MAXSHOT

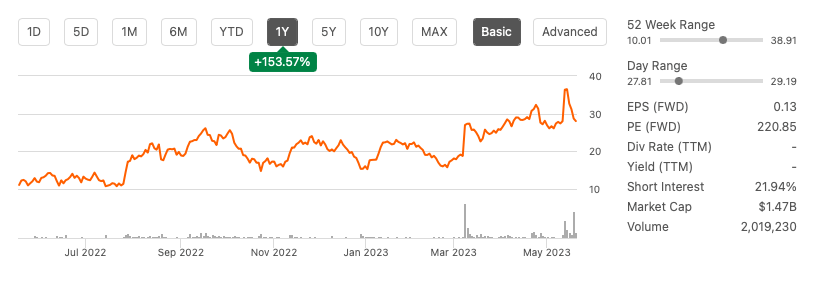

Maxeon Solar Technologies, Ltd. (NASDAQ:MAXN) has been an exciting stock to follow over the last year concerning its growing fundamentals and performance on the stock market. Although the stock has dropped since the company’s public offering of 7.5 million shares announcement, the stock price has rewarded investors with an incredible 153.57% in returns in one year.

One-year stock trend (seekingalpha.com)

Maxeon Solar has proven its ability to improve its profit margins quarter after quarter, its new US sales channel brings in significant upside growth potential, and the US utility-scale side of the business is already booked through 2025. Furthermore, Maxeon is raising capital, assisted by large affiliate TotalEnergies (TTE), to increase its manufacturing capacity. Although cautious of the high short-interest, negative free cash flow, and the stock’s historical volatility, I remain bullish as the company solidifies its space in the solar energy market.

Company Updates

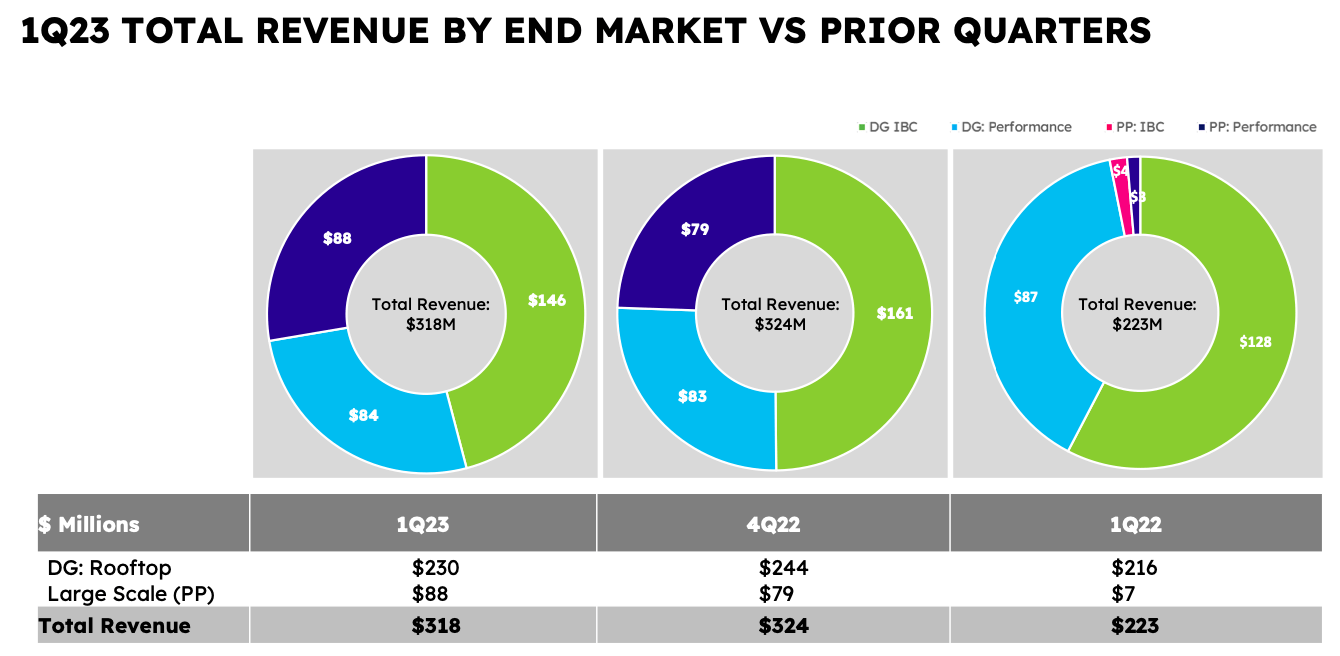

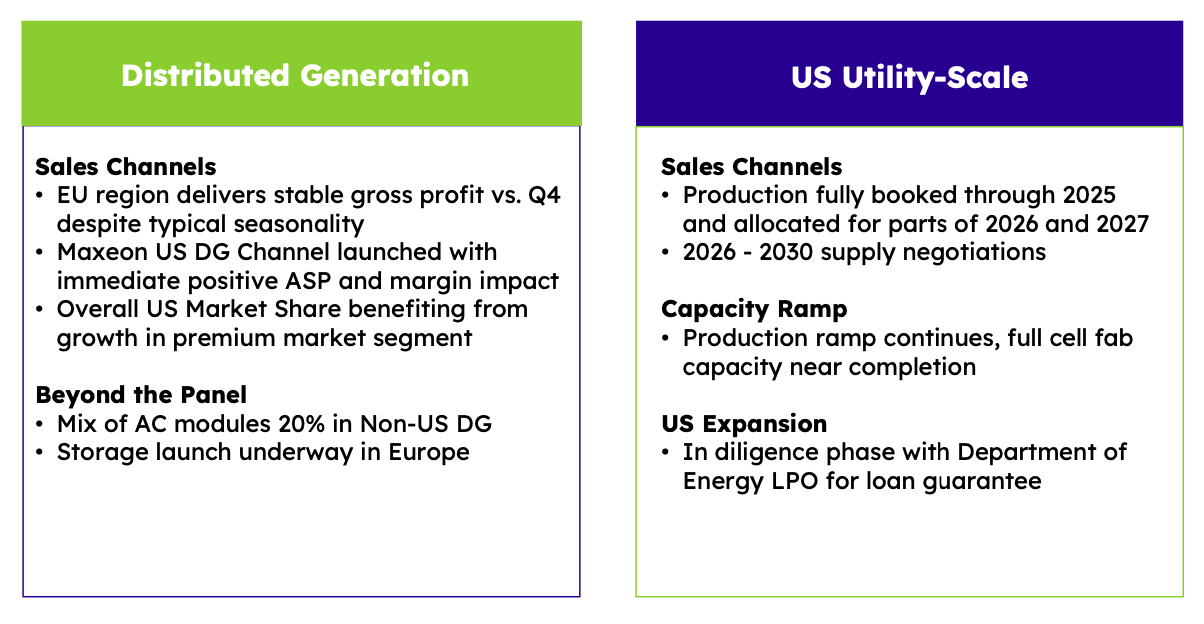

Maxeon Solar generates revenue through two segments, distributed generation (DG) and utility-scale. In my first article, I go into greater detail about the business. One of the important company updates is that Maxeon, in addition to its exclusive supply agreement for Maxeon 6 panels until 2025 to SunPower (SPWR), its previous parent company, has been able to launch its own Maxeon residential sales channel. This allows for a much greater market opportunity and improved profit margins. Secondly, US utility-scale (PP) production is already booked for 2025, and the company is progressing on its capacity expansion plans in the US. We can see that in Q1 2023, top-line growth has increased YoY across end markets.

Q1 2023 vs Q1 2022 (Investor Presentation 2023)

Fundamentals are improving, but the company also has concrete growth plans, assisted by a recent public offering of 7.5 million shares. Maxeon is investing in its capacity to manufacture Maxeon 7 products through its public offering; 1.8 million shares are through affiliate company TotalEnergies. The aim is to raise $200 million. We can see future growth through increased capacity, new sales channels increasing its market share, and a growing premium market segment demand.

Business segments (Investor Presentation 2023)

There are several industry tailwinds the company could benefit from; firstly, we are seeing a normalisation of pre-pandemic shipping and polyester prices. This is likely to continue to improve Maxeon’s operational margins. Another resource impacting manufacturing costs is the price of silicon, which has begun to drop with the return of the China market manufacturers ramping up production. All these factors have already started positively impacting companies across the solar industry. Furthermore, the company could benefit from the Biden administration’s new clean energy tax guidance of 10% if they increase their component production in the US facilities.

Q1 2023 Highlights

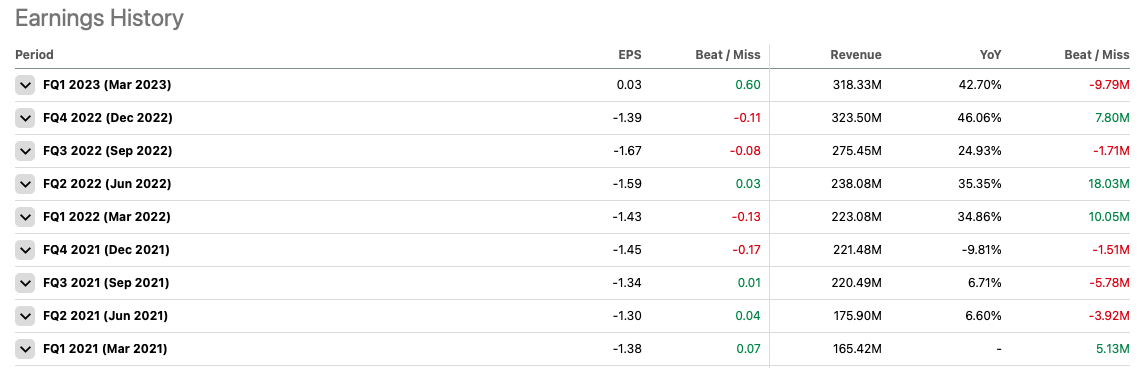

Maxeon Solar released its Q1 2023 earnings one week prior and beat EPS expectations by $0.60 to reach $0.03. This is the first positive EPS in nine quarters.

Earnings history per quarter (seekingalpha.com)

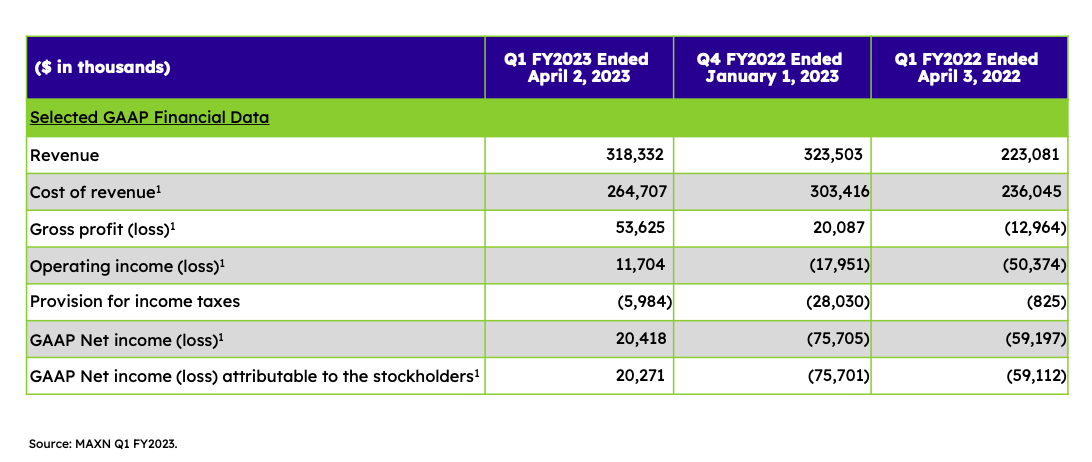

Revenue grew 42.7% to $318.33 million. We can see that over the last year, the company went from a negative gross profit of $12.96 million in Q1 2022 to a positive gross profit of $53.625 million. Furthermore, the company reported a positive net income of $20.418 million compared to consecutive quarters of negative income.

Income overview Q1 2023 versus Q1 2022 (Investor Presentation)

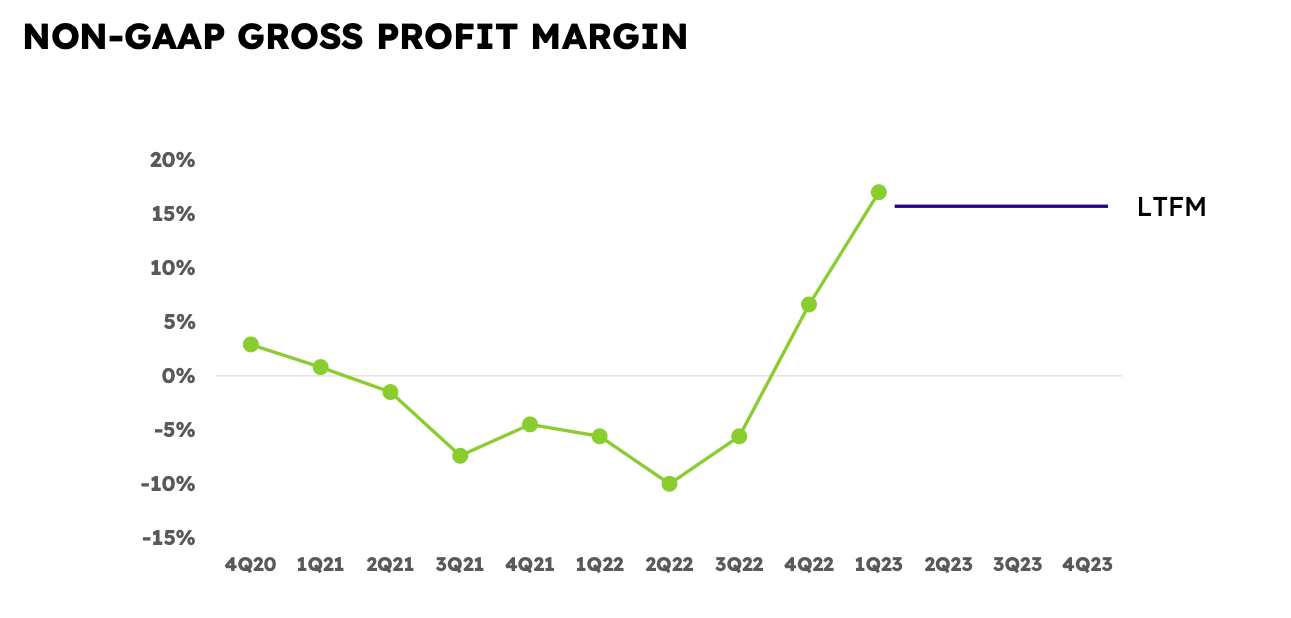

Maxeon has been criticized in the past for its poor gross profit margins. We have seen improvements over the last four quarters, reaching 17%, the highest since it became its own company.

Gross margin by quarter (Investor Presentation 2023)

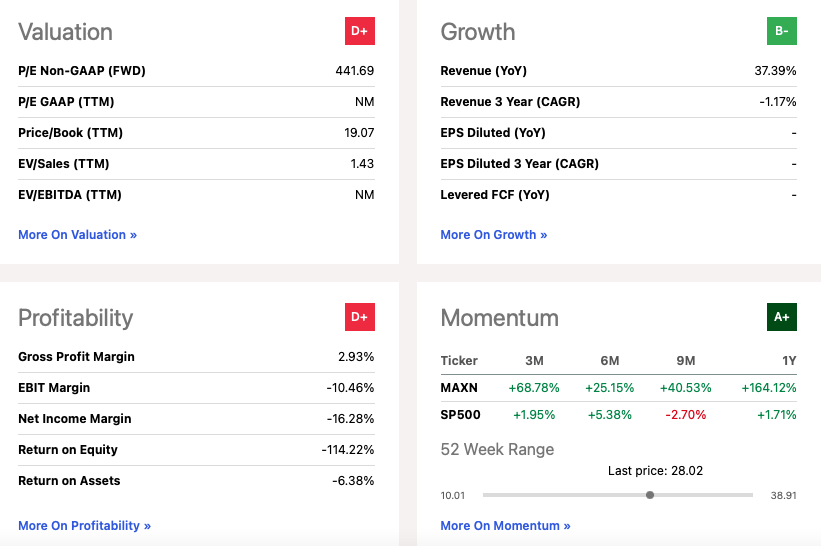

Since its spinoff, the company has not had positive net cash flow. Levered free cash flow at the end of Q1 2023 was negative $11.94 million TTM. If we look at the balance sheet, we can see that total cash was $278.85 million, and total debt was $456.96 million with a current ratio of 1.30 but a low quick ratio of 0.58, meaning that the business is not sufficiently liquid if it were to have to pay its short term liabilities.

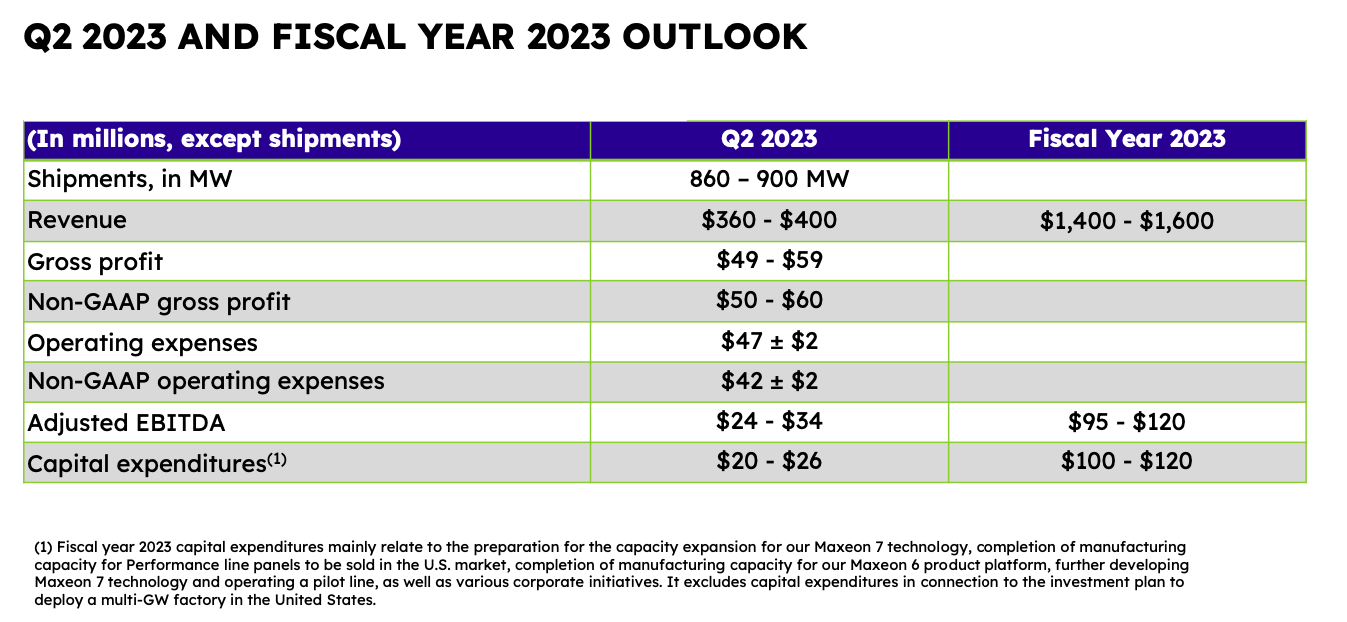

Management has a positive outlook for its Q2 2023 and FY 2023; it predicts revenue of between $360 and $400 million, gross profit between $50 and $60 million, adjusted EBITDA of between $24 and $34 million, and capital expenditures between $20 and $26 million. Its 2023 revenue outlook ranges between $1.4 billion and $1.6 billion, with adjusted EBITDA between $95 and $120 million.

Q2 2023 and FY 2023 Forecast (Investor Presentation 2023)

Valuation

The stock has received noteworthy attention after a strong Q1 2023 earnings report and clear growth momentum across its businesses.

Analyst recommendations after earnings Q1 2023 (marketscreener.com)

It is currently trading below its one-year target estimate of $34.50. The stock price dropped after the company announced its efforts to raise capital through a public offering of 7.2 million shares. Although unfavourable in the short term for investors, this is still an improvement from the previous dilution, which brought the stock down to $18 per share. The stock has outperformed the S&P 500 every quarter, with growth in the double digits at 37.39%. While this company is clearly in a growth phase, we expect the profitability and margin to improve, with a prediction of between $95 and $125 million for FY2023.

Quant Rating (seekingalpha.com)

Risks

Solar stocks tend to fluctuate according to macroeconomic factors; investors should know that these stocks can be rewarded generously. However, the stock price can steeply fall based on political, environmental or regulatory changes. As tensions between China and USA trade continue, additional costs and potential solar tax benefits could be negatively influenced due to the company’s presence in the China market, which could hurt the business in the long run. Furthermore, there is a high short interest in the company at 21.94% indicating that investors are pessimistic about the future.

Final Thoughts

Maxeon Solar is proving itself quarter after quarter concerning solid performances across its businesses. It has long-term growth potential through its new US Maxeon sales channel, it is investing in growing its capacity to meet rising demand, and it is showing clear signs of delivering a solid financial year with parts of its business already booked into 2025. Therefore, I remain bullish on this stock.

Be the first to comment