Scott Olson/Getty Images News

Introduction

Despite losing ~30% (or $750B) of its market capitalization over the last year, Microsoft (MSFT) continues to be a Wall Street darling. Out of 29 analysts covering the stock, 26 analysts rate it a “Buy”, and the rest rate it a “Hold”.

TipRanks

Top-tier banks like Goldman Sachs (GS), Morgan Stanley (MS), Bank of America (BAC), and several others have named Microsoft as a “Top Pick For 2023”. And Microsoft’s love affair with Wall Street is not just limited to sell-side research desks. In late 2022, Microsoft overtook Amazon as the most popular hedge fund bet. Clearly, everybody loves Microsoft!

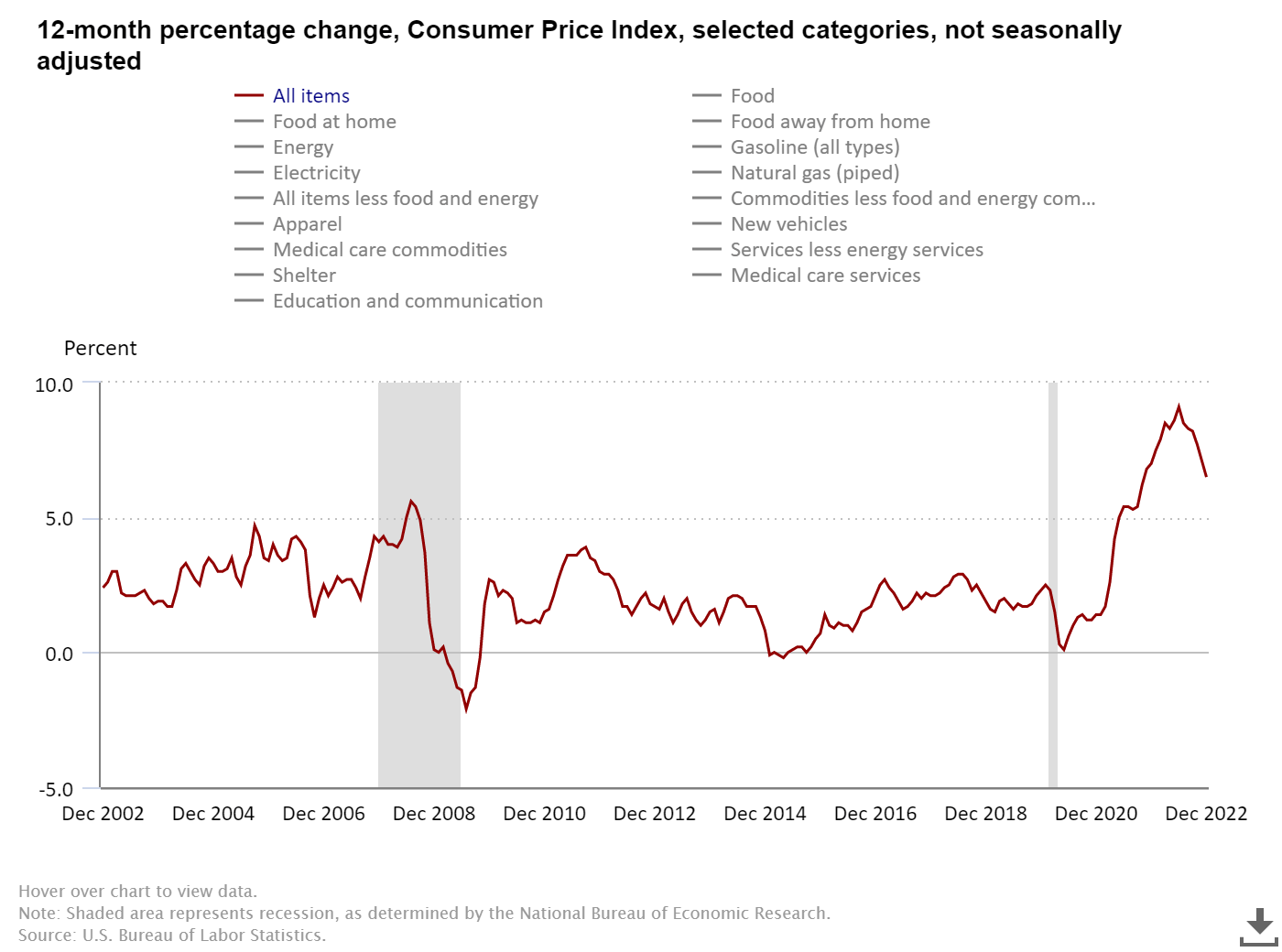

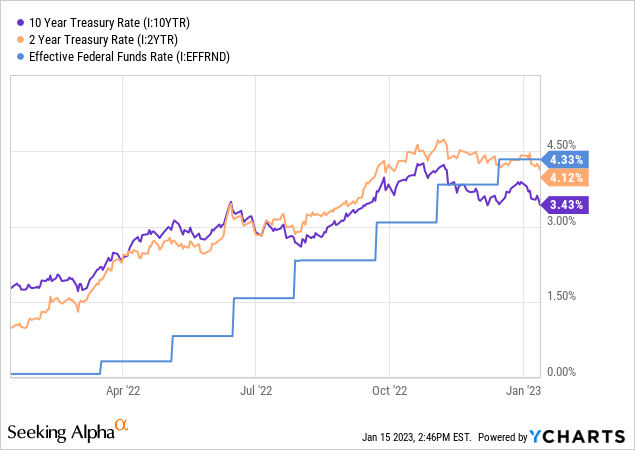

While the macroeconomic environment remains uncertain, two of the biggest headwinds for technology stocks – inflation and interest rates – are turning into tailwinds. Simply put, a higher inflation rate reduces the value of future free cash flows, and higher interest rates result in a higher discount rate (lower net present value for a given stream of cash flows) in discounted cash flow modeling. As you may have observed, inflation has been cooling off for months now (December CPI: -0.1% m/m), and interest rates (especially long-duration treasury yields) are moderating rapidly (10-yr treasury yield is down from recent highs of ~4.3% to ~3.4%).

bls.gov

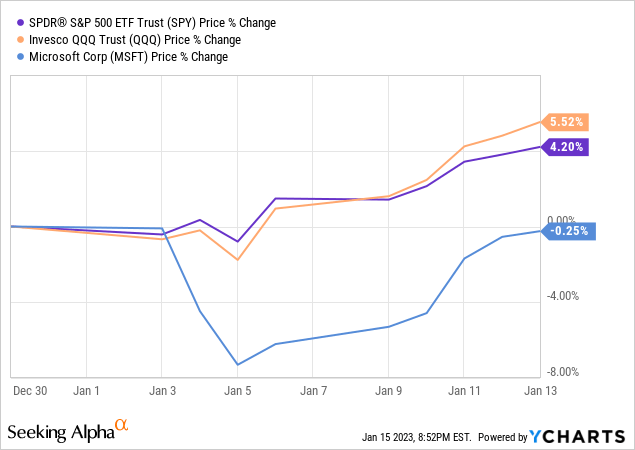

With inflation and interest rates cooling down in recent weeks, Mr. Market is getting excited about a potential rebound in equities in 2023, particularly in the beaten-down technology sector. Post the turn of the year, S&P 500 (SPY) and Nasdaq 100 (QQQ) are up 5.5% and 4.2%, respectively. Despite a broad year-to-date bounce in the markets, Microsoft’s stock is surprisingly flat.

Microsoft is one of the best businesses on this planet, and everybody loves its stock. Then, why are we seeing this anomalous relative underperformance at the start of 2023?

On 4th January, Microsoft’s stock fell by ~5% as Satya Nadella (Microsoft’s CEO) issued a serious warning for technology investors, and UBS downgraded Microsoft to “Neutral” from “Buy”, citing a growth deceleration in its cloud business. While I don’t really care about one analyst downgrading Microsoft, I think growing investor concerns about near to medium-term growth at the Redmond-based tech giant are highly warranted, given its premium valuation.

In his interview with CNBC, Nadella provided a grim outlook for technology companies:

The next two years are probably going to be the most challenging because, after all, we did have a lot of acceleration during the pandemic and there’s some amount of normalization of that demand and, on top of it, there is a real recession in large parts of the world. The combination of pull-forward and recession means we will have to adjust”

Honestly, Satya’s words sounded to me like a quick recap of my 2023 forecast for tech stocks:

With the FED still pulling liquidity out of our economy, a richly-valued equity market is facing the double whammy of an earnings recession and a trading multiple contraction. Microsoft is a fantastic business, but it is not immune to the broader economy. The tech giant is set to release its Q2 FY2023 quarterly report on 24th January 2023 and based on Nadella’s warning, I think this report could be a rude awakening for investors. Back in September, we discussed Microsoft’s Q2 FY2023 outlook and its management’s grim commentary on the economy in the following report:

In today’s note, we will review Microsoft’s valuation and check up on its technical chart & quant factor grades to see if it’s a worthwhile buy right now.

The Biggest Issue For MSFT Is That It’s Overvalued Going Into An Earnings Recession!

While the collapse in inflation and the moderation in interest rates are tailwinds for Microsoft’s stock, the demand environment could be about to get worse as an economic recession looms over us. Yes, Microsoft will be more resilient than most; however, it is not immune to the broader economy. For this quarter, the depreciation in the US dollar [USD] could offset the demand slowdown to a certain extent; however, Microsoft’s near-term growth looks challenged.

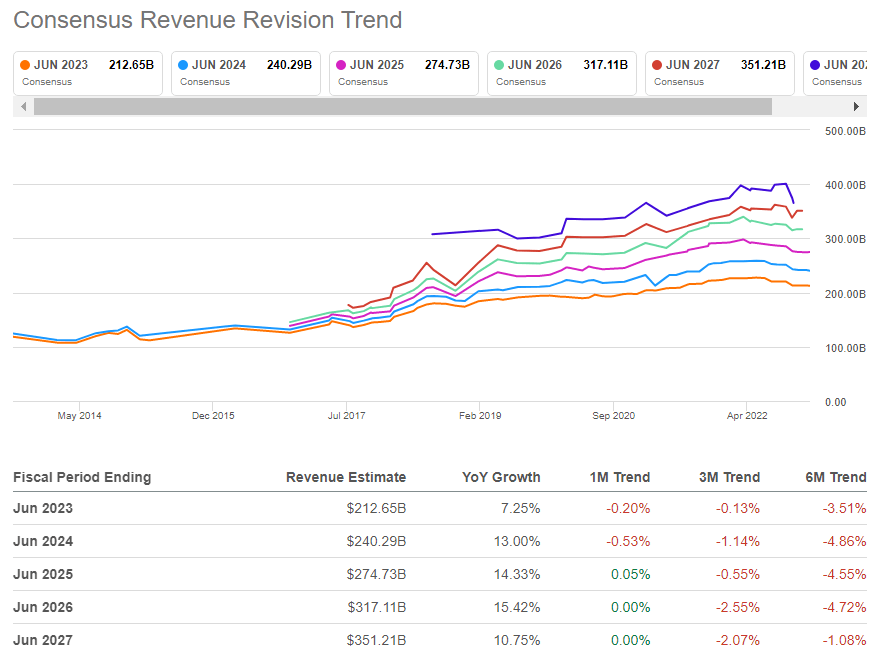

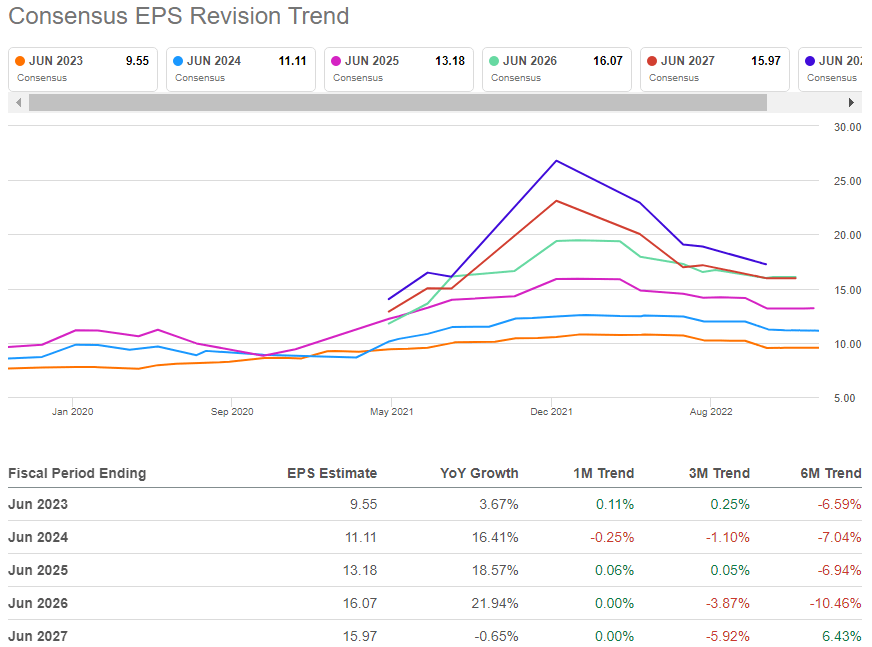

Over the last six months, Microsoft’s revenue and earnings estimates for FY2023 are down by ~3.5% and ~6.5%, respectively. And the upcoming quarterly report could lead to further cuts from analysts depending on financial performance in Q2 FY2023 and management’s guidance for Q3 and the rest of this year.

SeekingAlpha SeekingAlpha

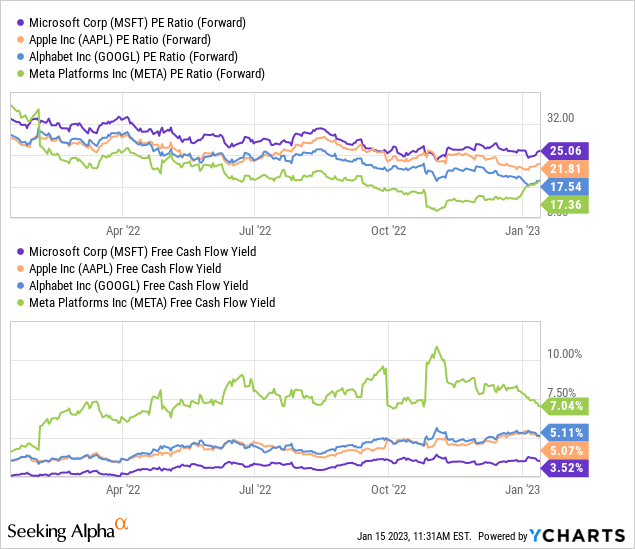

For FY2023, Microsoft is expected to grow revenue and earnings at 7.25% and 3.67%, respectively. With this drastic growth deceleration, Microsoft looks very expensive on a Price-to-Earnings basis. Furthermore, Microsoft’s free cash flow yield of 3.5% is lower than most (risk-free) treasury bonds at this moment in time. The sheer lack of equity risk premium means Microsoft is priced for perfection, and there is absolutely no room for error.

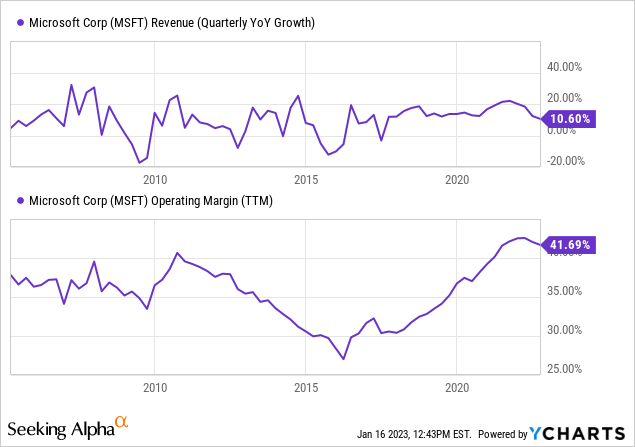

Personally, I don’t think these analyst estimates have been moderated enough, i.e., a recession is not baked into these numbers. During GFC [2007-09], Microsoft’s y/y revenue growth troughed at -17%, and operating margins compressed significantly. As of last quarter, Microsoft’s y/y growth has decelerated to ~10.60%, and operating margins are starting to come down too. If we do end up in a vicious economic downturn, Microsoft’s revenues and profitability could deteriorate significantly.

In my view, Microsoft’s stock (trading at 25x P/E) has not even priced in the ongoing growth slowdown. What happens if we go through a deep recession? Well, your guess is as good as mine, but I think Microsoft’s stock could be de-rated significantly from current levels. With all of this in mind, let’s re-evaluate Microsoft’s fair value and expected returns.

Updated Valuation For Microsoft

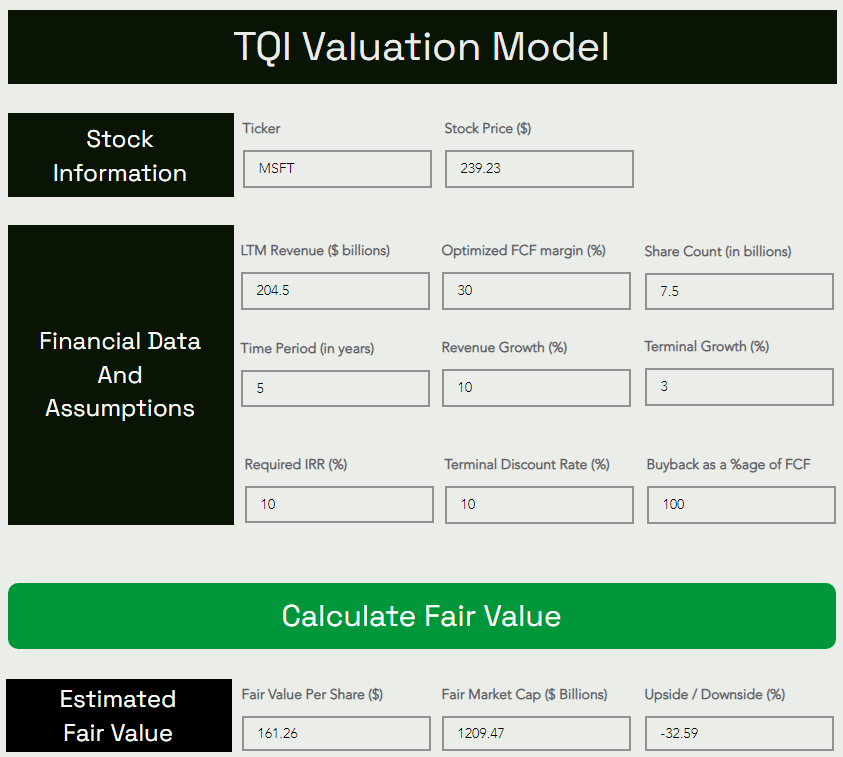

TQI Valuation Model (TQIG.org)

According to TQI’s Valuation Model, Microsoft’s fair value is ~$161.26 per share (or $1.2T). With the stock trading at ~$239 per share, I think it is still trading at a hefty premium to its intrinsic value.

Predicting where a stock would trade in the short term is impossible; however, over the long run, a stock would track its business fundamentals and obey the immutable laws of money. If the interest rates were to stay depressed, higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x. Since Microsoft’s scale and business quality deserve a premium, I assigned a base case exit P/FCF multiple of ~25x.

TQI Valuation Model (TQIG.org)

By 2027, Microsoft could grow from ~$239 to ~$399 at a CAGR of 10.77%. While Microsoft offers a double-digit CAGR return, I am still sitting on the sidelines here due to the large gap between Microsoft’s intrinsic value and its current stock price.

In the event of a recession, we could see Microsoft re-tracing to its fair value (and who knows, it could probably overshoot to the downside). Hence, I see a downside risk of 30-35%+ in MSFT. That said, I own shares in Microsoft, and I am not selling here. If Microsoft were to get down to $200, I would start buying again.

MSFT’s Technical Chart & Quant Factor Grades

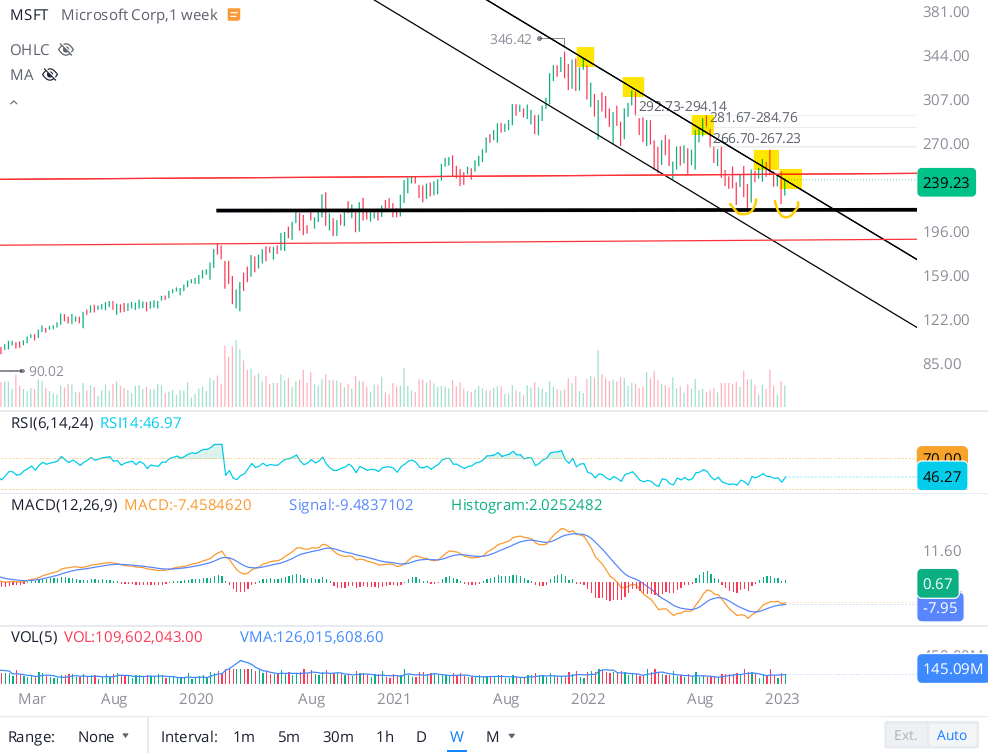

Microsoft’s stock has been undergoing a correction for more than a year now as its trading multiples normalize in a higher interest rate environment. With technology stocks showing signs of life at the start of 2023, Microsoft bulls are hoping for a breakout to the upside from the falling wedge pattern shown in the chart below. If we do break out to the upside, the first target would be the ~$265-280 range. In my view, Microsoft’s report will be decisive in determining the future path of its stock.

WeBull Desktop

As of today, the stock remains stuck in a falling wedge pattern. From a technical standpoint, the stock may just as well continue to spiral downwards and test the lower end of the falling wedge pattern. I think the $200-220 zone (200-DMA level) should act as support for the stock; however, if it fails to hold above this range amid an earnings contraction (in a recession), then we could test pre-COVID levels of $170-180.

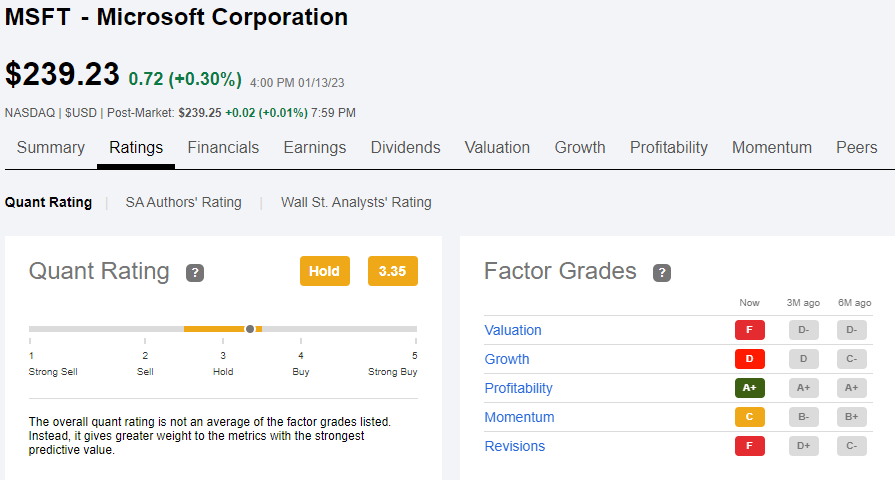

According to Seeking Alpha’s Quant Rating system, Microsoft is rated a “Hold” with a score of 3.35/5. While Microsoft’s superior profitability commands an “A+” rating, Momentum and Revisions (earnings) factor grades have deteriorated from “B+ to C” and “C- to F” in the last six months. A factor grade of “D” for Growth makes sense considering Microsoft’s sales are growing at just ~10-12% y/y. Having looked at Microsoft’s absolute valuation, I think a Valuation factor grade of “F” is fully deserved.

SeekingAlpha

Based on a mix of fundamental, quantitative, and technical data analysis, Microsoft’s stock is not a buy right now.

Final Thoughts

Heading into next week’s earnings release, Microsoft’s stock looks primed for a significant move (up or down) based on its technical chart. While the macroeconomic environment remains uncertain, Microsoft may continue to retain its safe haven status by being more resilient than its peers – like a good house in a bad neighborhood. Past headwinds – high inflation, rising interest rates, and a strong US dollar – have all turned into tailwinds in recent weeks.

While some macro headwinds have turned into tailwinds, rising wages and flailing demand (due to a weaker IT spending environment) are set to result in further deceleration in growth rates at Microsoft whilst causing a margin contraction! As I see it, the recent warning from Satya Nadella should be taken seriously by all investors.

At ~25x P/E, Microsoft is looking expensive compared to peers and the market (S&P 500 P/E: ~18x). I continue to believe in Microsoft as a business; however, the stock is overloved and overvalued. The risk/reward is unfavorable for a near to medium-term investment, and so, I am happy to sit on the sidelines until Microsoft gets down to $200 or the valuation gets better with time.

Key Takeaway: I rate Microsoft a “Hold/Neutral/Avoid” at $239.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Be the first to comment