Gearstd/iStock via Getty Images

Most investors have heard cautionary tales of not reaching for high yield. That may be true for distressed corporations and residential mortgage REITs that are highly sensitive to interest rates. However, there is no one-size fits all approach when it comes to investment maxims, especially when it comes to MLPs that are structured for high yield.

This brings me to MPLX LP (NYSE:MPLX), which yields higher than many of its peers and trades at a reasonable valuation. In this article, I highlight what makes MPLX a worthy high yield buy for income and growth investors alike, so let’s get started.

Why MPLX?

MPLX is a master limited partnership (issues K-1) that was spun off from Marathon Petroleum (MPC) 10 years ago. Its business model is rather straightforward, as it owns and operates long-lived assets, including pipelines and storage tanks, which are used to transport energy products from one point to another. MPLX also has an inland marine business, docks, and NGL processing and fractionation facilities linked to key U.S. supply basis, particularly in the Appalachia region.

MPLX’s assets were primarily built to serve its largest customer, Marathon Petroleum, which was its original equity sponsor. In a move seen as removing conflicts of interests, Marathon Petroleum and MPLX agreed to exchange its general partner economic interests, including incentive distribution rights, for MPLX’s common equity units back in 2017.

This relationship with MPC appears to be rock solid, as the two companies recently renewed a transportation services agreement for another 10 years. Moreover, the contracts have an automatic renewal provision that extends them to 2042.

MPLX also appears to be growing nicely, as Adjusted EBITDA grew by 6% YoY to $1.46 billion in the second quarter. This was driven by growth in both the Logistics & Storage and Gathering & Processing segments. Importantly, this growth while maintaining a low leverage ratio of 3.5x, which is more or less on par with that of other high quality midstream peers.

The distribution is also well protected by a 1.69x coverage ratio, and MPLX is aggressively returning capital to its unitholders, with $750 million worth of unit repurchases during the second quarter alone. In addition, MPLX recently announced an incremental $1 billion repurchase authorization.

Looking forward, MPLX seeks to replicate the success that peer Enterprise Products Partners (EPD) has had in Mont Belvieu, by building a significant asset base supporting the NGL market in Northeast U.S. It already has most of the assets in place, and management is making steady progress towards that goal, as noted during the recent conference call:

In the L&S segment, we continue to expand long haul natural gas and crude gathering pipeline supporting the growing Permian and Bakken regions. Specifically in the Permian, working with our partners, we continue to progress our natural gas strategy with the expansion of the Whistler pipeline from 2 bcf per day to 2.5 bcf per day, along with laterals into the Midland basin and Corpus Christi markets.

In the G&P segment, we remain focused on the Permian and Marcellus basins in response to producer demand. In the Permian, construction advanced on our Tornado 2 processing plant, which is expected to come online in the second half of 2022. We are also planning to build our sixth processing plant in the basin, Preakness II, which is expected to be online in the first half of 2024. This will bring our total Permian processing capacity up to 1.2 bcf per day.

In the Marcellus, our Smithburg de-ethanizer is expected to come online to meet incremental in-basin demand in the third quarter of 2022. Additionally, we plan to add the Harmon Creek II processing plant, which will expect to come online in the first half of 2024. This will bring total processing capacity up to 6.5 bcf per day in the Marcellus.

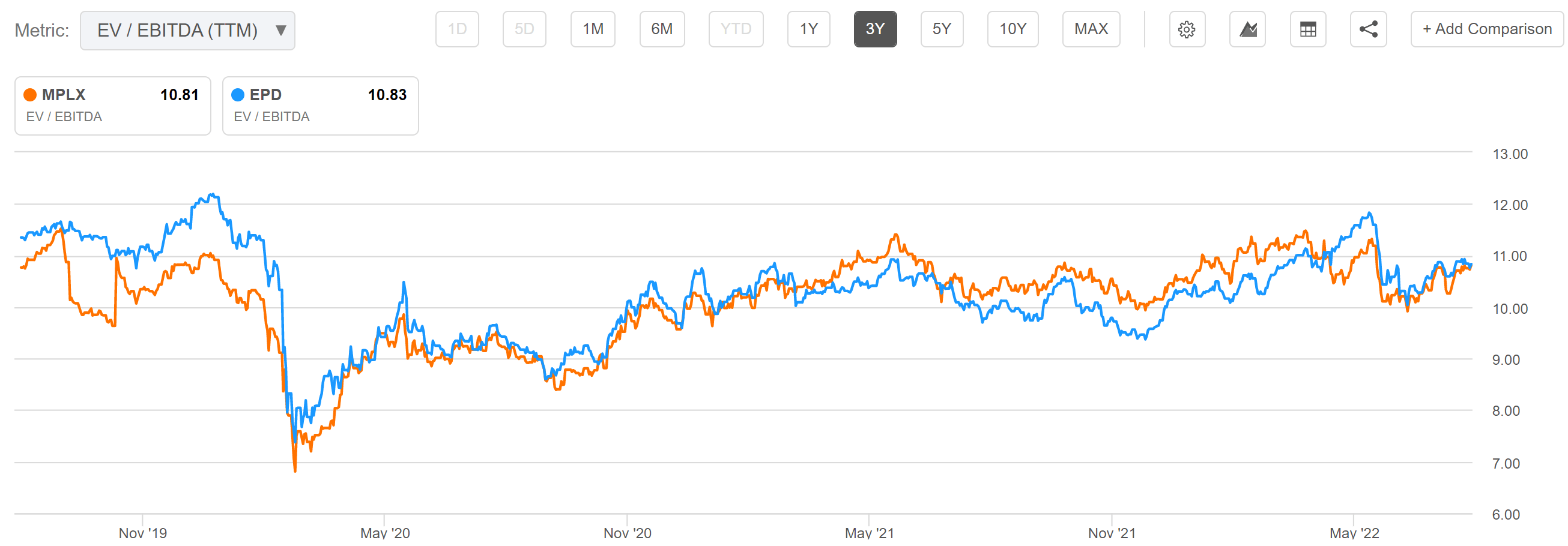

Meanwhile, I continue to see value in MPLX at the current price of $33.12 and its well-covered 8.5% distribution yield. As shown below, the shares appear to be reasonably priced in relation to its historical range, with an EV/EBITDA of 10.8x, putting it on par with that of EPD. For those who already own EPD, I see MPLX as being a solid addition, as it’s more aggressive with unit repurchases while also providing exposure to the Northeastern U.S. market.

MPLX EV/EBITDA (Seeking Alpha)

David Tepper of Appaloosa seems to agree, as the fund recently boosted its MPLX stake by 192K shares. Sell-side analysts have a consensus Buy rating, with an average price target of $37, translating to a potential one-year 20% total return including distributions.

Investor Takeaway

In summary, I believe MPLX is a high quality midstream name that remains attractively priced at the moment. It has a rock solid relationship with Marathon Petroleum, and it’s growing nicely while maintaining a low leverage ratio, and the distribution appears well covered by cash flow. MPLX is also aggressively returning capital to its unitholders, and I see the shares as being a solid addition to any income focused portfolio.

Be the first to comment