Aurore Kervoern/iStock Unreleased via Getty Images

My last article about LVMH Moët Hennessy – Louis Vuitton SE (OTCPK:LVMHF) was published a little more than a year ago in January 2022 and while the S&P 500 (SPY) – and many other indices – are nowhere close to the levels they were at the beginning of 2022, LVMH is trading almost at all-time highs and clearly outperformed the S&P 500.

And while my sell rating proved to be correct for a few months, the stock is now trading 4% higher while the S&P 500 is trading about 14% lower. I still think that LVMH is too expensive to be a good investment, but we must acknowledge the impressive performance of the company and will begin with the recently announced full-year results for fiscal 2022.

Annual Results

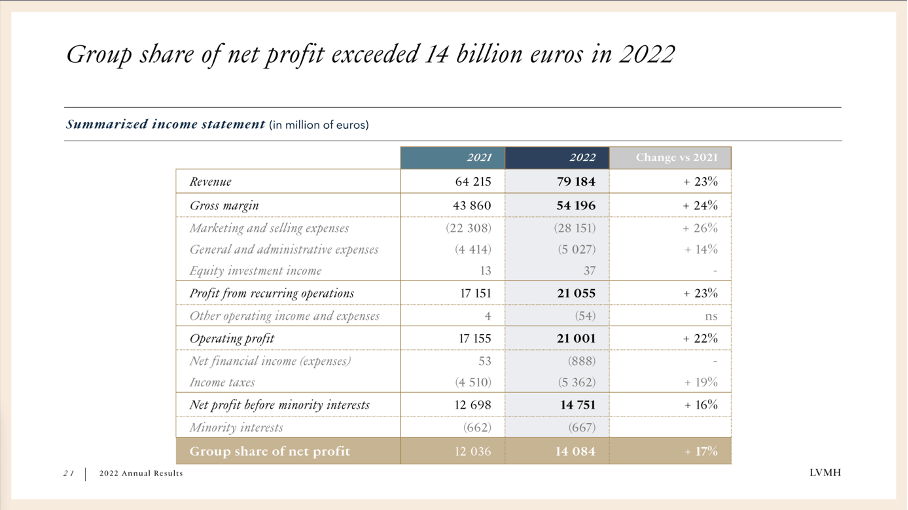

On January 26, 2023, LVMH reported full-year results for fiscal 2022 and while many other companies are already showing signs of slowing down, LVMH is still firing on all cylinders and reporting impressive numbers. In fiscal 2022, LVMH generated €79,184 million in revenue and compared to the previous year in which the company generated €64,215 million in revenue, this is an increase of 23.3% year-over-year. And while currency effects contributed about 6% growth, organic growth was 17%. Operating profit increased from €17,115 million in fiscal 2021 to €21,001 million in fiscal 2022 – resulting in 22.4% year-over-year growth. And earnings per share increased 17.3% YoY from €23.89 in fiscal 2021 to €28.03 in fiscal 2022.

LVMH Fiscal 2022 Presentation

Only operating free cash flow declined from €13,531 million in fiscal 2021 to €10,113 million in fiscal 2022 – reflecting a decline of 25.3% year-over-year. And although free cash flow is one of the most important metrics it is also a metric with higher fluctuations (even in case of great businesses).

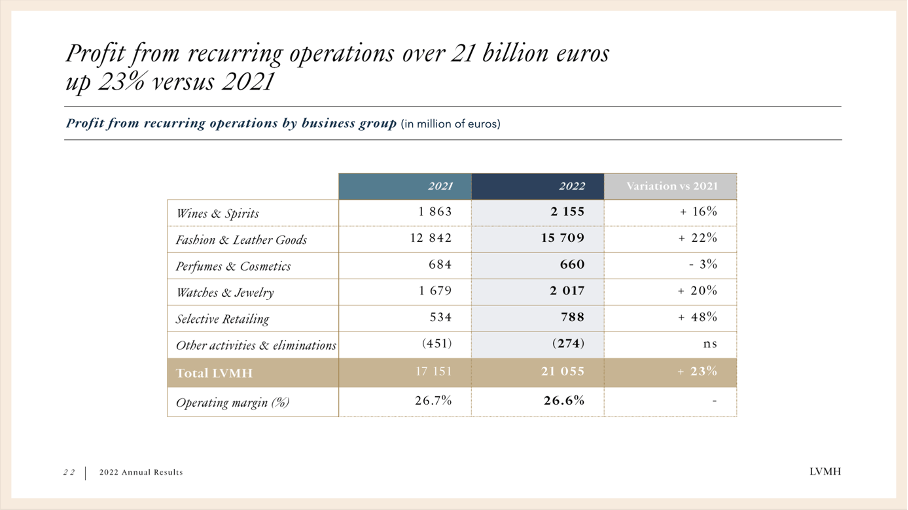

When looking at the different segments, all five contributed to revenue growth. Fashion and Leather Goods, which generated €38,648 million in revenue and was therefore responsible for almost half of the company’s revenue, could also report one the highest growth rates – 25% reported growth and 20% organic growth. Only “Selective Retailing” which generated €11,754 million in revenue reported a higher growth rate of 26% YoY (however organic growth was “only” 17%). The other three segments – “Wines and Spirit”, “Perfumes & Cosmetics” as well as “Watches & Jewelry” – could report growth rates between 17% and 19%.

LVMH Fiscal 2022 Presentation

Of course, all five segments are contributing to operating profit. However, not all segments are reporting similar growth rates or similar operating margins. The most important segment is once again “Fashion & Leather Goods” which could grow operating profit 22% and is responsible for 75% of the company’s total operating profit. “Selective Retailing” could grow operating profit 48% year-over-year, but the segment has a rather low operating margin of only 5.3% right now.

Dividend

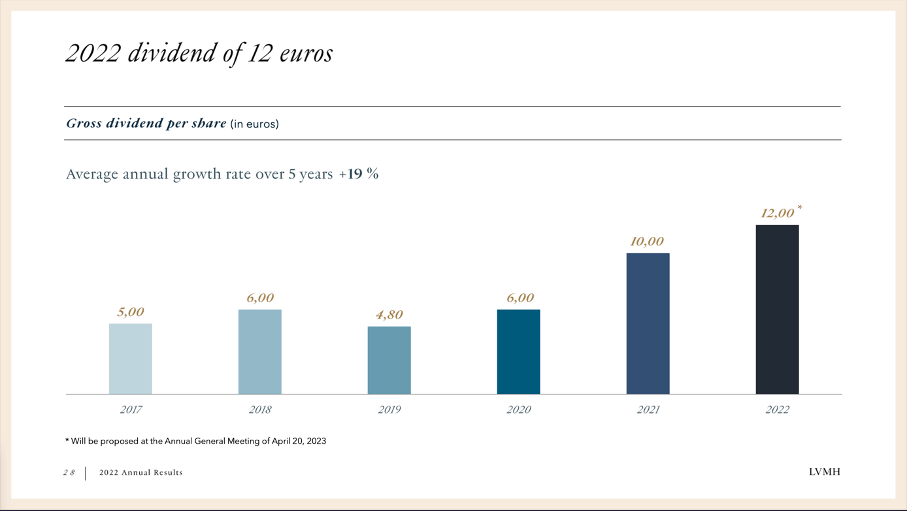

LVMH also announced a final dividend of €7.00 for fiscal 2022 and combined with the interim dividend of €5.00 the total dividend for fiscal 2022 is €12.00. Compared to a dividend of €10.00 in the previous year this is an increase of 20%. And in the last two years – between 2020 and 2022 – LVMH actually doubled its dividend.

LVMH Fiscal 2022 Presentation

When taking the earnings per share of fiscal 2022, we get a payout ratio of 43% which is acceptable and leaves room to increase the dividend further in the years to come. Of course, with a dividend yield of 1.5% it is a “nice-to-have” but most likely not the reason to invest in LVMH.

Are Current Growth Rates Sustainable?

