Tony Anderson

Summary

Following my coverage of Masco (NYSE:MAS), I recommended a hold rating as I awaited the 3Q23 results to see if MAS was on track with my bull case expectations. This post is to provide an update on my thoughts on the business and stock. I am not turning bullish on the stock, as 3Q23 supported my previous viewpoint on the business. I am recommending a buy rating for MAS, but with a small position size as there is still uncertainty in the macro environment.

Investment thesis

MAS’s adjusted EPS of $1 in 3Q23 was higher than the consensus estimate of $0.91. Despite a 10% drop in revenue growth, the company managed to beat expectations thanks to an increase in adjusted EBIT margin of 124 basis points. MAS’s performance in the third quarter of FY23 was exceptional, in my opinion, and this has increased my optimism about the company. To me, MAS’s pricing strategies and ongoing raw material cost deflation have supported margin performance. The most notable takeaway in 3Q23 was the accelerated decline in prices, both for commodities and shipping costs generally, which bodes well for the quarters ahead.

One significant area of emphasis for the current quarter, in my perspective, pertains to the PRO paint segment. This particular segment has demonstrated greater resilience compared to the DIY segment, primarily due to the market share gains achieved by MAS in the distribution channel. The volumes experienced a decrease in the low single digits as the backlogs returned to normal levels following the peak caused by the pandemic. It is my expectation that the segment will experience a resurgence in positive growth, as there are indications that the management’s long-term strategy, specifically the partnership with Home Depot, is yielding favorable outcomes. The evidence is in the pudding, as the 3-year growth stack in PRO is up more than 60%, and on a 2-year stack basis, comp is over 30%. The fact that management still sees plenty of growth opportunities to invest in PRO, such as increasing delivery options and enhancing loyalty programs, was a crucial comment that reassured investors at this growth moment, in my opinion. However, it should be noted that MAS may encounter certain challenges in the short term regarding its pricing strategy. In the third quarter of 2023, MAS experienced a slight decrease in the prices of paint inputs, falling within the low-single-digit range. The management anticipates a comparable rate of deflation in paint inputs for the fourth quarter of 2023. Deflation will continue to help MAS save money on raw materials in 2024, but the trend toward cheaper pricing will be a minor headwind. Promotions, however, have been fairly constant. With pricing being pressured given deflation in raw materials, profitability might be impacted in the near term. However, it is important to acknowledge that there is still a possibility of margin growth, as the management has been actively investing in the segment to enhance productivity. These investments should help to cushion any negative margin impacts.

“We are also planning an increased investment in people and capabilities in 2023 to drive future growth in our PRO paint business to have a greater impact in the coming quarters.” 1Q23 earnings call

The next focus is on the performance of plumbing. In general, the outcome of this segment in the third quarter of 2023 does not come as a surprise to me. Although there was a decline in demand in Europe and China when compared to previous periods, it is encouraging to note that there are initial indications of stabilization. Importantly, MAS is showcasing its robust ability to influence pricing through a series of moderate and focused pricing initiatives throughout the current year. It is crucial to acknowledge that MAS is demonstrating its ability to influence pricing, despite the current weakness in housing turnover that I would expect to have a negative impact on repair-and-remodel expenditure. Furthermore, it is worth noting that during the RBC Capital Markets Global Industrials Conference of 2021, the management explicitly stated their ability to maintain price stability once it has been implemented. Which means that MAS’s margins should grow as these external pressures abate. Moreover, management highlighted that freight, zinc, and copper have all moved off their recent peaks, which I anticipate will take a few months before it shows up in the P&L, suggesting MAS should benefit from favorable margins well into 2024. In fact, I expect margins to grow even further in FY24 if MAS decides to raise prices once again.

Oftentimes, we will hold on the price once it’s in the marketplace. So we generally don’t see significant rollback in pricing in the plumbing segment as compared to what we might see in the Decorative Architectural segment. 2021 RBC conference

Regarding guidance, management reiterated its revenue outlook for FY23, anticipating a decline of 10%. However, there has been a slight adjustment in the outlook for the Plumbing segment, which is now expected to experience a decline of 9-10%, as opposed to the previously projected range of 10-12%. The anticipated trend is for a decrease in volumes by a significant percentage in the low double-digits, which will be partially mitigated by a slight increase in pricing in the low single-digits. However, the management has increased its projected operating margin guidance for the year 2023 by 50 basis points to approximately 16.5%. This indicates that the margin improvements observed in the third quarter of 2023 are expected to persist throughout the fourth quarter of the same year. Overall, I perceive this quarter to be favorable for MAS. The long-term strategy for PRO paint has shown progress, and the company has successfully established its market position by raising prices for plumbing services, even in the current economic climate, and maintaining those price levels going forward.

Valuation

In my previous DCF model, my assumption was that, assuming consumer sentiment and housing-related end markets recover from their recent lows, I believe MAS will see improved performance in the second half of the year and beyond. Deflation in the cost of raw materials and shipping has somewhat neutralized the effect of falling unit sales, and the pricing strategies put in place over the past two years continue to hold. I believe the 3Q23 has provided data to support my previous assumptions, especially in the aspect of pricing strategies that will stay in effect moving forward, and that margin improvement should continue to support mid-single-digit FCF growth.

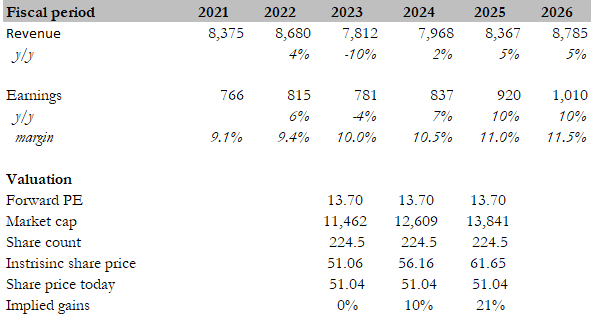

Own calculation

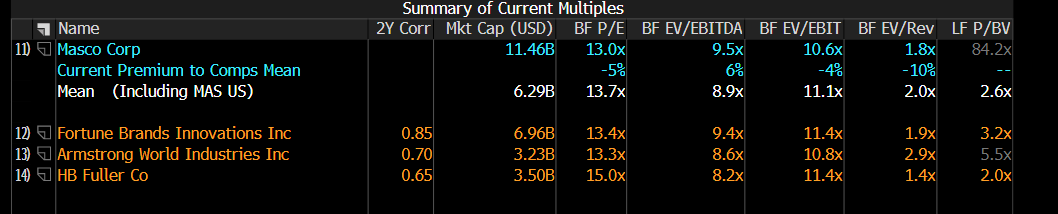

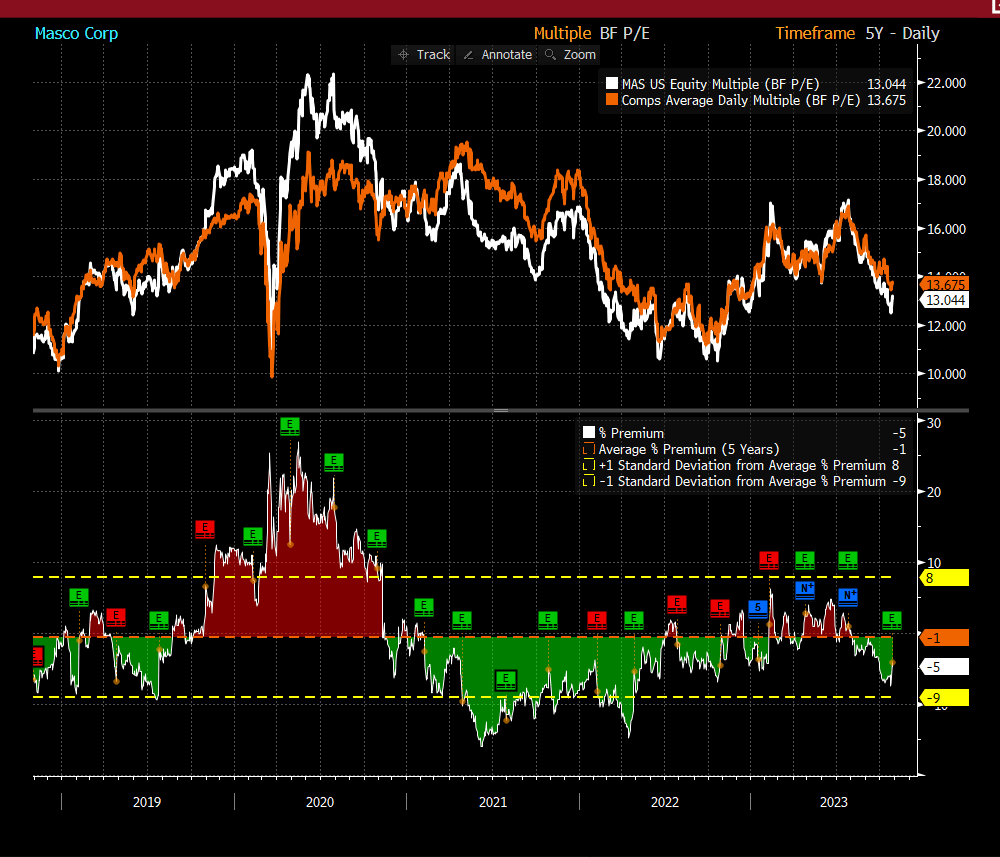

However, to better illustrate the near-term return dynamics, I have switched my model structure to a relative valuation method, focusing on FY24–FY26 performance. My model shows three price targets, ranging from the very near-term (FY23) to the mid-term (FY25). In the near term, before revenue growth recovery and margin expansion at a greater scale, the stock is roughly fairly valued. As we progress through FY26, the upside gets larger as MAS grows in line with peers and the margin expands. Breaking down the model, FY23 follows management revenue guidance, which I expect to be highly accurate as we are already three quarters into the year, and my expectations for margin to improve. FY24 should be a recovery year for MAS as the macro situation starts to turn better and it continues to raise prices. Top-line growth, coupled with deflationary cost movements and productivity gains, should continue to support margin expansion. MAS has historically traded in line with peers, and I do not see this dynamic changing in the future given my expectation that MAS growth should gradually recover from here to mid-single-digit percentage growth, which is in line with peers expected growth profile.

Bloomberg Bloomberg

Risk

The big risk with investing today is that the macroeconomic situation is not completely cleared off the books yet. While MAS has showcased its ability to hold on to price increases and its ability to raise prices even in the current climate, volume growth could be significantly impacted by a weaker macro environment. In that case, the higher price point might be a detrimental factor as consumers trade down to cheaper alternatives.

Conclusion

I am upgrading my rating for MAS to a buy, driven by the positive performance in 3Q23. Despite the slight challenges posed by deflation in raw material costs and pricing pressures, MAS’s strategic pricing initiatives and ongoing cost deflation are expected to continue supporting margins. The plumbing segment also shows resilience and the ability to influence pricing positively, despite some external pressures. In terms of valuation, my model suggests that MAS is fairly valued in the near term but holds upside potential as it recovers from the macroeconomic challenges and continues its growth trajectory in line with peers. However, the lingering macroeconomic uncertainty remains a key risk, potentially impacting volume growth and consumer behavior. While the pricing strategies have proven effective, any prolonged economic weakness could lead to trade-down behavior among consumers.

Be the first to comment