JamesBrey/E+ via Getty Images

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on April 13th.

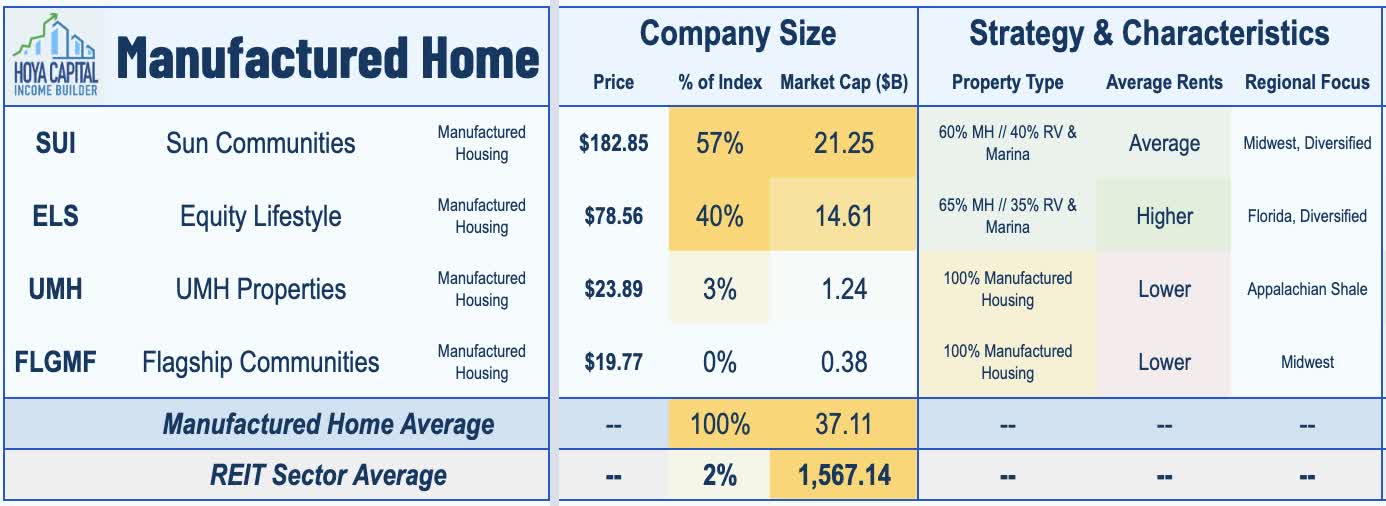

REIT Rankings: Manufactured Housing

Hoya Capital

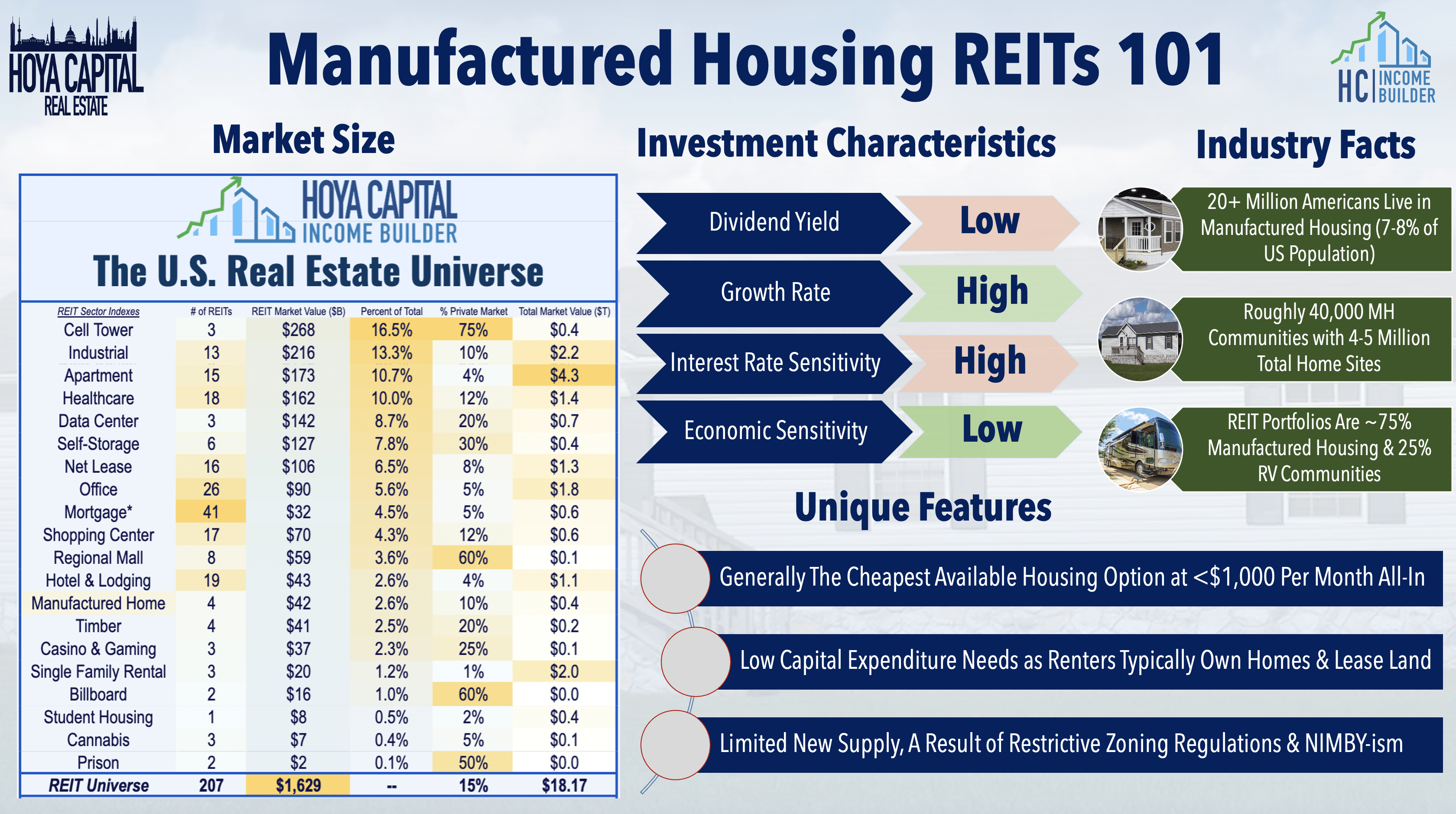

Manufactured Housing REITs have emerged over the past decade from relative obscurity into several of the largest and most well-run publicly-traded property owners in the world. Within the Hoya Capital Manufactured Housing Index, we track the three U.S.-listed MH REITs, which account for roughly $40B in market value: Equity LifeStyle (ELS), Sun Communities (NYSE:SUI), UMH Properties (UMH). We also track small-cap Flagship Communities (OTCPK:FLGMF), which trades on the Toronto Stock exchange.

Hoya Capital

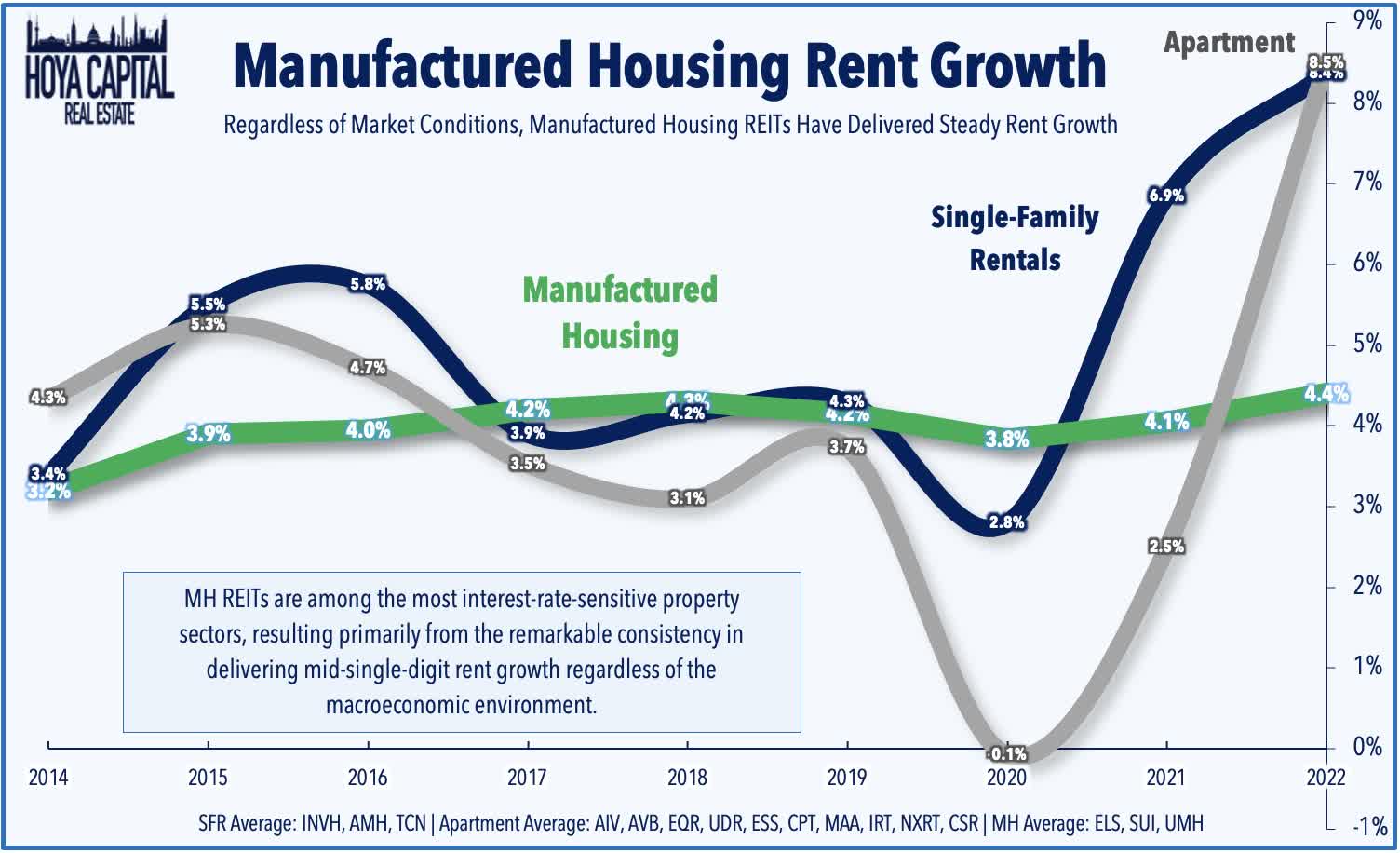

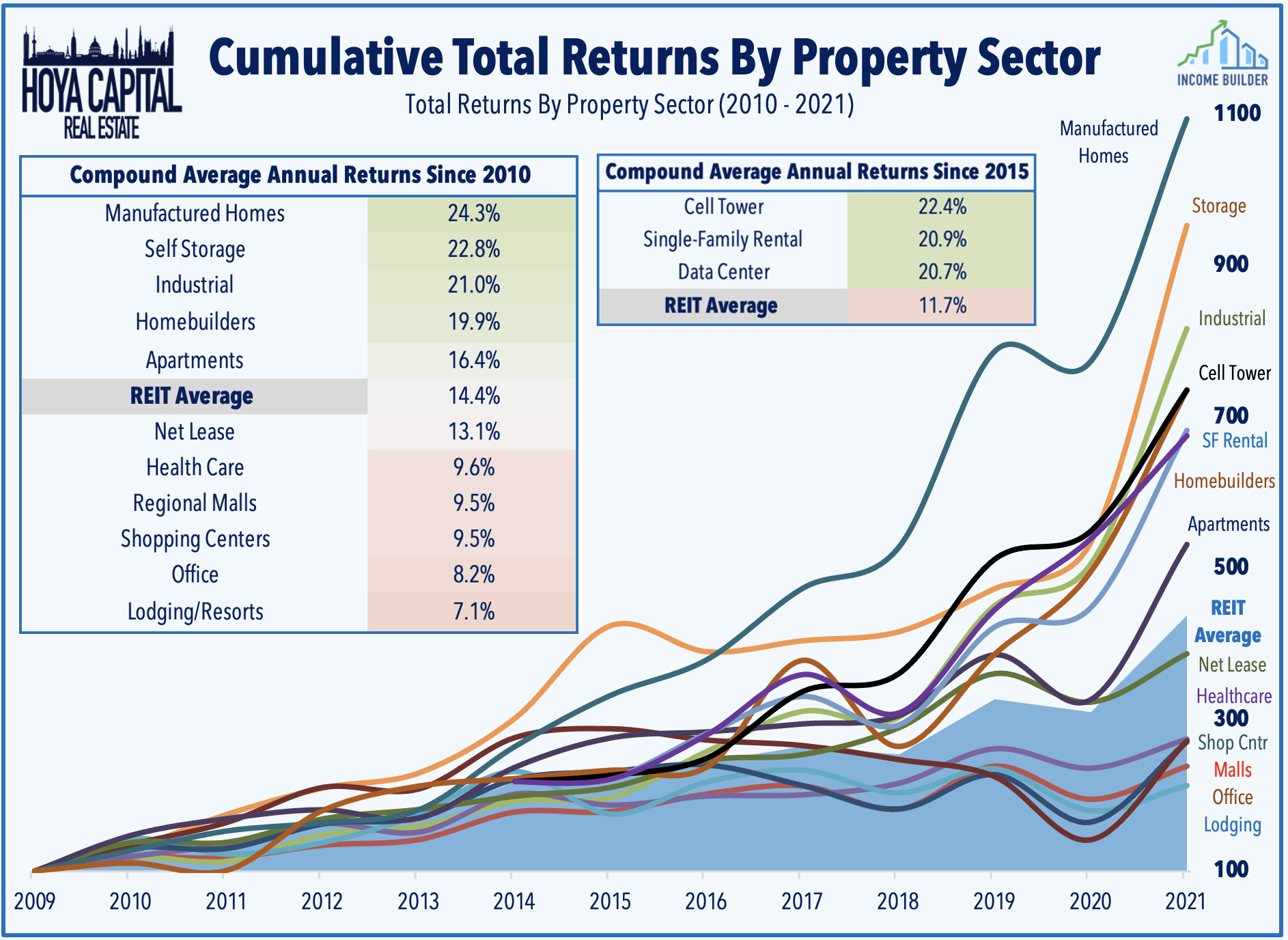

Beneficiaries of the intensifying affordable housing shortage across the United States resulting from a decade of underbuilding, manufactured housing REITs have been the single-best performing REIT sector since the start of 2010 with average annual total returns of nearly 25%, but have uncharacteristically lagged in early 2022. Counterintuitively, despite these double-digit annual returns, MH REITs are among the most interest-rate-sensitive property sectors, resulting primarily from the remarkable consistency in delivering mid-single-digit rent growth regardless of the macroeconomic environment.

Hoya Capital

Symptomatic of the lingering housing shortage in the United States, rents are soaring at the fastest pace on record in essentially every segment of the residential rental market across the country, but for MH REITs, the record-high set in 2021 at roughly 4.5% is only modestly above the historical averages. Apartment and single-family rental markets, meanwhile, are seeing far faster rent growth as Zillow (Z) data has shown double-digit rent increases across nearly every major market since mid-2021, momentum that has continued into early 2022. Zumper reported this week that the pace of rent increases in 2022 is actually outpacing 2021’s record-high year of rent growth.

Hoya Capital

While MH renters are unlikely to see double-digit rent hikes in the foreseeable future, we do expect rent growth to meaningfully accelerate and significantly exceed analyst forecasts. As the most affordable housing option with a significant share of renters in retirement age and receiving social security income or other inflation-linked transfers, rent growth tends to track broader inflation rates – and thus Cost-of-Living Adjustments – which have been substantial over the past twelve months. Social Security benefits received a 5.9% cost-of-living adjustment for 2022, the highest increase in about 40 years and could increase further in 2023 as the measure used for the COLA is currently higher by about 9% through the first quarter of 2022.

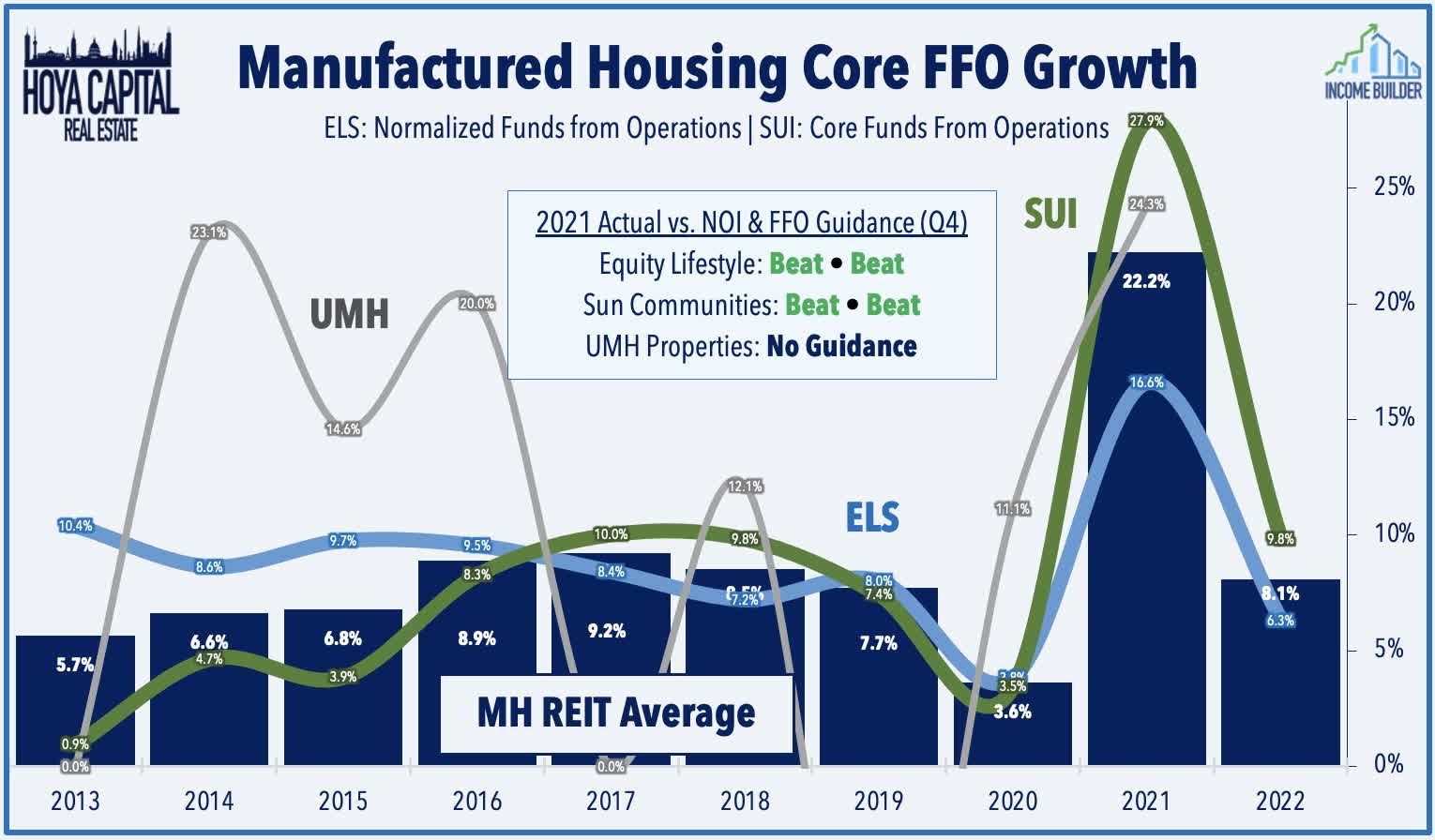

Growth in funds from operations (“FFO”) – the earnings per share “equivalent” for REITs – is driven by the combination of same-store “organic” growth and by external growth through acquisitions and new development. Manufactured housing REITs delivered incredible FFO growth of 22% in 2021, which was significantly above their earlier estimates and was the strongest year of FFO growth on record for all three of these REITs. The initial outlook for 2022 calls for average FFO growth of 8.1%, but we expect that accelerating rent growth will drive another year of at least 12-15% FFO growth.

Manufactured Housing Fundamentals

Earlier this year, Harvard University’s JCHS published its annual “State of the Nation’s Housing.” Researchers noted that “the supply of existing homes for sale has never been tighter,” as soaring home prices and rents have been fueled by “the combination of robust demand and limited supply.” JCHS concluded that “the pandemic is partially to blame for such tight conditions, but the biggest reason behind the constraints on supply is the underproduction of new homes since the mid-2000s.” The report noted that “supply constraints are nearly universal,” but particularly in the affordable housing segments. A separate report by the NAR estimated that the underproduction of new housing units relative to household formation totals 6.8 million units.

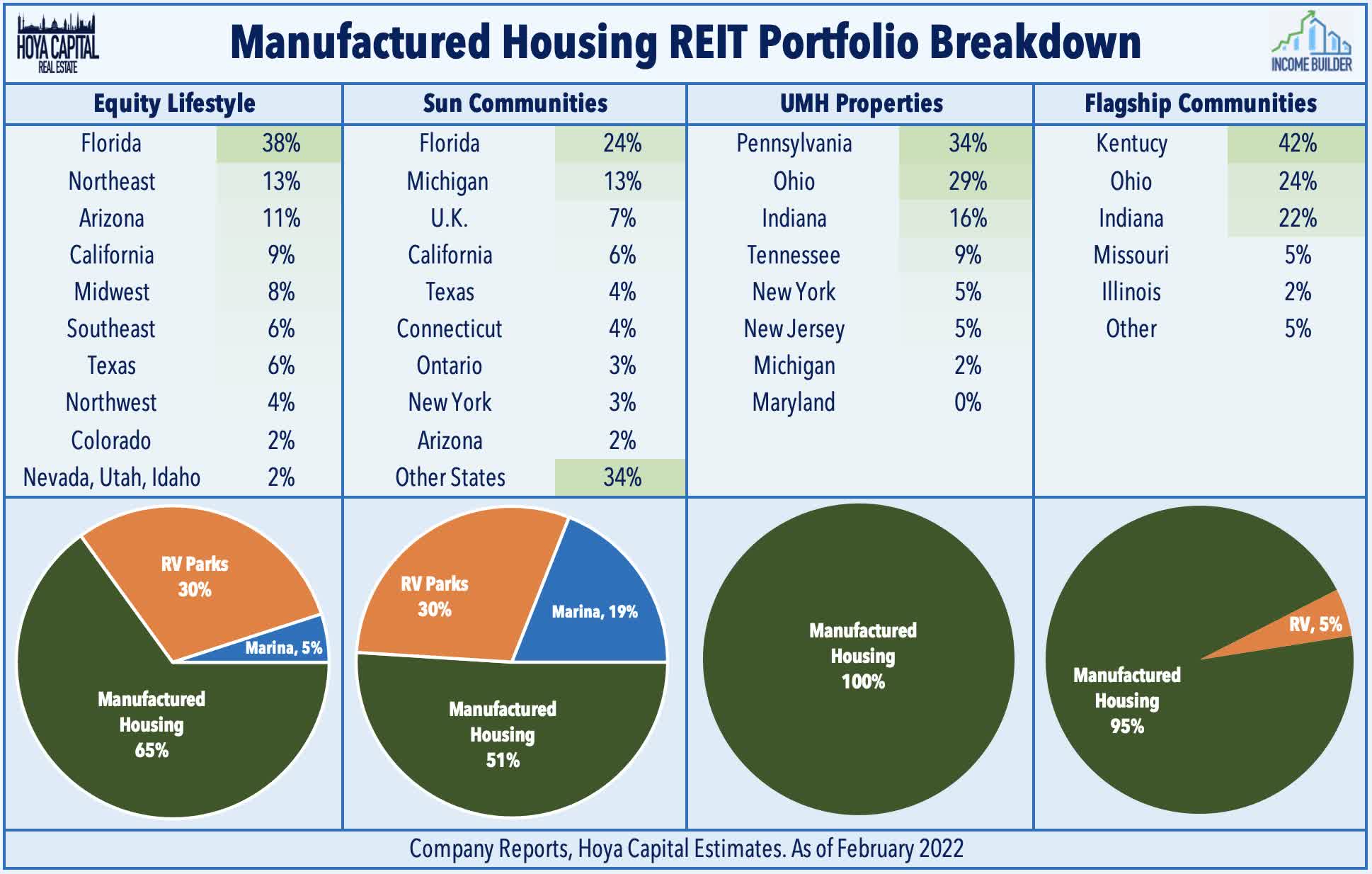

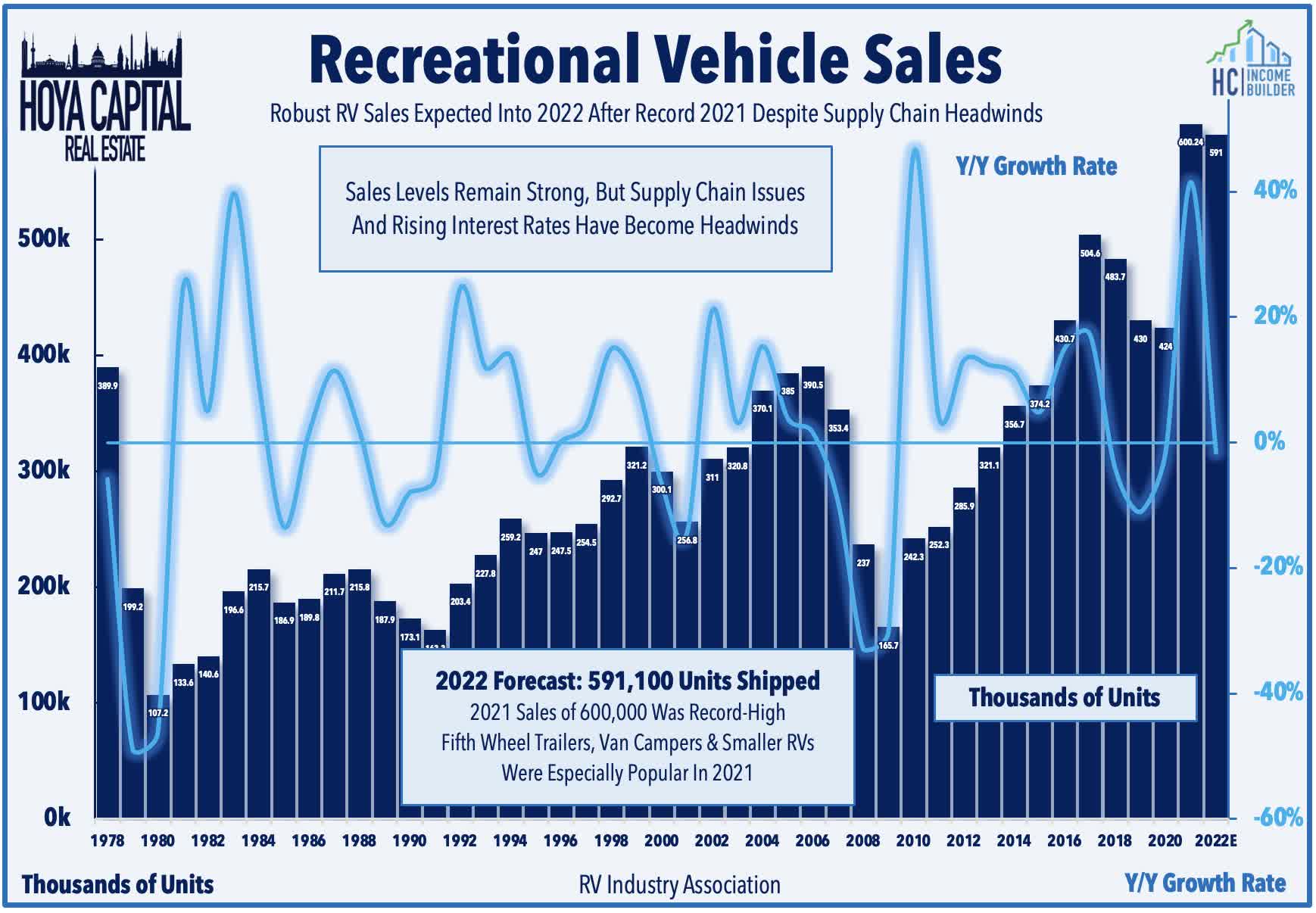

As noted in the JCHS report, “Work-From-Anywhere” has led to an uptick in not only traditional exurban housing demand like MH communities, but perhaps more significantly, it has powered a surge in demand for recreational vehicles (“RV”) and boat sales. MH REITs’ amplified focus on these analogous asset classes – RV parks and marinas – was perfectly-timed ahead of the coronavirus pandemic, providing an added external growth tailwind. RV parks now comprise roughly a third of assets for ELS and SUI, while marinas comprise 5% and 19%, respectively. UMH and newly-listed Flagship focus exclusively on traditional manufactured housing communities.

MH REITs have historically been one of the most interest-rate-sensitive REIT sectors – a function of their historically counter-cyclical fundamentals and the remarkable consistency in delivering mid-single-digit rent growth regardless of the macroeconomic environment. The diversification into RV parks and boat marinas – which have a more economically sensitive demand and cash flow profile – have provided a pro-cyclical counterbalance that should neutralize some of the potential headwinds from rising rates and inflation. The RV Industry Association reported that RV sales set record-highs in 2021 despite facing similar supply chain issues as traditional homebuilders, demand that helped power a 6% rise in “same-community” RV rents in 2021.

Hoya Capital

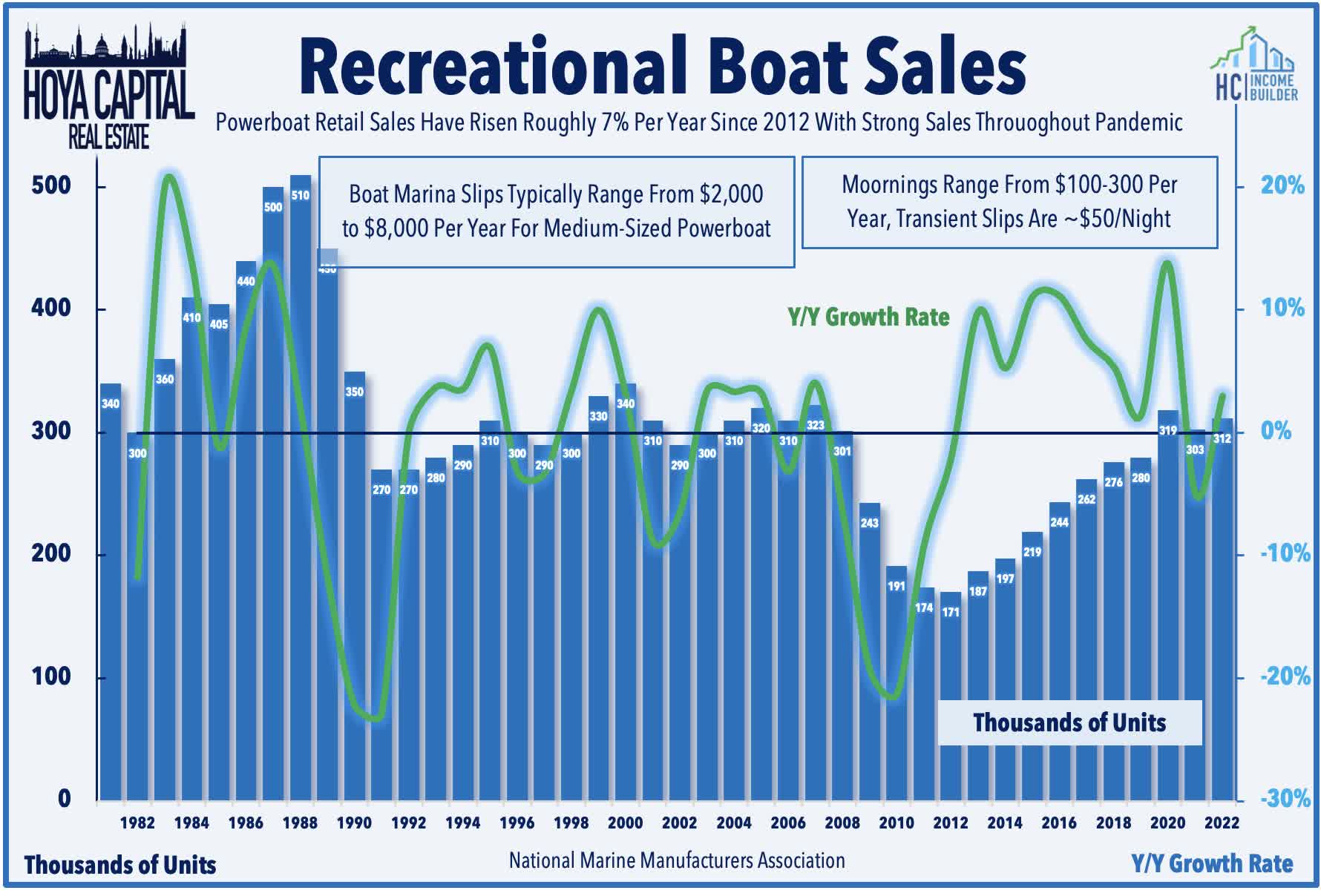

Recreational boat sales have also accelerated significantly during the pandemic despite ultra-lean inventory levels. The recreational boating industry – which includes MarineMax (HZO), Malibu Boats (MBUU), MasterCraft Boat (MCFT), and Brunswick Corporation (BC) – have significantly outpaced the broader equity market since the start of 2020. With SUI’s major investment in Safe Harbor Marinas, these MH REITs are now the two largest owners of marinas in the country. Institutional-quality marinas – of which there are roughly 500 across the U.S. – offer substantial operating parallels to the company’s RV business. ELS now owns 23 marinas comprising 6,800 slips while SUI owns 41,275 slips across 114 marinas.

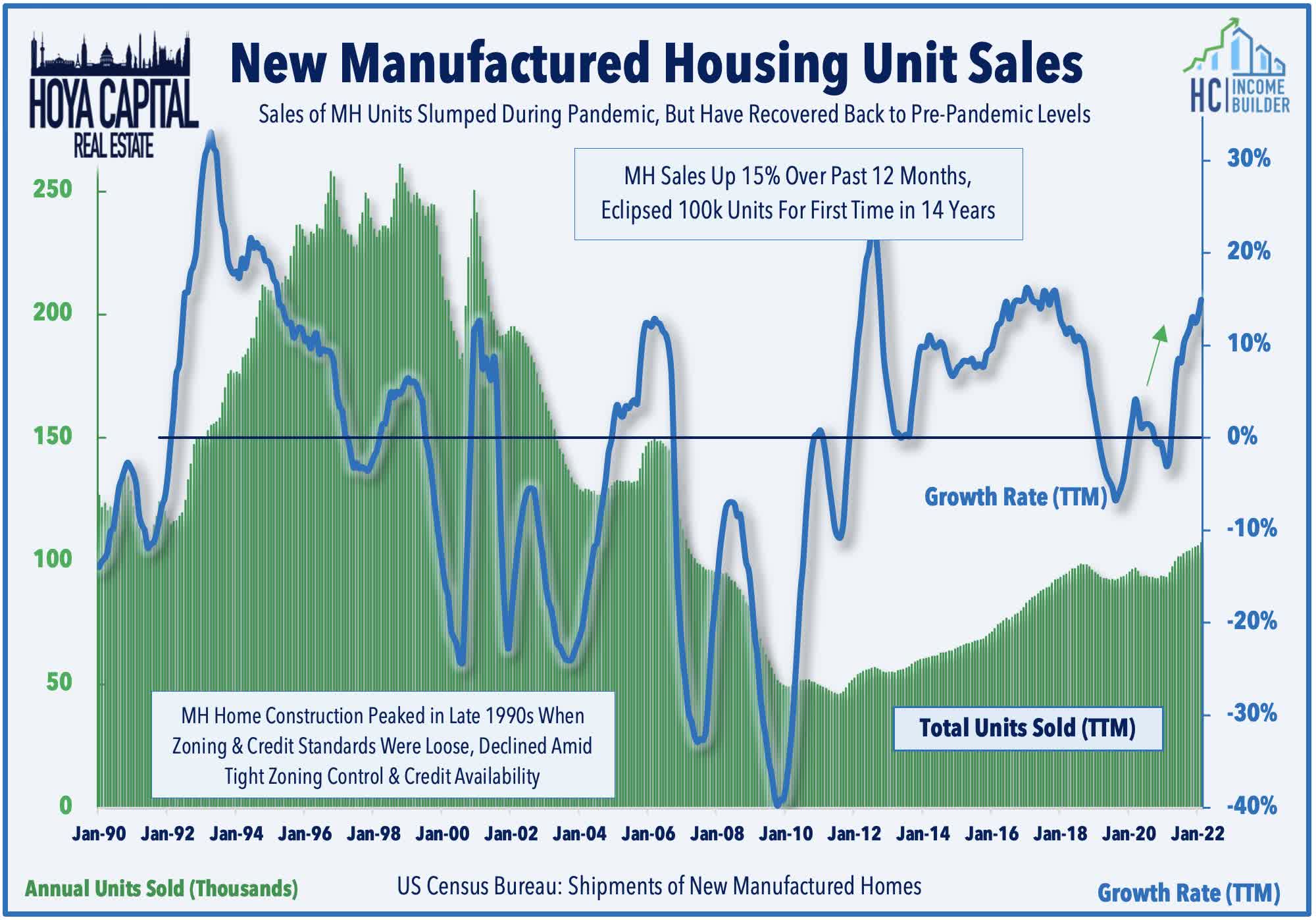

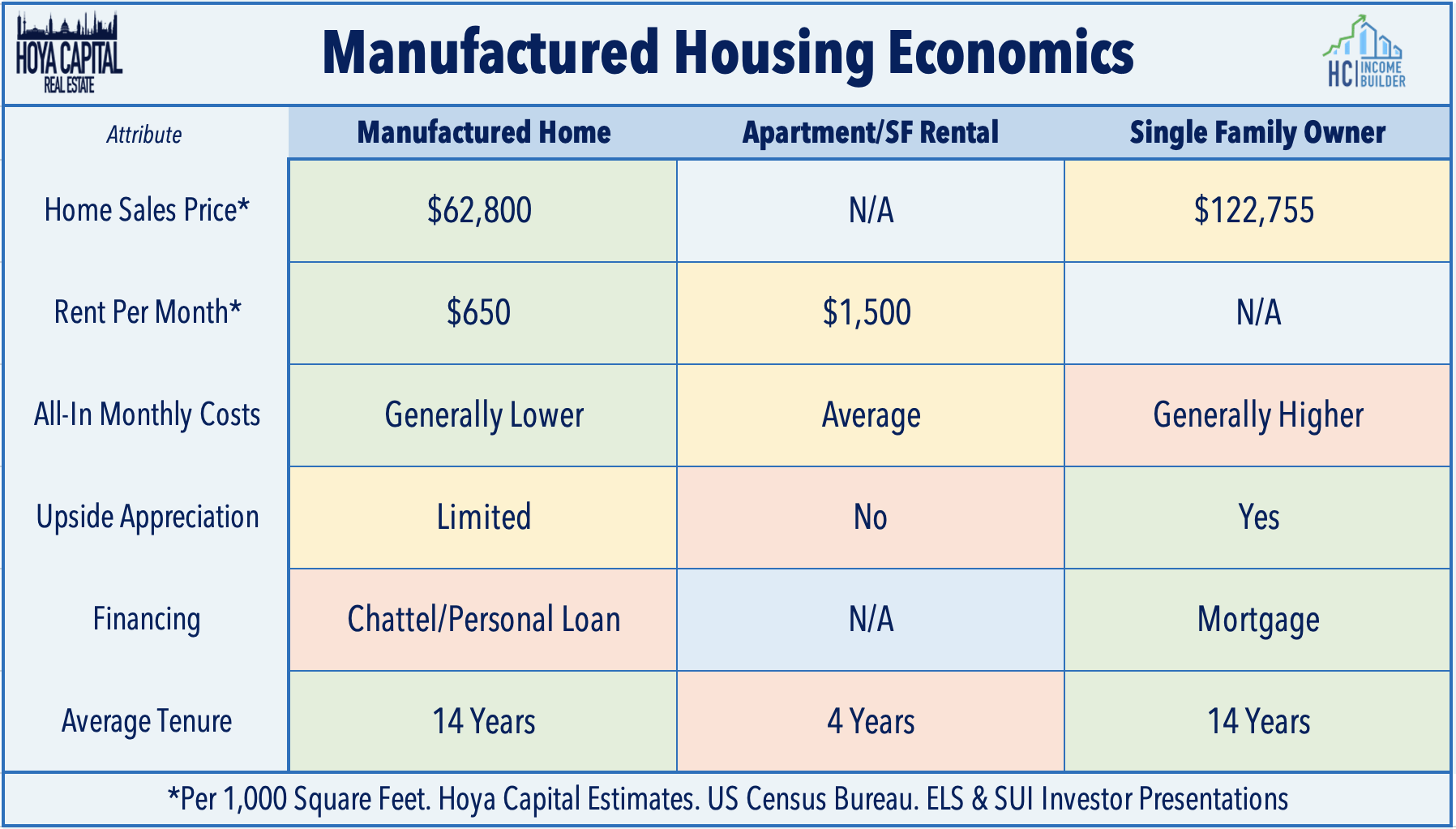

Sales of new manufactured housing units have also exhibited a strong acceleration over the last year, eclipsing 100k units in a twelve-month period for the first time in 14 years, driven largely by site expansions of existing MH REIT parks. MH sales peaked in the late 1990s when zoning and credit standards were loose, but declined sharply beginning in the early 2000s during the pre-GFC housing boom as demand shifted to site-built homes. MH units are typically the most affordable non-subsidized housing option in most markets and the manufactured housing resident base is incredibly “sticky”, as the average MH owner stays in a community for 14 years, far higher than the 3-5 year average for other rental units.

MH REIT Stock Price Performance

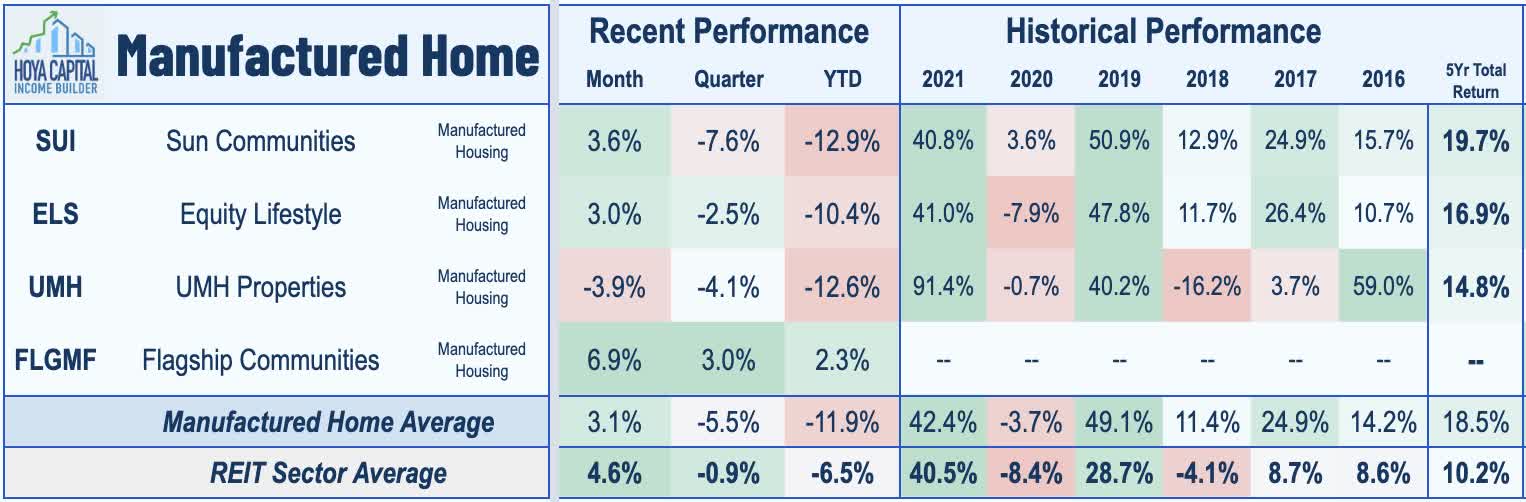

MH REITs edged out the Equity REIT Index in 2021 with total returns of 42% to push their incredible streak of nine straight years of outperformance. Pressured by rising interest rates and the growth-to-value rotation within the REIT sector, however, MH REITs have uncharacteristically underperformed in early 2022. Hoya Capital Manufactured Housing REIT Index is lower by 11.9%, lagging the 6.5% decline from the market-cap-weighted Vanguard Real Estate ETF (VNQ) and the 7.7% decline from the S&P 500 (SPY).

All three MH REITs have recorded similar declines in 2022 ranging between 10-13%. Consistent with the “reopening theme” across the REIT sector, small-cap UMH – which had lagged its two larger peers over the last decade – has led the way since the start of 2021 after boosting its dividend for the first time since 2008 last year. Still a relative unknown to many generalist investors, SUI – our largest position – is by many measures the GOAT (“Greatest of All Time”) of the REIT sector, delivering the strongest total returns of any REIT since 2005.

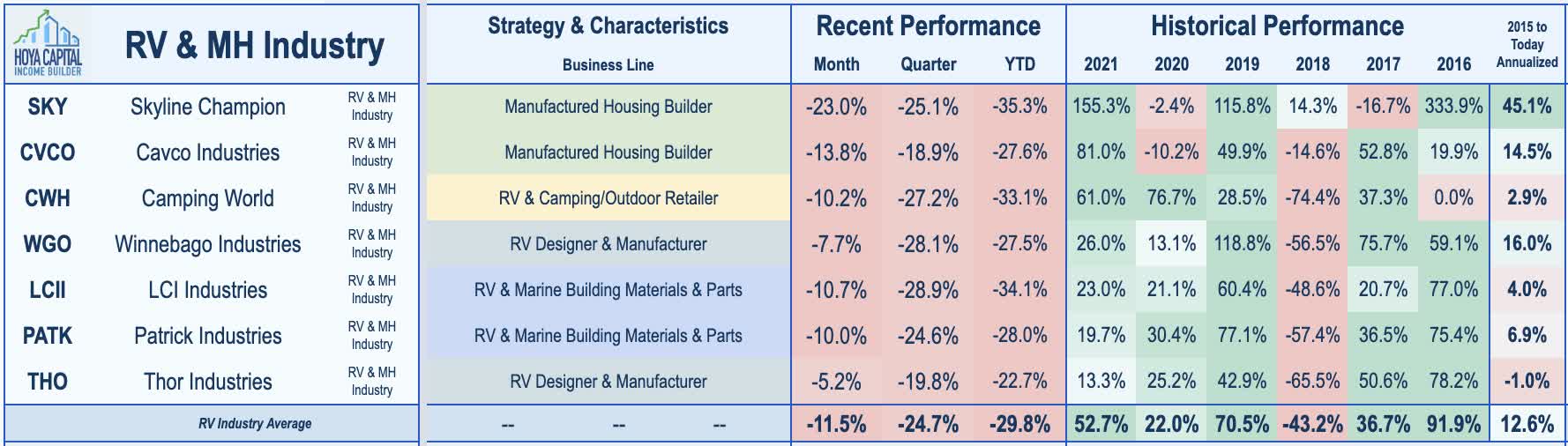

The non-REIT players in the manufactured housing and RV industry have also been under significant pressure this year following a robust 2021. After leading the gains last year, MH builders Skyline Champion (SKY) and Cavco Industries (CVCO) are each off by roughly 30% while RV retailer Camping World (CWH) is also lower by more than 30%. RV manufacturers including Thor Industries (THO) and Winnebago Industries (WGO) have seen similar declines of 25-35% so far in 2022, as have RV and marine parts dealers Patrick Industries (PATK) and LCI Industries (NYSE:LCII).

Deeper Dive: Inside Manufactured Housing

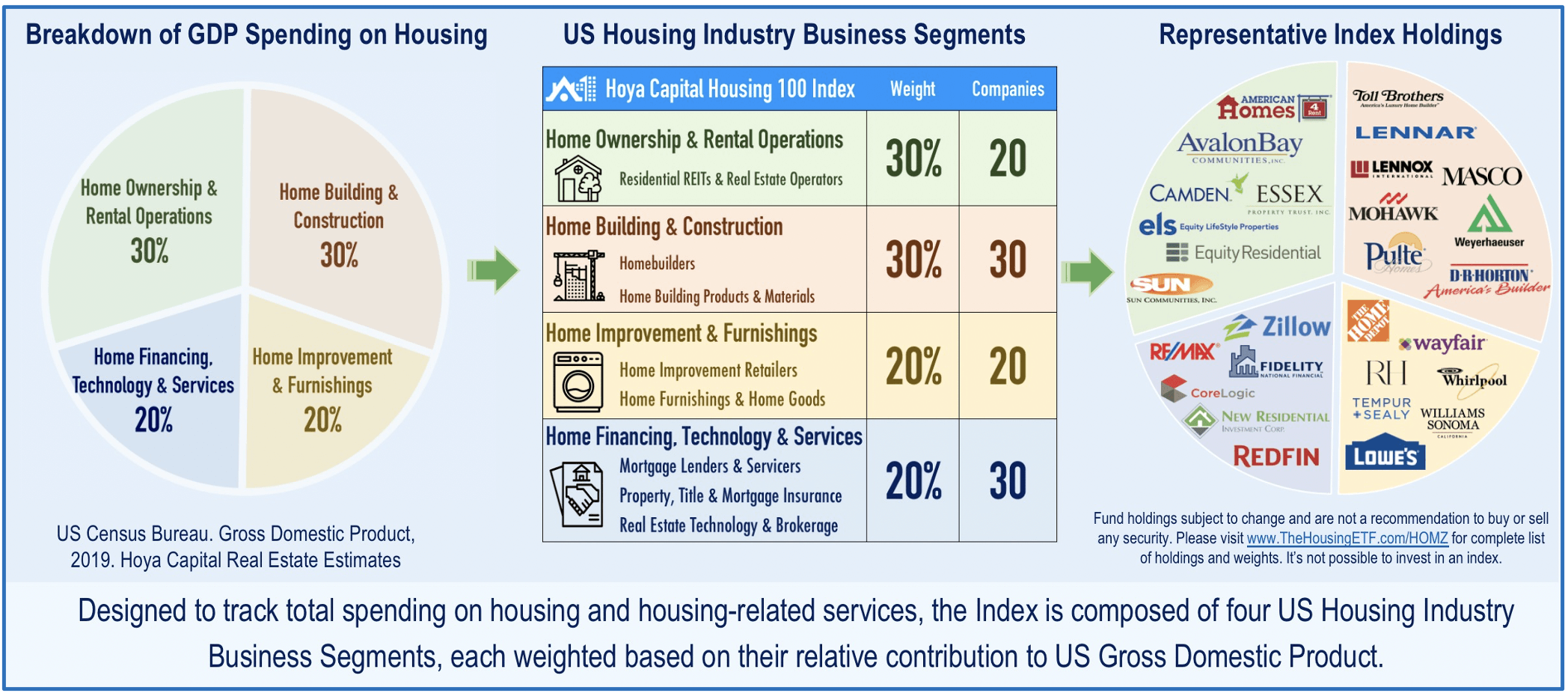

Roughly one-in-twelve Americans live in a factory-built manufactured home, and shipments of these units represent roughly 10% of housing starts in a typical year. MH REITs comprise 2% of the “Core” REIT ETFs and also represent 4% of the Hoya Capital US Housing Index, the benchmark that tracks the performance of the US housing industry. These REITs generally own communities in the higher tiers of the quality spectrum and are more “retiree-oriented” than the average MH community.

The quality and appearance of MH parks can vary significantly from communities that are nearly indistinguishable from a typical single-family master-planned community to the stereotypical “trailer parks.” Often misunderstood by investors, manufactured homes are generally not “mobile” (except for recreational vehicles “RVs”) as about 80% of MH units remain where they were initially installed, and while units are generally built to higher-quality standards than commonly believed, the JCHS report noted the MH homes were among those most “in need of repair.”

For residents, the economics of MH takes on the qualities of both renter and homeowner. Residents generally own their home but lease the land underneath it, paying an average of $70k for a new 1,500-square foot prefabricated home. The average monthly lease to set their home on a site and hook up to utilities in MH or RV community can range from $300 to $1,000 per month. By foregoing the investment in the land, however, property appreciation is generally minimal, and as a result, MH homeowners in land-lease communities generally cannot finance MH or RV purchases with traditional mortgages, and as with RVs, owners must finance the acquisition with a personal property (chattel) loan at a higher interest rate.

Manufactured Housing REIT Earnings

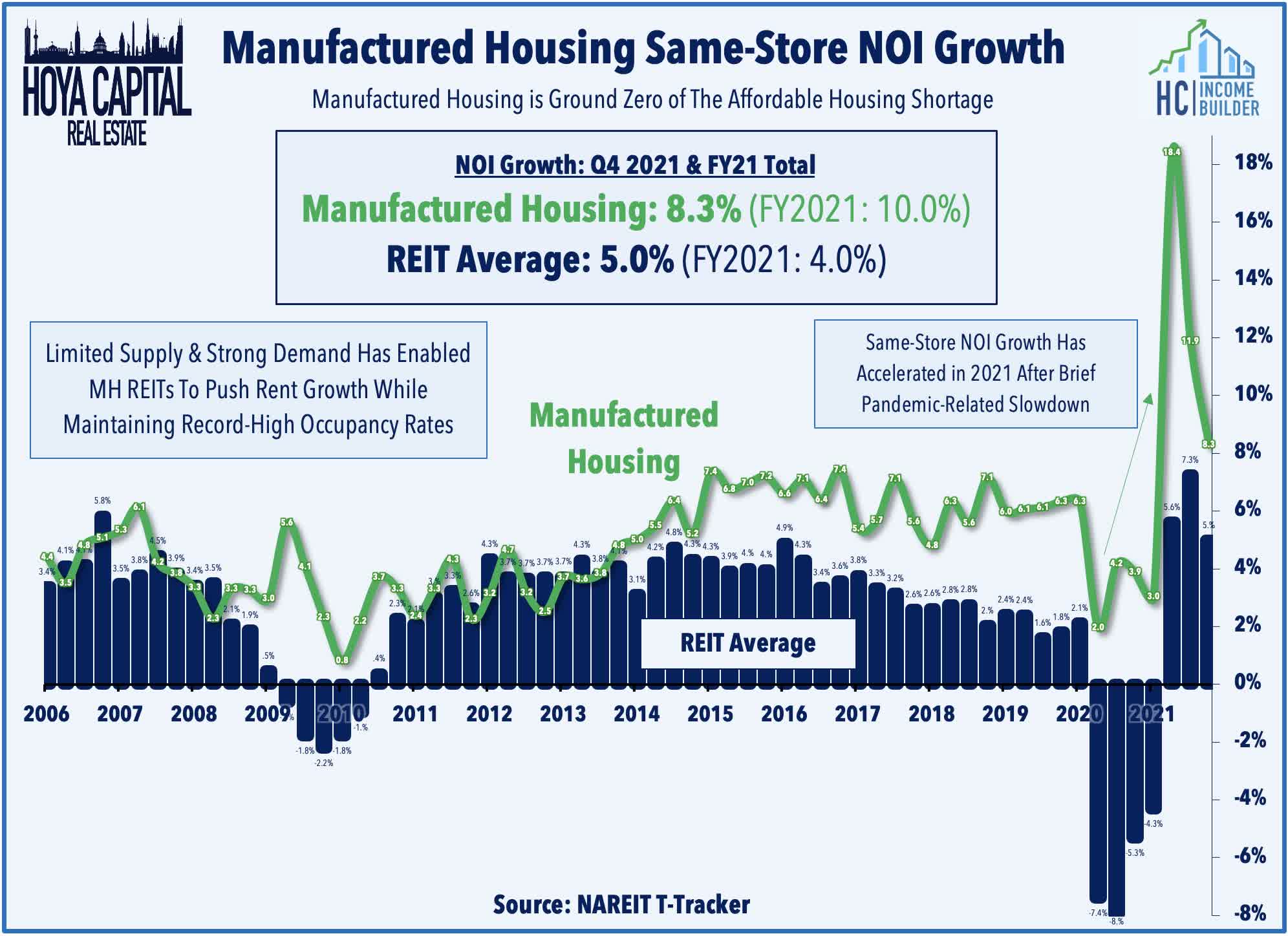

MH REITs have been the “canary in the coal mine” of the intensifying housing shortage for the past decade, continuing to produce sector-leading NOI and FFO growth and, as a result, have outperformed the Equity REIT Index in each of the past nine years – the longest streak of consecutive outperformance ever within the REIT sector. Driven by strong performance in their RV segment and occupancy increase in their core manufactured housing parks, the three major MH REITs – ELS, SUI, and UMH – delivered same-store NOI growth of 10% for full-year 2021 and these REITs are expecting NOI growth of another 8% in 2022 at the midpoint of their initial financial outlook.

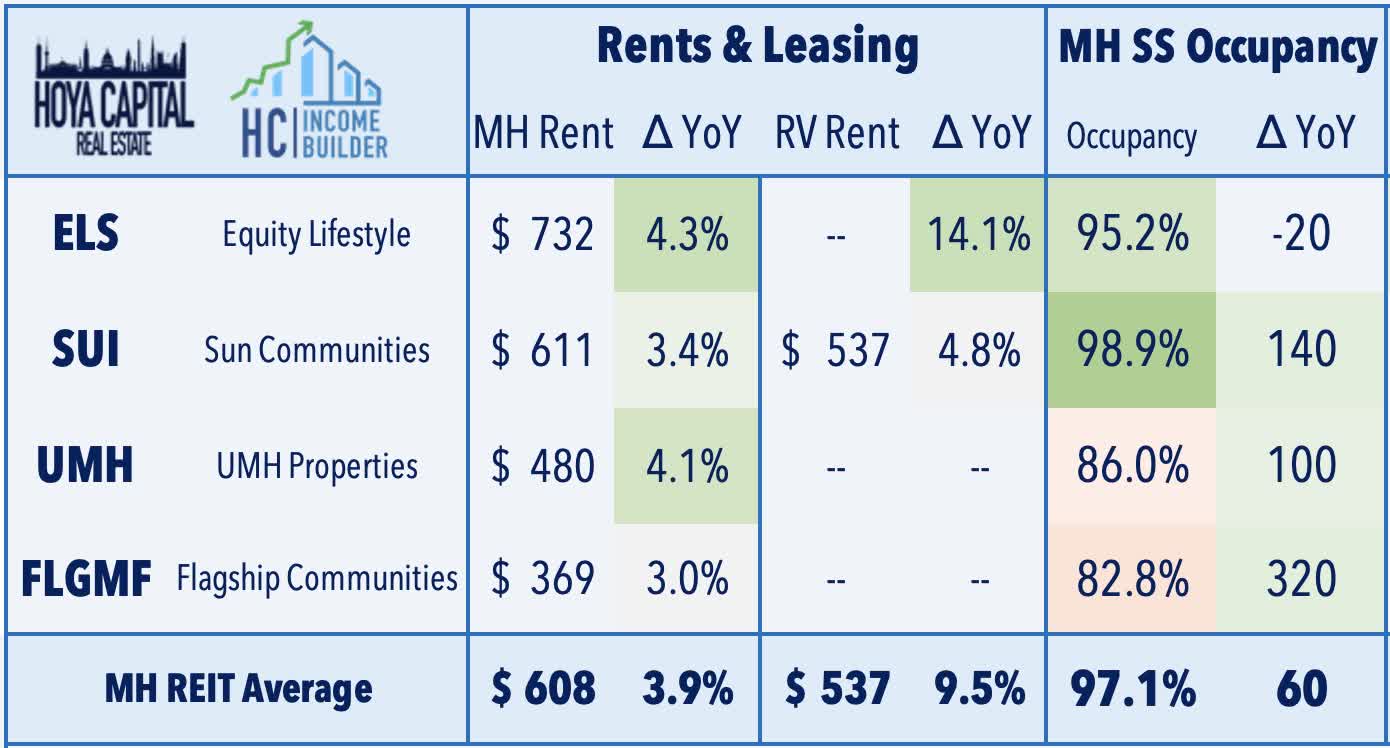

Occupancy rates ticked higher by another 60 basis points in Q4 while “core” manufactured housing rents increased by 3.9%. Driving much of the FFO gains in 2021 has been the strength seen in ELS’s and SUI’s transient RV facilities. ELS reported a 14% surge in RV rents in Q4 and expects to see another 5% rent growth in its RV segment in 2022 per its initial 2022 guidance, along with an acceleration in MH rents from 4.2% to 4.7%. SUI provided separate MH and RV revenue guidance for the first time this past quarter and sees an even more meaningful acceleration in both RV and MH rents in 2022.

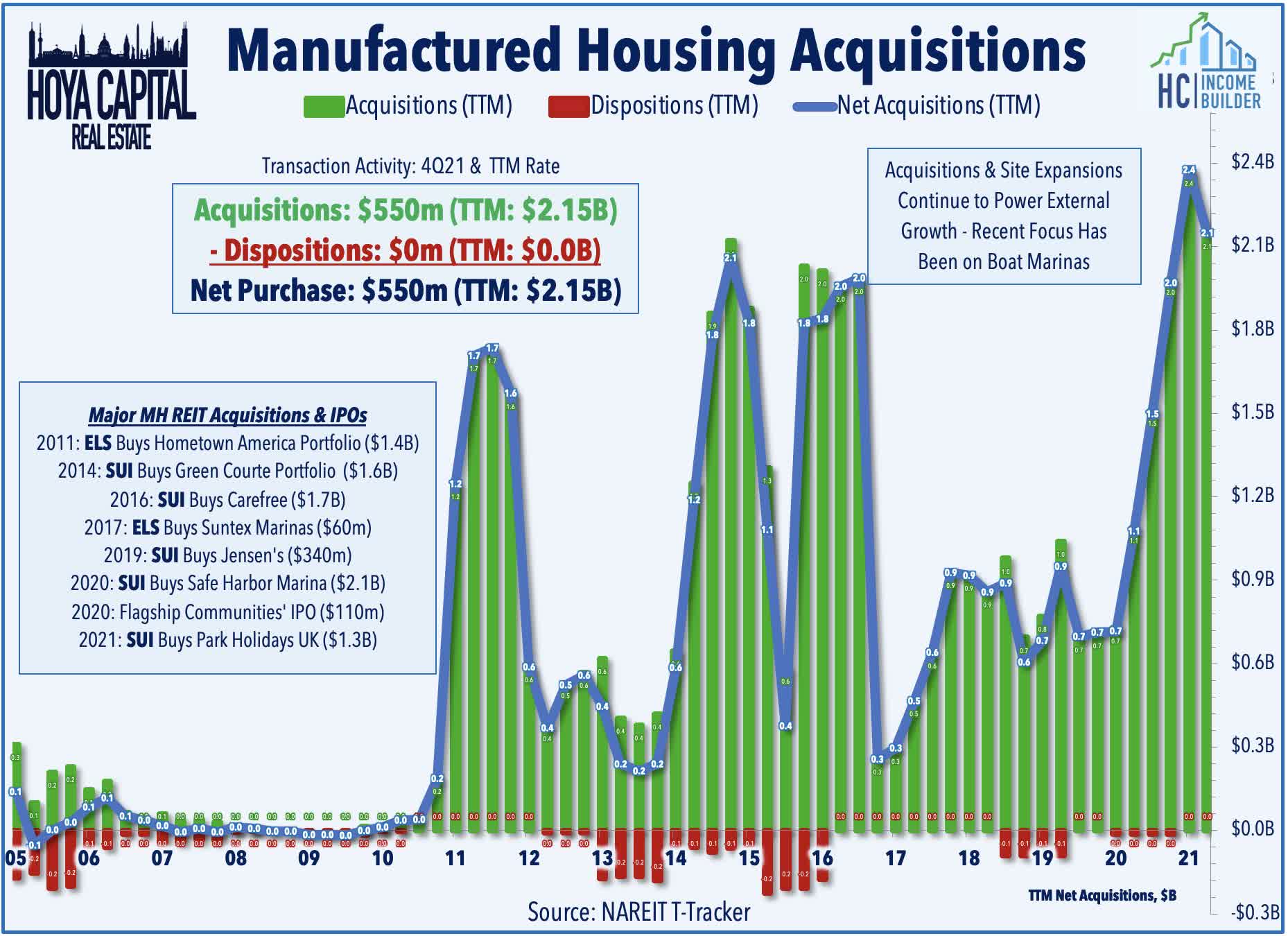

Utilizing a strong cost of equity capital, these REITs have continued to grow externally by adding units to existing sites and by growing via acquisitions and site expansions. MH REITs acquired nearly $2.5 billion in assets over the last year. On its earnings call last quarter, SUI CEO Gary Shiffman did note that while the acquisition pipeline remains robust, that SUI is “currently seeing continued cap rate compression in MH and RV. Certainly, everything is trading in the low-4s and much of it is trading sub-4 and the 3s. That pressure and the shortage of assets has continued with cap rate compression.” The most significant deal in 2021 was Sun Communities’ $1.3B purchase of Park Holidays, which is the second-largest owner and operator of holiday communities in the UK, with 40 owned and operated communities and an additional two managed communities.

Manufactured Housing REIT Dividend Yields

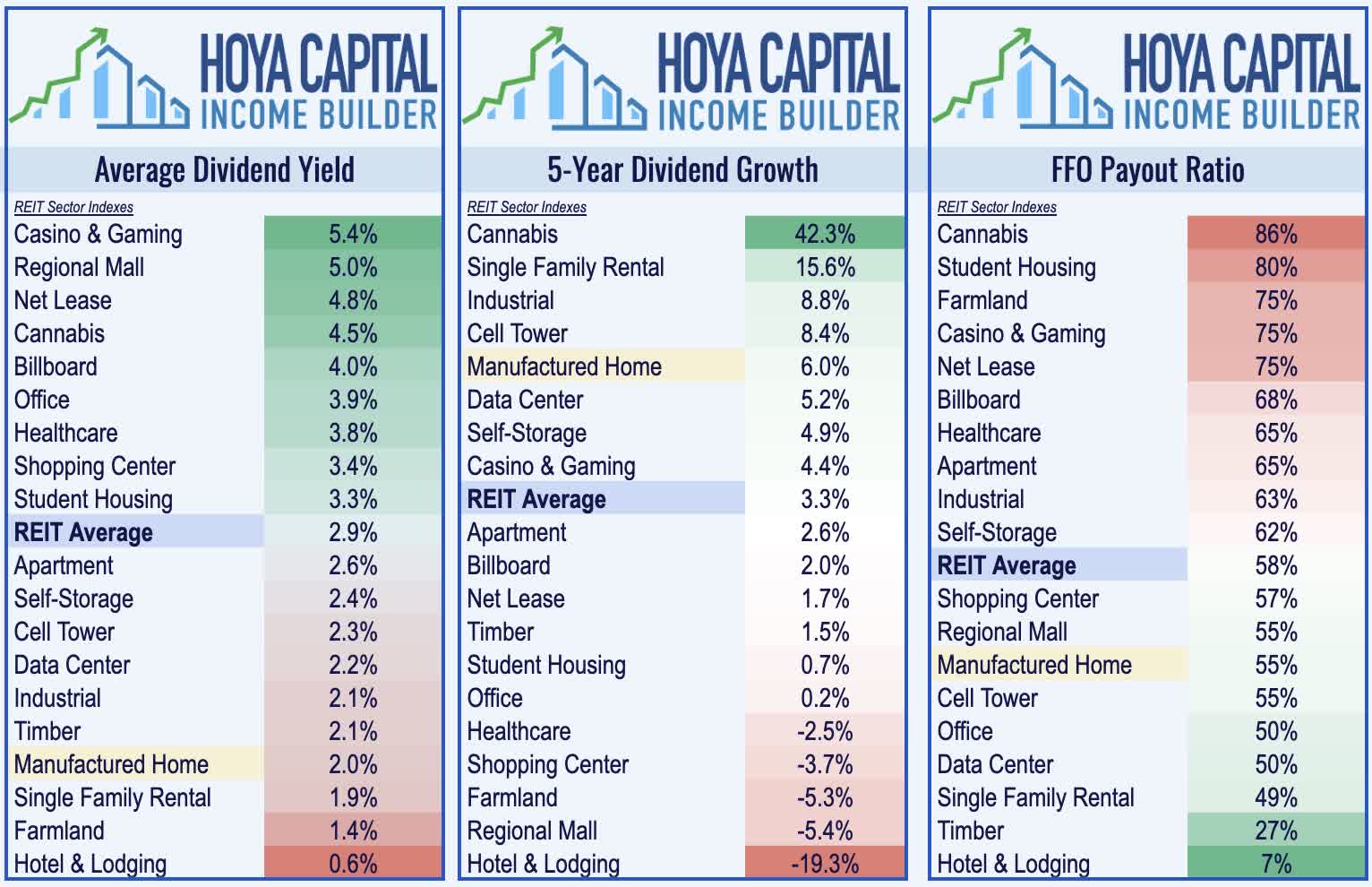

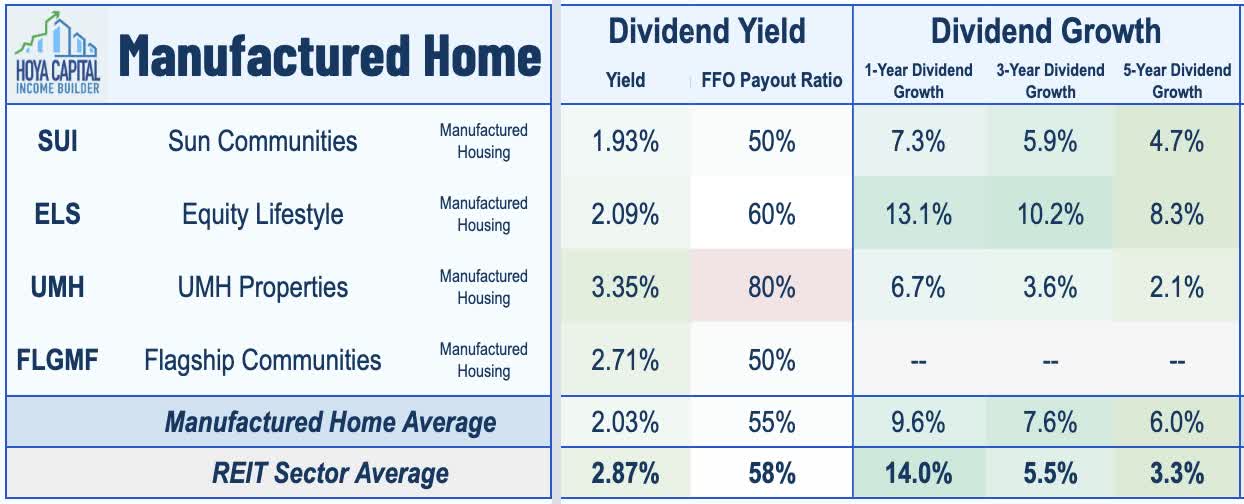

Manufactured Housing REITs pay an average dividend yield of 2.0%, ranking towards the bottom of the REIT sector and below the market-cap-weighted average of 2.9%. MH REITs, however, have delivered one of the strongest rates of dividend growth over the last five years. ELS and SUI are two of only a dozen REITs that raised their dividends in 2020, 2021, and again in 2022. MH REITs pay out just 50% of their available cash flow, implying strong potential for future dividend growth and more free cash flow to fund external growth.

Among the three larger MH REITs, UMH Properties pays the highest dividend yield in the sector at 3.35% but went nearly two decades with zero dividend growth before finally raising its distribution for the first time since 2008 earlier this year. Equity LifeStyle pays a dividend yield of 2.09%, while Sun Communities pays a dividend yield of 1.93%. ELS has delivered average annual dividend growth of 8.3% over the last five years, among the best in the REIT sector, while SUI has taken a more growth-oriented approach with a lower payout ratio and a dividend yield of 1.93%.

Takeaways: Affordable Prices for Elite REITs

Manufactured Housing REITs have emerged over the past decade from relative obscurity into several of the most well-run publicly-traded property owners in the world, but have uncharacteristically stumbled in early-2022. MH REITs are among the most interest-rate-sensitive property sectors, resulting primarily from the remarkable consistency in delivering mid-single-digit rent growth regardless of the macroeconomic environment. We expect rent growth to significantly exceed analyst forecasts due to the COLA effects, which will drive another year of double-digit FFO growth and, potentially, a tenth straight year of outperformance.

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Prisons, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Be the first to comment