Evening Standard/Hulton Archive via Getty Images

Investment thesis

Our current investment thesis is:

- Marks and Spencer Group plc (OTCQX:MAKSF) (“M&S”) is a large UK retailer that managed to marginally grow despite competition struggles due to its large UK footprint. This looks unlikely to be challenged, although growth beyond low single digits looks unlikely.

- Near-term issues with inflation are likely to reduce margins, which M&S may not be able to recover.

- Scope for outperformance will come from overseas, improvement in apparel, Ocado sales, and improving online presence.

- M&S is trading in line with its historical average, reflecting no material change in fortunes.

Company description

Marks and Spencer Group plc is a retail company that operates various retail stores. The company is divided into five segments: UK Clothing & Home, UK Food, International, Ocado, and All Other.

As well as its core retailing and groceries services, the company offers financial services, renewable energy services, and real estate investments. The company also operates international franchises and provides its products online.

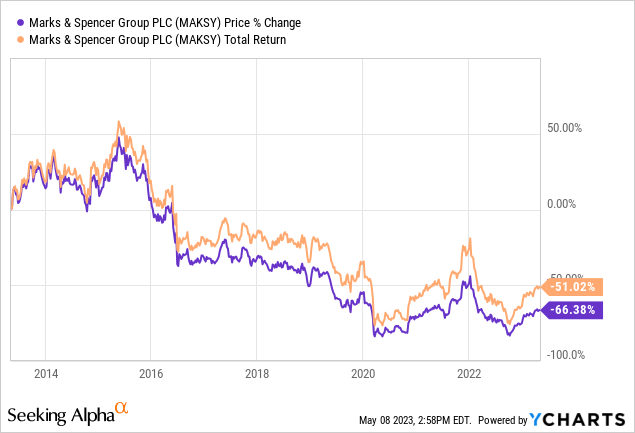

Share price

M&S’ share price has declined in the last decade, with dividends unable to reduce the slide. M&S is a high-end retailer in the UK, facing slowing growth as the younger generation favor other retailers who are more in tune with changing trends. This has left M&S facing a difficult long-term outlook, as its customer base ages.

Financial analysis

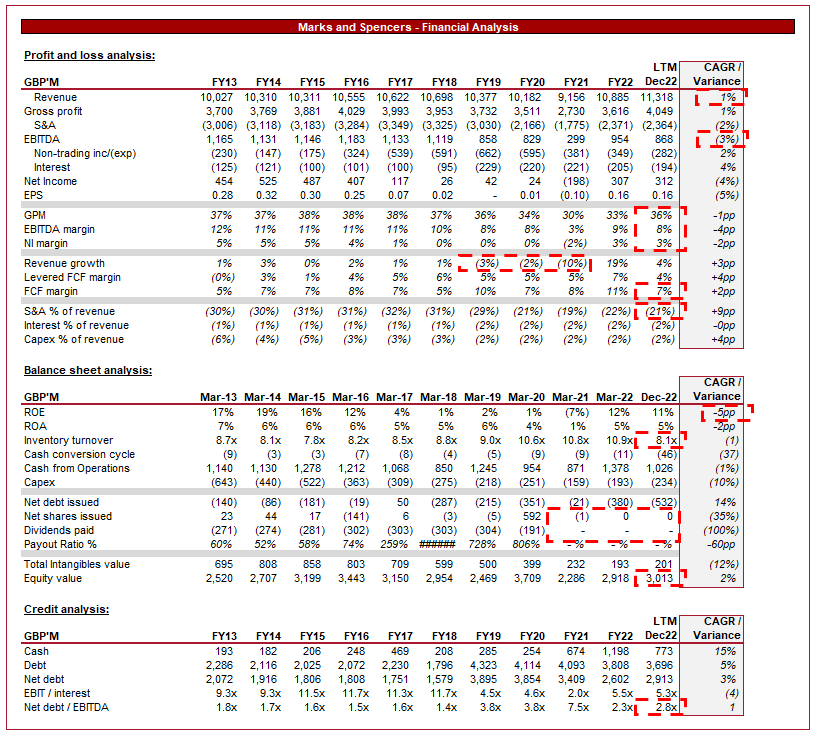

M&S Financial analysis (Tikr Terminal)

Presented above is M&S’ financial performance for the last decade.

Revenue

M&S’ revenue growth has been incredibly mild, with a 1% CAGR in the last 10 years. During this period, the company experienced 2 years of negative growth and no single year with revenue growth in excess of 5% (excl. Covid-19 impacted years).

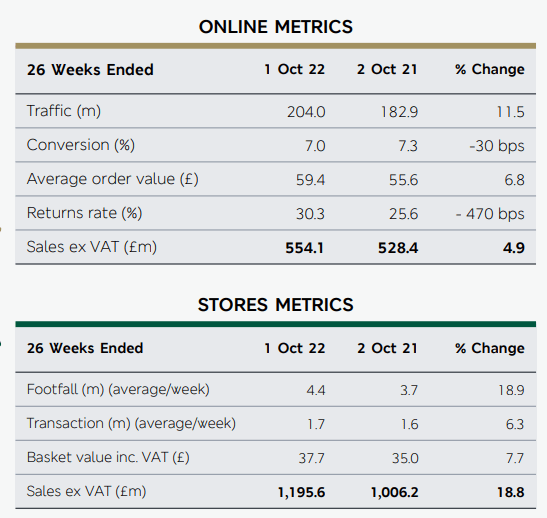

The growth of e-commerce has transformed the retail and groceries industry, with online shopping becoming increasingly popular among consumers. This has been driven by an improvement in the digital experience, alongside convenience and flexibility for consumers relative to in-store purchasing. M&S has been slow to adopt an e-commerce strategy, which has affected its ability to compete with other retailers. E-commerce retailers can price aggressively relative to brick-and-mortar businesses, as they lack the fixed overheads and headcount component of operations. The company has been rapidly expanding its digital operations but this is only acting to retain customers rather than as a means of growing the company. As the following data illustrates, M&S’ online sales continue to grow and are now 32% of total sales on a 26W basis.

Online/instore (M&S)

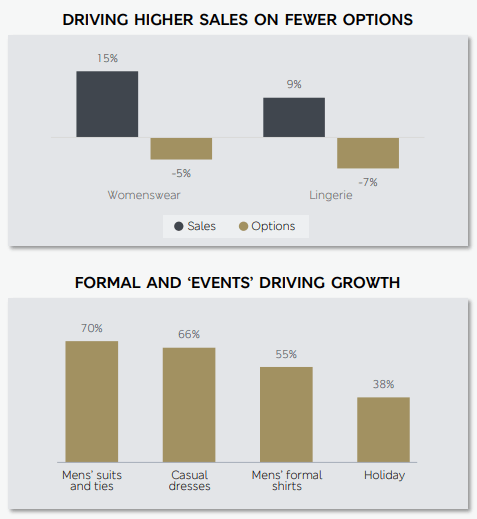

A shift in consumer shopping habits has had a significant impact on M&S. In the last decade, we have seen the rise of fast fashion, as well as social media-led marketing. Many “new school” retailers have exploded into prominence, powered by e-commerce. M&S, like many large corporates, has been slow to react and has seen many of its customers transition across to competitors, while also losing out on potential customers as the younger generation is uninterested. M&S is not cool and lacks any real cultural relevance. The company’s strategy to improve this is reducing the number of products and focusing on design and its key areas of expertise, such as formalwear and lingerie.

Retail change (M&S)

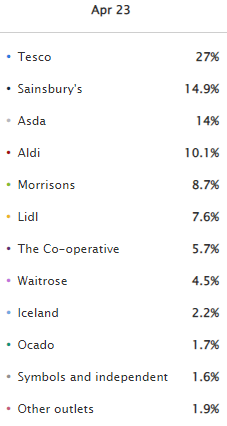

The groceries industry in the UK is highly competitive. In the mass market segment, we have the “Big 4”, J Sainsbury (OTCQX:JSNSF), Tesco (OTCPK:TSCDF), Asda, and Morrisons. In the disruptor/affordable segment, there is Aldi, Lidl, Iceland, and Co-op. Finally, in the premium segment, we have M&S, Waitrose, and Ocado (OTCPK:OCDGF). According to Statista, Market share breaks down as follows (Note M&S has not been included within this):

Market share UK (Statista)

Readers may question why we are presenting several segments in the market, as the expectation would be that M&S is not competing with them, but this is not the case. In the last decade, we have seen a rapid downward trend in spending by consumers, with discount brands growing rapidly and gaining market share. This is best illustrated by Aldi, which entered the UK 90 years after Morrisons and has recently broken into the Big 4. We have seen M&S and Waitrose losing pace to the traditional Big 4, as they lose out to the affordable brands. There is no single reason for this, but a general improvement in quality at the bottom end and difficulty to justify a premium at the top end is a major reason for this. Supermarket-branded products are far better relative to branded products now than they were 20 years ago.

The UK’s decision to leave the EU has had a significant impact on retail dynamics, with greater uncertainty around trade deals and tariffs. M&S has numerous European businesses, in many cases exporting products from the UK. This said, the overseas business continues to outperform the UK, representing a resilient opportunity for growth. This issue is that thus far, these regions represent a relatively small part of the company’s operations, and so a long runway of growth is required in order for it to move the needle.

Overseas (M&S)

M&S and Ocado Group became the joint owners of Ocado Retail in Aug19, with an equal 50:50 share in the venture. This allows Ocado to stock M&S products and rapidly accelerates M&S’ entry into the delivery business. Over the last decade, the business has reduced its physical locations as a means of controlling costs, and so this Ocado deal is a strong (although much delayed) response to maintaining its national presence.

The operations are not generating the desired profits yet, but our view is that this is a long-term play to improve M&S’ reach.

Ocado x M&S (M&S)

Economic considerations

Current economic conditions represent a near-term headwind for the business. UK inflation remains in excess of 10%, with interest rates continually being increased as a means of bringing it under control. This is squeezing consumers’ finances and leading to reducing spending where possible. As a premium in the market, M&S looks susceptible to a slowdown as consumers trade down. This said, the company has been able to increase prices, which is why sales growth remains healthy, but this is at the cost of volume.

Margin

M&S’ margins have trended down in the last decade, which is why its EBITDA has declined at a 3% rate despite the revenue growth. This is a reflection of heightened competition in the last decade, forcing the business to reduce prices as a means of maintaining customers and sales.

In the most recent quarter, margins continue to decline as the company has been unable to price / reduce costs sufficiently to offset the impact. M&S did acquire a part of its supply chain through Gist, which should allow the business to realize cost benefits while improving its control.

Costs (M&S)

H1 results

H1 results (M&S)

Presented above is M&S’ most recent quarterly results.

As mentioned prior, the ability to increase prices has allowed the business to improve sales, with H1 looking very impressive. The issue is that margins are declining despite the pricing impact. As we have seen in the historical period, the company has been unable to win back its margins following a decline, so it is critical to assess where the company will normalize.

Balance sheet

M&S currently has a ND/EBITDA ratio of 2.8x, which in our view is the top end of what the business can manage. A large amount of this relates to property leases and so we are not concerned, although it likely means continued deleveraging in the coming years.

Management has ceased to distribute cash since FY21, although we suspect this may be reinitiated in the coming 12-24 months.

Outlook

Outlook (Tikr Terminal)

Presented above is Wall Street’s consensus view on the coming 5 years.

Analysts are expected M&S to grow at a CAGR of 3%, with a slight decline in margins. This looks to be a reasonable assessment, although we believe margin dilution may be higher.

Valuation

Valuation (Tikr Terminal)

M&S is currently trading at 7x its LTM EBITDA and 6x its NTM EBITDA. This is in line with its historical trading range, reflecting the poor sentiment around the business. The argument becomes whether the business justifies a premium to its historical average or potentially a discount.

Based on our analysis, we struggle to see any strong argument in either direction. In some cases, we see scope for commercial improvement, such as through the Ocado deal and improving its apparel offering, but on the opposing side, margins are contracting and the near term looks difficult.

Final thoughts

M&S has experienced a steady decline in the last decade, despite the minuscule growth, as competition and changing industry dynamics have reduced its competitive positioning. This shift has now slowed and leaves M&S behind many of its new competitors, although the company is looking to now push on and improve.

We still have little hope for any material turnaround and suspect the business will continue on its current trajectory. At its current valuation, the business looks fairly valued.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment