stockcam

In my previous article Meta: Ads Business Growth At Risk, one question from the audience was how WhatsApp’s future monetization would impact Meta’s (META) stock price. This article took a closer look at WhatsApp, and focused on both their quantitative and qualitative aspects.

WhatsApp and WeChat – Similarities and Differences

This year, Meta CEO Mark Zuckerberg mapped out a super app-like vision for WhatsApp that would enable consumers in Brazil to find, message, and purchase within the chat. In 2019, Zuckerberg laid out his ambitions to turn Meta’s platforms into an all-in-one tool of “calls, video chats, groups, stories, businesses, payments, commerce, and…many other kinds of private services.” In the same year, Zuckerberg lamented that he didn’t listen to advice from The Information’s Jessica Lessin in 2015 to copy the success of WeChat.

In this section, I would mainly focus on the comparison between WhatsApp and WeChat.

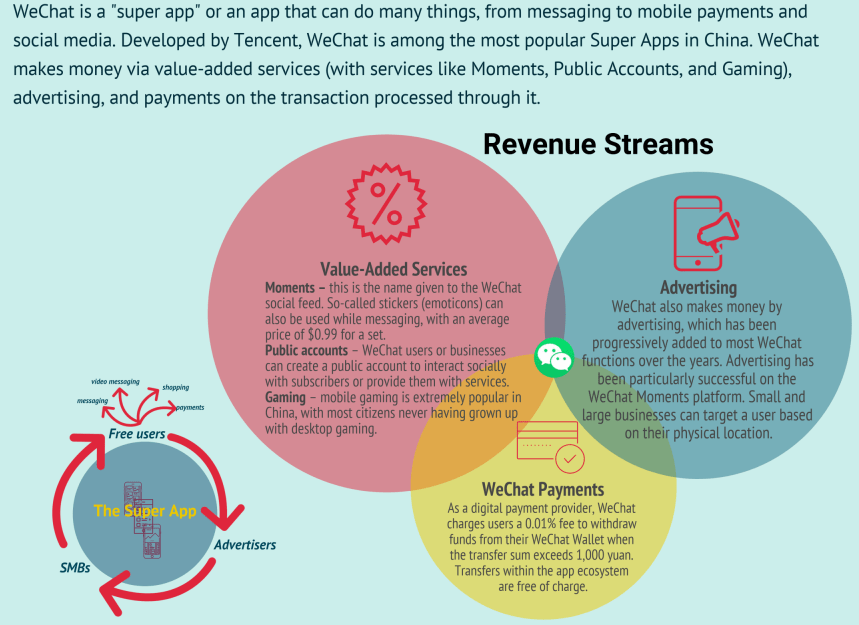

WeChat has established a variety of revenue streams as shown in the below figure.

fourweekmba.com

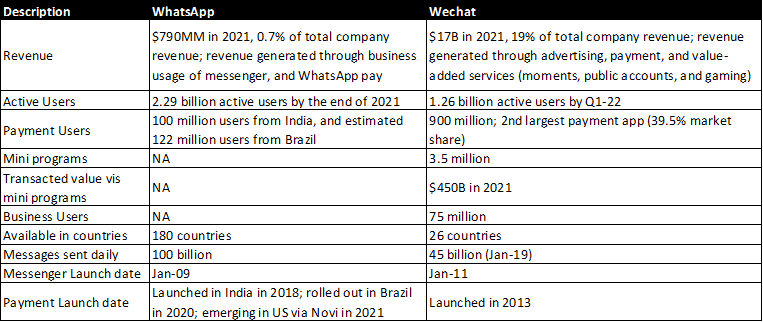

The following figure shows the comparison of WhatsApp and WeChat. Both have existed for over one decade, attract over one billion users across multiple countries, and serve both business users and consumers. Although numbers of users for the two platforms are comparable, WeChat’s monetization is more advanced. WhatsApp’s monetization is limited to business messaging usage and payment, whereas WeChat has expanded to more value-added services such as moments and gaming, and 3.5 million mini programs. WeChat has another name as “Everything App”.

Internet

I think there are three key differences between WeChat and WhatsApp that investors should pay attention to.

Contents: WeChat users spend 82 minutes on average every day. This represents high engagements. For comparison, users spend 32 minutes on TikTok, 33 minutes on Facebook, 28 minutes on WhatsApp, and 30 mins on Netflix. WeChat has gone well beyond a messenger, and created differentiated contents for quick and broad circulation. There are a good number of sophisticated WeChat operators or influencers proficient in creating original contents with 100k+ page views. Content creation, Traffic acquisition, and Advertising monetization reinforce each other in the WeChat ecosystem. The entire ecosystem has helped develop very rich 1P data for WeChat to monetize via advertising.

Competitive Landscape: In China, there is not any substitute for WeChat. However, in the US, WhatsApp is competing with Snapchat, Discord, and other. I am positive that WhatsApp can make great progress in India and Brazil, and maybe other international markets where fierce competition does not exist. For US, I am eager to see something more compelling.

Culture: WeChat’s success to some extent has been reinforced by Chinese culture. Red packet reflects a key aspect of Chinese culture, where families, relatives, and friends express their best wishes along with red packets filled with a certain amount of RMBs. WeChat Pay expanded this tradition beyond geographical boundaries and made sure the transaction can be done in one second. For businesses, WeChat has accelerated the transition of customer services of millions of businesses to a social network, which is a net result of 1) mobile-dominated and paperless business environment; 2) 24*7 customer services (pre-sales) that each consumer has access to; 3) swift services online vs long line at brick-and-mortar stores.

WhatsApp’s chance to succeed

To quantify WhatsApp’s impact, we should look at three buckets based on addressable timelines.

1) WhatsApp becomes a leader in messenger and payment app of India and Brazil (and a few other international markets in the future). WhatsApp is very likely to succeed, but the financial results from those markets will unlikely move the needle.

2) WhatsApp builds more offerings beyond messenger and payment via its Metaverse strategy, and eventually generates advertising revenue. This makes sense to build upon where WhatsApp has succeeded in the first step. Again, it’s very likely for WhatsApp to become an Everything-App in India, Brazil, and a few other international markets. However, the financial results from those markets will still not move the needle.

3) WhatsApp brings success back to the US market. At this point, I would not speculate as much considering already-saturated messenger apps market (WhatsApp, Snapchat, and Discord), and payment market (WhatsApp Pay, Apple Pay, Google Pay, and PayPal).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment