Jack Taylor

Introduction

My thesis is that sales outside the US and Canada are climbing quickly for Monster Beverage (NASDAQ:MNST).

The Numbers

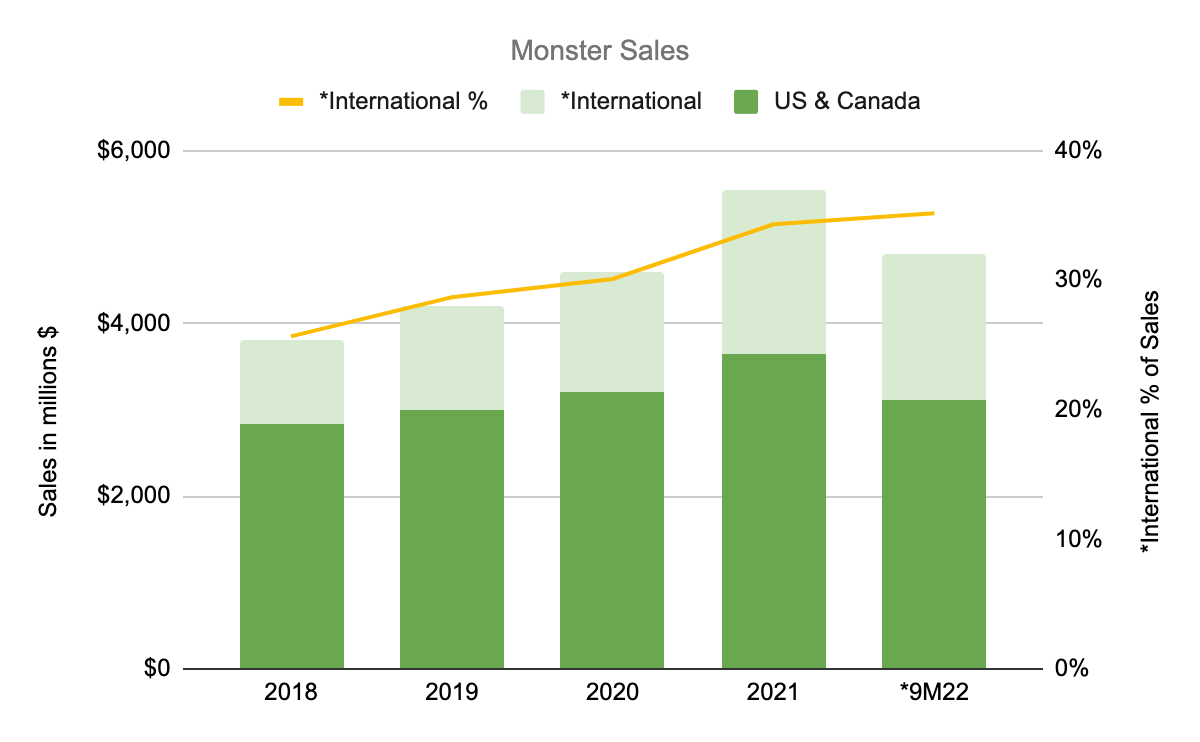

Sales from outside the US and Canada were just $977 million or 25.7% of the total in 2018 and this has climbed up to $1,687 million or 35.2% of the total for 9M22 per the 3Q22 10-Q:

Global sales (Author’s spreadsheet)

*Canada isn’t broken out separately so “International” means everything outside these 2 countries in the graph above.

*The 2022 10-K filing isn’t out yet so we use 9M22.

We see above that both international and overall sales in dollars have gone up nicely since 2018. Units have gone up as well but I don’t see them broken down by geography. Overall case sales in 192‑ounce case equivalents are as follows:

2018: 410.9 million

2019: 448.8 million

2020: 504.8 million

2021: 613.4 million

9M22: 535.5 million

There is still a tremendous amount of room to grow outside of the US. Coke (KO) energy drink sales were 40% US and 60% international back in 2015 when they did a deal with Monster. In a 2017 video interview, Co-CEO Rodney Sacks said that the US only accounts for about 1/3rd of the global energy drink market in volume and revenue.

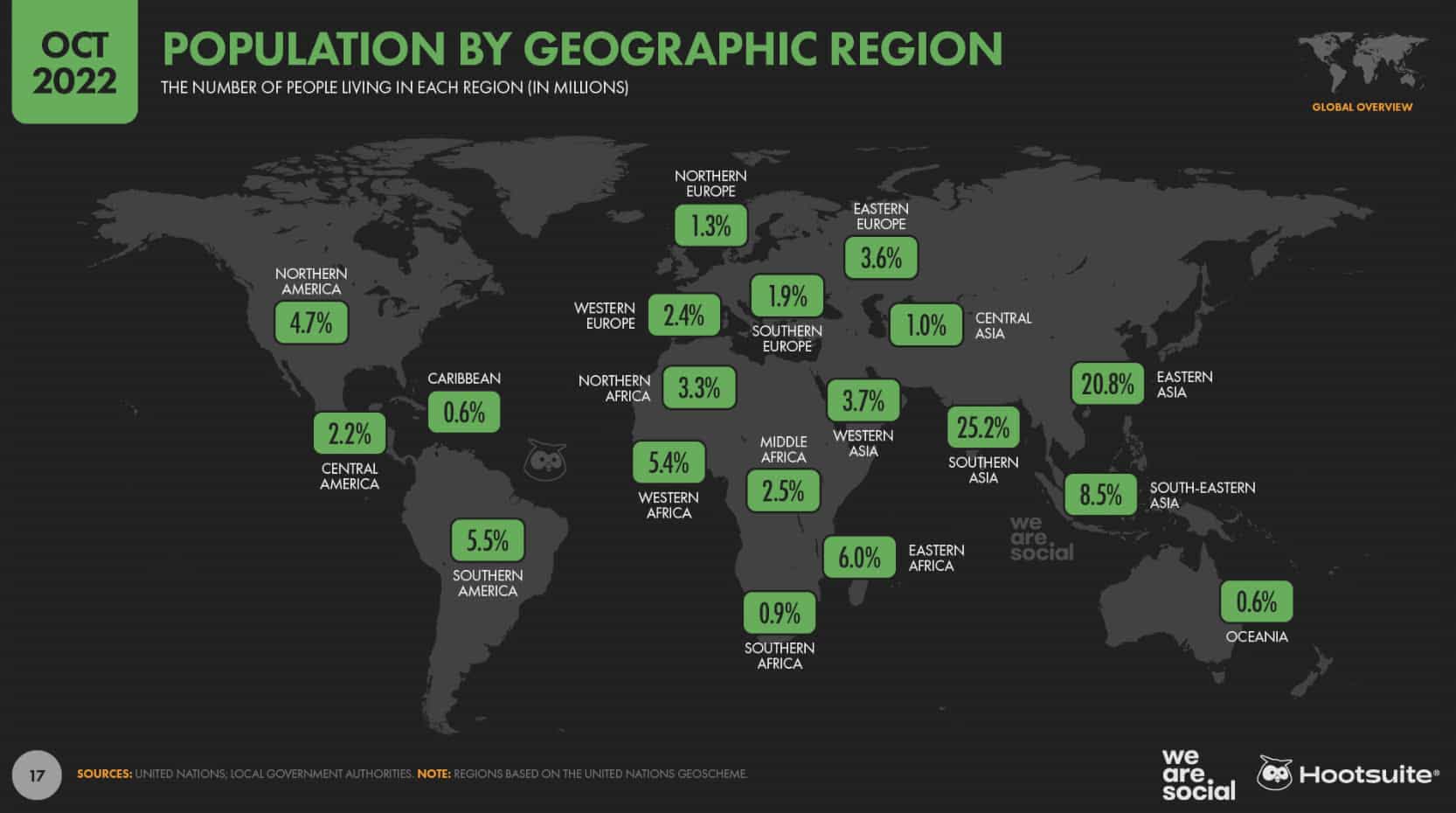

DataReportal gives us a visual reminder that Southern Asia, Eastern Asia and Southeastern Asia

account for 25.2%, 20.8% and 8.5% of the world’s population, respectively. Monster Beverage has a lot of work to do with respect to more expansion outside of the US:

Global population (DataReportal)

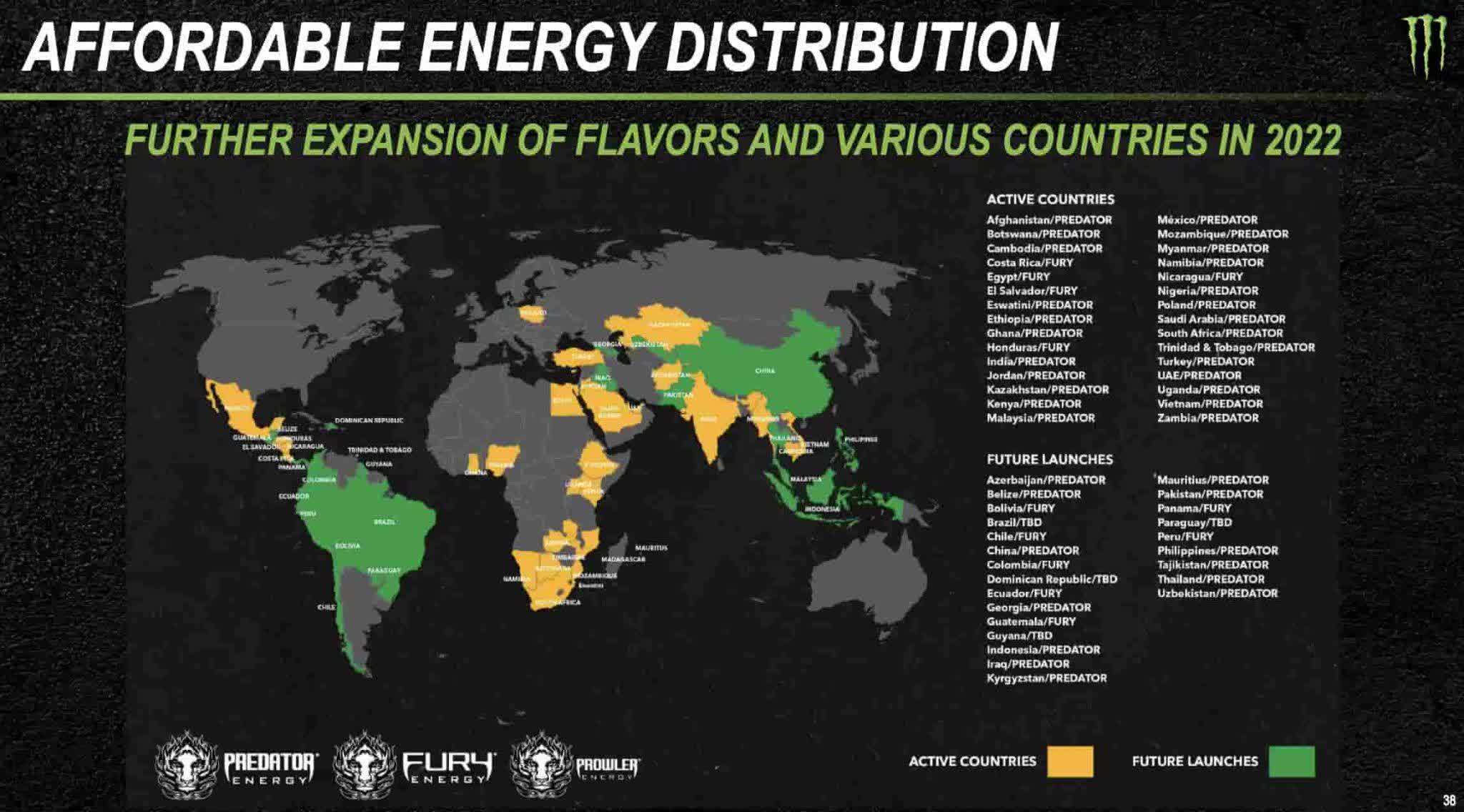

Growth has been especially fast in Latin America and the Caribbean where we saw sales jump from $147 million in 2018 all the way up to $472 million for the trailing twelve months (“TTM”) through September 2022. Per the January 2023 Business Update, affordable brands like Predator and Fury are coming to more countries in Latin America and Asia:

Expansion (January 2023 Business Update)

Valuation

In addition to selling more energy drinks worldwide, Monster Beverage continues to make their presence known in the world of alcohol:

Beast unleashed (January 2023 Business Update)

Trailing twelve month (“TTM”) operating income through September 2022 is $1,602 million or $1,190 million 9M22 + $1,797million FY21 – $1,385 million 9M21. This is on TTM gross profit of $3,158 million or $2,390 million + $3,109 million – $2,341 million. TTM revenue is $6,223 million or $4,798 million + $5,541 million – $4,116 million.

Normally we wouldn’t expect a company to be worth a high multiple of operating earnings in this environment of rising interest rates but the vestigial operating margins for Monster should bounce back eventually. In the 3Q22 call, Co-CEO Rodney Sacks talked about the fact that the above margins are lower than normal right now as the company uses expensive options like air freight in order to keep product moving:

Since the beginning of the COVID-19 pandemic and the subsequent increased demand for the company’s energy drinks, the company prioritized ensuring product availability for its customers and consumers. This strategic direction has remained in place throughout the global supply chain challenges and disruptions, despite adversely impacting the company’s profitability. We continue to air freight quantities of certain ingredients internationally, particularly to EMEA, Asia Pacific and Latin America at additional costs and inefficiencies to enable timely innovation launches. We continue to experience significant increases in distribution expenses, primarily as a result of increased warehousing expenses as well as other logistical expenses, which adversely impacted operating expenses.

The operating margin exceeded 1/3rd from 2015 to 2020 and I expect it to climb from today’s TTM level of 26% once the issues above are addressed. If today’s margin was 1/3rd then TTM operating income would be over $2 billion and a valuation of 25 to 30x this might be reasonable if interest rates eventually start to decline. As such, a valuation of $50 to $60 billion might not be out of the question.

The market cap is a little over $54 billion based on the January 25th share price of $103.52 and the 521,743,612 shares outstanding as of October in the 3Q22 10-Q. The enterprise value is $2,650 million less than the market cap due to $1,303 million in cash and equivalents in addition to $1,347 million in short-term investments.

Forward-looking investors should keep an eye out for the 2022 10-K filing to see how the year ended. This filing should help investors understand when margins will start going back to normal.

Be the first to comment