Studio_Dagdagaz/iStock via Getty Images

Mercer International (NASDAQ:MERC) is a combination of a manufacturer of a niche grade of wood pulp, a biofuel electricity generator, and a producer of lumber and structural cross-laminated building products. As a forest products stock, MERC fits well within a diversified basic materials sector portfolio, and very much with an international flair.

Pulp is a basic raw material used to manufacture paper. Pulp is made from decomposing the fibrous part of trees or recycled paper. Pulp made from trees is the most common source of fiber used in papermaking and the primary material for many paper and wood products. The physical properties of various grades of pulp impact the performance of the paper it is made into. For instance, there is usually a decrease in tensile strength, bursting strength, and density of recycled pulp vs the use of “virgin pulp”. Investors desiring a more in-depth description of the various types of pulp can review these excellent descriptions.

Mercer Int’l focuses on Northern Bleached Softwood Kraft (NBSK) pulp vs its cousin Northern Bleached Hardwood Kraft pulp. MERC is the 2nd largest global manufacturer of NBSK. The most important physical difference is softwood pulp offers more strength than hardwood due to the long- vs short-fiber nature of softwood trees vs hardwood trees. For example, the physical requirement of corrugated paper is substantially different than the physical requirements of toilet tissue. Corrugated can be made thicker to compensate for a lack of strength while tissue paper needs to be ultra-strong and flexible for its thickness. Due to its increased strength properties, NBSK is more suitable for fine papers, absorbent applications, and tissues than NBHK, which is better suited for corrugated and packaging paper.

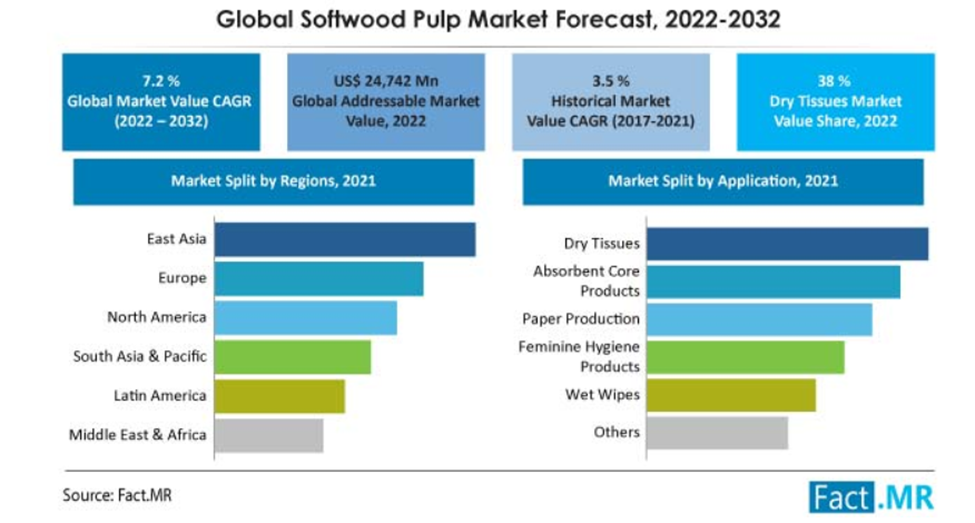

Overall, according to factmr.com, the demand for softwood pulp is expected to continue to expand over the next 10 years. The graphic below outlines a supportive market growth for NBSK in its main use as a major raw material for tissues.

Global Softwood Pulp Market (Fact.MR)

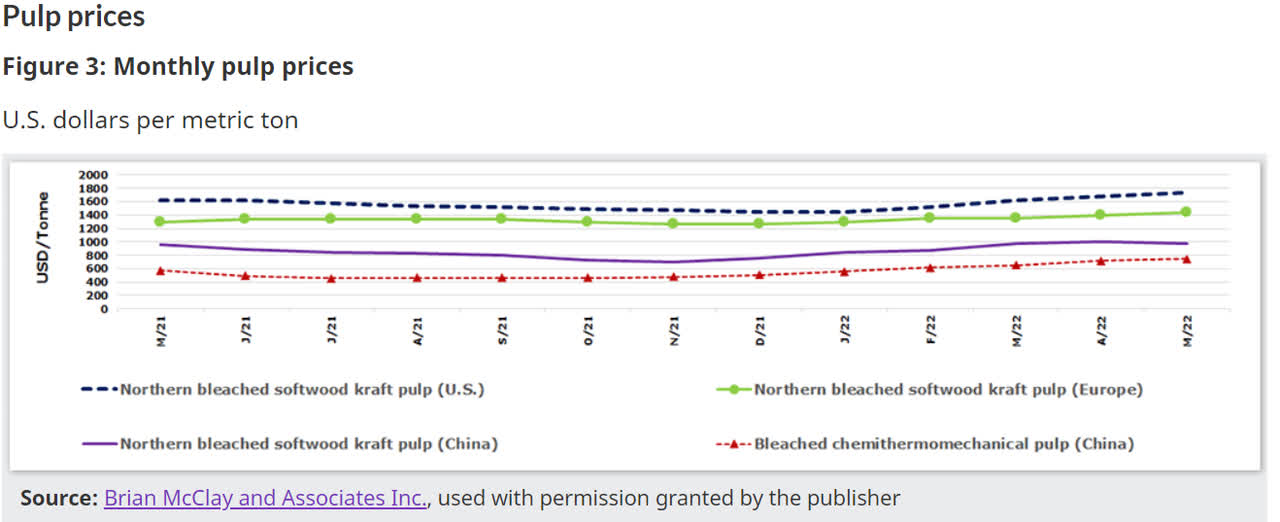

Mercer Int’l operates five virgin pulp facilities, three in Canada and two in Germany. Apart from the Canadian Peace River mill which can switch from NBSK to NBHK based on market conditions and short-term profitability, the majority of MERC production is NBSK. NBSK usually carries a 15% to 20% premium price over NBHK. Both grades are volatile and, like the commodity they are, are subject to the whims of supply and demand. The chart below from the Canadian Natural Resources Agency outlines the price of NBSK over the past 12 months. As shown, the price varies based on destination. For example, in May 2022, NBSK in the US was priced at $1,800 a metric ton while shipments destined for China were priced at $1,000. The major reason is the buying power of China as it represents about 30% of global demand for NBSK and upwards of 50% of the global consumption for all grades of papermaking pulp.

NBSK Pulp Price May 2021 to May 2022 (Canadian Natural Resources Agency)

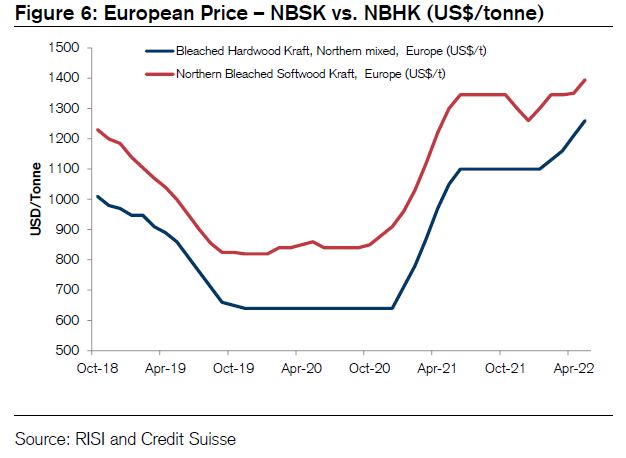

Credit Suisse offers the following chart of the historic price for NBSK and NBHK from Oct 2018 to present:

Pricing: NBSK vs NBHK Oct 2018 to April 2022 (Credit Suisse)

According to Mercer Int’l, most recent investor’s presentation, from a supply-side, management expects a large jump in capacity in 2023, but minor additions until post-2025. The spike in capacity in 2023 is expected to negatively affect pricing, and MERC’s profitability, for 2023 and 2024 as the capacity additions are absorbed into the marketplace.

In addition to NBSK pulp, Mercer Int’l generates electricity from its in-house biofuel created through the pulp-making process. MERC prioritizes its power generation first to its internal needs as pulp making is energy-intensive, with any excess power sold to third parties. When MERC began building power-generating facilities at their Canadian pulp plants around 2015, management estimated it reduced production costs by upwards of $40 a ton. It is not hard to imagine even more substantial savings today, as not all competitors are energy self-sufficient. Power generation is also a profit generator for MERC, with Credit Suisse estimating 2023 Power EBITDA of $120 million. With the current difficulties with energy in Germany, having excess electric power to sell is a strong attribute. MERC has an overall generating capacity companywide of 416 MW.

Mercer Int’l operates a lumber sawmill in Germany and a structural laminated beam facility in the US. MERC is the 5th largest producer of softwood lumber in North America and Europe. MERC recently purchased a cross-laminated timber (CLT) production facility from a company filing for bankruptcy. The use of CLT in construction is expected to grow by ~30% annually and MERC’s Spokane CLT facility currently represents about 1/3 of the North American production of CLT.

As a commodity producer, Mercer Int’l earnings per share are volatile. During the lockdowns of 2020, EPS was -$0.26 and rebounded to $2.58 in 2021. Currently, there seem to be tight market conditions for NBSK, which is supporting a higher market price and will contribute to higher earnings this year. However, the added 2023 NBSK capacity should pressure commodity prices and MERC’s profitability. According to marketscreener.com, the consensus of the 5 analysts offering EPS estimates is $3.44 in 2022, $1.93 in 2023, and $0.96 in 2024. Credit Suisse is more aggressive with a $3.96 estimate for this year.

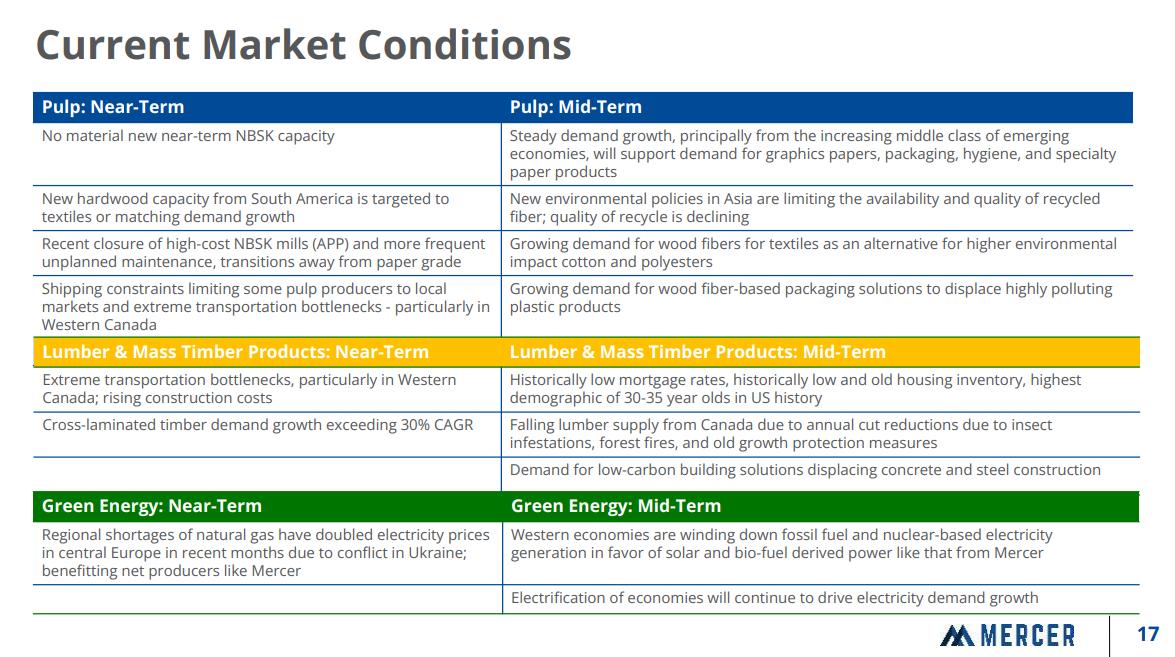

Management offers an interesting recap of market condition for its products. Found on page 17 of their latest presentation, management outlines what they see as near-term and medium-term outlook for their business conditions, and is very worthy of review.

Product Market Conditions Overview (Mercer Int’l May 2022 Presentation)

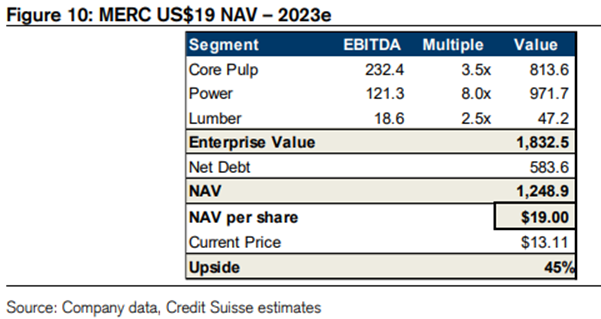

In a recent Mercer Int’l company review, Credit Suisse offers the following Sum-of the-Parts valuation, based on estimated 2023 EBITDA. This provides a great benchmark for establishing a stock price target.

Sum-of-the-Parts MERC Valuation (Credit Suisse)

I have been a shareholder since 2011, subsequent to studying the investments of billionaire investor Peter R. Kellogg and his Bermuda-based IAT Reinsurance Co., Ltd. According to secform4.com, Kellogg has recently been buying more shares. After a $2 million buying binge in Nov 2021 in the $10.35 to $10.50 range which followed a 3-year hiatus, Kellogg has made two purchases this year. In March, he purchased 11,000 shares at $12.75 to $13.00 range and just last month bought 63,000 shares, worth $972,000, at $14.90 to $15.95. It is reported Kellogg owns 23.264 million shares and IAT Reinsurance Co., Ltd owns 16.480 million shares, for combined control of over 54% of MERC outstanding stock.

Investors looking for more commodity exposure should spend some time with Mercer Int’l. MERC fits nicely in the portfolio investment bucket titled, “equities bought primarily for capital gains”. It looks undervalued at its current price, and I have placed a GTC order to buy more at $12.75 on any further dips. If I did not already have a long-term position, I would not be hesitant to start one at current valuations.

Be the first to comment