Jean-Luc Ichard

While the current drawdown has been painful for many large-cap technology companies, I believe Microsoft Corporation (NASDAQ:NASDAQ:MSFT) is the best of the bunch and is set to outperform peers. Microsoft has the most leverage to mission critical business functions (office productivity software, cloud computing) that is relatively more immune to economic headwinds. Furthermore, Microsoft’s valuation has already normalized to pre-COVID levels, which offers an attractive entry point.

Large Cap Tech Stocks Have Sold Off, Now What?

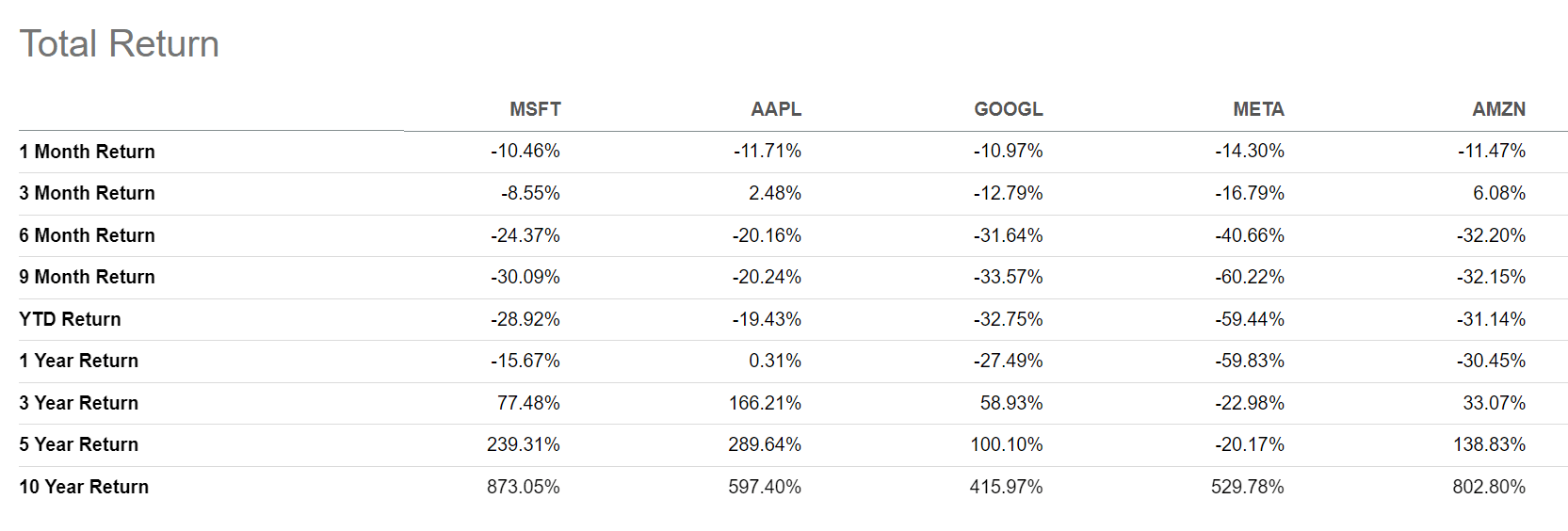

As many investors know, 2022 has been characterized by almost indiscriminate selling of high growth technology stocks, with some former high flyers such as Meta Platforms, Inc. (META) falling by almost 60% YTD (Figure 1). Even the largest technology company in the world, Apple Inc. (AAPL), has begun to falter in recent days due to concerns of slowing demand for its new handsets, which I wrote about in a recent article.

Figure 1 – Total Return of MAGMA Stocks (Seeking Alpha)

Is this a replay of the early 2000s tech bust, and investors should run for the hills and avoid all tech investments for years? While there are signs of speculative excess in the past few years (the meme stock and SPAC phenomena, for example), I don’t think we will see a lost decade like in the early 2000s, particularly for solidly profitable companies like Microsoft.

Cleanest Dirty Shirt

Each of the large technology megacaps are facing unique challenges and issues. For example, Alphabet Inc. (GOOG, GOOGL) and Meta are facing threats in their core advertising businesses from Apple and Amazon.com, Inc (AMZN), as well as headwinds from a worsening economy. Apple is seeing slowing demand for its handsets, which drives the majority of corporate profits. Amazon’s retail business is also threatened by a consumer slowdown due to the worsening economic outlook. The one company out of the five technology mega caps (“MAGMA”) that seem best positioned to outperform is Microsoft.

SaaS Subscriptions Extremely Sticky

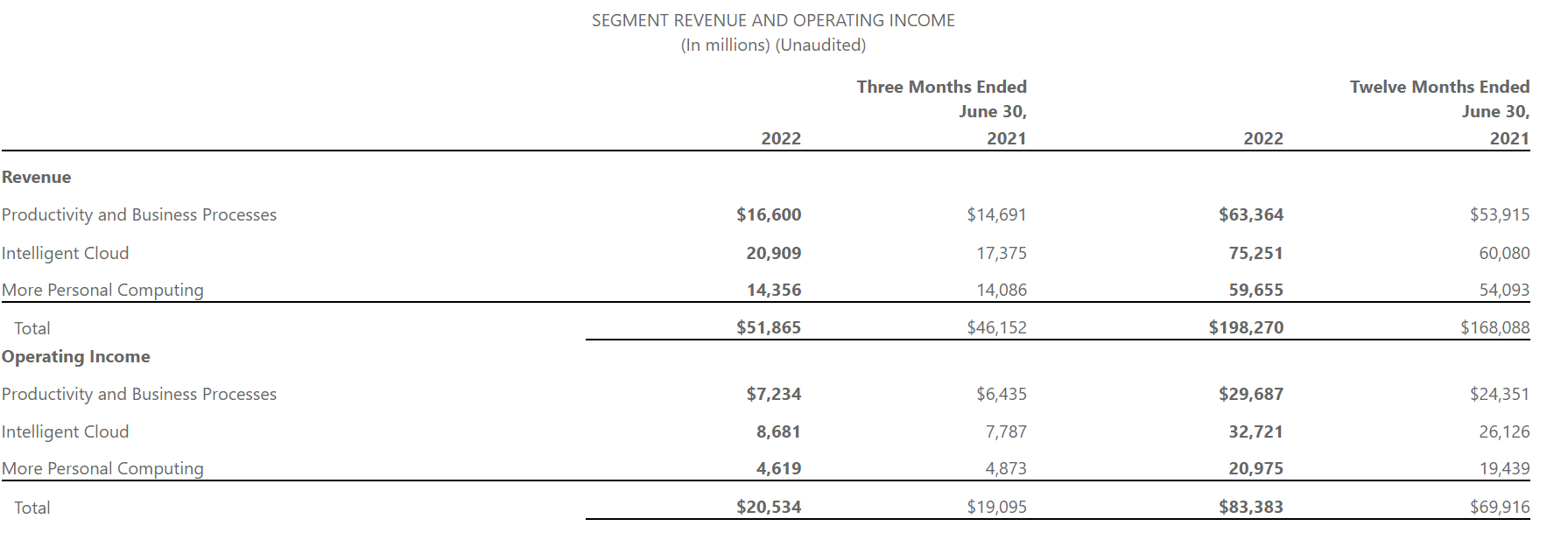

Analyzing Microsoft’s operations through its main business segments, we can draw several observations. First, the Productivity and Business Processes segment, which encompasses the Office productivity franchise, continues to see strong revenue growth. In the LTM to June 30, Productivity and Business Processes saw 17.6% YoY growth. Operating Income grew even faster at 21.7% YoY, to a 46.8% operating margin (Figure 2).

Figure 2 – Microsoft Segmented Revenues and Operating Income (MSFT Q4/F22 Report)

Essentially, Microsoft has a stranglehold on office productivity software. In years past, companies could choose to delay upgrading to the latest version of Office. As long as users didn’t care about the latest bells and whistles, core business functionalities like spreadsheets and word processing were not affected by using an older version of the software. In fact, I have personally only used four versions of Office over two decades (2000, 2007, 2013, and Office 365), as the IT departments of the companies I worked at did not think the other versions offered significant benefits compared to their cost.

However, as customers have been migrated to the SaaS subscription-based Office 365 (and the equivalent consumer offerings), the delayed upgrade cycle is no longer possible. If companies don’t pay the subscription fee, they lose access to all of their mission critical software and data.

Furthermore, the SaaS subscription model gives Microsoft the ability to raise pricing on a yearly basis, with companies essentially locked in.

Cloud Benefiting From A Growing Pie

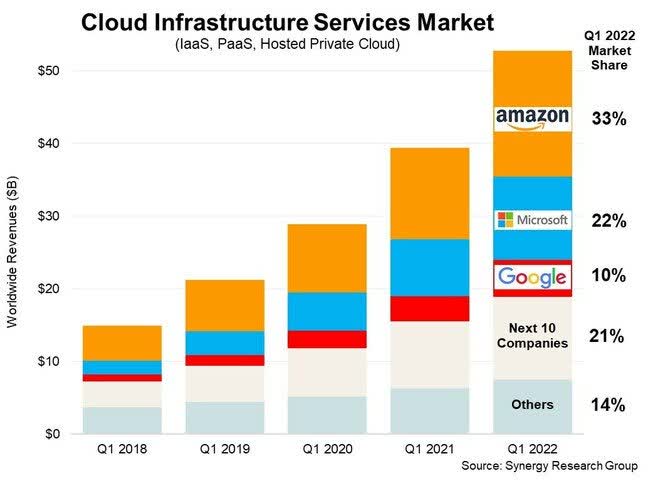

Increasingly, businesses find it cheaper and more convenient to obtain computing power from the “cloud” rather than build their own server farms. Amazon’s AWS, Microsoft’s Azure, and Google’s Cloud Platform (“GCP”) together account for more than 60% of the cloud computing market (Figure 3).

Figure 3 – Cloud Computing Market Share (Synergy Research Group via theregister.com)

Although some analysts have highlighted increased competitive pressures in the cloud computing market, so far it has not led to margin pressure. AWS reported operating margins of 29% in the latest quarter, and Microsoft’s Cloud segment appears to be even more profitable, with 43.4% operating margins in the LTM to June 30 (from Figure 2 above).

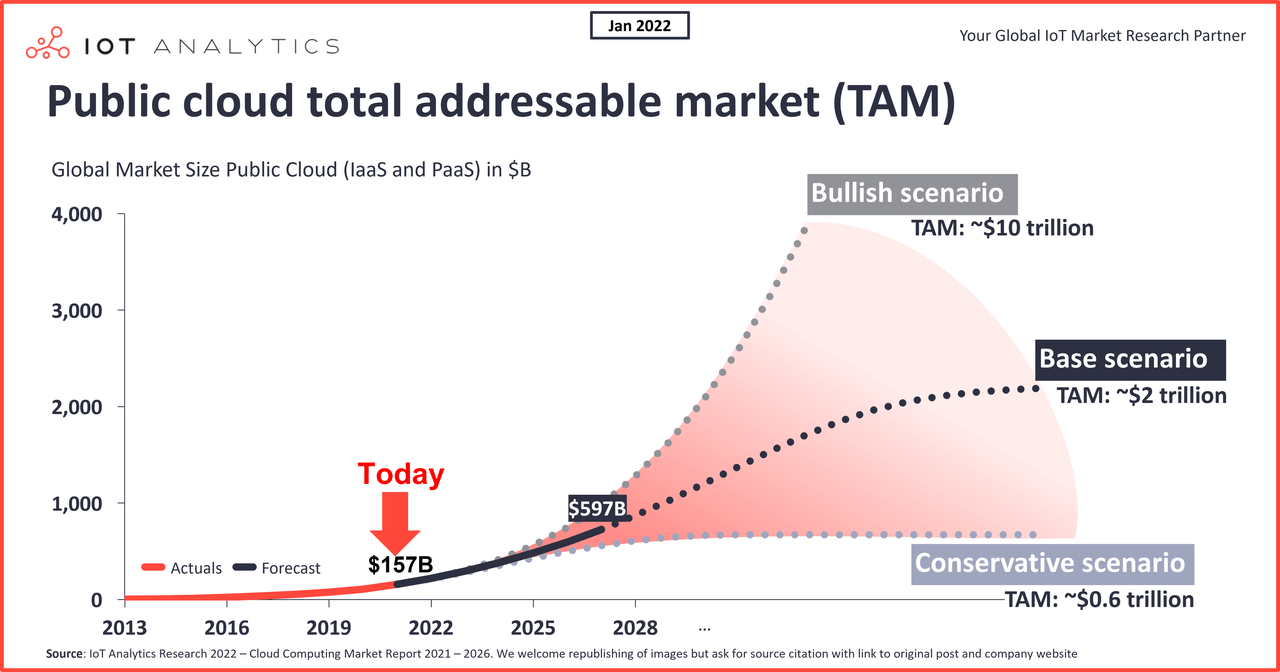

Although economic weakness could curtail some cyclical growth in the cloud business, I believe the secular tailwind from increasing cloud adoption should still provide plenty of growth and profit opportunities for Microsoft Azure for years to come (Figure 4).

Figure 4 – Cloud Computing Secular Tailwind (iot-analytics.com)

Personal Computing Weakest Link

The weakest business segment in Microsoft’s portfolio is the “More Personal Computing” segment, which encompasses OEM installation of Windows, Bing search revenues, and Xbox revenues. These are more cyclical businesses that could face headwinds in a tough economic environment. So far, from Figure 1 above, we can see that revenue growth has slowed to just 2.1% YoY in the latest quarter, and operating profits actually dipped to 31.9% operating margin vs. 34.7%.

However, investors need to put these figures into context. A business that generates $14 billion in quarterly revenues at a 32% operating margin is still fantastic!

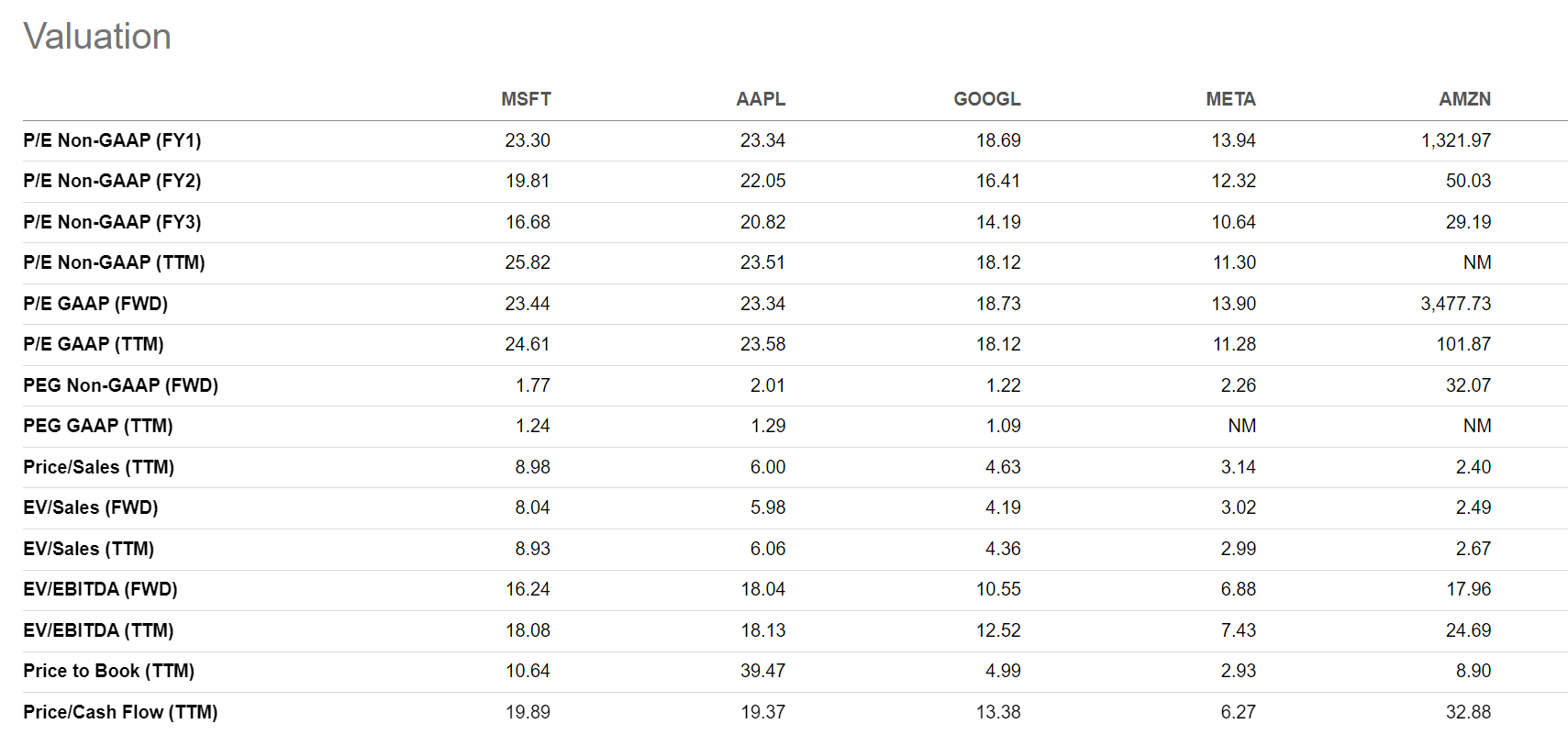

Valuation At A Justified Premium…

Microsoft currently trades at a 23.3x FWD P/E, above the sector median 16.7x. Compared to the rest of MAGMA, MSFT also does not screen cheap, having the 2nd highest FWD P/E multiple.

Figure 5 – MSFT Valuation vs. Peers (Seeking Alpha)

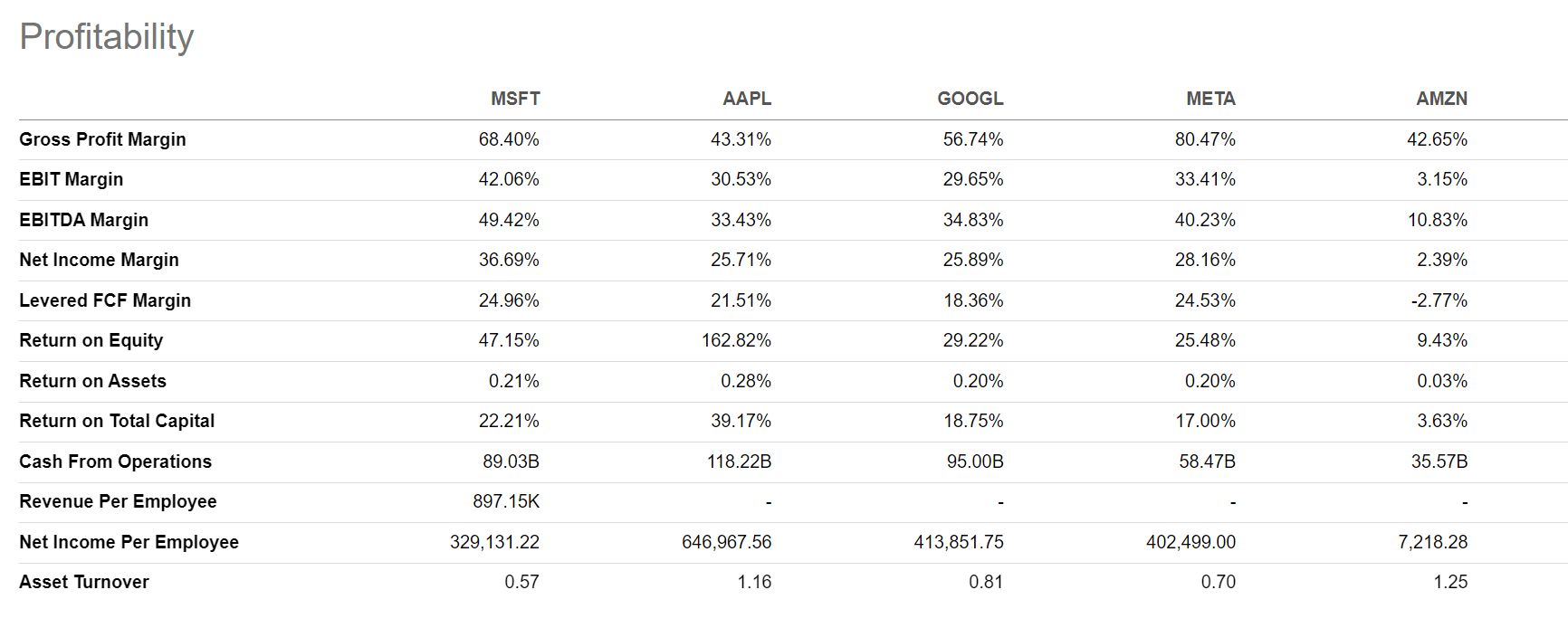

However, valuation multiples should be viewed in the context of profitability and risk. Out of the MAGMA peers, Microsoft has the highest net margin at 36.7% (Figure 6).

Figure 6 – MSFT Profitability vs. Peers (Seeking Alpha)

Also, when we think about the core business of each of the MAGMA peers, we find that they are all at significant risk from a weakening economy. AAPL’s business is consumer-facing, and the consumer is hurting right now from high inflation. AMZN derives the vast majority of its revenues from its online retail operations, which is also consumer facing. GOOGL and META both generate the majority of their revenues from advertising, which could see headwinds as companies cut back on ad-spending.

Microsoft, in contrast, has 70% of revenues tied to mission critical functions (Office 365, Cloud compute) that companies are unlikely to cut back on, unless absolutely necessary.

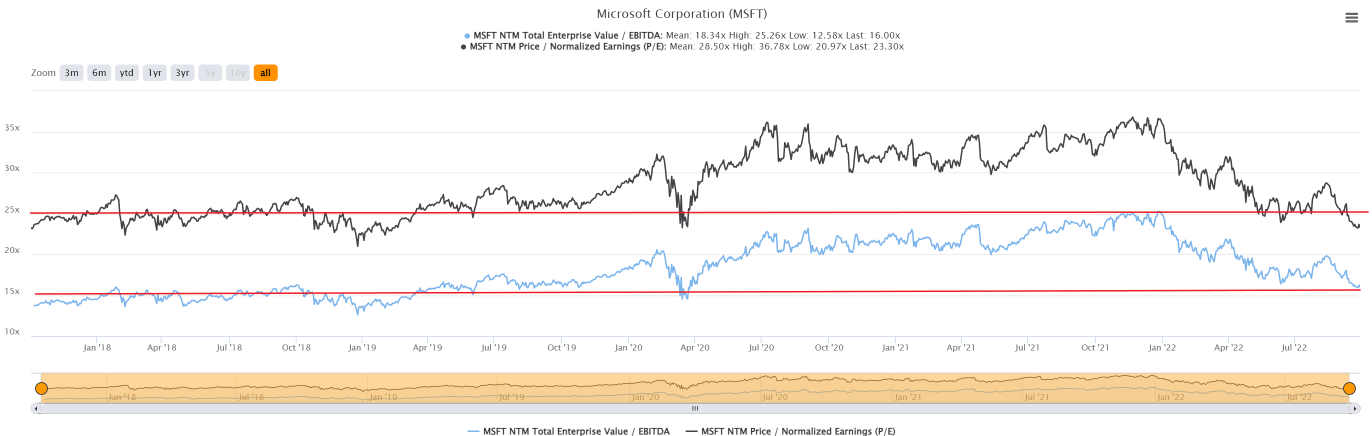

…And Normalized To Pre-COVID Levels

Furthermore, when viewed through a historical lens, Microsoft’s current valuation appears to have normalized, with both FWD P/E and EV/EBITDA returning to pre-COVID levels.

Figure 7 – MSFT Valuation Normalized To Historical Levels (tikr.com)

Although Microsoft’s valuation can still fall further, at least Microsoft is not trading at a significantly higher valuation than pre-COVID like AAPL, for example, which is currently trading at 23x FWD P/E vs. 15x FWD P/E pre-COVID.

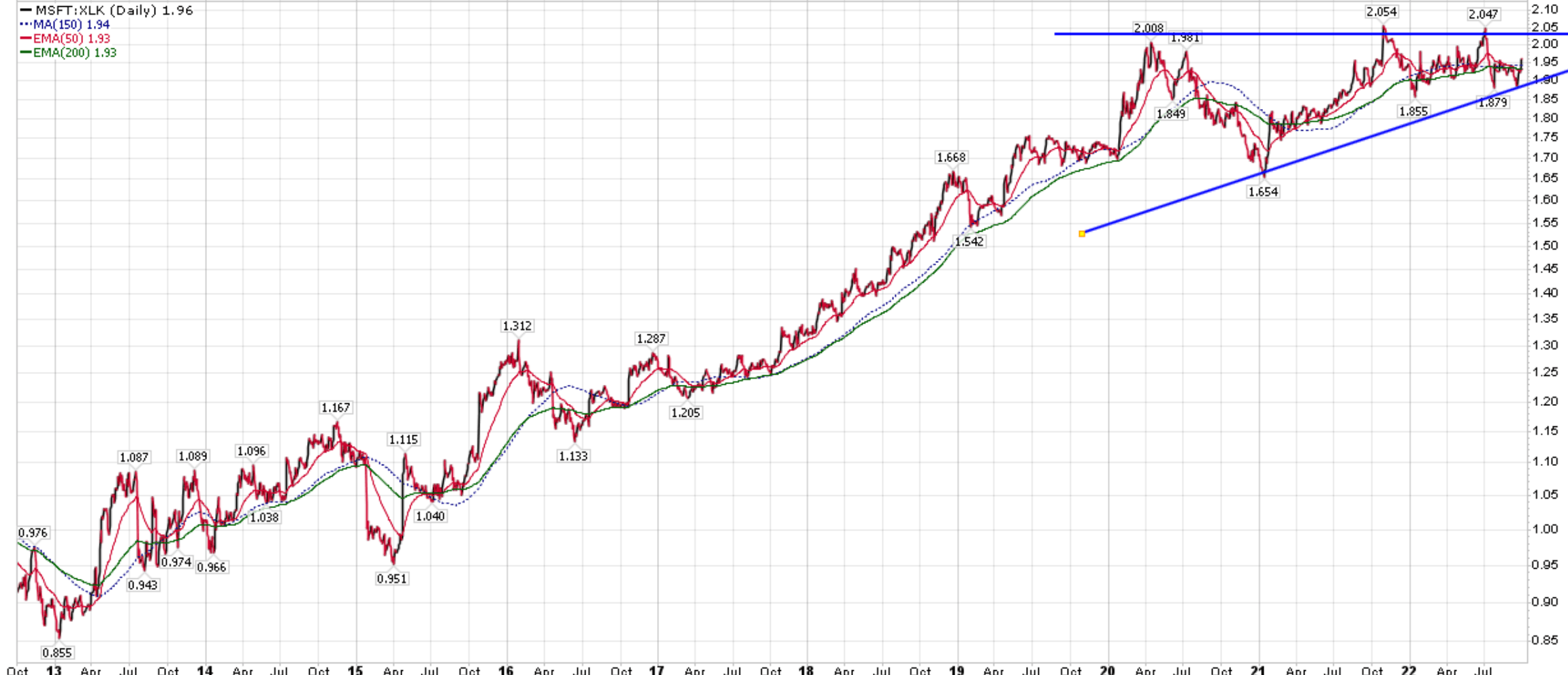

Technicals Set Up To Outperform

From a technical perspective, we can see that Microsoft has been in a multi-year sideways consolidation pattern, relative to the technology sector, as represented by the Technology Select Sector SPDR Fund (XLK). I think this chart pattern will break out to the upside, as Microsoft’s sticky productivity and cloud businesses will allow it to outperform technology peers in the next few quarters as the global economy weakens (Figure 8).

Figure 8 – MSFT relative to XLK in a bullish consolidation pattern (Author created with price chart from stockcharts.com)

Conclusion

In summary, While the current drawdown has been painful for many technology companies, I believe Microsoft is the best of the bunch and is set to outperform peers. Microsoft has the most leverage to mission critical business functions (office productivity software, cloud computing) that is relatively immune to economic headwinds. Furthermore, Microsoft’s valuation has already normalized to pre-COVID levels, offering an attractive entry point.

Be the first to comment