Drew Angerer

Investment thesis

Once the largest department store chain in the U.S., Macy’s (NYSE:M), is struggling to keep up with rapid changes in the retail industry. In recent years, the company has seen declining sales that have led to store closings and job cuts. The company has been slow to invest in e-commerce and has not differentiated itself from other brick-and-mortar retailers. In the current tight economic environment with rising interest rates and fierce competition Macy’s will most likely struggle to generate sufficient cash flows to support future growth or increase dividends. All these factors, in my opinion, make Macy’s a risky investment with very limited upside potential.

Company information

Macy’s Inc, operates department stores under the names Macy’s and Bloomingdale’s. Founded in 1858 and based in New York City, the company operates more than 620 stores including outlets and about 160 Bluemercury specialty beauty stores.

Macy’s

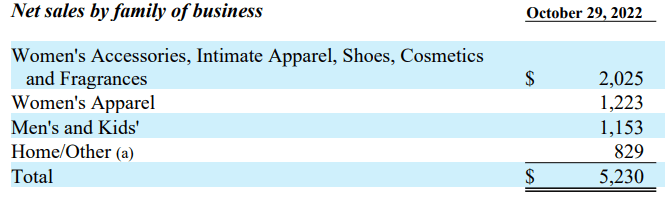

Women’s apparel, accessories, shoes, cosmetics, and fragrances comprise about 62% of Macy’s sales. The men’s and children’s businesses represent a combined 22% of sales, and home/miscellaneous about 16%. The company has almost 90,000 employees.

Below you can see Macy’s disaggregation between business segments for the quarter ended October 29, amounts are presented in $ millions.

Macy’s 10-Q

Financials are weakening

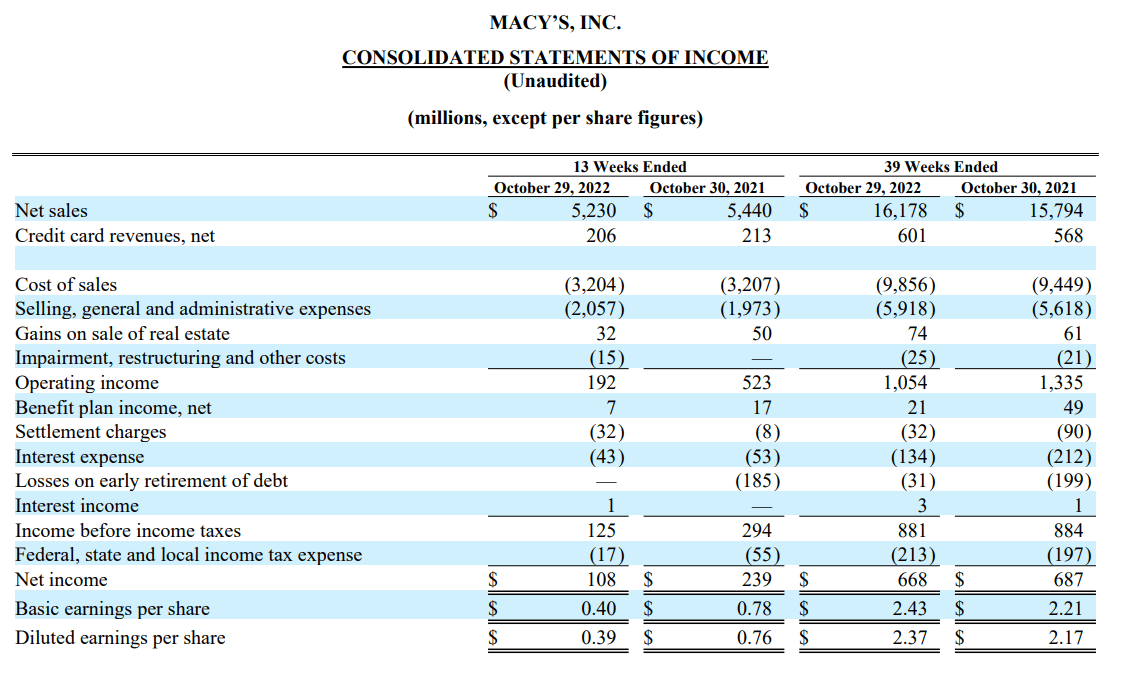

The company reported it’s latest quarterly results on November 17, 2022.