When talking about the fiscal 2022 results and high growth rates we should not ignore that these strong results are coming on top of an already impressive fiscal year 2021. But despite all excitement about these high growth rates, we should not get carried away. When looking at longer timeframes we must realize that the growth rates in the last few years are rather an outlier – this is true for LVMH’s growth rates as well as the growth rates for the entire industry.

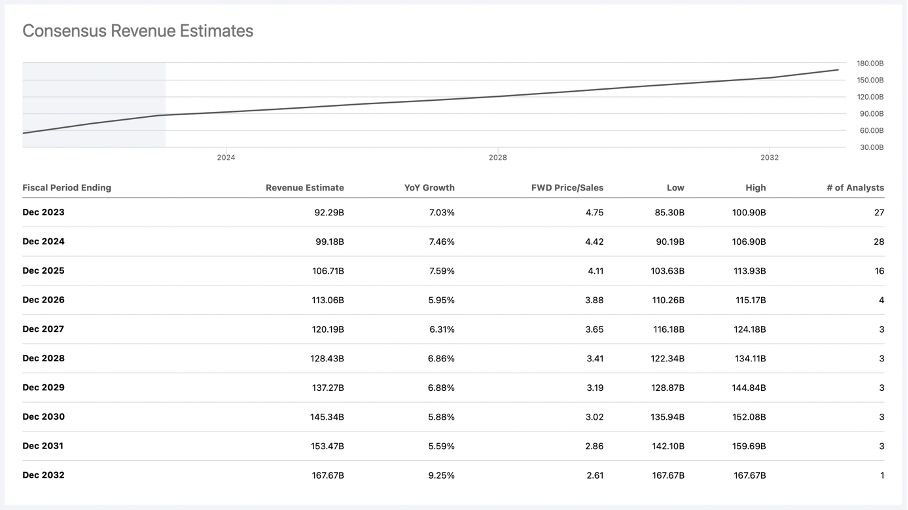

And when we look there are several hints that these high growth rates will probably not last. We could start with analysts’ expectations in the years to come. In the next ten years, analysts are expecting LVMH’s revenue to increase with a CAGR of 6.88%, which is still a high growth rate but clearly below the growth rates the business could report in the last few years.

LVMH Revenue Estimates (Seeking Alpha)

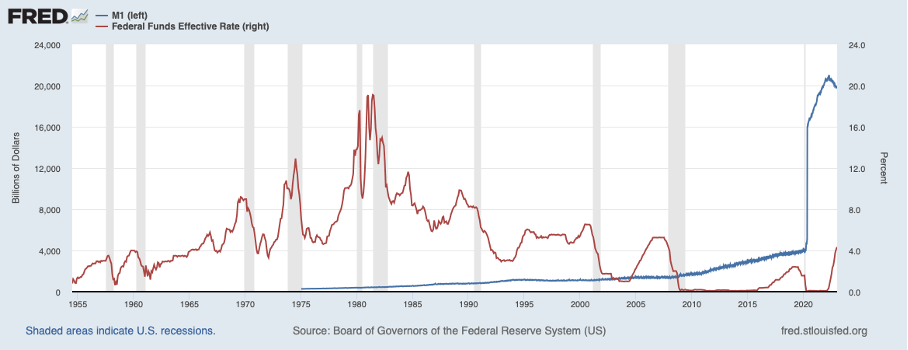

We should also not forget what contributed to these high growth rates in the last few years – the same reason that led to extreme high asset prices (including extremely high stock prices): low interest rates and billions of dollars (and euros) pumped into the economy. These extreme amounts had to find its way and the money flows into different assets were visible by exploding prices for stocks, real estate as well as luxury goods.

FRED

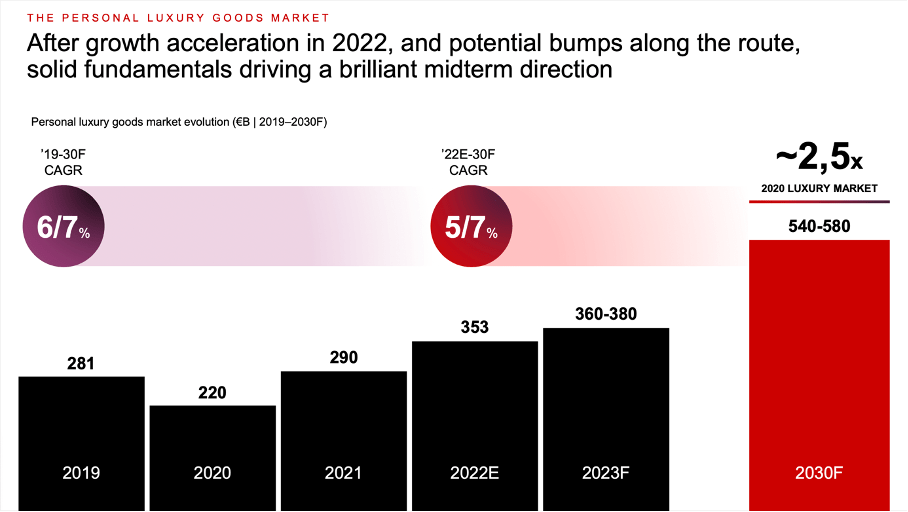

And although it seems likely that interest rates will be lower again in the next few years, M1 is already declining, and liquidity could dry up in the coming months. Bain & Company is also seeing potential bumps along the route but expects the luxury goods market to increase with a CAGR of 6% over the next seven to eight years and reach a market size of $540 billion to $580 billion in 2030.

Bain & Company Luxury Goods Study

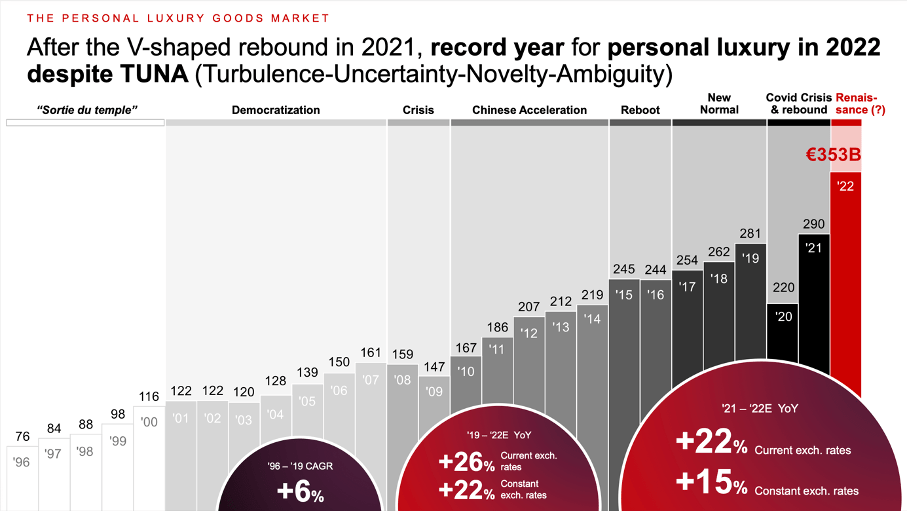

These growth expectations are also in line with the long-term growth rates of the luxury goods market. Since 1997, the luxury goods market was growing with an annual growth rate slightly above 6%.

Bain & Company Luxury Goods Study

And when looking at these growth numbers we must see that fiscal 2021 and fiscal 2022 are definitely outliers with extraordinary high growth rates and the likelihood of repeating these growth rates in the years to come is low.

When looking at LVMH’s performance during the same timeframe (since 1996) the company could grow earnings per share with a CAGR of 12.25%. And we can see that LVMH outperformed the market and grew with twice the pace as the overall market did. It is certainly reasonable to make the argument that LVMH will outperform once again in the years to come and grow with a higher pace than the overall market.

Recession

But when talking about the years to come and growth potential, we should also keep in mind that the global economy might be headed for a recession in the next few quarters – despite investors obviously getting more optimistic once again (but the extreme greed is just another warning sign). When looking at several early warning indicators, the alarm bells are ringing in my opinion. Not only have we a steeply inverted yield curve (see 10-year vs. 2-year as well as 10-year vs. 3-months), but we also have declining housing permits. Additionally, the United States ISM non-manufacturing PMI declined below 50 in December 2022 (however, we saw a strong rebound in January 2023). Of course, other indicators are still signaling a strong economy – like the labor market with extremely low initial unemployment claims (but the labor market is always lagging a bit).

In my opinion, there is little doubt that we are heading towards a recession, but as I pointed out in my last article, LVMH proved to be rather resilient in case of a recession:

LVMH is a very stable business for the reasons mentioned above, but it is also pretty recession-proof (when ignoring 2020). During the 2001/2002 recession LVMH was able to increase revenue constantly although growth slowed down. In 2001, revenue grew 5.6% and in 2002 revenue grew 3.8%. During the financial crisis, the development was similar: LVMH was able to increase revenue by 4.3% in 2008, but revenue declined a little in 2009 (0.8% decline).

Even when LVMH will avoid a steep drawdown in case of a recession, we should not assume LVMH will be able to increase with a similar pace it has in the last few years. And when looking at the performance of the luxury market during the Great Financial Crisis, declining numbers in the single digits seem likely.

Intrinsic Value Calculation

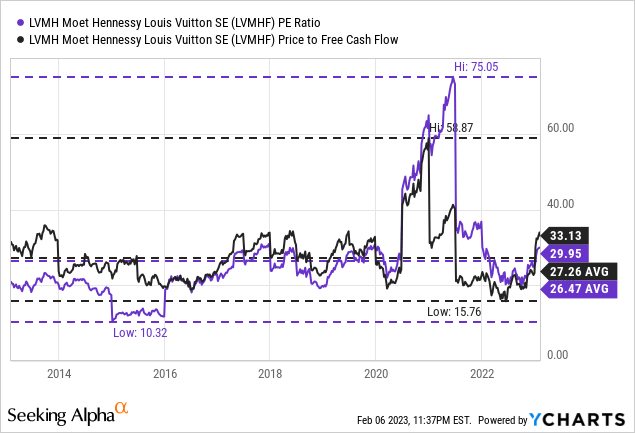

I already mentioned above that LVMH is still trading for rather high valuation multiples. At the time of writing, LVMH is trading for a P/E ratio of 30 as well as a price-free-cash-flow ratio of 33.1. And not only is the stock trading above the 10-year averages (average P/E ratio is 26.47 and average P/FCF ratio is 27.26), but when excluding the high valuation multiples during the COVID-19 crash, LVMH is trading for one of the highest valuation multiples in the last ten years.

When considering the extremely high growth rates LVMH is reporting, high valuation multiples are also not surprising. Nevertheless, I am not quite sure if these valuation multiples are justified. We can also calculate an intrinsic value for LVMH by using a discount cash flow calculation. And when using the free cash flow LVMH reported for fiscal 2022 (€10,113 million) and assume a discount rate of 10%, the company must grow 13% annually for the next 10 years followed by 6% growth till perpetuity in order to be fairly valued (calculating with 502.5 million outstanding shares).

When looking at past growth rates of LVMH, future growth rates of 13% should in theory be possible. In the last ten years, earnings per share grew with a CAGR of 15.18% and in the last five years earnings per share grew even with a CAGR of 22.45%. But when calculating with more cautious growth rates, LVMH seems to be overvalued. If LVMH can grow only 6% – in line with the market – the intrinsic value for the stock would only be $503.64.

But when looking at the growth rates LVMH could report in the last 2.5 decades (compared to the industry), we can assume that LVMH will be able to outperform the industry in the years to come. I think we can be more optimistic and assume a growth rate of 10% in the next ten years (combination of overall market growth, LVMH gaining market shares, improving margins and maybe share buybacks). Of course, this is not including the negative impacts of a potential recession, but let’s be optimistic and assume LVMH will perform quite well. When calculating with these assumptions and once again 6% growth till perpetuity, we get an intrinsic value of €668.46 for LVMH.

Conclusion

Although LVMH is without any doubt a great company, I still don’t think the stock is a good investment. And although I assigned the stock a “Sell” rating once again, I would not short the stock. Not only do I short very seldom. Even if I would short a company, it would most likely not be a high-quality business like LVMH.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment