CJNattanai/iStock via Getty Images

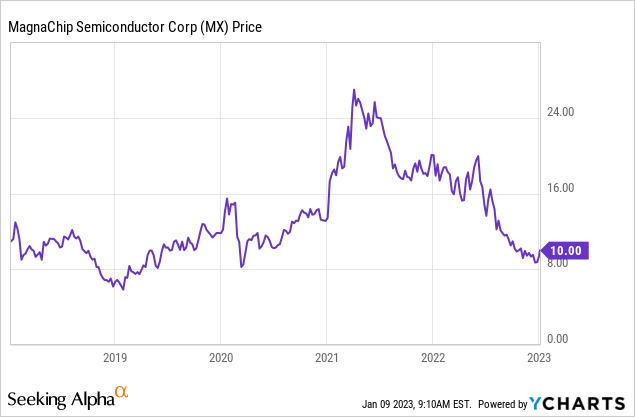

Magnachip Semiconductor Corporation (NYSE:MX) was going to be taken out at $29 per share. It wasn’t and it is left for dead at ~$10 per share. Magnachip has been one of my bad calls. I’ve been bullish from a signed deal (that got blocked) to rumors of another deal (that didn’t come to pass either). I’ve been holding and adding as its valuation got ever more ridiculous. Is it now finally bottoming around $10? It is back to where it was at the bottom in March 2020…

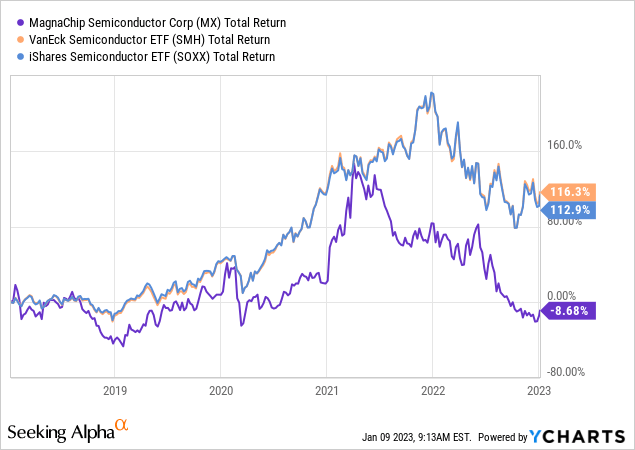

To put the level of disappointment with the deals falling apart into perspective, I’ve pulled up a five-year chart that shows MX its correlation to popular semiconductor exchange-traded funds (“ETFs”) VanEck Semiconductor ETF (SMH) and iShares Semiconductor ETF (SOXX):

There’s been disappointment since the deal fell apart in 2021 (steep drop H1 2021) and no deal coming to fruition in 2022 (sharp drop mid-2022), but I’d argue a lot of the selloff has been driven by interest rate moves and the effect it has had on the broader semiconductor space. The effect seems to have been larger with Magnachip, but that’s not surprising, given it is a small-cap Korean semiconductor with a concentrated customer base. I believe the downside moves should increasingly be limited because of a large amount of cash and the absence of debt. The company holds something like $5.6 in net cash per share on a $10 stock of a company that should act as something of an anchor. I would be highly supportive if management is smart enough to pound the outstanding shares.

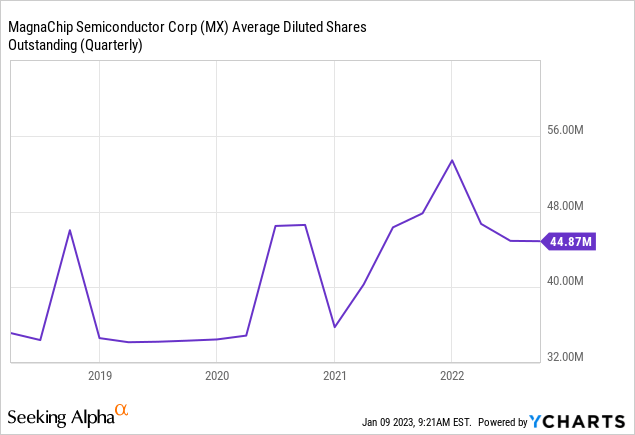

They’ve recently done a solid job decreasing the outstanding shares a bit, but they could be more aggressive. At this point, the cash hoard could (theoretically) take out 25 million shares. That’s over half the shares… If they would assume $40 million in debt, they could take out another 4 million shares. That would leave the company with an efficient, but not overly leveraged, capital structure, and theoretically, it would take out 65% of the existing shares. This is only a theoretical exercise, because if you’re taking out shares, it will drive up the share price, which makes it increasingly costly to take out shares. It’s just a theoretical exercise to make a point the current share price seems excessively pessimistic, especially as management has shown a willingness, albeit tentatively so, to take out some shares.

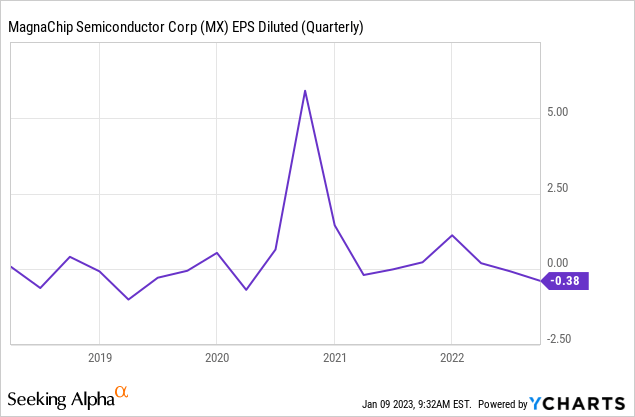

Why would shares trade at such abysmal levels? Well, earnings estimates (scheduled for February) aren’t good. Per Seeking Alpha numbers, the consensus is around $-0.26 per share. At that rate, we’re bleeding the excess cash at a rate of $1 per year.

MX upcoming earnings (Seeking Alpha)

There is some good news in that the company has recently been outperforming expectations:

EPS suprises MX (Seeking Alpha)

There is more good news in that the EPS estimate for the entire 2022 was actually positive and analysts expect it to be positive (and significantly higher at $0.36) for the entirety of 2023.

EPS estimates MX FY 2022 2023 (Seeking Alpha)

The recent earnings have been pretty bad. Semiconductor specialists likely saw that coming and sold off or didn’t want to buy the stock from exiting arbs.

The main culprit of the very weak earnings recently has been the display business getting destroyed. Per the most recent earnings call (emphasis added):

Beginning with our Display business, Q3 revenue was $6.4 million, down 89.1% year-over-year, and 77.6% sequentially. These results were primarily due to the supply shortages of 28 nanometer 12-inch OLED wafers in the second half of this year that impacted design-in projects from our large panel customer in Korea, which are typically awarded in advance based on future wafer supply allocation.

In addition, China COVID lockdowns and the dramatic slowdown in consumer spending as a result of global inflationary pressures reduced demand for smartphones, particularly in China, and resulted in an oversupply of channel inventories. This caused our large customer in Korea to significantly reduce orders to normalize inventory levels. Unfortunately, we believe these poor dynamics will continue in the near future, but we expect inventory levels will normalize by the middle of next year.

As the global geopolitical situation and economy remains very uncertain, we are focusing on executing the initiatives that are in our control and delivering a strong recovery of our Display business in 2023. During Q3, we made progress in these following areas:

As it happens, China has seemed to curb its Covid protocols of late, and its stock market seems to like it. China averages are up quite a bit in the last three months after an extended period of poor performance.

Coincidentally, it looks like Magnachip’s share price has finally bottomed and is coming off its floor. The company also provided further color on how it believes the display business will recover in 2023. There should be a catalyst at the end of Q1 2023 and at the end of 2023 (emphasis added):

First, regarding our new top-tier panel customer, last quarter, we disclosed that the timing of our mass production ramp was delayed due to the customer requesting a feature change so we had to make modifications to our product. In the beginning of October, we successfully released the new modified OLED DDIC to this customer and is now undergoing customer qualification. We anticipate this customer to complete qualification by the end of this year.

However, due to the continued weak consumer demand and channel inventory oversupply in China, we expect the production to commence towards end of Q1 2023. While this is unfortunate, the good news is that we received a second design-in project with this large customer.

We are extremely excited about this new award as it presents greater volume potential than the first project and also demonstrates our committed partnership. We expect to begin taping out this new part in November this year and begin mass production in late 2023. Over the next few years, OLED production in this region of the world is expected to more than double so we are obviously excited about our growing relationship with this customer.

For me, this is currently a 3.53% position. That’s with being deeply underwater already. I’m contemplating adding a little bit here. It’s not necessarily the greatest idea to average down losers – as someone recently pointed out to me in my Silvergate Capital (SI) article.

In this case with the net cash and absence of debt, I’m more inclined to do so. For me, a 3.53% position is currently on the larger side. For many people, that’s small, but for me, it is a top 6 position.

I tend to prefer situations where there’s some catalyst on the horizon. Semiconductor experts will have much better insight into this, but the China reopening could actually serve as something of a hidden 2023 catalyst for Magnachip Semiconductor Corporation. It will take time to play out, but markets are forward-looking and a rerate can happen quickly. On an ex-cash basis, Magnachip Semiconductor Corporation trades around 12x consensus 23′ earnings. That’s not rich for a semiconductor company active in what are long-term secularly growing areas of businesses(displays and electrification). Meanwhile, I’m feeling pretty good about the downside because of the financial position of Magnachip Semiconductor Corporation.

Be the first to comment