Macy’s

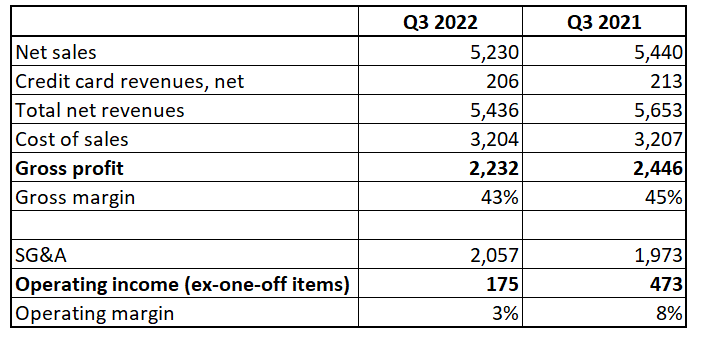

Macy’s demonstrated consensus estimates beat both in terms of revenue and in terms of EPS, but margins and earnings shrinked significantly if we compare on a year-over-year basis.

Author’s calculations

Operating income decreased by 63% comparing to 3Q2021 (excluding one-off items) due to both decrease in net sales by almost 4% as well as narrowing gross margin and increased SG&A. As we can see from the table above, gross margin demonstrated a 230-basis point decline YoY. This decrease was driven by increase in promotional and permanent markdowns within the Macy’s brand to sell through slower moving categories, according to company’s earnings presentation. Increased fuel costs was the second major factor which put downward pressure to gross margin.

To better understand the financial dynamics of Macy’s, I decided to analyze the company’s income statement for the last 10 years:

Author’s calculations

As you can see, the company’s financial performance has deteriorated across the board over the last 10 years, with revenue down nearly 9% in absolute terms since 2013 and operating income down 13% over the same period. Selling, general and administrative expenses have also decreased, but their percentage of revenue is still over 30%.

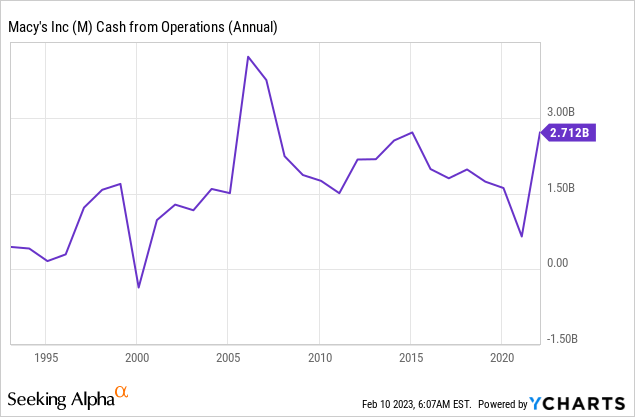

From cash flows perspective we can see that last year the company demonstrated cash from operations far below its’ peak before Global Financial Crisis and almost at 2015 levels. Given inflationary factor, it is obviuos that in real terms company’s cash flows from operations deteriorated significantly if there was no change in nominal amounts in last 7 years.

The company had a lot of different strategic initiatives in recent years, but the numbers above suggest that they do not seem to be helping to drive revenue growth or increase profit margins. I totally agree with Chris Walton from Forbes, who wrote the following in his article three years ago:

None of Macy’s referenced strategies answer the fundamental question: Why still come to a Macy’s to shop?

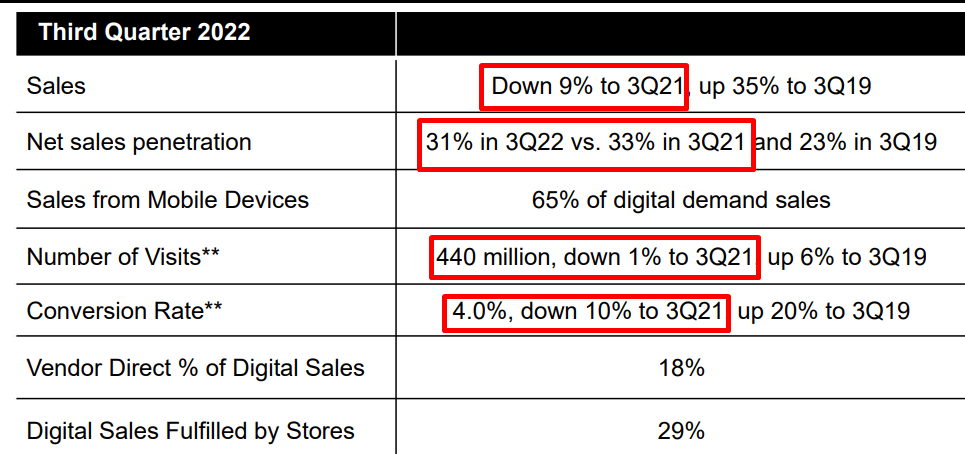

The company’s management believes that its’ Digital sales channel will be important growth driver fro future revenues, but, as we can see from the latest earnings presentation, it demonstrated decline almost accross all metrics in 3Q2022 compared to 3Q 2021:

Macy’s

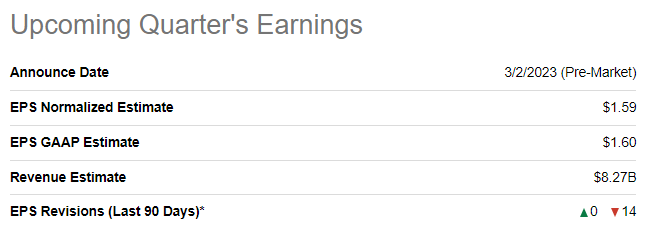

Nowadays Macy’s is trying to stay relevant through its Polaris and omnichannel initiatives. Polaris strategy was unveiled in early 2020, but since then the company’s financial performance has improved only marginally and consensus forecasts indicate that revenue will not grow over the next three years and EPS will shrink by FY2025. For the nearest reporting quarter there were 14 downward EPS revisions within last 90 days:

Seeking Alpha

To summarize this part, there is little evidence that management’s strategic initiatives are attracting new customers or causing existing customers to increase spending. In my opinion, without revenue growth the company has no way to significantly improve its bottom line, given the current hyperinflationary macro environment.

DDM suggests stock is overvalued

In order to conduct Macy’s valuation I implemented the Dividend Discount Model (DDM) because in current macroeconomic circumstances I am not sure that it is possible to reliably estimate company’s revenues and margins beyond FY 2025.

So, in order to use DDM I need to incorporate reasonable assumptions about , next FY dividend per share, the pace of dividend growth and the required rate of return.

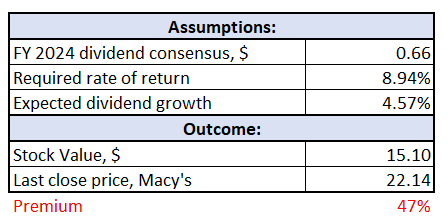

For FY 2024 we have consensus estimates on Macy’s dividend per share, which is currently projected at $0.66 per share. From dividend growth perspective forecasting is trickier because the company’s dividend growth CAGR for last 3, 5 and 10 years was negative and, on the other hand, forward rate looks way too high. So, to be conservative and fair I decided to implement Dividend Per Share Growth FY1-FY3, which is estimated at 4.57%.

Seeking Alpha

For the required rate of return I assume that incorporating WACC is a sound choice. According to Gurufocus, current company’s WACC is 8.94%.

Incorporating all above assumptions to DDM I ended up with fair stock value of $15.10 per share which is almost 50% lower that the last close price of $22.14 per share.

Author’s calculations

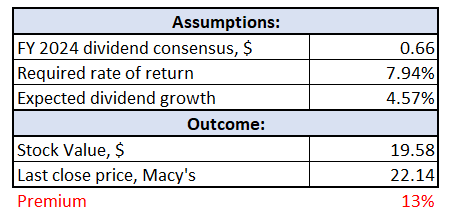

I challenged the DDM with sensitivity checks by playing separately with required rate of return and expected dividend growth rate.

For first sensitivity check I implemented a 100 bp lower WACC of 7.94% which is rather soft, the model suggests 13% premium now:

Author’s calculations

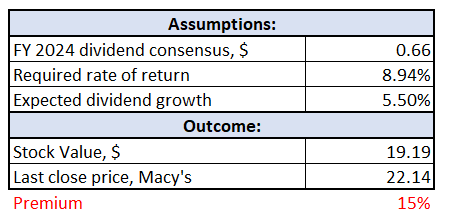

For second sensitivity check I left WACC at 8.94% but implemented more generous expected dividend growth rate at 5.5% pace, calculations still show that the stock is overvalued at the moment:

Author’s calculations

To make sure that my DDM calculations are sound let’s also check P/E multiples. Company’s 5 year average TTM P/E is 5.29, which means stock fair value is $20 per share if we incorporate FY2024 consensus EPS. Multiples analysis results look better than my DDM outcomes, but still demonstrates no upside potential for the stock.

Don’t forget about risks as well

The major risk which is inherent to all retailers is that they are vulnerable to a downturn in the economy. Much of the merchandise sold by Macy’s related to upscale segment which are discretionary items, and thus, these purchases can be deferred. During tight economic times customers, like we are facing now, usually step back and buy cheaper products at other stores like Kohl’s or Target.

Another significant risk is rapidly growing e-commerce competition. It is not only about e-commerce giants like Amazon, but also about vendors who are enhancing their own e-commerce platforms and applications, selling their products directly to customers online, or opening their online stores at marketplaces like Amazon. For example, in early 2021 Nike cut ties with several retailers, including Macy’s. The ultimate result is price competition here because numerous retailers fight for the client and market share. Therefore it is difficult to expect margins to widen for companies like Macy’s.

Two risks above will highly likely put pressure on Macy’s financial performance which can be painful for the company considering its $3 billion long-tem debt on the balance sheet. For sure, it is much lower than we have seen recently, but still credit risks will grow if results worsen in case of a recession.

Bottom line

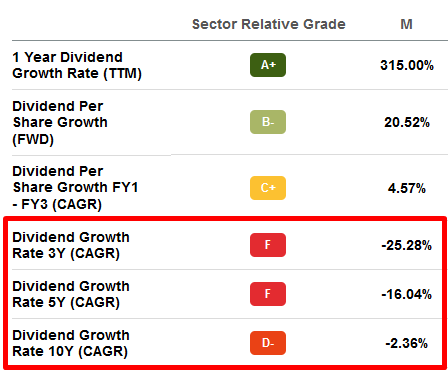

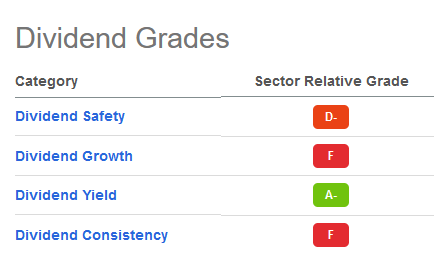

In summary, I believe that the risks associated with investing in Macy’s stock far outweight the potential benefits. The stock is a strong sell as DDM and multiples analysis suggests the stock is currently traded at a premium and there are several headwinds for Macy’s to drive future growth. Dividends are also at risk in the current macroeconomic environment, as evidenced by very low dividend grades provided by Seeking Alpha Quant ratings:

Seeking Alpha

Be the first to comment