Torsten Asmus/iStock via Getty Images

Introduction

Magnet Forensics (TSX:MAGT:CA) (OTCPK:MAGTF) describes itself as a developer of data analytics software used for digital forensics investigations. Investigators use Magnet’s software to identify, extract and analyze forensic artifacts and the company’s initial product offering was specifically targeting law enforcement agencies all over the world.

Magnet Forensics Investor Relations

Fellow author Another Mountain’s Rock Investing provided an excellent breakdown of Magnet Forensics in his article which you can find here. Kudos to Another Mountain, as the company announced last week it’s being acquired by a private equity group in an all-cash deal at C$44.25 per share.

Magnet Forensics Investor Relations

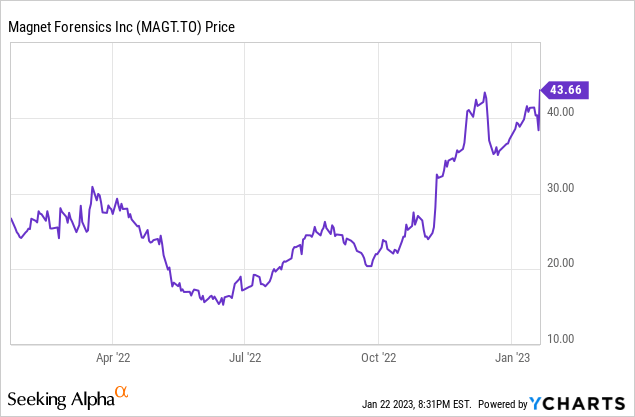

Magnet’s primary listing is on the Toronto Stock Exchange where the company is trading with MAGT as its ticker symbol. The average daily volume is just over 60,000 shares per day. The stock is trading at a small discount vs. the offered price, so while arbitrage is possible, the 1.5% upside potential may not be sufficiently appealing unless the deal closes fast. As of Sunday evening, no date has been set for the general meeting to approve the transaction but plans of arrangements usually take anywhere between 2-4 months.

Magnet’s 9M 2022 results were good, but the buyout offer comes at the right time

Before diving into the specifics of the buyout offer, we should first discuss the financial performance of the company as that ultimately determines whether or not the all-cash acquisition offer is fair and reasonable.

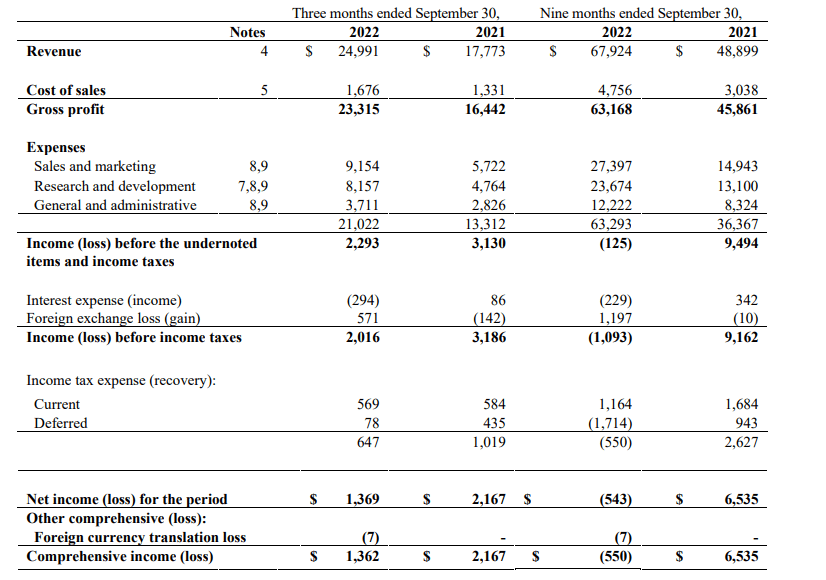

During the third quarter of 2022, Magnet reported total revenue of US$25M (the company reports its financial results in USD) which resulted in a gross profit of $23.3M as the COGS is exceptionally low (which obviously isn’t unheard of in the software sector).

Magnet Forensics Investor Relations

The majority of the operating expenses are related to R&D and sales and marketing, but after spending in excess of $21M on these (useful) expenses, the company still reported a quarterly EBIT of $2.3M which ultimately resulted in a net income of $1.36M for an EPS of $0.03.

Looking at the 9M 2022 performance, the total revenue was almost $68M and this resulted in a small net loss of $0.55M thanks to a net tax benefit of approximately $0.55M as well.

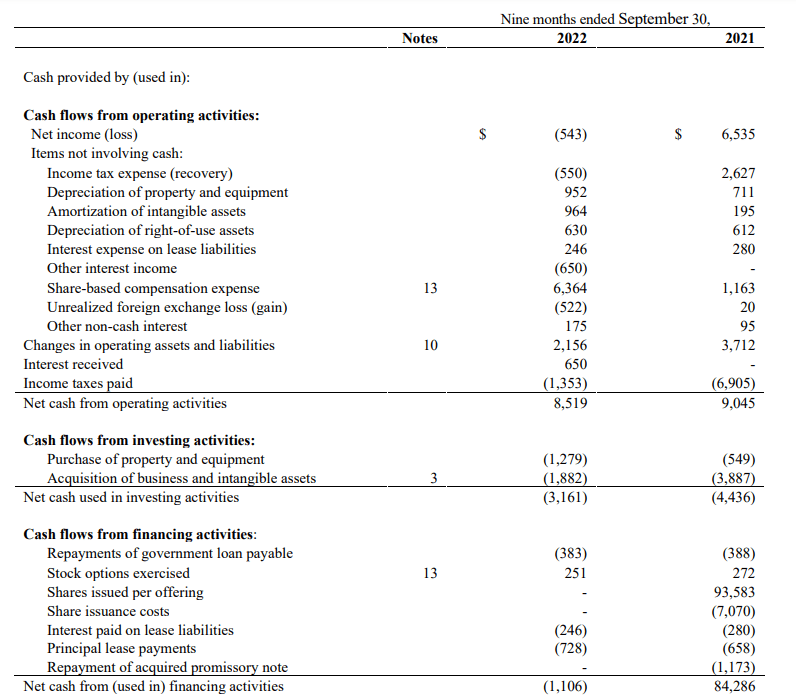

Keep in mind the share-based compensation is very high, and as that’s a non-cash expense, the cash flow statement actually looks more interesting than the income statement. We see the reported operating cash flow was approximately $8.5M in the first nine months of last year although this was also fueled by a $2.15M contribution from changes in the working capital position.

Magnet Forensics Investor Relations

If we would isolate the impact of those working capital changes an subsequently also deduct the $1M in lease and lease interest payments, the adjusted operating cash flow was approximately $5.35M. And with a total capex of $1.3M (excluding acquisitions), the underlying free cash flow result was roughly $4M. A much better result than the $0.55M net loss, despite having paid $1.35M in taxes, so on an underlying basis, the free cash flow result would have been even higher than the aforementioned $4M.

It’s important to note there was a pretty drastic acceleration in the free cash flow result in the third quarter. Magnet Forensics ended June with an adjusted operating cash flow of approximately $1.5M and a free cash flow result of $0.7M so the free cash flow result in the third quarter

What’s Thoma Bravo offering the Magnet shareholders?

Thoma Bravo, a US based private equity firm with a specific focus on software, is offering the shareholders of Magnet Forensics C$44.25 per share in cash to acquire full ownership. Upon completion of the acquisition, Thoma Bravo plans to merge Magnet Forensics with Grayshift, another company in its asset portfolio.

Grayshift is a provider of mobile device digital forensics so it makes sense to merge both Magnet and Grayshift as there must be some cross-selling opportunities while creating a leader in the digital forensics space.

I expect the transaction to go ahead. Not only is there unanimous board approval, the stock is acquired at a 52-week high. Not an all-time high as the share price peaked above C$60 in the second half of 2021 but valuations in the tech sector are more reasonable now. Additionally, the stock was trading at less than C$15 per share as recent as June, so receiving a C$44.25 buyout offer will for sure feel like a win.

Thoma Bravo is paying approximately 50 times the anticipated EBITDA in 2023 and likely still north of 30 times the 2024 EBITDA. This limits the possibility for a third party to emerge as challengers as Thoma Bravo will be able to unlock synergy benefits by combining the entity with Grayshift.

Investment thesis

I have very little doubt the deal will go ahead as the offer appears to be very fair, the management and board are supporting it, and shareholders can walk away with a check valuing the company at roughly 50 times this year’s EBITDA.

Arbitrage is possible, but the current 1.35% spread may not be meaningful enough for investors. That being said, if the deal closes within three months, we are looking at an annualized return of 5.5% (excluding transaction fees).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment