Daniel Grizelj

Introduction

Following a very strong recovery during 2021, LyondellBasell (NYSE:LYB) saw a very strong start to 2022 but at the same time, only provided soft shareholder returns despite their prospects to ramp them up much higher, as my previous article discussed. Thankfully, this soon changed with the second quarter of 2022 seeing a very large special dividend, their first ever declared that if continued, stands to boost the moderate yield of 5.16% from their routine quarterly dividends to a very high 10%+. When looking ahead, this marks a new era for dividends, despite lacking communication from management, as discussed within this follow-up analysis that also reviews their recently released results for the second quarter of 2022.

Executive Summary & Ratings

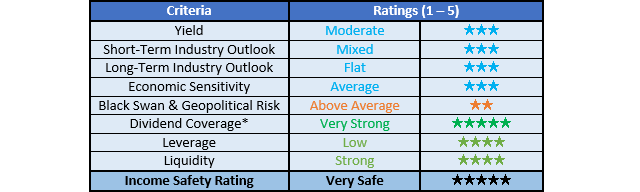

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing dividend coverage through earnings per share cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

Author

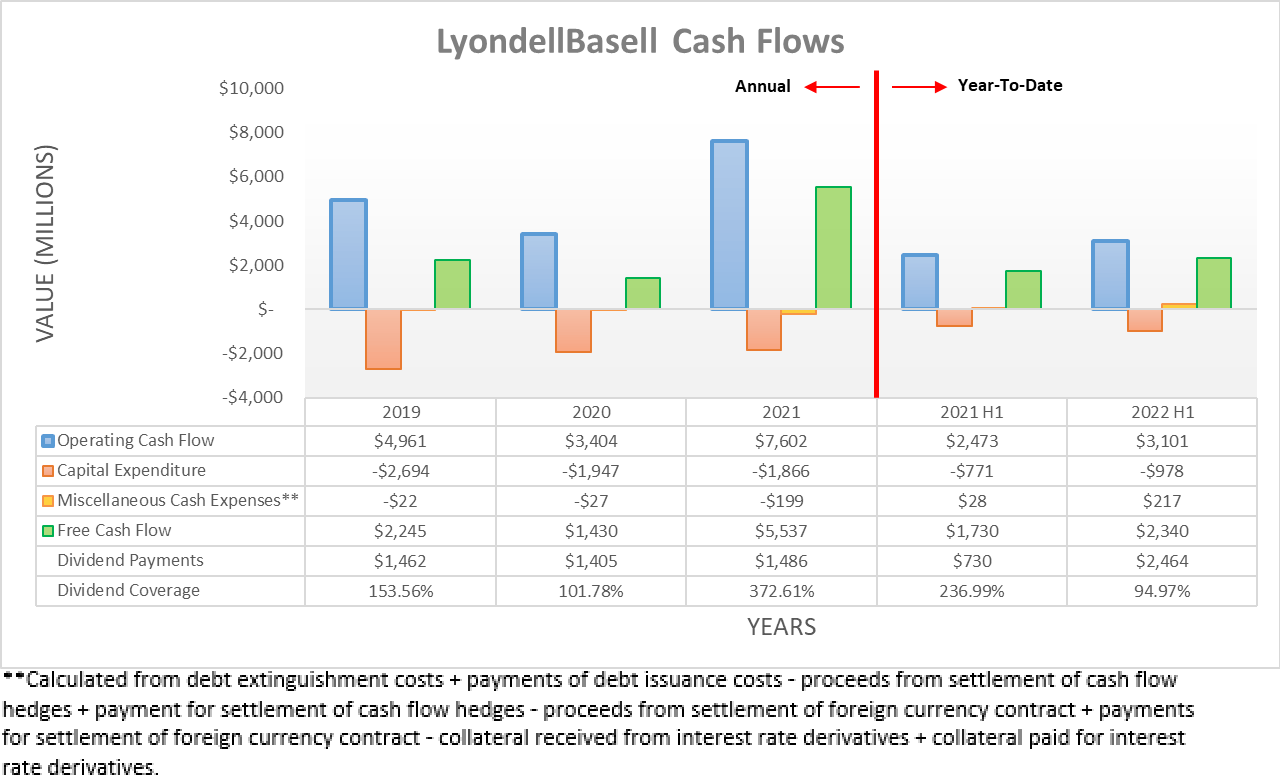

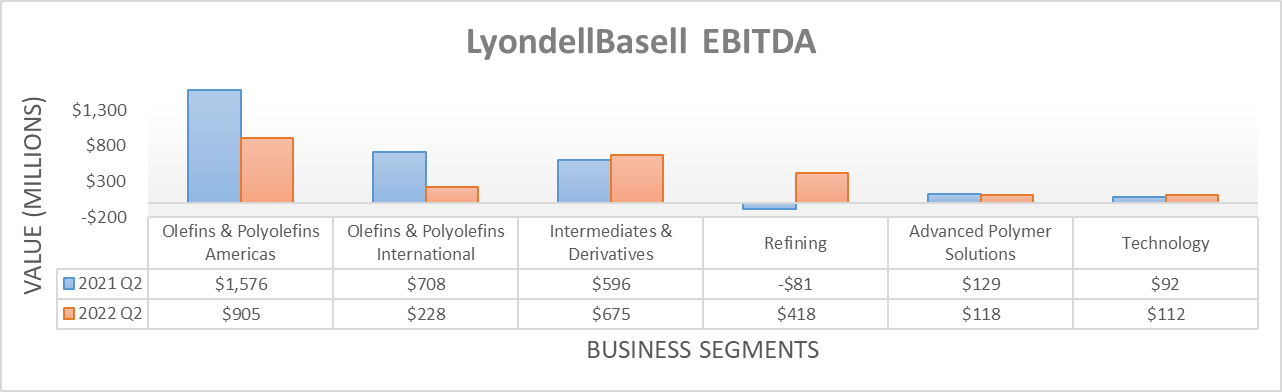

On the surface, it appears their very strong cash flow performance during the first quarter of 2022 carried through into the second quarter with their operating cash flow increasing to $3.101b during the first half, thereby sitting 25.39% higher year-on-year versus their previous result of $2.473b during the first half of 2021. Although upon digging deeper, this comparison was skewed favorably by their temporary working capital movements, which if removed see their underlying operating cash flow for the first half of 2022 at $3.595b. Whilst this is actually $494m higher, the benefit to their equivalent previous result for the first half of 2021 is far more significant with its result climbing to $4.034b. Since this represents a decrease of 10.88% year-on-year for the first half of 2022 whereas the first quarter saw a very strong increase of 27.32%, it means that the second quarter actually saw significantly lower results, which were driven by their olefins and polyolefins business segments, as the table included below displays.

Author

Similar to most companies, they do not list their cash flow performance by business segment but given its positive correlation to EBITDA, we can still seek the cause of their weak second quarter of 2022 results, which was clearly due to their olefins and polyolefins business segments for the Americas and International markets. The opaque nature of these markets makes it difficult as an outsider to assess the moving parts as they are nowhere nearly as publicized as the oil market and disappointingly, they were only discussed very briefly during their second quarter of 2022 results conference call with higher costs appearing to have hindered their results, as per the commentary from management included below.

“North American demand for polyolefins continue to be very strong. Higher costs for ethane and energy pressured olefin margins and offset the benefits of improved polymer prices.”

-LyondellBasell Q2 2022 Conference Call.

Despite not being ideal, thankfully they still generated free cash flow of $2.34b during the first half of 2022 and even more excitingly, they marked the beginning of a new era by paying their first ever special dividend that landed at a very large $5.20 per share. Even momentarily ignoring their normal quarterly dividend that was boosted slightly more than 5% to $1.19 per share, this singular special dividend already represents a yield of circa 5.60% on their current share price of $92.33. Even if this only occurred once per year, which is a conservative assumption, when added to their routine quarterly dividends, it lifts the yearly total to $9.96 per share and thus would see shareholders taking home a very high 10%+ yield on current cost.

When last discussing their shares, the prospects of seeing shareholder returns ramp up was at the core of my buy rating and thus it was very positive to see management follow through with a generous reward. After being combined with their routine quarterly dividends, they made dividend payments of $2.464b during the first half of 2022 and whilst this was technically $124m higher than their free cash flow of $2.34b, this was only due to their working capital build of $494m.

Even after boosting their routine quarterly dividends to $1.19 per share, these should still only cost $1.552b per annum given their latest outstanding share count of 326,206,003 and thus working capital build or not, they clearly should have no issues maintaining very strong coverage. In theory, this also implies that further special dividends are coming but despite this very exciting development, their dividends barely received any mention during their second quarter of 2022 results conference call, as per the commentary from management included below.

“After generating $1.6 billion in cash from operations during the second quarter, we returned $2.1 billion to shareholders through a $5.20 per share special dividend, a 5% increase to our quarterly dividend that paid another $1.19 per share, all while repurchasing 45 million of our shares during the quarter.”

-LyondellBasell Q2 2022 Conference Call (previously linked).

After reading literally hundreds of earnings call transcripts, anecdotally speaking, normally a company declaring a very large special dividend for the first time sees management discuss their shareholder returns policy. Or alternatively, they would see questions from analysts seeking clarification, yet oddly neither transpired and thus in my eyes, it leaves a lack of communication from management that makes it difficult to provide thoughts on their shareholder returns. Despite this drawback, at least they seem intent on rewarding their shareholders with this representing a very positive start that will hopefully see more continue as their financial position remains in great shape.

Author

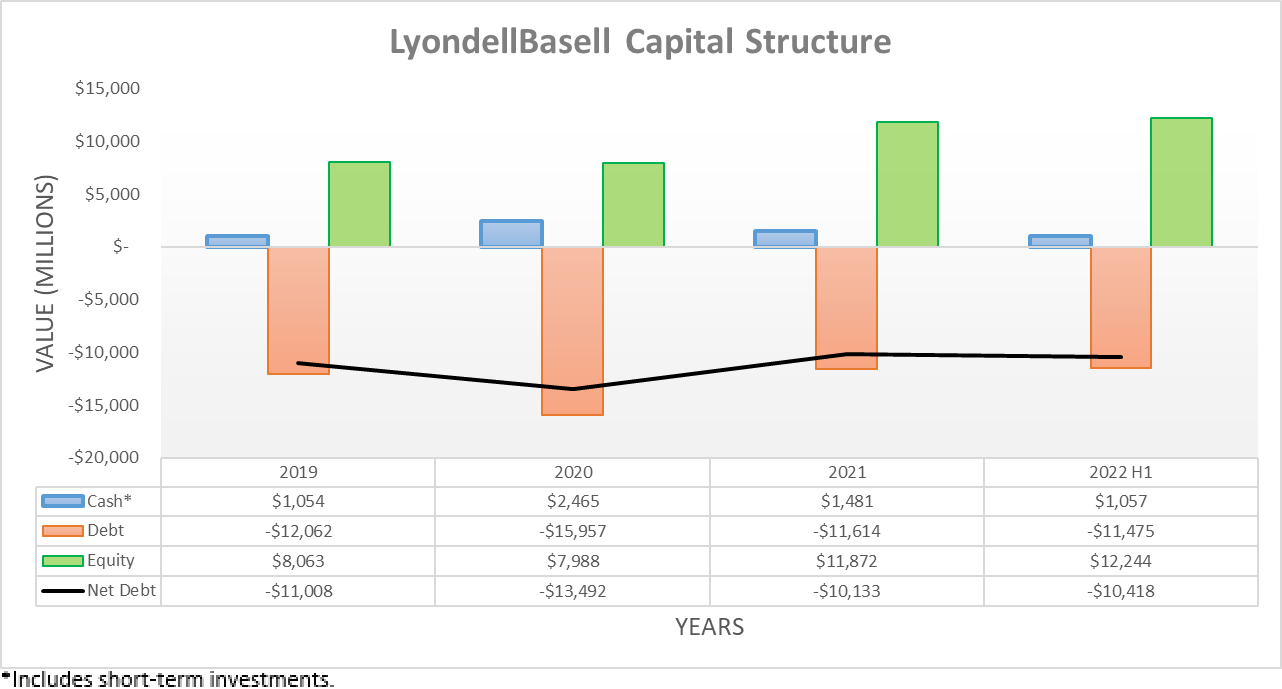

After funding their very large special dividend during the second quarter of 2022, it saw their net debt revert higher to $10.418b after dipping to $9.539b following the first quarter, which is consistent with their earlier stated intention not to deleverage any further, as per my previously linked article. Whilst now technically higher than the $10.133b where it ended 2021, if not for their modest working capital build of $494m during the first half of 2022, their net debt would have otherwise still been slightly lower at $9.924b. Despite the lack of discussion regarding future shareholder returns, as nothing was released nor discussed that indicates they will change course, it implies more generous shareholder returns are very likely inbound and thus as a result, their net debt should stay broadly unchanged at around $10b.

Author

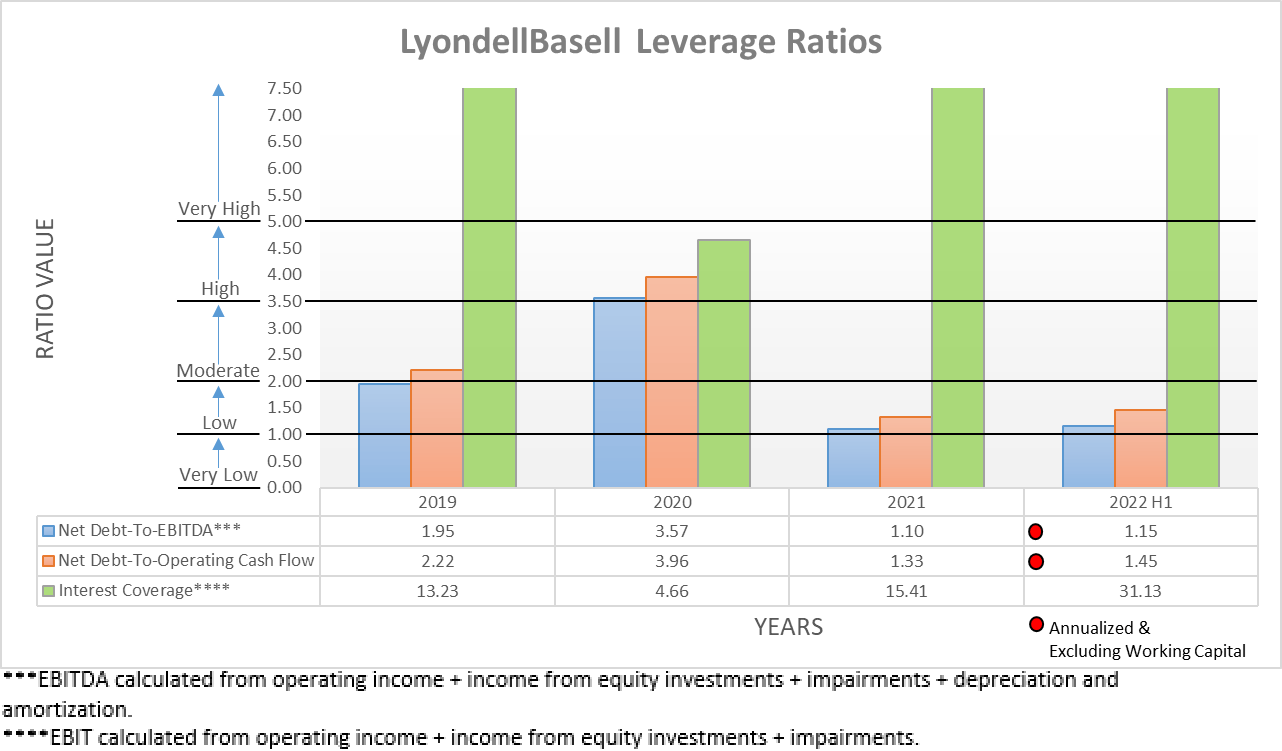

Despite seeing their net debt climb higher during the second quarter of 2022, their leverage remained broadly steady with their respective net debt-to-EBITDA and net debt-to-operating cash flow at 1.15 and 1.45, versus their respective results of 1.19 and 1.56 when conducting the previous analysis following the first quarter. This remains an open and shut case of low leverage with these results sitting comfortably within the applicable range of between 1.01 and 2.00. Meanwhile, their interest coverage of 31.13 after the second quarter once again represents another solid improvement versus its previous result of 23.47 after the first quarter, which is now slightly more than double its result of 15.41 at the end of 2021 and thus the prospects of higher interest rates are no reason for concern.

Author

A similar story to their leverage is shared when turning to their liquidity with their current ratio of 1.68 broadly steady after the second quarter of 2022 versus its result of 1.76 when conducting the previous analysis following the first quarter. Whilst their cash ratio dipped to 0.14 versus its previous result of 0.24 across these same two points in time, overall, their liquidity remains strong, especially given their operational size. Since they are one of the largest chemical companies, they should always retain superior access to capital markets to easily source liquidity if required, such as refinancing any future debt maturities, even if central banks further tighten monetary policy.

Conclusion

Even though it was strange to see no discussions surrounding their very large special dividend nor path for future shareholder returns, thankfully their low leverage and strong liquidity create a powerful backdrop for returning cash to their shareholders. Even though their lacking communication might hold their share price back slightly, at least their actions have still been very positive and mark a new era for dividends and thus it should not be a surprise that I believe maintaining my buy rating is still appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from LyondellBasell’s SEC filings, all calculated figures were performed by the author.

Be the first to comment