Bet_Noire

Automobiles and Parts Account for the Lion’s Share of the US Economy, and Motorcar Parts of America (NASDAQ:MPAA) Is Bracing for the Industry Tailwind

Not only are cars and parts driving up spending on goods, but they’re also among the activities that account for the lion’s share of annualized US Gross Domestic Product [GDP] growth of 2.9% QoQ in the fourth quarter of 2022 versus the 2.6% forecast.

Reduced supply chain headwinds coupled with the continued strong recovery in internal combustion engine sales as gasoline prices become significantly cheaper in the United States (down 32.3% from an all-time high of $1.30/liter in June 2022 to 0.88 $/ liter in January 2023) are reflected in higher spending on motor vehicles and parts.

The positive trend in auto and parts spending should continue to reflect higher light vehicle sales in the US and the availability of larger inventories. The latter will benefit as supply chains ease pressure on vehicle production in their bid to recapture pre-COVID-19 shape.

As such, tailwinds are expected for the US auto and parts industry, and investors should seek to capitalize on this growth opportunity by repositioning their portfolios invested in US-listed makers of auto and parts accordingly.

Motorcar Parts of America has a Buy rating given the company’s strong portfolio of activities and good sales and earnings prospects.

If sales and earnings are the drivers of the stock price, then this holding is on track to perform well in the period ahead.

About Motorcar Parts of America in the Auto Parts Industry

Motorcar Parts of America, Inc., headquartered in Torrance, California, remanufactures, manufactures and sells automotive aftermarket parts for vehicles.

The category of auto parts is wide and diverse, including alternators, starters, wheel bearings and hub assemblies, brake calipers, brake pads, rotors, power and master cylinders, boosters, turbochargers and diagnostic testers.

The latter is used in imported and domestic passenger cars as well as light trucks and heavy-duty applications.

Its products are sold primarily to the automotive retail and professional repair markets throughout North America, while manufacturing facilities are located in California, New York, Mexico, Malaysia, China, and India.

The company also operates an electric vehicle subsidiary that designs and manufactures test solutions for multiple components in the electric powertrain to meet the specific performance requirements of ongoing electrification in the automotive and aerospace industries.

Results for the Third Quarter of Fiscal 2023

On Thursday, February 9, prior to the start of regular trading, Motorcar Parts of America reported results for the third quarter of fiscal 2023 ended December 30, 2022.

Net sales were $151.8 million for the third quarter of fiscal 2023, reflecting a 6% decrease year over year due to lower orders from certain customers, which did not result in a loss of market share.

That data shouldn’t dampen Motorcar Parts of America’s growth prospects at all, as the downtrend in customer orders appears to be temporary in the third quarter of fiscal 2023.

The company reports that it has already seen a rebound in orders in the current quarter and this should continue to improve significantly throughout fiscal 2024 ending March 31, 2024 thanks to the macro factors mentioned before.

According to the company, demand for Motorcar Parts of America products will receive a boost as the company’s customers have to adjust their inventory levels to meet the expected sharp increase in demand in the coming seasons.

As for the company’s forecast for future orders, this is very likely as the fall in fuel prices (down 32.3% from a record high of $1.30/liter June 2022 to $0.88/liter January 2023) will be an incentive for the production and registration of new vehicles, but also for the re-use of older vehicles.

Not only will more new vehicles on the road require a growing auto parts market to meet future replacement needs, but demand for Motorcar Parts of America products will also benefit from older vehicles returning to service after months of inactivity taken due to high fuel prices.

Net income of $1 million (or $0.05 per diluted share) in Q3 FY 2023 was lower than $3.1 million (or $0.16 per diluted share) in the same period of FY 2022.

The decline in net income was due to factors beyond the company’s control, such as higher financing costs due to higher interest rates and higher costs related to inconveniences along the supply chain.

However, these costs are temporary in nature, so they do not weigh on income in the long term.

Gross margin for the Q3 FY 2023 was 13.8% of total revenue, reflecting a year-over-year decrease of 630 basis points, primarily impacted by temporary headwinds.

These gross profitability negatives included inflationary costs that will cease as the US Federal Reserve’s disinflation process continues to unfold and higher overhead costs that will disappear as production ramps up on expected strong demand for auto parts. The gross profitability was also impacted by product mix changes which effects will settle down as operations move forward.

It’s also worth noting that according to the company, inflationary costs have not yet been offset by price increases, so the higher pricing policy is expected to make a strong contribution as well to Motorcar Parts of America’s future profitability.

The company also reported financial results for an extended 9-month period through Q3 FY 2023, of which the most relevant improvements are described as follows.

The bottom line was a net loss of $5.7 million (or -$0.29 per share) versus a net income of $7.7 million ($0.39 per share) for the 9-same month last year, although revenue increased 3.2% year over year to $488.3 million.

Gross profit of 15.9% fell 300 basis points year over year.

The nine-month year-over-year trend was impacted by the same temporary headwind.

Company Outlook Versus Analyst Estimates

Thus, Motorcar Parts of America’s profitability should improve as the passing headwinds ease.

Sales

The company expects the full fiscal year 2023 revenue to range between $672 million and $680 million (vs. $650.13 million in FY 2022) and expects quarterly revenue to be a record for the last quarter of FY 2023, which will end March 30, 2023.

Motorcar Parts of America is not saying how much sales it expects for the full fiscal 2024, but it certainly expects 2024 to be a very strong year. This is possible because by that time all temporary headwinds, including recessionary ones, will have passed.

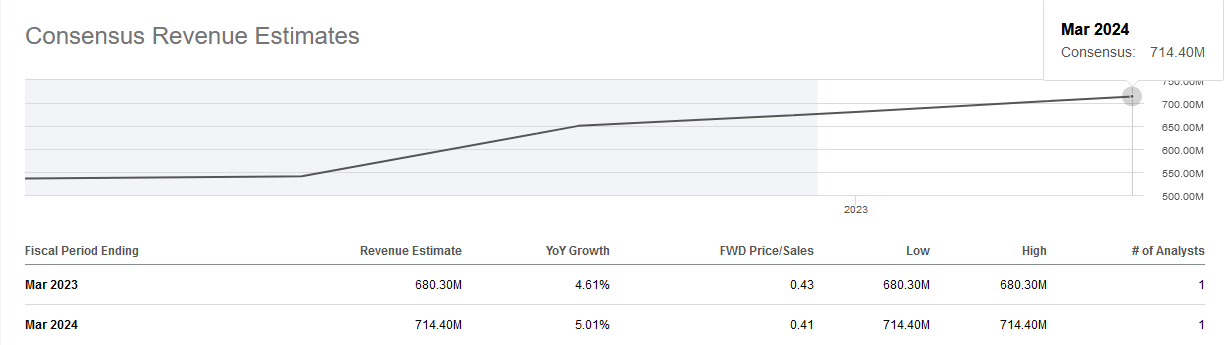

While the analysts project total revenue of $680.30 million in FY 2023, which will be an increase of 4.61% year-over-year, and total revenue of $714.40 million in FY 2024, which will be an increase of 5.01% year-over-year.

Source: Seeking Alpha

The Net Income

The company has not provided a guidance range for net profit but expects margin improvement. According to Motorcar Parts of America, this will be the result of more favorable pricing, alleviating supply chain constraints and achieving operational efficiencies through the implementation of additional cost reduction initiatives. So, the bottom line should improve from previous years.

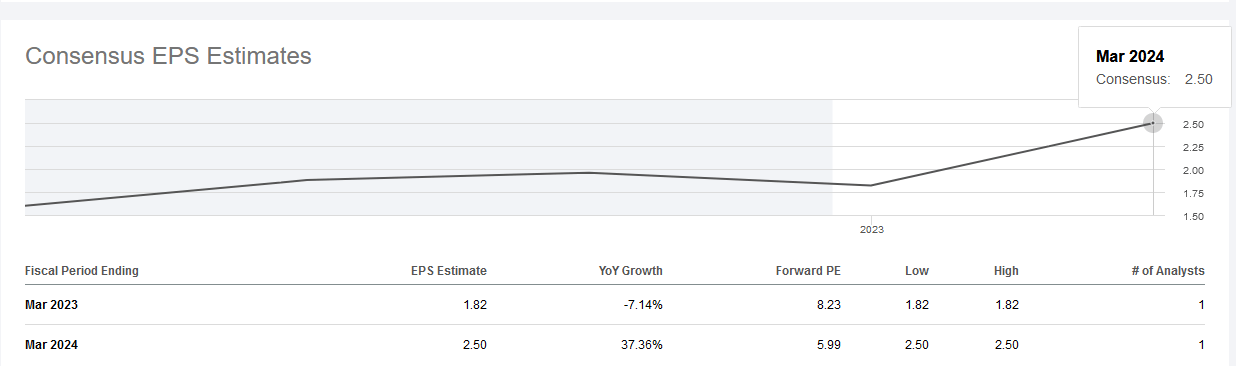

While the analysts project total earnings per share [EPS] of $1.82 in FY 2023, which will be a slight drop of 7.14% year-over-year, but an EPS of $2.50 in FY 2024, which will instead be an increase of 37.36% year-over-year.

Source: Seeking Alpha

The Financial Condition

As of December 30, 2022, the balance sheet reported net debt of approximately $260 million, which resulted in financial costs affecting the company’s profitability.

However, the achievement of some managerial efficiency targets, primarily operating cost reductions and other cost containment initiatives, along with ending inflationary pressures and costs associated with supply chain disruptions should allow the company to improve its leverage.

The Stock Valuation

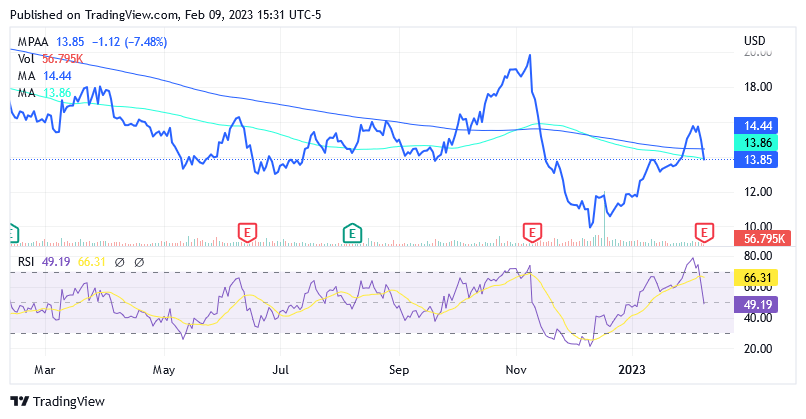

Motorcar Parts of America, Inc. shares were trading at $13.85 per share at the time of this writing, giving it a market cap of $290.75 million.

Source: Seeking Alpha

The shares are trading below the 200-day moving average line, but at almost the same level as the 75-day moving average line. Shares are also slightly below the $14.865 median of the 52-week range of $9.80 to $19.93.

Based on the technical indicators above, shares do not appear to be trading high, so given the growth prospects, investors could also start building the position from these levels. However, the 14-day relative strength indicator at 49.19, which shows the middle ground between overbought and oversold levels, presents a curve that appears to be on a strong downward move.

It is not easy to determine when this downtrend in Motorcar Parts of America, Inc.’s stock price might end, but one thing is certain: this trend will create a more favorable entry point for this stock with strong upside potential on anticipated higher sales and better margins.

However, as long as the economy lags a bit to provide recessionary responses that the US Federal Reserve is waiting for, the market could fear more rate hikes along the way.

Financial results for the third quarter of fiscal 2023 showed that higher borrowing costs were causing some headaches for the company’s profitability. Based on this information, market demand for Motorcar Parts of America shares may continue to struggle.

Therefore, the investor should wait until the ongoing decline in the share price has completely subsided before buying shares. But this stock definitely deserves a Buy recommendation.

Conclusion

Motorcar Parts of America has a Buy rating that investors may want to implement after the stock price completes its current trajectory that is on track to create a more convenient entry point.

The market is currently bearish in Motorcar Parts of America shares as it reacts to Fed Chair Jerome Powell’s Tuesday speech, resulting in higher borrowing costs that appear to be seriously hurting the company’s profitability margin.

But these headwinds for the company’s shares will end when the market understands that with the disinflation process effectively unfolding and the cumulative impact of multiple rate hikes that have yet to hit the economy, fears of a repeat of aggressive rate-hiking policies are futile.

That, along with the company’s expectation for a strong ending to fiscal 2023, paves the way for higher profitability going forward, which should help the stock price return to its uptrend.

Be the first to comment