lcva2

Thesis

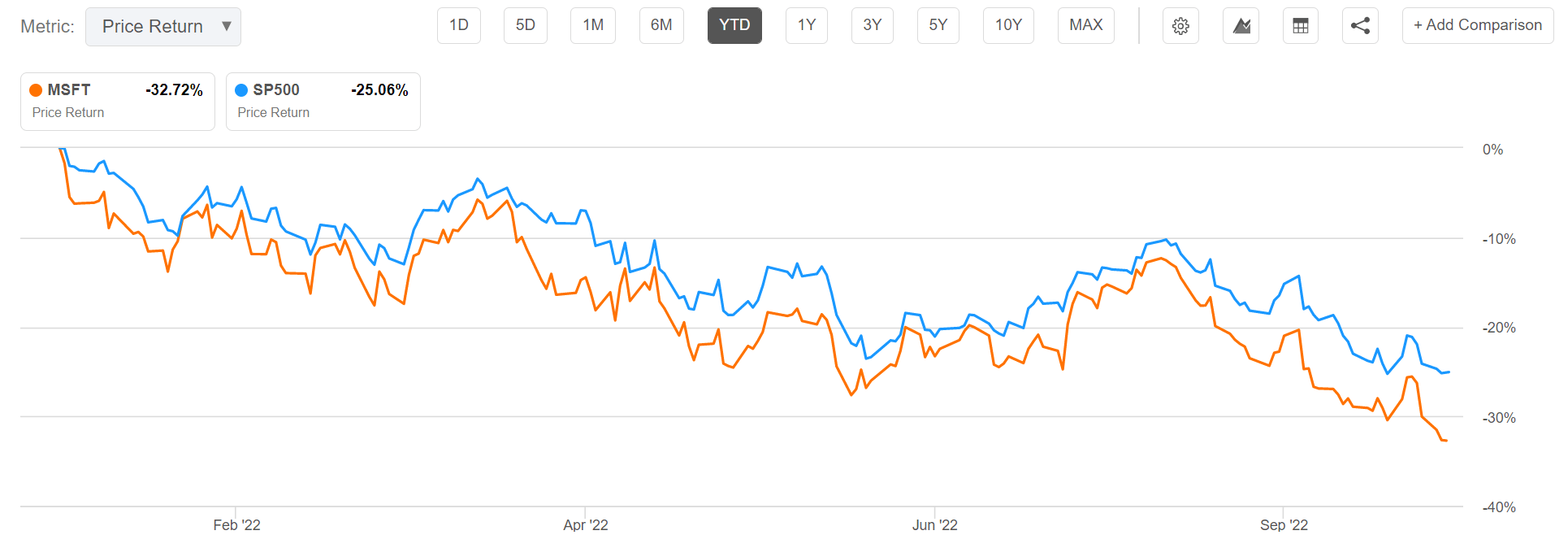

For the past 20 quarters, Microsoft (NASDAQ:MSFT) has beaten analyst consensus estimates – both revenue and earnings – 95% of time. But arguably, few quarters have needed a beat so urgently as the upcoming Q1 FY 2023. Having lost slightly less than 33% of equity value year to date, versus a loss of about 25% for the S&P 500 (SPX), sentiment is very nervous for MSFT. Perhaps to bearish?

Seeking Alpha

In this article I discuss everything an investor needs to know about Microsoft’s upcoming Q1 FY 2023 earnings results, which are expected for October 25 pre-market.

Earnings Preview

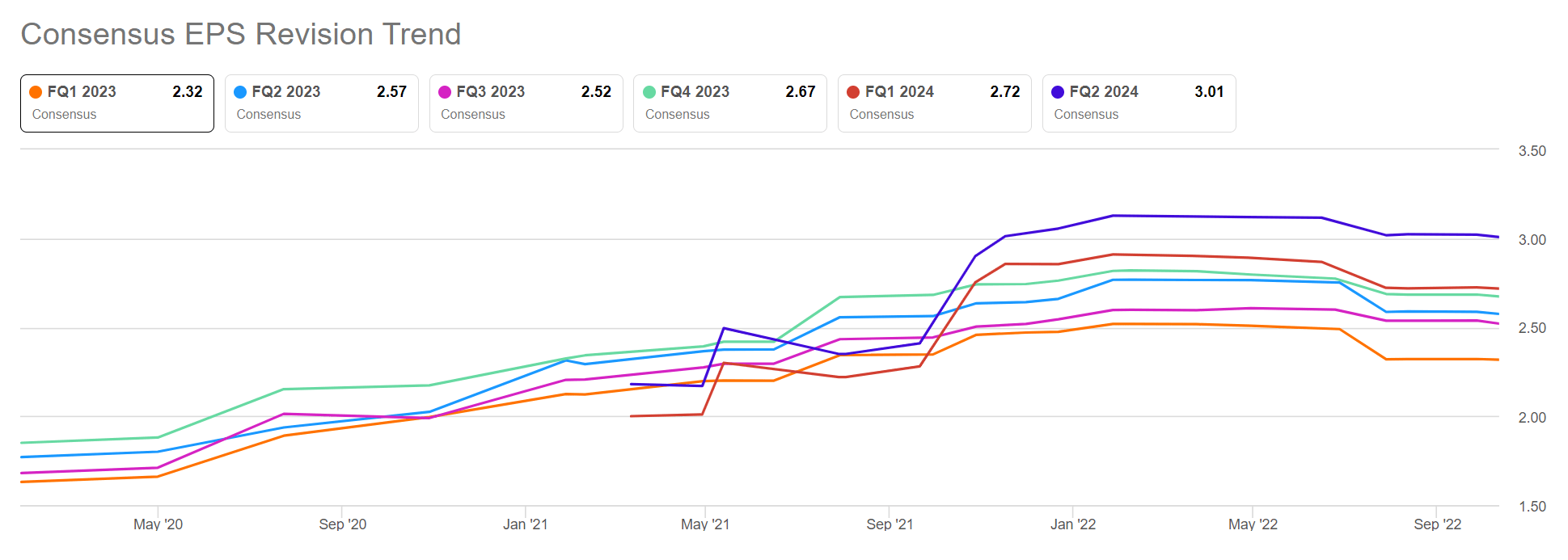

According to the data compiled by Seeking Alpha, as of October 12th, 33 analysts have submitted their estimates for Microsoft’s Q1 FY 2023 results. Total sales are expected to be between $48.67 billion and $51.44 billion, with the average estimate being $49.82 billion. So, the dispersion is actually quite wide. If an investor would assume the average as the anchor, Microsoft’s Q1 sales are estimated to grow at about 9.9% as compared to the same quarter in 2021. EPS estimates are between $2.25 and $2.46 The average is $2.32, which would imply a year over year growth of only 2.1%.

With regards to MSFT’s earnings expectations, investors should note two key points: First, earnings expectations only estimate a year over year EPS growth of slightly more than 2%, which is clearly disappointing in my opinion. And second, earnings expectations (EPS revisions) for Q3 have decreased by more than 10% versus the respective expectations in January 2022.

Seeking Alpha

Are Estimates Too Bearish?

Arguably, one of the major reasons why Q3 expectations are somewhat low is due to a very challenging macro-economic environment – driven by inflation, rising interest rates, depressed consumer confidence and geo-political tensions. And thus, investors should note that whatever bearishness is priced into the stock price, it is likely a function of the economy, and not specific to Microsoft’s competitive moat, earnings growth and business profitability.

Intelligent Cloud – Losing Steam

To counter the negative impact of a slowing, Microsoft has already announced to slow down hiring, as well as potentially laying off existing employees. According to various news outlets, the workforce reduction is predominantly affecting Microsoft’s cloud and security units.

This is surprising in my opinion, as cloud – and especially security – has been labeled as key-growth areas for Microsoft. In fact, in FY Q4 2022 management commented: (emphasis added)

In a dynamic environment we saw strong demand, took share, and increased customer commitment to our cloud platform. Commercial bookings grew 25% and Microsoft Cloud revenue was $25 billion, up 28% year over year

Moreover, specifically with regards to security, management told analysts:

As the rate and pace of threats continue to accelerate, security is the top priority for every organization …

We’re taking share across all major categories we serve. All up, our security revenue increased 40% … We are the only cloud provider with protection for the top three cloud platforms, and we are seeing more and more customers turn to us to protect their multi-cloud, multi-platform infrastructure.

Has the environment changed so materially since early June, that the market is trusting outdated information? Perhaps. Investors should consider how unexpected, fast and vicious the environment turned for other blue chip companies such as Advanced Micro Devices (AMD), Amazon (AMZN), and Nike (NKE) — to name just a few.

Reflecting on the above considerations, in my opinion, it is not unlikely that Microsoft’s major revenue driver – Intelligent Cloud, with about 45% of total sales – will disappoint in FY 2023 Q1.

Personal Computing

Microsoft’s personal computing division accounts for about one third of sales and includes Windows OEM products, Xbox content and services, Search and news advertising, as well as Microsoft Surface.

The personal computing division already slowed in Q4 FY 2022, increasing revenues only by about 2% year over year to $14.4 billion. Also, the September quarter marked a further slowdown in global PC demand – the steepest demand decline in over two decades.

Investors should not demand for too much positivity here. But expectations are likely already very low.

Productivity and Processes

Reflecting on Microsoft’s September quarter, the key (open) question for me is the performance for ‘productivity and processes’. A few months ago, Microsoft management commented that the segment is expected to grow between 12% and 14% in constant currency or $15.95 billion to $16.25 billion. And also added:

In Office commercial, revenue growth will again be driven by Office 365 with seat growth across customer segments and ARPU growth through E5. We expect Office 365 revenue growth to be sequentially lower by roughly two points on a constant currency basis with a bit more FX impact on U.S. dollar growth than at the segment level.

Although I understand that productivity gains and process-optimization efforts should be key for businesses in a challenging economic environment, I doubt that businesses will actually invest in such ‘optional’ initiatives.

Personally, I would think the lower estimate of the revenue guidance range ($15.95 billion) will be a more likely scenario.

Other Considerations

In Q4 2022, Microsoft returned to shareholders $12.4 billion in the form of share repurchases and dividends. But I think there could be considerable upside to this number in Q1 2023 and/or in the future — given that Microsoft is a net-creditor and generates about double the operating cash flow as compared to what has been distributed in FY Q4 2022.

Microsoft’s business is strongly anchored on a subscription-based business model. Accordingly, it is very unlikely that the company’s revenues and cash flows fluctuate enormously quarter over quarter. Note that as of June 2023, Microsoft recorded on the balance sheet about $43.5 billion of unearned revenues.

Investors should consider that the risk may not be in the past Q1 2023 quarter, but in the upcoming Q2 2023 and Q3 2023 quarters, which could preliminary disappoint/surprise due to a weak/strong guidance.

Conclusion

Going into the September quarter earnings season, I am less bullish on MSFT than I am for example on Meta (META) and Alphabet (GOOG) (GOOGL). I believe Microsoft’s earnings estimate are reasonable – I just do not think there will a material upside surprise as compared to sentiment.

As a consequence, I label Microsoft stock a ‘Hold’ going into earnings. But long-term I remain confident in the software giant’s earnings prospects. And there should be little doubt that the company is undervalued.

Further reading on Microsoft: Is Microsoft Stock Cheap?

Be the first to comment