z1b/iStock via Getty Images

Investment Thesis

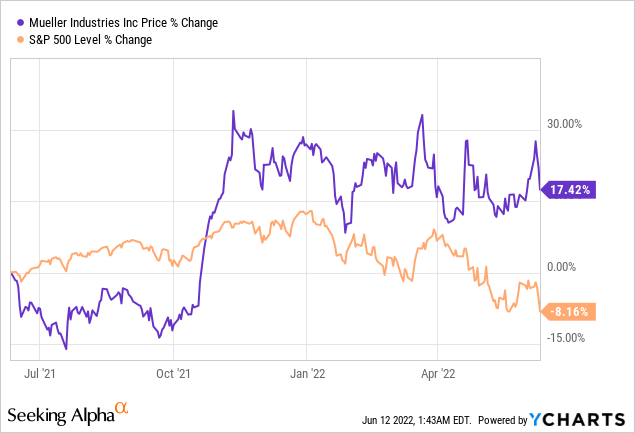

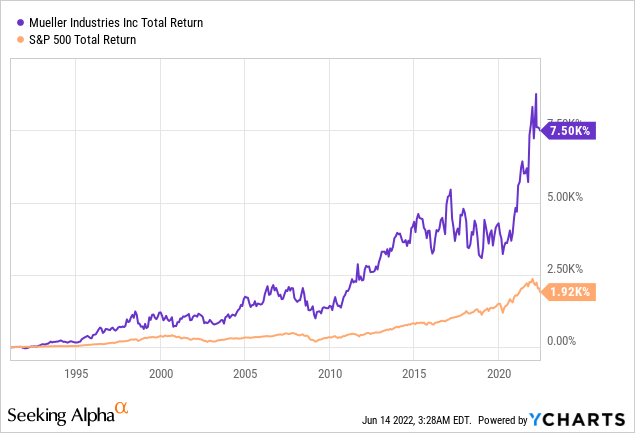

Mueller Industries Inc. (NYSE:MLI) is a small-cap dividend-paying company that has consistently performed well for over a century. It has almost doubled its share price in the previous 3 years, outperforming the market in the previous 1 year and YTD.

The company’s strong profitability, high growth prospects, attractive valuation metrics, optimal resource utilization, fortified balance sheet, and low volatility indicate a desirable investment opportunity.

The Company

The company manufactures and sells copper, brass, aluminum, and plastic products throughout North America, Mexico, Great Britain, South Korea, the Middle East, and China. Its three revenue-generating segments are:

- Piping Systems: It manufactures and distributes copper tubes, fittings, line sets, a complete line of products for PEX plumbing and radiant systems, pipe nipples, and copper-based joining products globally. Its primary customers are wholesalers in the plumbing and refrigeration markets, distributors to the manufactured housing and recreational vehicle industries, building material retailers, and air-conditioning OEMs. It accounted for 69% of total sales for Q1 2022.

- Industrial Metals: It manufactures and sells brass rods, bars and shapes, aluminum and brass forgings, aluminum impact extrusions, gas valves and assemblies, specialty copper, copper alloy, and aluminum tubes. Its primary customers are domestic OEMs in the industrial, transportation, construction, heating, ventilation, air-conditioning, plumbing, refrigeration, and energy sectors. It accounted for 17% of total sales for Q1 2022.

- Climate: It manufactures and sells refrigeration valves and fittings, high-pressure components, coaxial heat exchangers, and insulated HVAC flexible duct systems and line sets. Its primary customers are in the heating, ventilation, air-conditioning, and refrigeration markets in the United States. It accounted for 14% of total sales for Q1 2022.

Housing Market

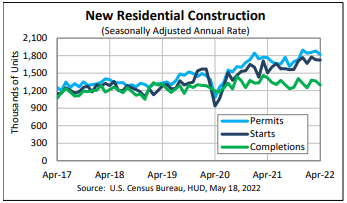

The nature of the company’s products makes it deeply correlated with the residential and commercial construction and repair and maintenance markets. The company reported in its Form 10-Q that the seasonally adjusted annual rate of new housing starts in March 2022 was 1.79 million. This has since been revised down to 1.724 million amid concerns of soaring inflation, 12-year high mortgage rates, elevated building material costs, persisting supply constraints, an uncertain economy, and a looming threat of a recession.

Despite this slight decline, the housing starts are levitating at their highest since the economic crisis in 2008, and even if there is a forecasted decline for the upcoming year, the current facts and figures support a strong growth opportunity for MLI in 2022. Any upcoming concerns about the housing market are likely to be short-lived, and the long-term market prospects are still expected to be booming.

U.S Census Bureau

Source: Census.gov

Commodity Pricing

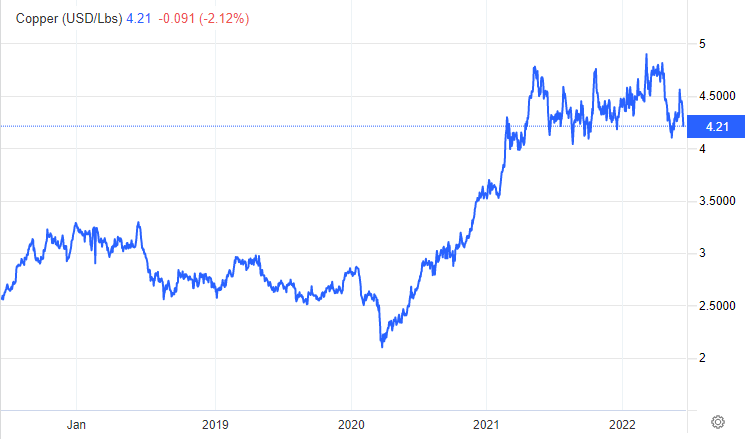

Additionally, since MLI uses the FIFO method to dole its inventory and passes on raw material costs to its customers, the pricing surge in the copper and brass commodity market is also extremely favorable to the company. The commodity prices experienced high YoY growth in 2022, integrally contributing to the 23.4% YoY sales growth, but copper prices have declined in Q2 and are expected to stay depressed, limiting the high spreads enjoyed by Mueller.

Trading Economics MLI Form-10Q

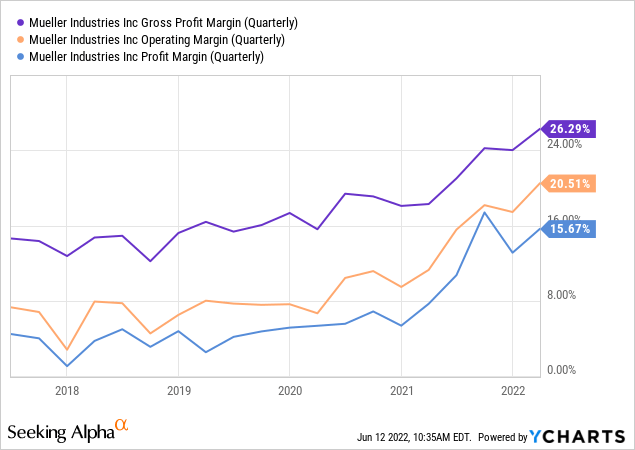

Mueller Industries has been operating a profitable business for decades but has been increasing its profitability since late 2019 after a depressing previous decade in the wake of post-pandemic pricing hikes. The gross margin grew from 18.3% to 26.3% YoY in the MRQ, pushed by higher selling prices, also elevating operating and net margins.

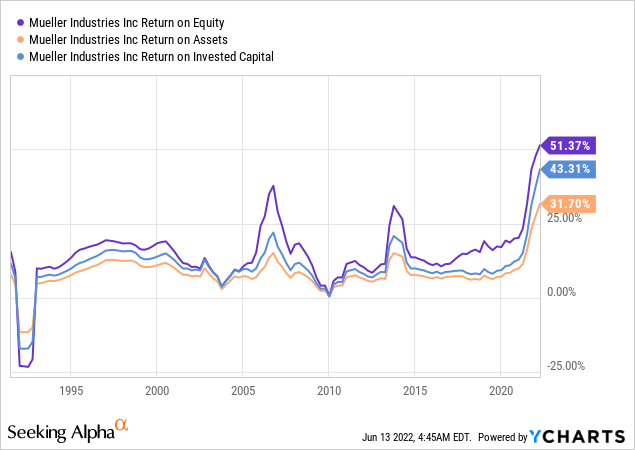

This increase in recent periods has also pushed the company’s resource utilization metrics to all-time highs, with ROE at 51.4% and ROA at 43.3%, considerably higher than the industry medians. These returns and profitability margins have resulted in the stock being traded at attractive valuation metrics because of the market downturn.

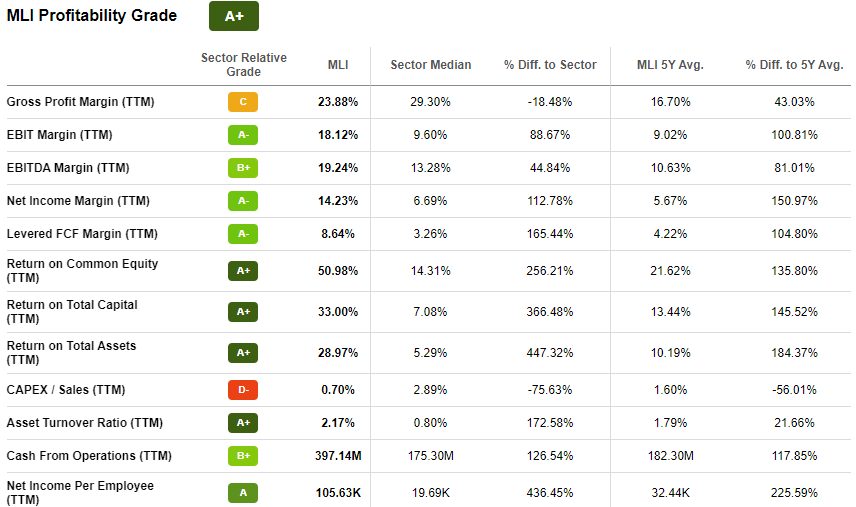

The company’s Seeking Alpha Profitability tab is a green oasis because of its exceptional profitability metrics. If the commodity prices remain flat, which is highly unlikely because of the highly volatile macroeconomic conditions fueled by geopolitical tensions, the company’s profitability will undoubtedly go down, but not enough to show any kind of YoY decline. However, since copper is a leading indicator of economic health, the high prices point to strong market demand for the benefit of Mueller.

Seeking Alpha

Debt & Liquidity

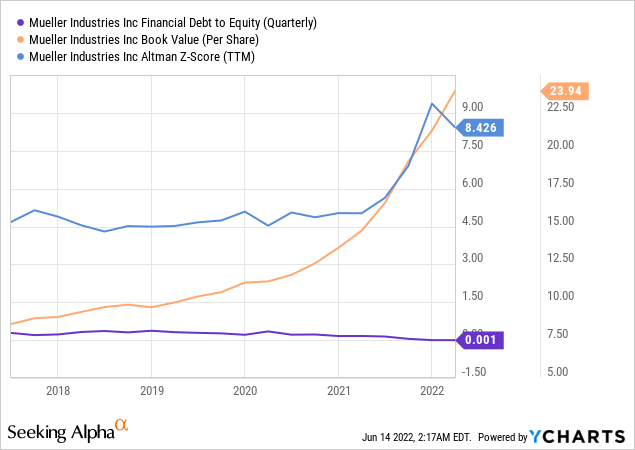

The company has an almost debt-free balance sheet, sequentially improving book value per share, and an exceptional Altman Z score of 8.04, testifying its strong financial position.

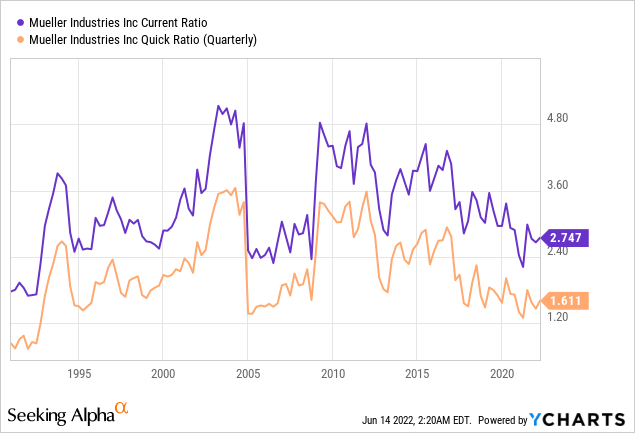

Its Levered FCF has grown over 4.6 times YoY in the MRQ, and the Levered FCF margin of 8.64% is 165% higher than the industry median of 3.26%, adding to its current ratio of 2.75 and Quick ratio of 1.61, indicating that the company has ample resources to settle its short-term obligations with ease. Mueller has a long history of efficient resource utilization and maintaining a strong balance sheet.

Valuation Metrics

The year 2022 hasn’t been kind to the financial markets, but the recent price declines have led to stocks attaining attractive valuations. MLI is currently trading at below its 5-year average relative valuation metrics despite being at a high financial stature. The company’s P/E, P/S, and P/B ratios of 5.54x, 0.78x, and 2.29x are almost 70%, 42.5%, and 6% lower than the industry medians.

The stock appears severely undervalued, with a price tag of at least over $100 when applying the company’s metrics to its 5-year average and the industry medians. However, that seems unlikely when factoring in the macroeconomic risks. Although the rewards of potential long-term upside still outweigh the downturn risks, especially considering that the company has operated for over 100 years, triumphing over extreme economic crises, including the world wars and the great depression.

Since the share price has been levitating around an all-time high since late 2021, we’re in uncharted territory on how high the stock can go. If the current trajectory persists, a $100 price per share isn’t out of the question by the next 12 months.

Conclusion

I have tried to isolate a brief and clean assessment of Mueller Industries in this article because of its long history of trampling through idiosyncratic risks and creating wealth with a substantial premium to the market. In the previous 3 decades, the company’s total returns have outmatched the market by a wide margin, and it is likely to keep doing that because of its strong and consistent performance in delivering an economic staple.

Add in the $1 quarterly dividend per share with a yield of 1.82%, and even though it is not much, it still adds a lot of value when considering the long-term holding of a growth stock.

The company might face difficulties in maintaining its profitability if the housing and the commodity pricing market experience serious downturns in the wake of the upcoming macroeconomic uncertainties. Still, given its long and strong history, I expect the company to endure these tribulations.

I rate the stock as a buy because the long-term buy-and-hold rewards of the company far outweigh the risks despite factoring in the short-term risks of the upcoming threats of a recession.

Be the first to comment