FABRICE COFFRINI/AFP via Getty Images![]()

Investment Thesis

Microsoft Corporation (NASDAQ:MSFT) has been one of the best investments in the past decade, with its share price up over 700% during the period even after the big pullback last year. I believe the tech giant will continue to outperform, as it is well-positioned to benefit from different technology trends. Despite having a market cap of over $1.8 trillion, the company still has a lot of room to grow. There are multiple growth opportunities out there, as cloud and AI are only in their early innings and Microsoft is poised to benefit from the tailwinds. The latest quarterly earnings appear to be mixed, but Azure killed it once again with impressive growth.

Microsoft seems expensive compared to other large-cap tech companies, but considering the quality, a premium is more than justified. On a historical basis, the valuation is actually very fair, as its multiple is now below the 5-year average. It also has one of the best management teams with very shareholder-friendly policies. Microsoft continues to be one of the highest-quality companies, and I rate it as a buy at the current price.

Huge Growth Opportunities

The most obvious growth driver at the moment continues to be Azure and related cloud services, which recorded a 25% growth despite facing a tough backdrop. Cloud is still in its early days and the opportunity it presents is truly massive. According to Precedence Research, the global cloud computing market is expected to grow from $446.5 billion in 2022 to $1.61 trillion in 2030, representing an impressive CAGR (compounded annual growth rate) of 17.4%. On a relative basis, the penetration rate of Azure is actually still quite small. I think we will see an acceleration in cloud spending, as digital transformation is now happening at a much faster pace compared to the past few years.

AI presents another huge growth opportunity. ChatGPT has been the latest hot controversial topic as Microsoft further invested multi-billions in OpenAI, its parent company. Some say it is a total game changer and some say it is just an overhyped AI tool. I believe ChatGPT will open up many new growth opportunities, and the investment is certainly worth it. Is this an iPhone moment for Microsoft? Probably not. But does it need to be an iPhone moment for this to work? Also no.

Satya Nadella, CEO, on OpenAI’s partnership

“In this next phase of our partnership, developers and organizations across industries will have access to the best AI infrastructure, models, and toolchain with Azure to build and run their applications.”

I do not think ChatGPT as a standalone product will be too valuable at the moment, it recently launched a professional plan that charges $42/month so you can imagine how hard it would be to generate meaningful revenue. I believe its integration with Microsoft’s product is what will matter the most. Through the integration with products such as Azure, Office365, and GitHub, ChatGPT is able to bring superior AI capabilities to these products and vastly improve its competitive advantage. The combination with Bing should also be quite interesting as it can now offer a search platform that excels at informative queries.

Another hidden opportunity would be the integration with Nuance, an AI communication company Microsoft acquired for $19.7 billion in 2021. The integration should see strong synergies and level up the capabilities of Nuance’s current conversational AI products. Overall, I believe ChatGPT should bring a lot of value and growth by improving and revamping the current offerings from Microsoft.

There are also a few smaller opportunities that could turn out to be huge. The company has been gaining strong traction in the advertising space, with obviously LinkedIn and also the surprising partnership with Netflix (NFLX) for its ad-supported membership. With Netflix reporting better-than-expected subscriber growth and now looking to further work on its ad-supported plan, I believe this could boost ad revenue moving forward.

Another example would be GitHub, which passed $1 billion in ARR (annual recurring revenue) last year with over 90 million active users. The developer ecosystem has been growing rapidly, and the DevOps market is now forecasted to reach $57.9 billion in 2030 with a CAGR of 24.2%, according to Allied Market Research. There are just so many opportunities out there for Microsoft to capture, and these technology trends should continue to drive growth in the future.

Dividends and Buybacks

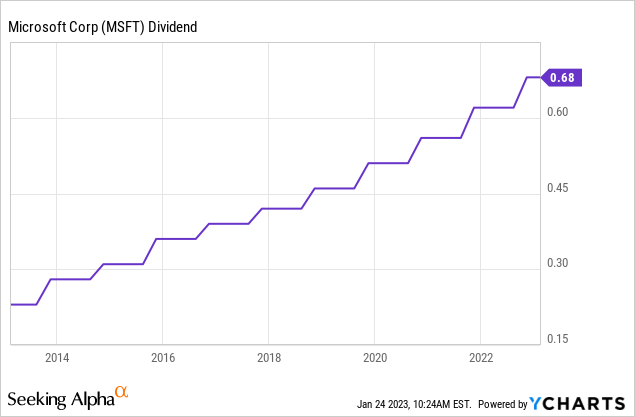

Microsoft has very shareholder-friendly policies and actively returns cash through dividends and buybacks. Even though the current dividend is $0.68, which translates to a yield of only 1.05%, the company has consistently increased the payout every year. From the first chart below, you can see that the dividend has actually grown over 200% in the past decade.

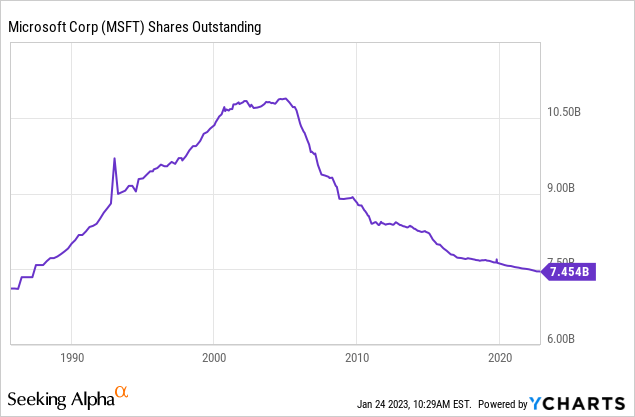

Besides dividends, Microsoft has also reduced its share count significantly through share buybacks. From the second chart below, you can see that since the mid-2010s, the company’s share count dropped from slightly over 10.5 billion to around 7.45 billion currently, which represents almost a whopping 30% reduction. This boosts the EPS figure substantially which in turn provides strong support for the stock price. Considering the strength of the company’s balance sheet, I believe dividends and share buybacks will continue to increase in the foreseeable future.

Financials and Valuation

Microsoft reported its fiscal second quarter earnings yesterday, and the results are very mixed. Cloud continues to be the spotlight while personal computing took a hit due to the weakening economy. The company reported revenue of $52.7 billion, up 2% YoY (year-over-year) compared to $51.7 billion (or 7% growth using constant currency). The growth is largely driven by the strength in cloud revenue, which was up 18% YoY to $21.5 billion. Azure was the star within the segment with a whopping 31% growth.

The productivity and business segment also showed decent growth with revenue increasing 7% YoY to $17 billion. This is led by Office365 and Dynamic365 with 11% and 21% respectively, further proofing the strength of its subscription products. The personal computing segment was what dragged the overall result down. It reported revenue of $14.2 billion or a 19% decrease YoY. Within the segment, hardware suffered the most as Windows OEM revenue and Devices revenue were both down 39% YoY.

I am not too worried about this, as Microsoft is continuing to transform into a pure software company. Cloud remains strong and now accounts for over 40% of total revenue while personal computing only accounts for roughly 27%. The weighting should continue to shift towards the cloud segment, and the company should see more resilient growth moving forward.

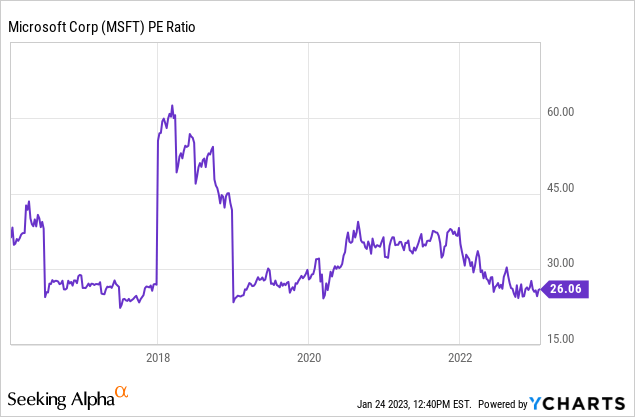

After the drop in share price last year, Microsoft is now trading at a P/E ratio of 26.06x. This is above other tech mega-caps like Apple (AAPL) and Google (GOOGL) but is actually at the lower end of its historical valuation since Satya Nadella took over in 2014, as shown in the chart below. Besides, the company has evolved a lot in the past decade. Fundamentals have improved a lot with the shift from a licensing business model to a subscription business model plus a bunch of important acquisitions such as LinkedIn in 2016 and GitHub in 2018. Cloud has also grown from being a small piece to now accounting for one-third of the revenue. The current valuation is definitely fair in my opinion considering the quality and growth opportunities it has.

Conclusion

In conclusion, I believe Microsoft Corporation will continue to outperform in the future. It is seeing some headwinds from the weakening economy but the long-term growth trajectory remains intact. There are still multiple huge opportunities out there, especially with cloud and AI, which continue to show impressive growth this quarter. ChatGPT should also boost growth through different integration moving forward. Personal computing was slowing down but as mentioned above its importance should continue to decline over time.

The current Microsoft Corporation valuation is at the low end of its historical average, and ongoing buybacks should provide some support for the share price. Therefore, I rate Microsoft Corporation as a buy.

Be the first to comment