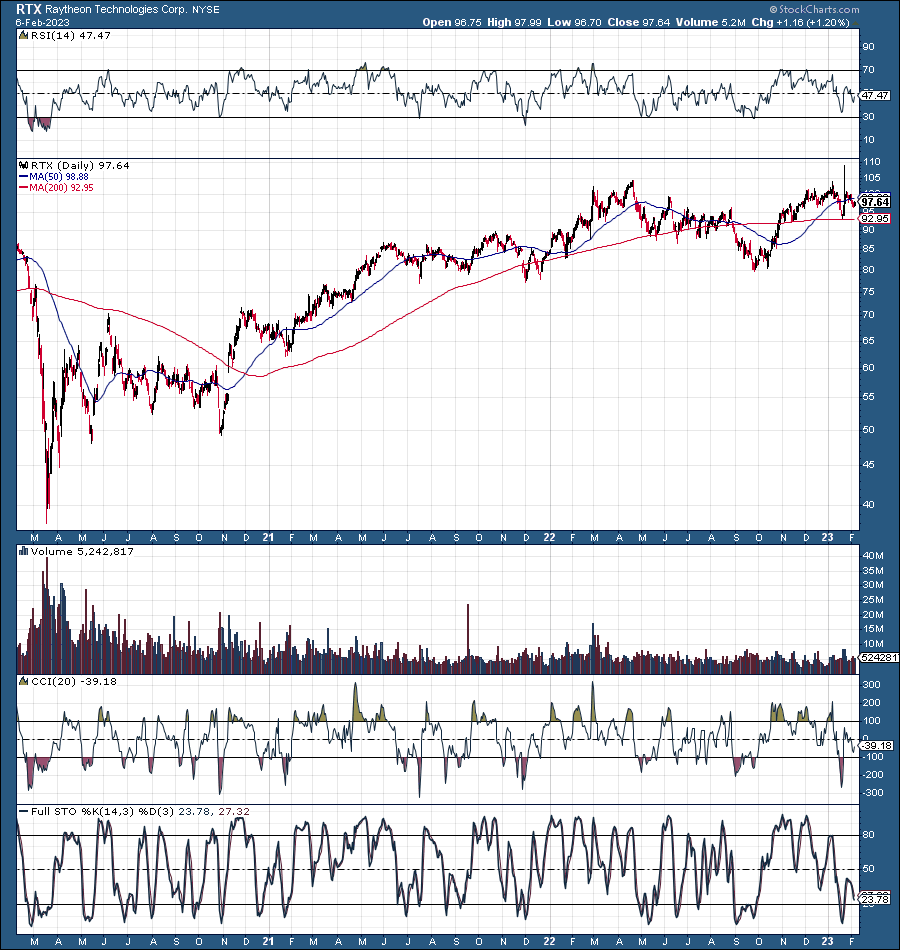

RTX (StockCharts.com)

Raytheon is the creator of the Tomahawk cruise missile and an abundant array of other missile and defense technologies. The company is regarded as one of the top specialists in its expertise areas globally and is valued at approximately $140 billion. Moreover, Raytheon trades below 20 times this year’s EPS estimates and is expected to grow revenues and EPS steadily in the coming years.

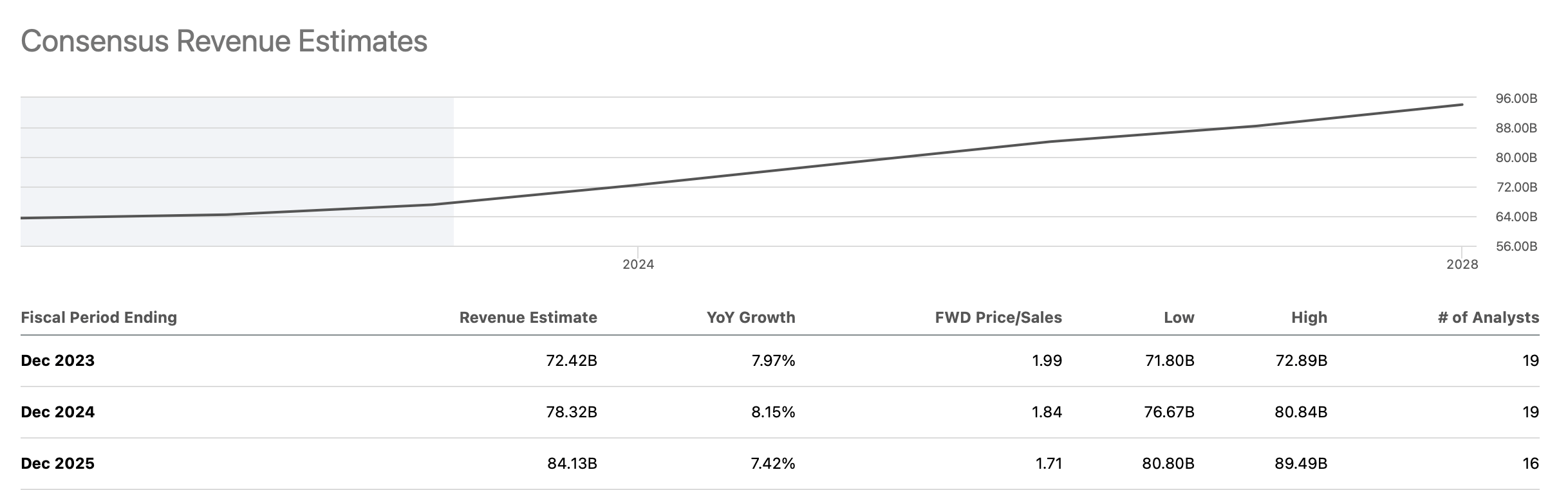

Raytheon’s Revenue Estimates – Likely to Rise

Revenues (SeekingAlpha.com)

Consensus revenue estimates are around $72.5 billion this year and roughly $80 billion next year, with approximately a 10% YoY revenue growth rate. Raytheon’s revenue and EPS estimates could be too low here. The transitory slowdown should not impact the business of Raytheon or any other major defense company. Furthermore, some analysts still need to get up to speed on quality defense stocks. Technically, the stock has been consolidating around the $100 level for roughly a year and will likely break out to new highs as demand for defense equipment globally increases in the coming years.

3. Northrop Grumman

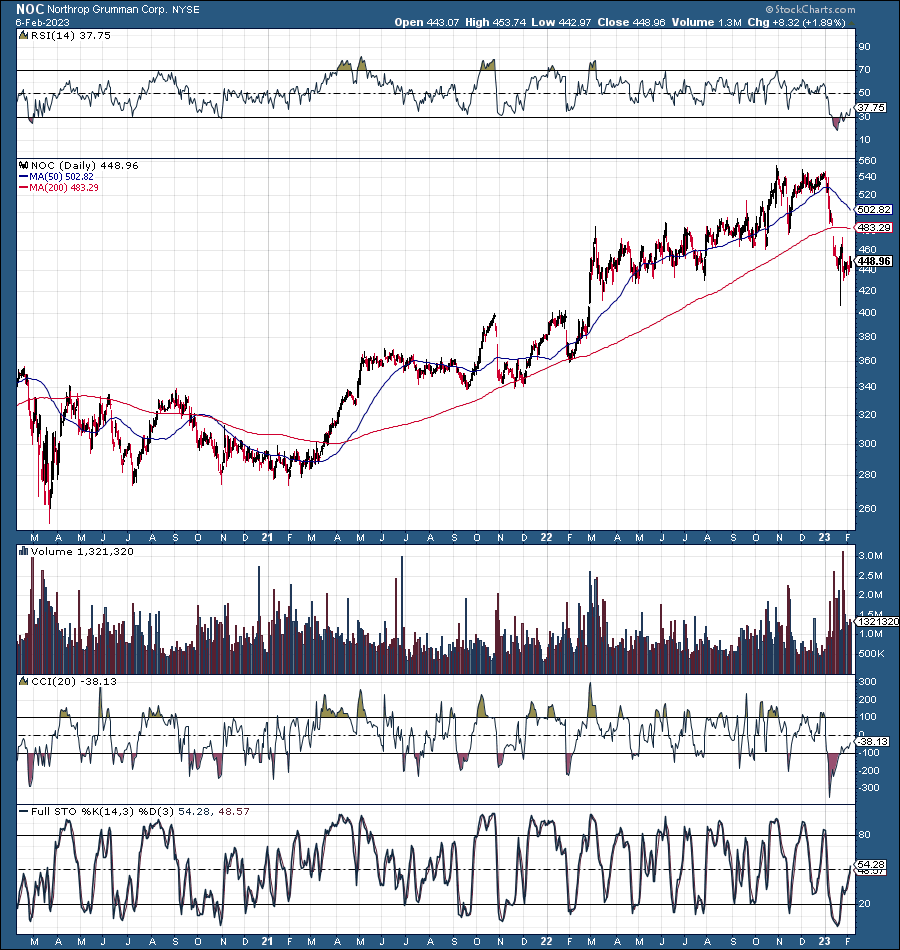

NOC (SeekingAlpha.com )

Northrop is on the cutting edge of missile systems and other advanced technologies. Moreover, the company makes significant advancements in AI and machine learning, providing it with an edge over some competitors. Furthermore, the stock had a significant pullback, making shares much more attractive at current levels.

Northrop’s forward P/E ratio is down to 18 now, relatively low considering the company’s expected 11% EPS growth rate. Moreover, Northrop can do better, and consensus analysts’ figures may be substantially lower than future earnings results indicate. Therefore, Northrop is a strong buy after the 25% pullback, and I suspect this stock can go significantly higher in the coming years.

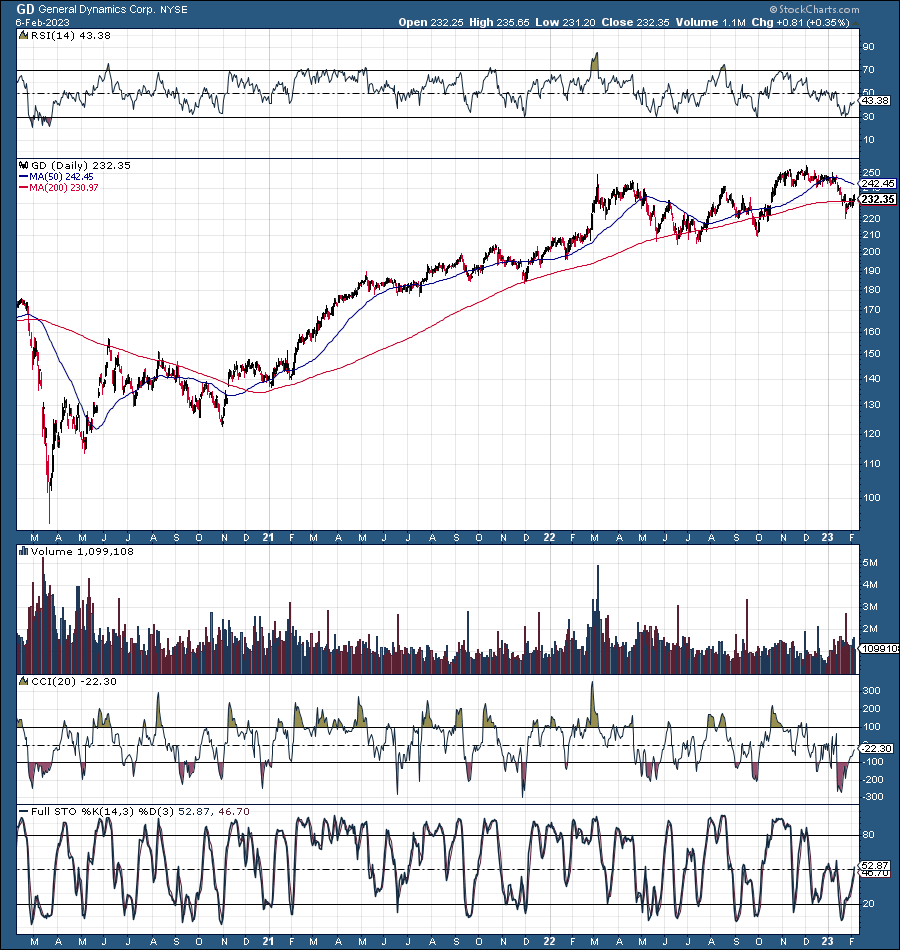

4. General Dynamics

GD (StockCharts.com)

General Dynamics is a highly versatile and capable company. Its systems are present on land, sea, air, and space, and this company has fantastic potential. The stock appears very bullish and should break out above $250 soon. We also see a nice uptrend along with the upward 50 and 200-day MAs. Additionally, GD just touched down on the critical 30 RSI level. This dynamic implies that the stock became extremely oversold and will probably rebound and move higher soon.

Furthermore, General Dynamics is fundamentally powerful. General Dynamics is worth around $63 billion and has exceptional growth and earnings potential ahead. Next year’s EPS estimates are around $15, illustrating that the stock is trading at just a 15-forward P/E ratio.

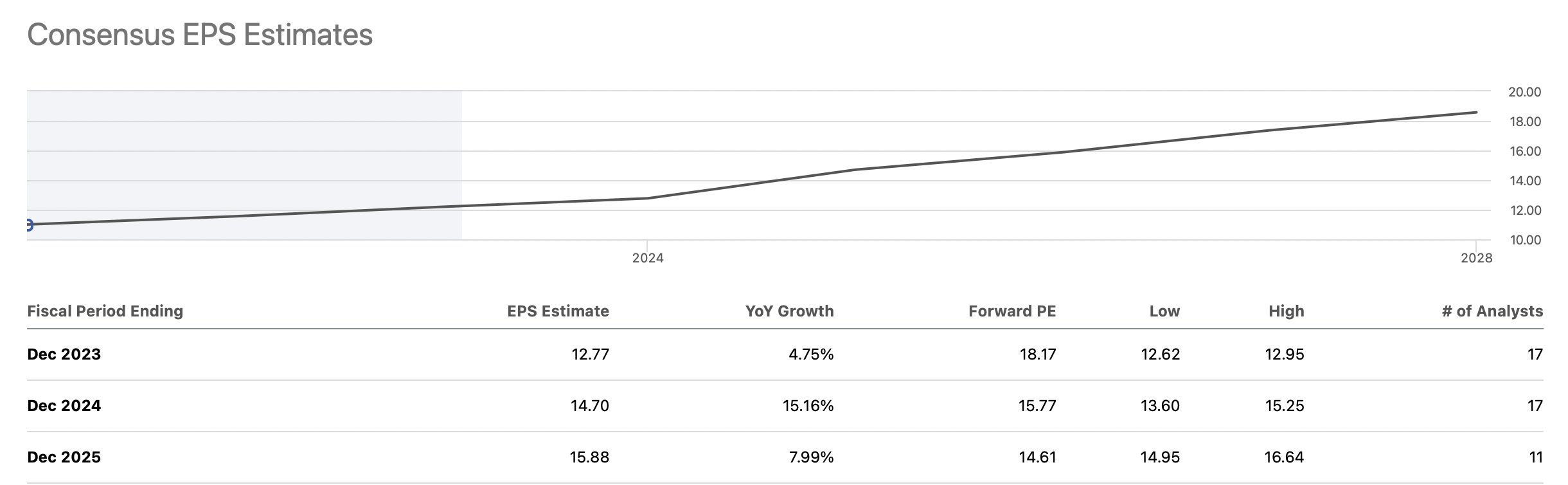

EPS Estimates Will Likely Rise

EPS estimates (SeekingAlpha.com)

General Dynamics and other top defense companies can increase their earnings more than expected due to higher defense spending that the market is not pricing in yet. Higher earnings revisions could arrive soon, sending GD and other defense stocks significantly higher.

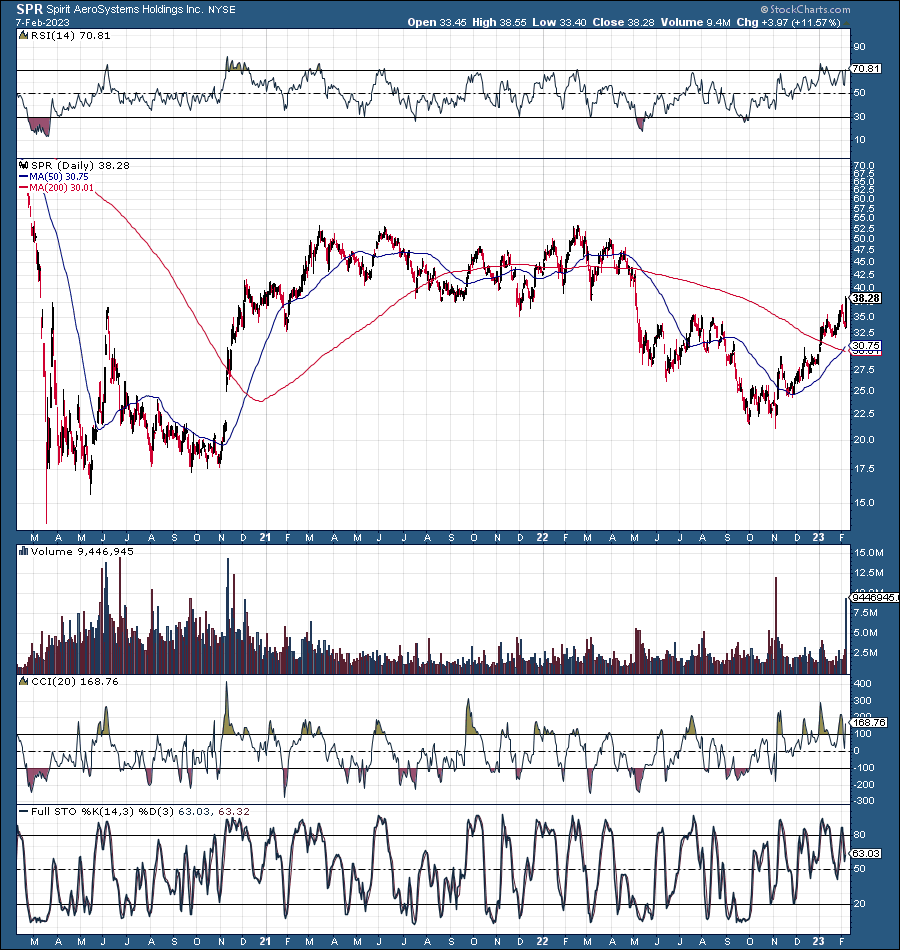

5. Spirit AeroSystems

SPR (StockCharts.com)

Spirit AeroSystems is one of my favorite defense stocks, especially as a long-term play. Spirit’s business has been correlated with Boeing’s (BA), and its stock price suffered accordingly in previous years. However, now that Boeing is bullish again, Spirit’s business likely has a substantial upside. Spirit is a small-cap company worth around $3.6 billion now, yet the company has remarkable potential.

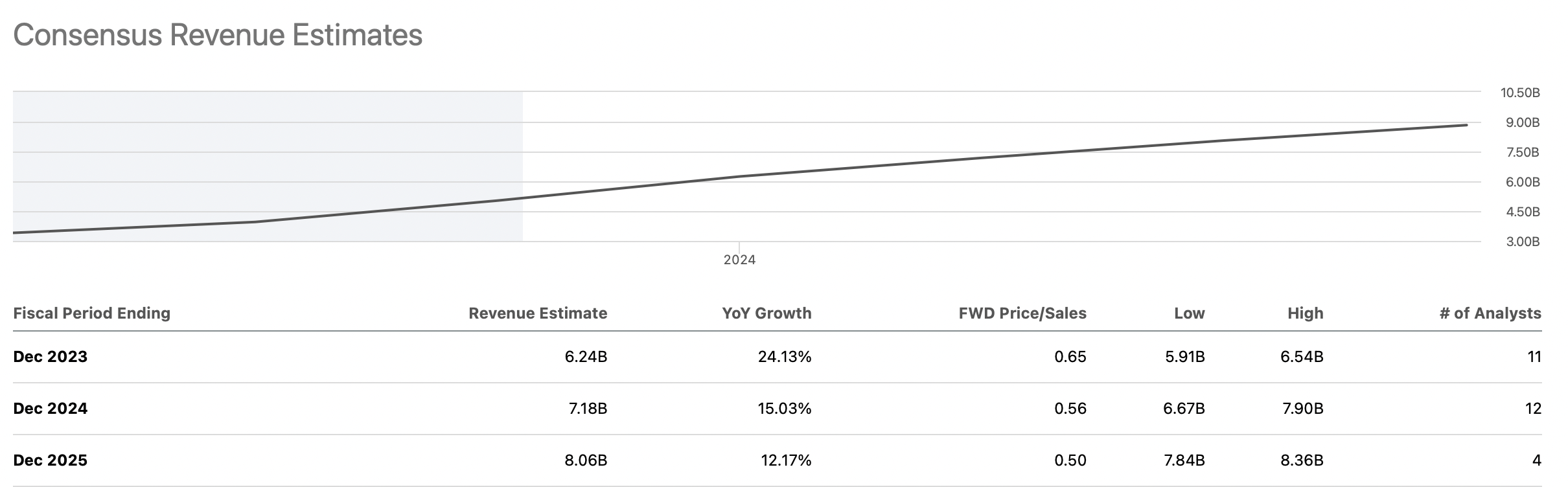

Revenue Estimates – Substantial Growth to Continue

Revenues (SeekingAlpha.com )

We see significnat double-digit revenue growth likely to continue at SPR, and the company could get to $10 billion in revenues annually quicker than most analysts predict. Spirit delivers specific components for the commercial, defense, and space industries. Therefore, the company should witness increased demand as we move forward in the new age of higher defense spending. Spirit’s technical trajectory is solid, and given the current revenue growth and earnings power potential, Spirit’s stock could be at $60-$75 a year from now.

Additionally – As a Bonus, You Get Growing Dividends With Many Defense Stocks

Be the first to comment