PonyWang

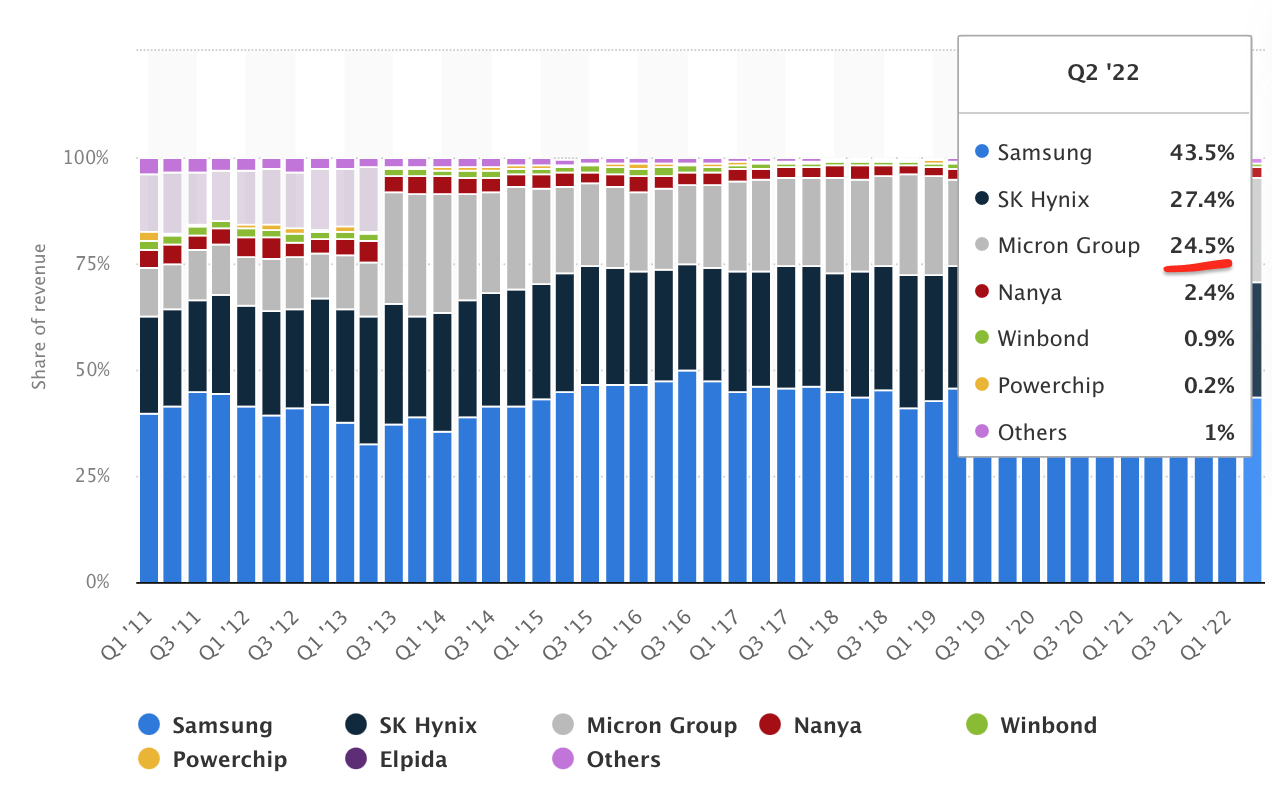

Micron Technology, Inc. (NASDAQ:MU) is a semiconductor manufacturing company that is one of the “big three” suppliers of DRAM (Dynamic Random Access Memory) with a 24.5% share of the market, just behind Samsung (OTCPK:SSNNF, OTCPK:SSNLF) at 43.5% and SK Hynix at 27.4%.

DRAM market share (Statista)

DRAM contributes to ~69% of Micron’s revenue and is a key component of all computers. If you open up your laptop to upgrade your RAM, you will likely see a Micron product or “Crucial,” which is a brand owned by Micron. The DRAM industry is forecasted to grow at a 9.2% compounded annual growth rate [CAGR] and reach a value of $221.67 billion by 2027. This is expected to be driven by the growth in electronics, the Internet of Things [IoT], Data centers and more. Micron also manufactures NAND [flash memory], which is expected to have up to 3 times more usage in 5G smartphones.

Given this backdrop, you would expect Micron to be thriving in this environment, but it is not. The industry is currently going through a cyclical downturn right now and Micron is experiencing a lot of pain as a result. However, the long-term secular trend is positive. In addition, management is being proactive, buying back shares and rigorously slashing capital expenditures. In this post, I’m going to break down Micron’s recent financial report and valuation, let’s dive in.

Earnings Bloodbath

In the first quarter of the fiscal year 2023 as reported on 21 December, Micron reported $4.1 billion in revenue. This declined by an eye-watering 39% quarter-over-quarter and 47% year-over-year. This was mainly driven by a “severe imbalance” between supply and demand. In 2020, we saw a “chip shortage” as the economy reopened and industry boomed. However, since 2022, the macroeconomic environment has been atrocious, driven by high inflation and rising interest rates, which has partly caused a sharp decline in this demand. This was then combined with an oversupply of many chips being produced, but not getting to customers fast, because of supply chain constraints. We are now experiencing a cyclical downturn in the market.

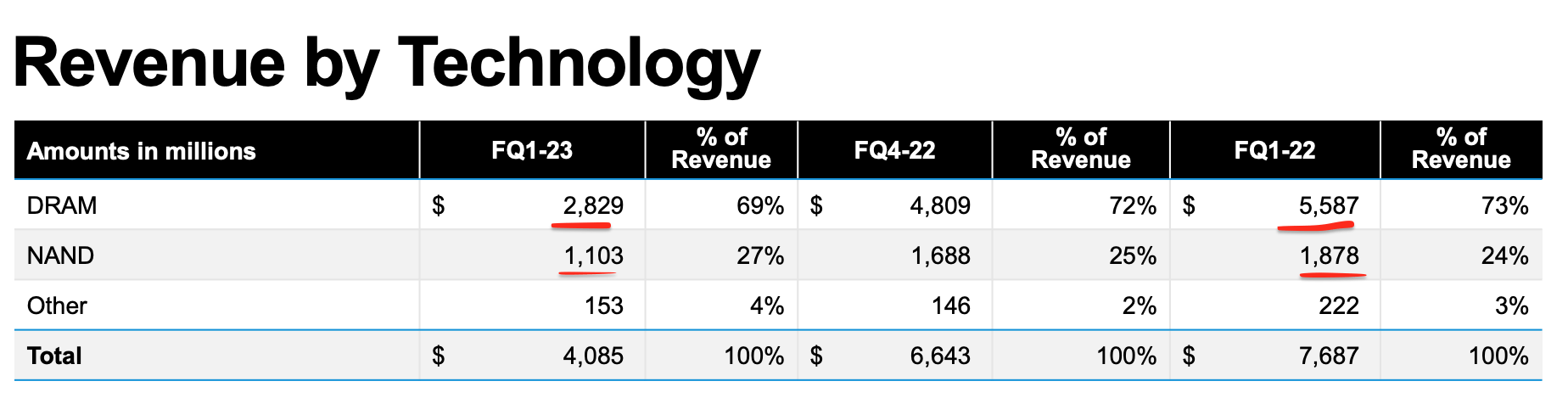

Breaking revenue down by technology, DRAM [Dynamic Random Access Memory] revenue in the most recent quarter was $2.8 billion, which declined by 41% quarter-over-quarter. This was driven by a mid-20% range decline in overall volume “bit shipments” and a price decline in the low 20% range, as the company aimed to sell through its inventory at a discount.

NAND revenue contributed 27% of Micron’s total revenue and followed a similar dynamic. Its revenue declined by 35% quarter-over-quarter, to $1.103 billion. This was driven by bit shipments declining by the mid-teens and prices declining by the low 20% range.

Revenue by Technology (Q1.FY23 report)

The positive is Micron is still a leader and innovating across both its DRAM and NAND [Flash Memory] chips. The company has had the first-mover advantage in producing its “1-beta” DRAM. This offers 15% better power efficiency and a 35% improvement in bit density over previous models. Its latest “232-Layer” NAND also is manufactured at a lower price point than previous versions, which should boost margins long term.

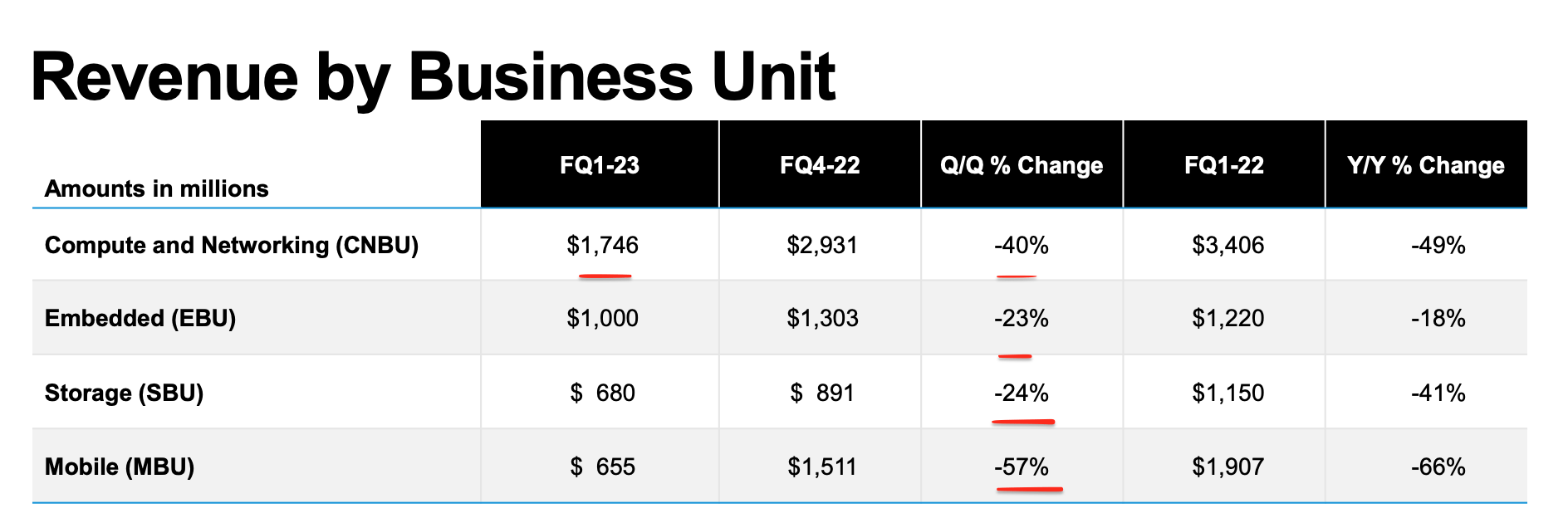

Breaking down revenue by business unit, Compute and Networking revenue was $1.746 billion, which declined by 40% quarter-over-quarter. This nosedive was a weakness in demand across client, graphics, and surprisingly data centers. The Cloud has been a solid growth industry over the past few years. It is the fastest-growing segment of many companies such as Amazon (AMZN) with AWS, and Google (GOOG) with Google Cloud. However, Micron is forecasting cloud demand below its “historic trend,” due to investor reductions by key customers. A positive is the Cloud industry is still forecasted to grow at a rapid 17.9% compounded annual growth rate to $1.24 trillion by 2027. In addition, Micron has continued to sample new products such as the “CXL DRAM” with it data center customers in FQ1. In addition, the company has completed the “qualification” of its groundbreaking 176-layer QLC NAND with a large enterprise customer.

Revenue by business Unit (Q1,FY23 report)

The Embedded business unit revenue was $1 billion in FQ1, which declined by 23% sequentially and 18% quarter over quarter. This was pretty terrible again but a positive is automotive revenue did show strength. Automotive revenue increased by ~30% year-over-year, which was slightly below the prior quarterly record in fiscal Q4,2022. The industry trend toward electronics packed vehicles and fully electric vehicles doesn’t show much sign of slowing down long term. Management is forecasting “robust growth” for automotive memory in the full fiscal year 2023, with bit growth “twice the rate” of the market. This is expected to be driven by more advanced driver assistance systems and the next wave of in-vehicle infotainment dashboards which are coming online.

The Storage business unit revenue was $680 million, which declined by 41% year-over-year. Its Mobile business revenue generated $655 million, which was partially driven by the timing of orders. Moving forward management is forecasting “flat to slightly up” demand for smartphone units.

Profitability and Expenses

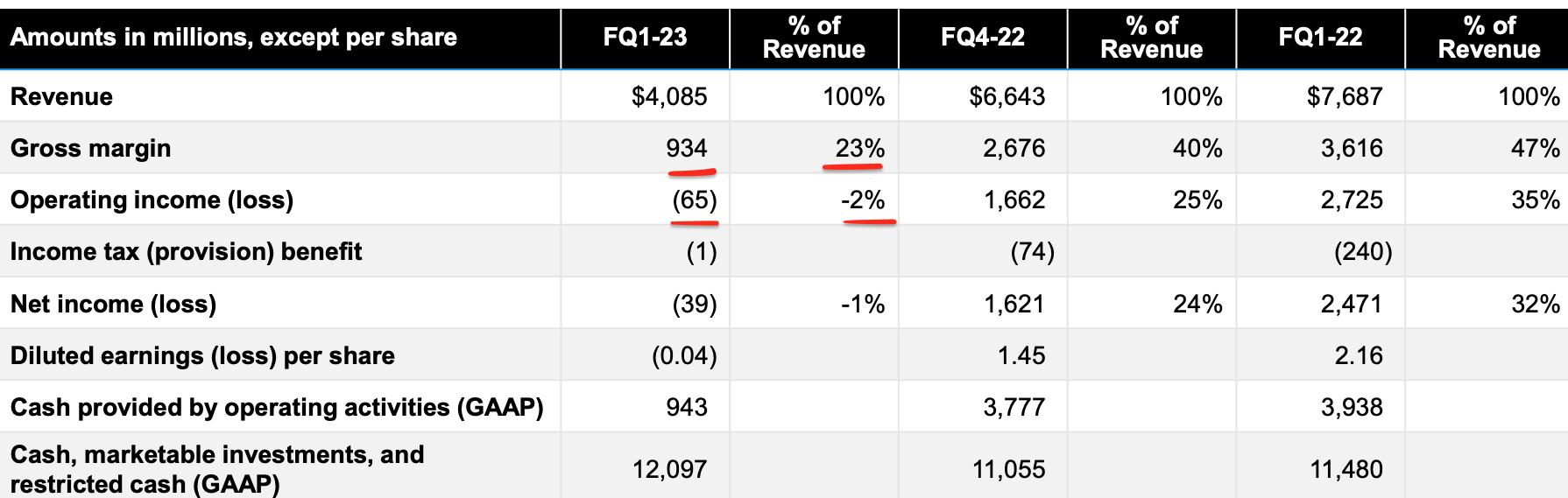

Micron reported a gross margin for FQ1 23 of 22.9%, which declined by 17 percentage points quarter-over-quarter. This was primarily driven by lower pricing as the company planned to offload its inventory and sell units at a discount. Its Operating margin nosedived from a healthy 25% in the prior quarter, to negative 2%. This resulted in Micron reporting a loss of $65 million in the quarter. A positive is the company has taken a series of actions to reduce its expenses. Operating expenses in fiscal Q1, declined by $50 million over the prior quarter, to $101 million.

Micron Financials (Q1FY23)

In Q1 FY23, Micron reported $943 million in cash from operations or 23% of revenue. In addition, the company reported $2.47 billion in capital expenditures which has trended downwards from $3.267 billion in the equivalent quarter last year. Moving forward into the full fiscal year 2023, management aims to reduce its Wafer Fabrication Equipment [WFE] expenses by 50% year-over-year.

Capital Expenses (Q1,FY23)

Free cash flow (“FCF”) was negative $1.5 billion in Q1, FY23, which was down from the $671 million in the prior year. The company reported fiscal Q1 inventory of $8.4 billion.

Management showed confidence long term as the company bought back 8.6 million shares, at an average price of $49.57. This equated to $425 million.

Micron has a robust balance sheet with $12.1 billion in total cash and investments and $14.6 billion in total liquidity. Due to the macroeconomic uncertainty, management did add an eye-watering $3.4 billion of debt to improve their liquidity position. This brings the total debt to $10.3 billion.

Given macroeconomic uncertainty and the market environment, we bolstered our liquidity in the quarter through $3.4 billion of added debt, bringing our total fiscal Q1 ending debt to $10.3 billion. This extra debt could be seen as a risk, but I will discuss more about that in the “risks section.”

Outlook

In Q2,FY23 management is expecting bit shipments to increase for both DRAM and NAND, but revenue to still be down due to lower prices. However, the company is expecting a $120 million insurance payout in the quarter, related to an operational disruption in 2017. In the second quarter, management is forecasting approximately $3.8 billion in revenue, which would imply a 51% decline year over year and 7% decline quarter over quarter.

After the second quarter, management is expecting revenue and free cash flow to improve and demand to continue to recover. However, the company is expected a substantial $460 million cost of goods sold headwind related to “wafer start reductions” in the fiscal year 2023.

Advanced Valuation

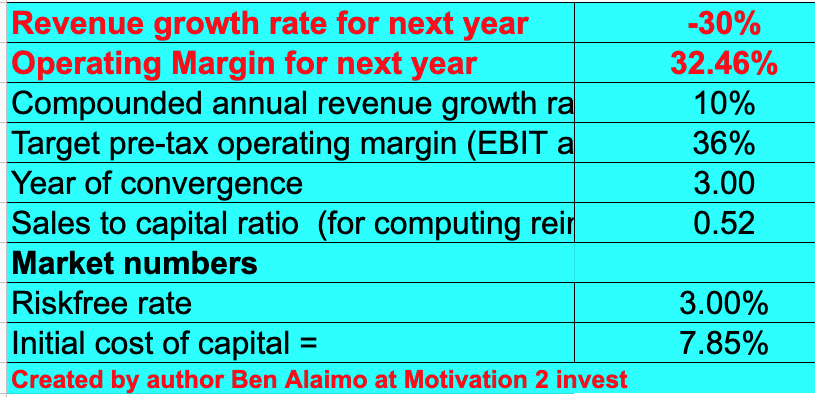

To value Micron, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow (“DCF”) method of valuation. I have forecasted negative 30% revenue growth for next year as revenue recovers but still remains down from the prior year. However, in years 2 to 5, I have forecasted 10% revenue growth per year.

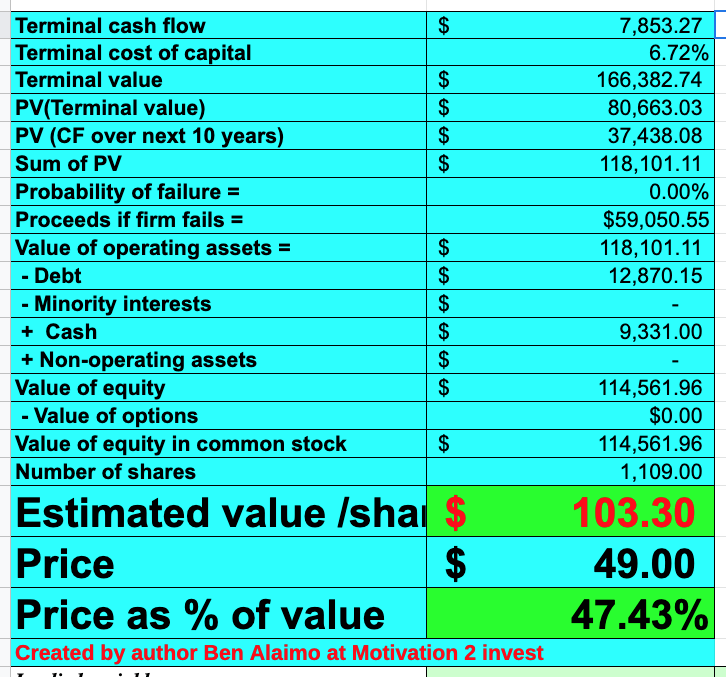

Micron stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized the company’s R&D expenses which has lifted net income. In addition, I have forecasted its margins at 36% over 3 years. This is fairly optimistic, but based upon rigorous cost controls, combined with higher prices as demand is expected to recover.

Micron stock valuation 2 (created by author Ben at Motivation 2 Invest)

Given these factors, I get a fair value of $103.30 per share. Micron stock is trading at $49 per share at the time of writing, and thus is over 50% undervalued.

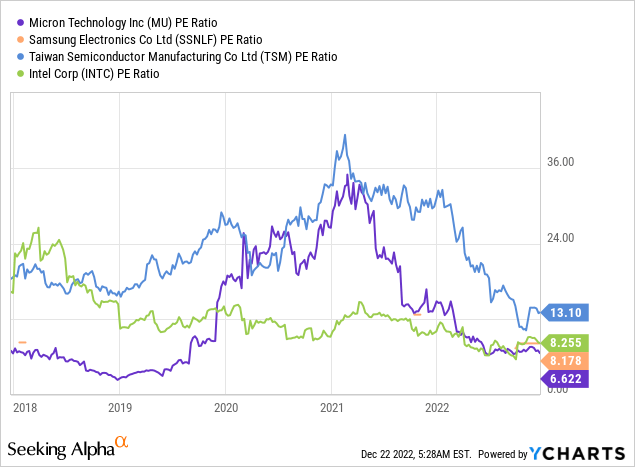

As an extra data point, Micron trades at a Price to Earnings ratio = 6.6, which is 51% cheaper than its 5-year average. In addition, it is surprisingly cheaper than other companies in the semiconductor manufacturing industry, such as Intel (INTC) which trades at a P/E ratio = 8.3, and TSM, which trades at a P/E ratio = 13.1.

Risks

Recession/Semiconductor demand

We are currently in a rising interest rate and high inflation environment, which has caused many analysts to forecast a recession. Micron’s management recently loaded on $3.4 billion worth of debt, which could be risky especially as the cost to service debt has increased due to interest rate hikes.

We are also experiencing a cyclical downturn in the electronics – and thus semiconductor – industry. A positive is the long-term secular growth trend is forecasted to be up, and thus I forecast a rebound.

Final Thoughts

Micron Technology, Inc. is a technology leader in both DRAM and NAND technology, two key components of modern-day computers and electronic devices. The industry is currently going through a cyclical downturn right now but is poised to grow long-term. Micron stock is undervalued intrinsically and relative to historic multiples, therefore, the stock could be a great long-term investment opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment