MarkPiovesan/iStock via Getty Images

National Fuel Gas Company (NYSE:NFG) is a $4.8 billion market-cap hybrid of upstream, midstream, and downstream (utility). The stock price is down since my last analysis eighteen months ago, when I shifted from a buy to a hold recommendation. I am reversing that recommendation with an expectation of higher prices for formerly constrained Marcellus gas as the Mountain Valley Pipeline comes online, projected to be at the end of 2023.

Investors should nonetheless be aware of local, state, and federal regulations and proposals to limit or reduce the use of natural gas.

Since NFG is a natural gas operation, its revenues reflect weather seasonality, with more revenues in the October-March time frame. Similar companies often see an October-February stock price peak, so potential investors should be aware of this.

NFG has adapted to this seasonality with a non-traditional financial reporting schedule, albeit one that makes sense for the natural gas pricing cycle that peaks in the winter: the company’s fiscal fourth quarter ends September 30. The most recent results, for April-June 2023, are thus its third quarter of 2023 results.

The company’s four reporting segments span upstream, midstream, and downstream:

*exploration and production (Seneca Resources);

*pipeline and storage (National Fuel Gas Supply and Empire Pipeline);

*gathering (National Fuel Gas Midstream);

*utility (National Fuel Gas Distribution).

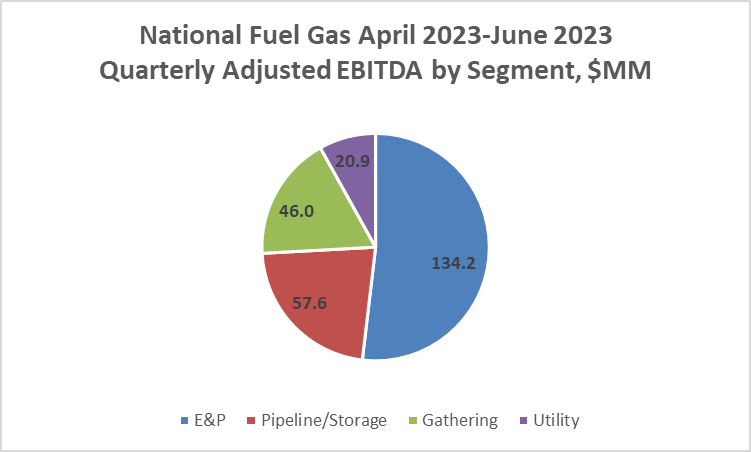

In the most recent quarter, over half of the company’s adjusted EBITDA came from its Seneca Resources exploration and production division.

Current dividend yield is 3.8%.

At a lower stock price in its cycle and with higher natural gas prices ahead, I am upgrading my ranking on National Fuel Gas stock to buy.

Third Quarter 2023 (Quarter Ending June 30, 2023) Results and Guidance

In NFG’s third fiscal quarter of 2023 (April 2023-June 2023), GAAP net income was $92.6 million, or $1.00/share, compared to GAAP net income of $108.2 million or $1.17/share in the prior year.

For the first nine months of the fiscal year (October 2022-June 2023), GAAP net income was $403 million or $4.37/share compared to $408 million or $4.69/share for the same period a year earlier.

Adjusted operating results, a non-GAAP measure, for the April-June 2023 quarter were $1.01/share, compared to $1.54/share in the prior year.

The chart below shows the relative size of adjusted EBITDA by segment for the April 2023- June 2023 quarter (3Q23).

Starks Energy Economics, LLC & National Fuel Gas

The company’s full-year (October 2022-September 2023) earnings guidance is $5.15-$5.25/share. Its fiscal 2024 earnings guidance is $5.50-$6.00/share, an 11% increase.

Gas production for the fiscal year is expected be 370-380 BCFe, or 1.01-1.04 BCFe/day. Per the company, this reflects over 5 BCFe of price-related curtailments and volumes shut-in due to low in-basin pricing and third-party pipeline system constraints. Seneca has firm sales contracts in place for the remainder of its fiscal 2023 gas production (July-September 2023).

For fiscal 2024, the company assumes average NYMEX prices of $3.25/MMBTU. Seneca has firm sales contracts for 88% of its expected 2024 production. Two-thirds of production is hedged financially or covered by fixed price contracts.

Capital expenditures for the Pipeline, Storage, and Utility segments are expected to be between $250 million and $290 million in fiscal 2024. The spending is focused on infrastructure safety, reliability, and resiliency, as well as reducing emissions.

Capital spending for exploration and production (Seneca) is expected to be down slightly at $525 million to $575 million in fiscal 2024. The company is leaning into exploration in Tioga and Lycoming counties, in Pennsylvania.

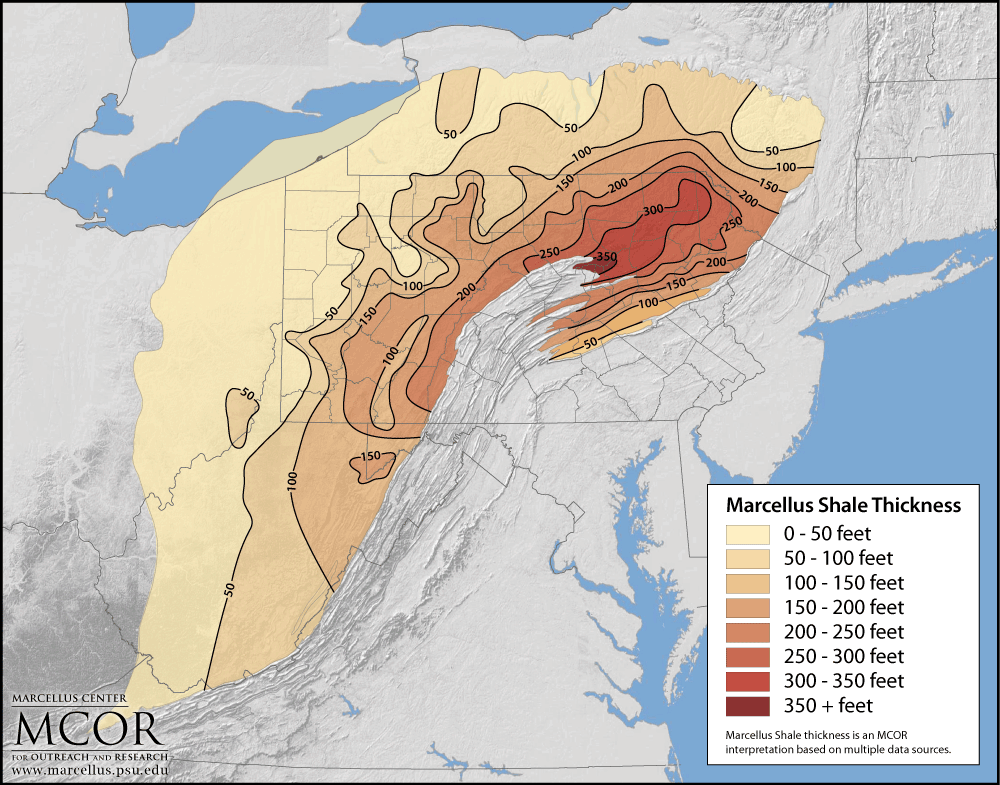

Penn State Marcellus Center

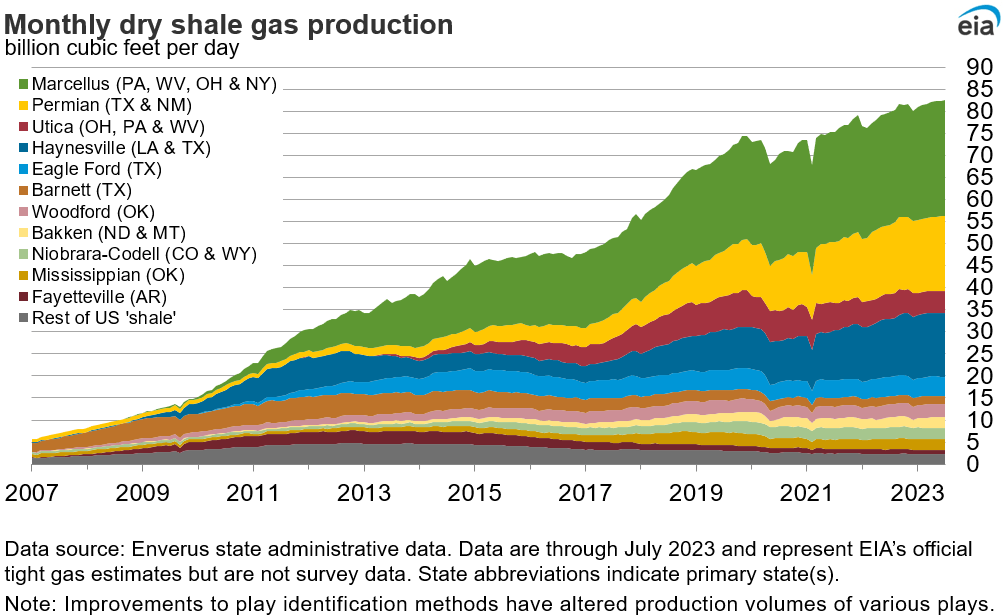

US Gas Production and Prices

The map above shows the areal and depth extent of the Marcellus formation.

The Energy Information Administration (EIA) projects Appalachian volumes to be 35.7 BCF/day in September 2023, out of about 103 BCF/D total US gas production. The Appalachian area is the combination of the green-colored Marcellus and the brown-colored Utica in the graph below.

EIA

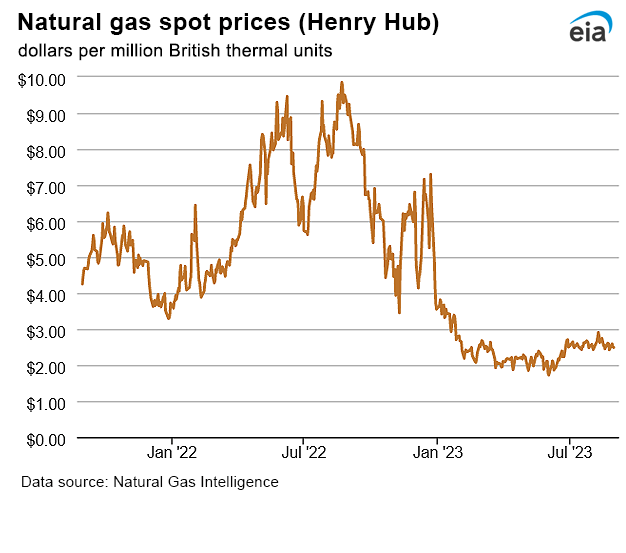

The September 5, 2023, NYMEX natural gas closing price for delivery in October 2023 was $2.59/MMBTU at Henry Hub, Louisiana. The price for Marcellus natural gas (Tennessee Zone 4 and Eastern Gas South hubs) is typically lower. Natural gas prices have fallen dramatically (albeit back to normal) since the beginning of 2023.

EIA

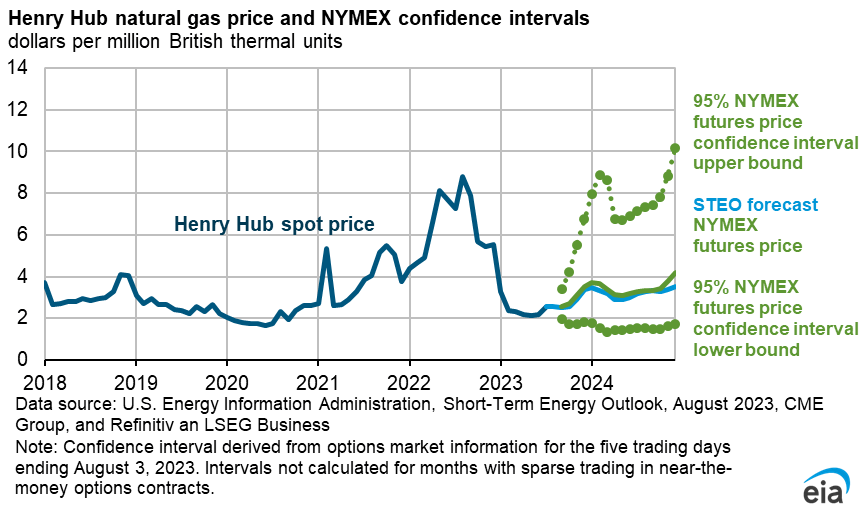

The EIA’s 5-95 confidence interval for gas prices through the end of 2024 is shown below.

EIA

Reserves and Operations

At September 30, 2022, National Fuel Gas’ Seneca Resources Company had total proved reserves of 4.2 trillion cubic feet (TCF) of Appalachian natural gas and a small 250,000 barrels of oil (1.5 BCFe).

The PV-10 of future net revenues of the company’s proved developed and undeveloped reserves at September 30, 2022, was $7.2 billion. However, investors should be aware this used an average Henry Hub price (appropriate at the time but high now) to value gas of $6.13/MMBTU. After adjusted for quality, transportation fees, and market differentials, the gas price used for Seneca’s reserve calculation was $4.60/MCF.

Given the sharp drop in gas prices shown above, Seneca’s reserve value calculated on September 30, 2023, is likely to be lower than the 2022 total.

The map below generally shows NFG’s operations in NW Pennsylvania and western New York: light blue is utility service area, dark blue is Seneca Resources exploration and production, yellow is pipelines and storage. (For additional clarity, see page 3 of the pdf version here.)

National Fuel GAS

Competitors

NFG is headquartered in Williamsville, New York.

Competitors across the company’s various operating segments include Coterra (CTRA), National Grid (NGG), and EQT (EQT).

Technically, US natural gas in any region east of the Rockies competes with gas in all other east-of-Rockies regions. But in the (vast) Appalachian Marcellus specifically, gas-producing competitors in addition to CTRA and EQT include Antero Resources (AR), Chesapeake (CHK), CNX Resources (CNX), Northern Oil and Gas (NOG), Ovintiv (OVV), Range Resources (RRC), and Southwestern Energy (SWN).

NFG is also active in the Utica: additional competitors there include EOG (EOG), Gulfport Energy (GPOR) and some private companies.

Similar to the original Cabot segment of Coterra, with experience and ownership of infrastructure (gathering, pipelines, and storage) and its own gas utility, National Fuel Gas can more easily transport and sell its natural gas than other producers. When Mountain Valley Pipeline opens, that may be less of a differentiating factor than it has been.

In June 2022 the company’s Seneca Resources division sold its California oil assets to Sentinel Peak Resources California for between $280 million and $310 million: $280 million at closing and annual payments in 2023-2025 of up to $30 million, depending on oil prices.

Governance

At September 1, 2023, Institutional Shareholder Services ranked NFG’s overall governance as a stellar 1, with sub-scores of audit (1), board (6), shareholder rights (2), and compensation (1). In this ranking a 1 indicates lower governance risk and a 10 indicates higher governance risk.

At August 15, 2023, shorts were 3.0% of the stock float. Insiders owned 1.2%.

The company’s most recent beta is 0.69 indicating that the stock price moves directionally with the overall market but less sharply.

Because the company’s gas operations are primarily in New York and Pennsylvania, it is subject to New York’s strict hydrocarbon regulatory limitations designed to discourage consumption, including a prohibition on drilling (Affects Seneca Resources).

Moreover, New York has passed a law banning the use of natural gas in residential buildings starting in 2026, and larger buildings in 2029. (Affects other NFG segments operating in New York).

Investors should also be aware of the Biden administration’s proposed regulation to essentially outlaw current gas-powered generators. This could endanger those who rely on gas generators for backup during power outages, winter and summer.

At June 29, 2023, the top three institutional holders were Vanguard (14.0%), BlackRock (9.3%), and State Street (8.7%). Some institutional fund holdings represent index fund investments that match the overall market. BlackRock and State Street signatories to the Net Zero Asset Managers initiative, a group that, as of June 30, 2023, manages $59 trillion in assets worldwide. NZAM limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

Although BlackRock hasn’t left the group as Vanguard did several months ago BlackRock recently made a point of saying it had rejected 93% of this year’s climate and social shareholder proposals.

Financial and Stock Highlights

National Fuel Gas’s September 5, 2023, closing stock price of $51.99/share gives a market capitalization of $4.77 billion.

With a 52-week price range of $48.89-$72.24/share, the closing price is 72% of the 52-week high. The company’s one-year target price is $62.25/share, putting its current price at 84% of that level. Put another way, upside to the one-year target price is 20%.

Trailing twelve-month earnings per share (EPS) was $6.09 for a trailing price/earnings ratio of 8.5. The midpoint of the company-projected fiscal 2024 EPS is $5.75 for a forward price-earnings ratio of 9.0.

At June 30, 2023, the company had $5.17 billion in liabilities, debt, and deferred credits and $8.11 billion in assets giving NFG a liability-to-asset ratio of 64%. The long-term debt net of the current portion is $2.38 billion.

A dividend of $1.98/share yields 3.8%. NFG’s trailing twelve-month return on assets is 6.3% and return on equity is 22.7%.

The company’s mean analyst rating in September 2023 from seven analysts is 2.7, closer to “hold” than “buy.”

One analyst considers the stock to be significantly undervalued.

Notes on Valuation

The company’s book value per share of $31.98, about 60% of current market price, suggests positive investor sentiment.

With an enterprise value (EV) of $7.04 billion, NFG’s EV/EBITDA ratio is 5.8, well below the preferred ratio of 10 or less and so in bargain territory.

Positive and Negative Risks

Like other companies that operate in regulatorily-hostile areas, NFG is exposed to numerous constraints from the state of New York. While its New York-based gathering, storage, and pipelines can’t be physically moved, the company is already making much of its income from non-New York exploration and production.

The company has addressed its price sensitivity risks with fixed-price contracts and, when necessary, curtailments. It nonetheless is exposed to gas prices in a general way as contracts roll over.

However, a positive risk is the price upside for natural gas from LNG and electricity demand. Another positive risk is the potential upside as transportation out of the region becomes more available.

The price for this year’s (September 30, 2023) reserve value is already baked in. Investors should expect a lower reserve valuation.

Inflation increases costs-especially financing costs–a particular concern for a company with a 64% ratio of liabilities to assets and $2.4 billion of long-term debt.

The restrictive regulatory environments for drilling, transportation, and demand (e.g. all three sectors) in which National Fuel Gas operates, especially New York is another double-edged sword. Regulation may limit growth and upside potential of NFG’s operation, but it also acts a barrier to entry to additional competitors.

Recommendations for National Fuel Gas

Although NFG is headquartered and has a segment of its operations in gas-unfriendly New York, much of its operations, including all of its drilling, are in less-restrictive Pennsylvania. Moreover, by nature of the dense, legacy pipeline system in Pennsylvania, gas produced there can go to other markets far outside of New York.

The company’s stock price has 20% upside to its one-year target, superb governance scores, and has done an excellent job of integrating Appalachian gas across upstream, midstream, and utility sectors.

The company offers a 3.8% dividend and estimated 2024 EPS of $5.50-$6.00/share for a forward price/earnings ratio of 9.0.

As noted, I am upgrading National Fuel Gas to a buy.

National Fuel Gas

Be the first to comment