The trust will remain in existence until the later to occur of (1) June 30, 2026, or (2) the time when 14.4 MMBoe have been produced from the underlying properties and sold (which amount is the equivalent of 11.5 MMBoe in respect of the trust’s right to receive 80% of the net proceeds from the underlying properties pursuant to the net profits interest).

“The trust will dissolve prior to its termination if:

the trust sells the net profits interest; annual cash proceeds received by the trust are less than $1 million for each of two consecutive years;

the holders of a majority of the outstanding trust units vote in favor of dissolution; or

there is a judicial dissolution of the trust.

Upon dissolution, the trustee would then sell all of the trust’s assets, either by private sale or public auction, and distribute the net proceeds of the sale to the trust unitholders.

Performance

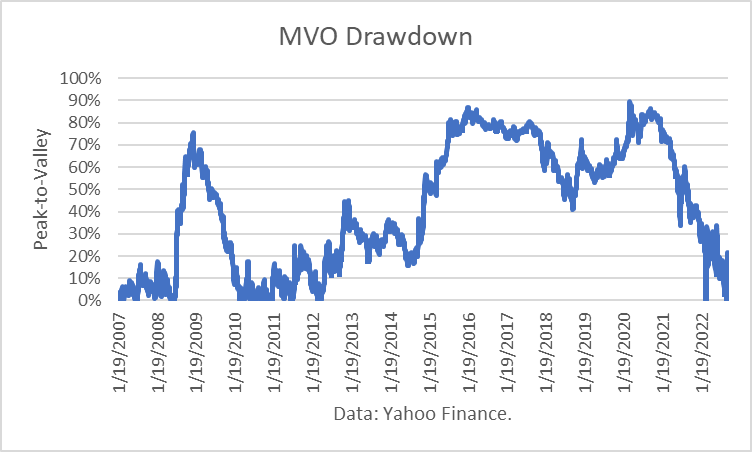

The total return of MVO from inception (January 2007) was 239%, including the surge in crude oil prices in 2022.

Yahoo Finance data

However, the Maximum Drawdown (“MD”) was 89%. I view the MD as the primary risk measure because it quantifies how much an investor could have lost from its peak valley. Investors often exit positions when losses exceed risk tolerances, locking in the loss. An MD of 89% implies that the product is not suitable as a long-term investment.

Yahoo Finance data

I recently wrote an article, VOC Energy Trust: A Pure Play In Crude Oil Price Exposure. MVO and VOC Energy Trust (VOC), VOC are both limited trusts run by Vess Oil. As is the case for VOC, MVO is mainly a pure play on crude oil prices.

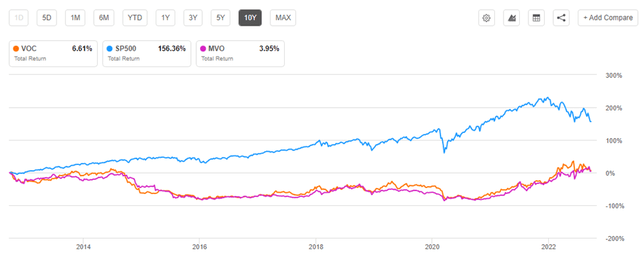

Over the past ten years, MVO and VOC had a total return of single digits. That compares to the S&P (SP500TR) return of 156.4%.

Seeking Alpha

Dollar-Oil Illusion

In my article about VOC, I discussed the crude oil market fundamentals in terms of supply, demand, imports, exports and inventories. Following my VOC article, a reader referred me to another article entitled, The Energy Report: Decouple Worries, dated September 28, 2022, in which the author states:

You don’t have to worry about oil fundamentals, you just have to worry about the value of the dollar and that is a very safe way to look at the market until it isn’t.”

There is a lot of confusion about the relationship between the value of the dollar and oil prices. The media compounds the problem by citing the change in the dollar as the reason for the crude price change in daily reports.

I had previously published an article on Seeking Alpha titled, The Dollar-Crude Oil Price Illusion, in which I wrote:

Classical economics explains how exchange rates are determined by the interconnections among interest rates, inflation, the economy, balance of payments and expectations. Oil prices factor into that equation. The oil price is sometimes a big factor, and at other times, not.”

Within my article, I published results of two trading simulations:

Using the dollar as a signal for crude price in the next month

Using the crude price as a signal for the dollar in the next month.

I performed these simulations by first performing a “best-fit” regression between the trade-weighted value of the dollar (from the Federal Reserve’s “FRED” database) and the WTI crude oil price (next month). I then set up a trading simulation. Using the regression equation, I predicted the price of oil in the next month, knowing the value of the dollar this month. I went 100% short if the predicted price was lower than the current price, and vice-versa. Using the dollar as a trading signal for crude oil resulted in a loss.

I developed another trading strategy: using the price of oil to predict the value of the dollar. As above, I developed a regression using the oil price one month ahead to predict the value of the dollar. As above, I compared the predicted value of the dollar to the actual current value. If the dollar was predicted to go lower, the strategy went short, and vice-versa. That strategy produced a trading gain.

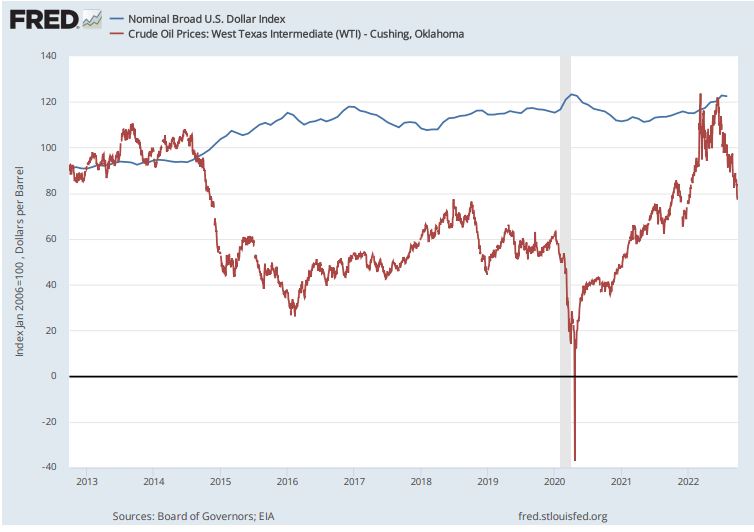

The trading period was from June 2014 through May 2016. I lengthened the period to go monthly from September 2012 through August 2022. As shown below, the dollar and WTI had fairly low correlations over the 10-year period (i.e., the r-squared in both regressions is around 38%).

FRED

FRED

FRED

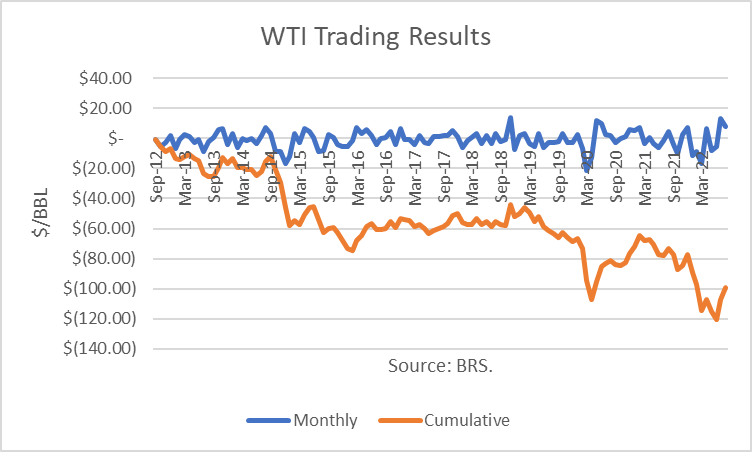

Trading WTI using the dollar signal from the month before yielded a loss of $99.41/bbl over the 10-year period.

BRS

Whereas trading the dollar using the WTI signal had a gain of $4.39 over the same period.

BRS

Admittedly, both trading strategies are simplistic. However, the result of a huge loss trading WTI and a modest gain trading the dollar provides evidence that WTI leads dollar changes, rather than the dollar signaling WTI changes.

Conclusions

MVO is an energy trust which is almost entirely exposed to crude oil prices. For investors who want that exposure without trading an oil futures market account, it is a suitable alternative. However, as noted above, it is not a suitable long-term investment because it has returned too little and has been subject to an excessively-large drawdown.

As I concluded in my VOC article, the oil market has shifted since Russia’s invasion of Ukraine in February. High oil and natural gas prices, especially in Europe, have created major risks of economic recessions. And the most recent rises in interest rates to combat inflation adds to the risks. Therefore, petroleum demand has dropped and inventories have adjusted along with trade flows.

However, there is an OPEC meeting on October 5th, and there have been reports that Russia is backing a production cut of one million barrels per day. In August, the Saudi energy minister hinted that a production cut may be in order to stabilize prices. So such a cut could support oil prices short term.

Regarding the dollar, the data and a simple trading test show that WTI is a leading indicator of the dollar, instead of the dollar being a leading indicator of WTI. And so my conclusion is not to “worry about the value of the dollar.”

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment