Anadolu Agency/Anadolu Agency via Getty Images![]()

Following the Chinese zero-COVID ‘U-turn’ in recent months, the Android smartphone value chain backdrop looks set for a timely reversal into restocking mode. Given its leading position within the China smartphone supply chain, fabless semiconductor company MediaTek (OTCPK:MDTKF) offers investors direct exposure to the near-term demand upside. The consensus bar also remains low – estimates still call for a revenue decline in FY23 despite the prospect of a demand boost from a Chinese recovery into H1 2023, as well as the Dimensity 9200 flagship launch, which boasts competitive specs and a higher price point.

That said, MediaTek will need to contend with some near-term margin pressure following TSMC’s (TSM) price hikes and ongoing R&D investments to capitalize on future growth opportunities across compute and autos, among others. The valuation helps, though. Even after the rebound over the last month, the stock trades at an undemanding ~11x fwd P/E and offers a well-covered ~10% dividend yield, so investors don’t need too much to go right to see upside from here. The upcoming Q4 earnings result next month presents a near-term upside catalyst.

A Pending China Demand Recovery Presents Upside to the Lowered Guidance Bar

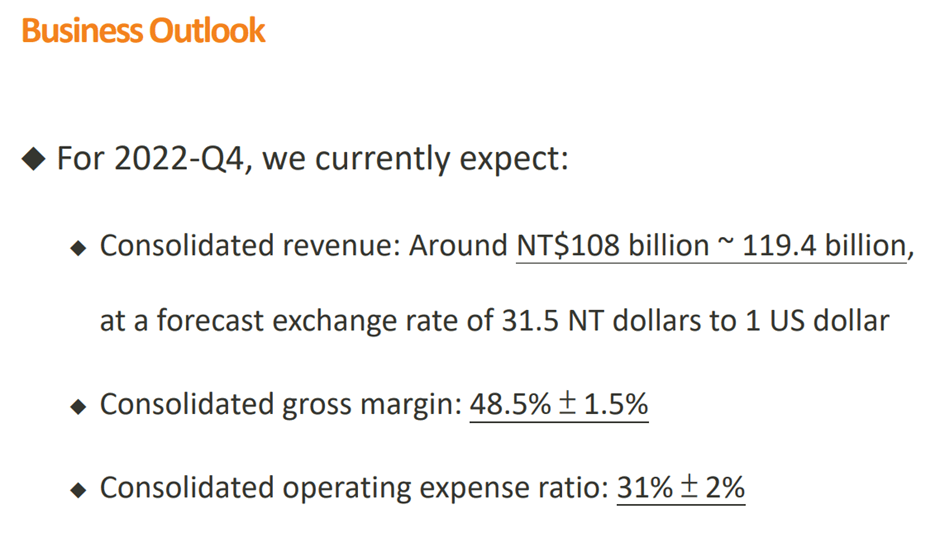

At its last earnings report, MediaTek had already guided for a weaker-than-expected Q4 2022 revenue result at 16-24% QoQ to factor in an inventory correction scenario. Similarly, gross margins were also guided slightly lower at 48.5%, likely in anticipation of 5G-related pricing pressure. While bears will contend that the margin guidance remains vulnerable to downward revisions in the face of higher foundry costs (due to the TSM hikes) and the pressured budgets at its customers, the recent China reopening is a game changer. Relative to prior market and supplier expectations for depressed China smartphone demand for FY23, the combination of improved mobility and further fiscal/monetary easing should drive a re-acceleration in growth. By extension, China smartphone shipments could recover sooner than anticipated (likely in H1 2023), and MediaTek is well-positioned to capitalize.

MediaTek

Any demand recovery could surprise to the upside, in my view, as inventory needs to be restocked in line with the step change in demand expectations post-reopening. Given China is served to a large extent by the Android smartphone ecosystem, players across the supply chain, including MediaTek, stand to benefit in the coming quarters. Plus, we are heading into a busy period of new model launches (Samsung Unpacked 2023 is scheduled for Feb 1st), which could add to the demand upswing.

The path forward for margins won’t be straightforward, though – SoC (system-on-chip) competition among Android brands is tough, with MediaTek likely to face further pricing pressure from the likes of Qualcomm (QCOM), which has a more established brand. In turn, MediaTek’s investments in future growth will drive R&D spending higher as it looks to stay ahead of the development curve and tap into key end markets like computing, autos, and ASICs going forward. That said, the company has levers available to support margins, including via bonus accruals and by passing on any input cost inflationary pressures over time (likely in a phased approach, given its comparatively lower pricing power vs. QCOM).

Competitiveness of Dimensity 9200 Bodes Well for Flagship Adoption

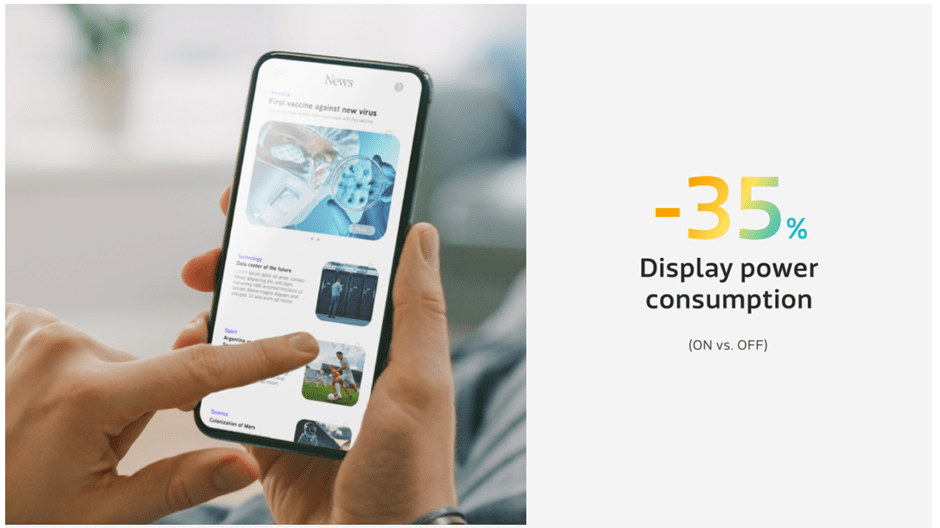

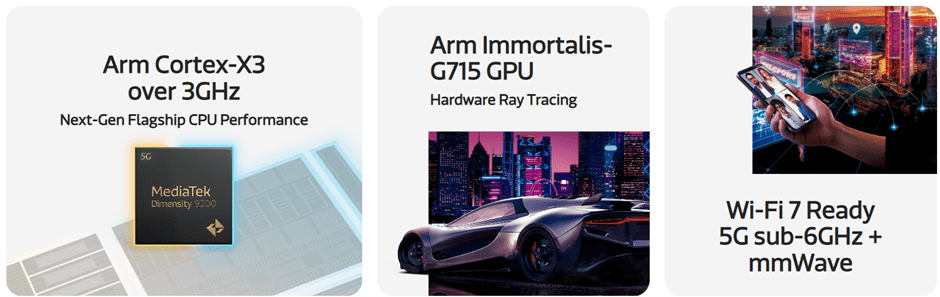

The launch of MediaTek’s latest flagship 5G SoC, Dimensity 9200, is a key statement of intent as it looks to move up the value chain. Based on the latest 4nm process from TSM, the chip is competitive in specs against best-in-class flagship processors such as QCOM’s Snapdragon and the Apple (AAPL) A16 Bionic – an impressive feat given its prior track record is focused on mid-range and entry-level SoCs. Key highlights are on the GPU (Arm Immortalis-G715 GPU with hardware ray tracing) and power consumption (up to 35% panel power savings).

MediaTek

Perhaps most importantly, at this stage of China’s 5G adoption curve, the Dimensity 9200 also supports sub-6GHz and mmWave 5G technologies, a key improvement over the prior Dimensity 9000 (only sub-6GHz support). While the 5G capabilities aren’t a major consideration currently, given the slower mmWave deployment in China, the post-COVID reopening will likely accelerate the shift. And in the meantime, MediaTek’s inroads with the Dimensity 9200 could pave the way for increased penetration into US/EU markets.

MediaTek

Thus far, traction has been encouraging – key customers like Vivo, Oppo, and Xiaomi (OTCPK:XIACF) have indicated an interest in adopting the Dimensity 9200 for their upcoming flagship models. Building on its competitiveness (note this is MediaTek’s first year of entry at the flagship smartphone level) and consistent execution on the flagship product roadmap, expect more market penetration into FY23/24 as well. With Dimensity 9200 also going for a much higher price point, growth here should prove accretive to the overall revenue base. Beyond the Dimensity 9200, upcoming SoC design pipeline launches, such as the N3E processor (subject to production costs at TSM), will be worth monitoring in FY23 alongside ongoing flagship share gains.

A Reasonably Priced China Reopening Beneficiary

The MediaTek setup looks compelling heading into next month’s earnings report. With the Chinese economy reopening, the company is well-positioned to capitalize on a new smartphone restocking cycle in the region, given its China-focused client base. In line with this view and the competitiveness of the Dimensity 9200 flagship, MediaTek should see revenue growth outpace expectations for an FY23 decline. Margin expectations also remain low, though some weakness is justified following pressure from TSM’s latest price hike and ongoing investment needs. Still, the stock offers good value at a very reasonable ~11x fwd earnings (~8x P/E ex-cash) and an attractive high-single-digit to double-digit % dividend yield for long-term investors willing to wait.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment