MattoMatteo

MSC Industrial Direct Co., Inc. (NYSE:NYSE:MSM) is a small-cap industrial with a high-quality business model whose common shares have been trapping the bear by outperforming the broader market for three years, including the 2022 bear market.

By focusing investment research on the fact-based current wealth of companies and the present value of their representative shares instead of unreliable predictive analysis and speculative growth, the holdings of our family portfolio have collectively outperformed the broader market since 2009.

In this initial primary ticker research report, I put MSC Industrial Direct and its Class A common shares through my proprietary, data-driven investment research checklist of the value proposition, shareholder yields, fundamentals, valuation multiples, and downside risk.

The resulting investment thesis:

Although MSC Industrial Direct’s value proposition, fundamentals, and downside risks are compelling, MSM’s yields and valuation multiples relative to cash flows suggest the stock may now be trading at fair value.

My current overall rating: Hold, based on a bullish view of the company and a neutral view of the stock.

Unless noted, all data presented is sourced from Seeking Alpha Premium as of the intraday market on November 14, 2022; and intended for illustration only.

Small-Cap Industrial Stock Trapping The Bear

MSM is a dividend-paying small-cap stock in the industrials sector’s trading companies and distributors industry.

MSC Industrial Direct Co., Inc., with its subsidiaries, distributes metalworking and maintenance, repair and operations [MRO] products and services in the United States, Canada, Mexico, and the United Kingdom. MSC Industrial Direct Co. was founded in 1941 and is headquartered in Melville, New York, USA.

My value proposition elevator pitch for MSC Industrial Direct:

In this bear market, underfollowed small-cap MSC Industrial Direct has been outperforming the broader market distributing metalworking and maintenance, repair and operations [MRO] products and services with growth and profitability.

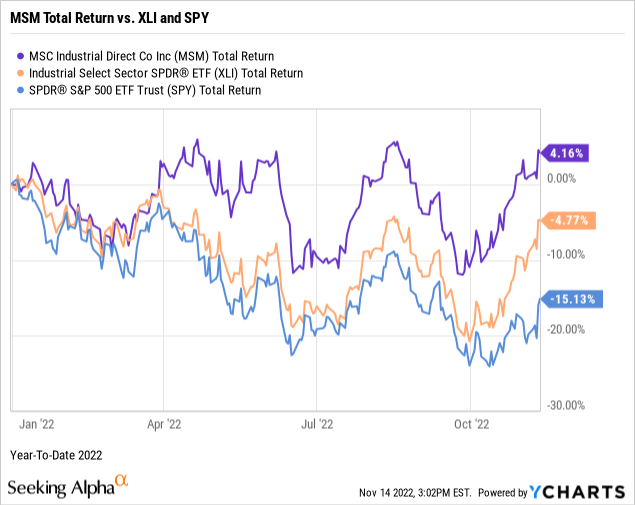

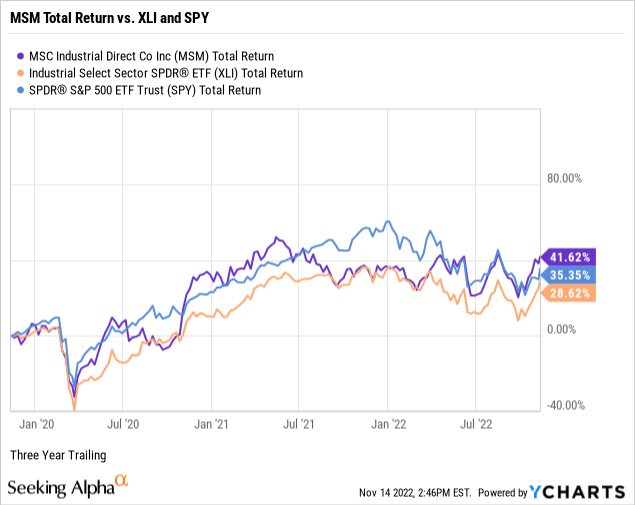

The charts below illustrate the stock’s performance against the Industrial Select Sector SPDR Fund ETF (NYSE:XLI) and the SPDR S&P 500 ETF Trust (NYSE:SPY) for year-to-date 2022 and the prior three years.

MSM has outperformed the total returns of its sector and the broader market during the timeframes up to and including the current bear market.

My value proposition rating for MSC Industrial Direct Co.: Bullish.

Long-Term Yield-On-Cost Crushing The 10-Year

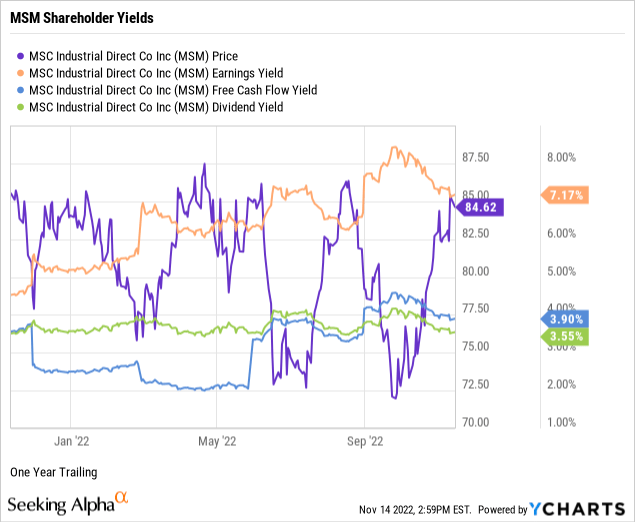

Let’s uncover the equity bond rate of MSC Industrial Direct’s common shares.

MSM was trading with an earnings yield of 7.17% and a free cash flow yield of 3.90%. In addition, the company offers a generous forward dividend yield of 3.55%, supported by a manageable 49.43% payout ratio, thus indicating a safe, covered dividend with room for annual raises.

I prefer high dividend yields only when calculated on a long-term cost basis. For example, MSM yielded 18.96% or 1,541 basis points above the forward yield from an annual payout of $3.16 on a split- and dividend-adjusted cost basis of $16.67 per share on March 9, 2009, the last major market bottom.

Next, I take the average of the three shareholder yields to measure how the stock compares to the prevailing yield of 3.87% on the 10-Year Treasury benchmark note. For example, the average result for MSM was 4.87% and 10.01% when using the 2009 yield-on-cost basis. Securities such as MSM, which reward shareholders with yields above the government benchmark, argue for owning the stock instead of the bond.

Remember that earnings and free cash flow yields are inverse valuation multiples, suggesting that MSM trades at a discount to earnings but at a premium to cash flows. I’ll further explore valuation later in this report.

My shareholder yields rating for MSM: Bullish.

High-Quality Management Performance

Next, I’ll explore the fundamentals of MSC Industrial Direct Co., uncovering the performance strength of the company’s senior management.

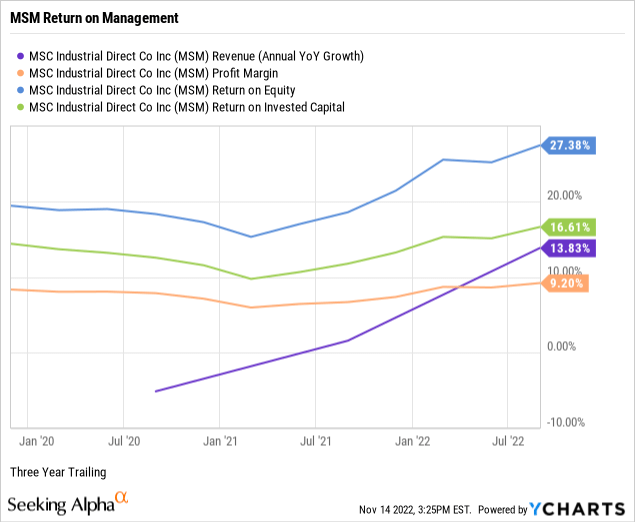

Per the below chart, MSC Industrial Direct had positive three-year annualized revenue growth of 13.83%, in line with the 16.41% double-digit median growth for the industrials sector.

MSC Industrial Direct had a trailing three-year pre-tax net profit margin of 9.20%, topping the sector’s median net margin of 6.80%.

In further showcasing its shareholder-friendly management, MSC Industrial Direct was producing trailing three-year returns on equity or ROE of 27.38%, nearly doubling the sector’s median ROE of 14.31%.

Typically an accelerator of ROE, MSC Industrial Direct’s board announced a five million dollar share repurchase program in October 2021 with no expiration date.

At 16.61%, MSC Industrial Direct’s return on invested capital, or ROIC, doubles the sector’s median ROIC of 6.83%, indicating that its senior executives are outstanding capital allocators.

MSC Industrial Direct’s ROIC nearly doubles its trailing weighted average cost of capital or WACC of 8.56%, confirming management’s ability to outperform its capital costs. (Source of WACC: GuruFocus).

The double-digit revenue growth, sector-beating net profit margin, and attractive returns on equity and capital indicate quality management performance on Long Island.

My fundamentals rating for MSC Industrial Direct: Bullish.

Cash Flow Is King (And Queen)

I rely on just four valuation multiples to estimate the intrinsic value of a targeted quality enterprise’s stock price.

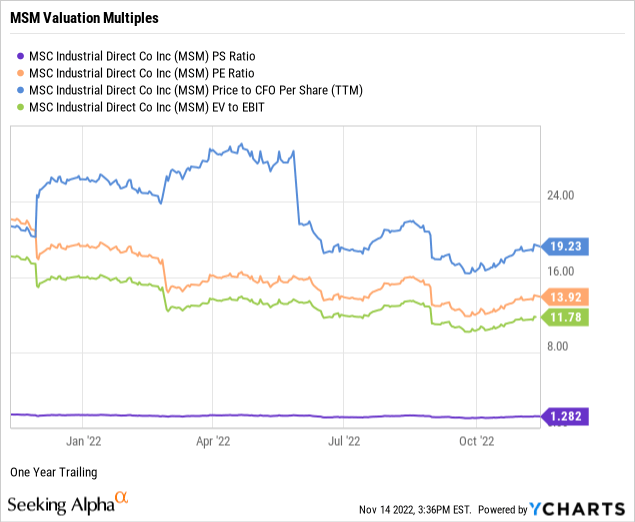

MSM was trading at a trailing price-to-sales ratio or P/S of 1.28 times, in line with the 1.34 median for the industrials sector and 2.17 times for the S&P 500. (Source of S&P 500 P/S: Charles Schwab & Co.) Thus, the weighted industry plus market sentiment suggests a reasonably-priced stock relative to MSC Industrial Direct’s topline. However, the S&P 500 implies the sector is trading at a slight discount to sales.

At 13.92 times, MSM had price-to-trailing earnings or a P/E multiple against a sector median P/E of 19.39, indicating investor sentiment discounts the stock price relative to earnings per share. Further, MSM traded at a discount to the S&P 500’s overall P/E of 19.35. (Source of S&P 500 P/E: Barron’s).

MSM’s price-to-operating cash flow multiple of 19.23 times traded at a slight premium to the sector’s median of 16.78, indicating that the market prices the stock at or above fair value relative to current cash flows.

Against the broader sector median of 16.98, MSM was trading at 11.78 times enterprise value to operating earnings or EV/EBIT, signaling the stock was oversold or underbought by the market.

Weighting my preferred valuation multiples suggests the market assigns a discount to MSC Industrial Direct’s stock price relative to sales, earnings, and enterprise value but a premium to the ultimate investor target of cash flows. Therefore, based on the fundamentals and valuation metrics uncovered in this report, risks and potential catalysts notwithstanding, I would call MSM a fair value-priced stock of a bear market-beating, B-rated industrial supplies provider.

My valuation rating for MSM: Neutral.

Downside Risks Are Below Average

When assessing the downside risks of a company and its common shares, I focus on five metrics that, in my experience as an individual investor and market observer, often predict the potential risk/reward of the investment. Hence, I assign a downside risk-weighted rating of above average, average, below average, or low, biased toward below average-risk and low-risk profiles.

Alpha-rich investors target companies with clear competitive advantages from their products or services. An investor or analyst can streamline the value proposition of an enterprise with an economic moat assignment of wide, narrow, or none. For example, Morningstar assigns MSM a narrow moat rating.

Notably, as reported on its September 2022 quarterly financial statements, at 3.29 times, MSC Industrial Direct’s long-term debt coverage or current assets to long-term debt could pay off its longer-term debt obligations in a crisis using its liquid assets, such as cash and equivalents, short-term investments, accounts receivables, and inventory.

In a further test of its paydown capacity, MSC Industrial Direct’s long-term debt to equity was a conservative 37.92%.

MSC Industrial Direct’s short-term debt coverage or current ratio was 2.13 times. Thus, its balance sheet provides significant liquid assets to pay down its current liabilities, including accounts payable, accrued expenses, short-term borrowings, and income taxes.

MSM’s 60-month trailing beta was 1.00. However, at 0.84, its shorter-term 24-month beta was less volatile. Thus, with price volatility trading at or below the S&P 500 standard of 1.00, MSM presents as a market-average volatility small-cap portfolio holding.

The short interest percentage of the float for MSM was a bear paws-off of 1.90%. So perhaps the near-sighted traders view the stock as a market-leading, narrow-moat industrial services provider with a loyal and sustainable customer base.

MSC Industrial Direct is a fundamentally superior industrials company with an enduring value proposition and an attractive risk profile, particularly its debt coverage, against a broader bear market.

My downside risk rating for MSM: Below Average.

MSM Catalysts And Final Thoughts

Catalysts confirming or contradicting my overall hold investment thesis on MSC Industrial Direct Co. and its common shares include, but are not limited to:

- Confirmations: MSC could continue to face gross margin pressure amid soft demand and fierce competition. Amazon (NASDAQ:AMZN) and other e-commerce players could structurally change the competitive environment, taking market share and pressuring margins. Cash flow yields and multiples suggest a fair-valued stock price.

- Contradictions: As end-market demand improves, MSC could return to mid- to high-single-digit sales growth and high teens’ return on invested capital. MSC does generate consistent free cash flow and runs a shareholder-friendly capital-allocation strategy. In addition, MSC management is executing its Mission Critical corporate strategy.

(Additional source of catalysts: Morningstar and Charles Schwab & Co.)

MSC Industrial Direct is an underfollowed small-cap distributor of metalworking and maintenance, repair and operations [MRO] products and services, outperforming the broader market with growth and profitability. Nonetheless, despite its high-quality business model and compelling valuations on sales, earnings, and enterprise value, its stock price multiples on otherwise solid operating and free cash flows suggest a wait-and-see if market sentiment changes direction in valuation following a hiccup quarter or similar temporary event.

Be the first to comment