style-photography

Lumen Technologies, Inc. (NYSE:LUMN) reported Q4 2022 results yesterday, and markets are not happy. The actual performance, albeit showing continued, annoying declines, was more or less in line with what the up-to-date investor should have expected from a company like Lumen in the current macroeconomic climate.

The problem is that ever since CEO Jeff Storey left and the company took a new direction, starting with eliminating the dividend, management policy has become an issue. They are pushing with CAPEX and OPEX when all anyone wants is the company to stay its course, even if it is in managed decline, and to pay the dividend that it used to have. No one is buying Lumen thinking it’s a tech company, and management waffling about the proposed transformation comes across as tone-deaf. Lumen’s assets are undervalued, more so than before, but the mode of return needs to be a dividend when more asset sales like of Lumen’s ILEC business can’t be expected in the current sponsor environment.

Lumen Technologies Q4 Earnings

The thing about these LUMN Q4 results is they are not that terrible. Yes, Lumen Technologies, Inc. continues to see declines (adjusting for the divestitures), but the legacy voice exposure cannot be escaped. Investors know that these will continue to drag heavily on results until these revenues inevitably vanish from the mix. While some more legacy assets were gotten rid of in asset sales a couple of years ago, voice is still regrettably important in the mix.

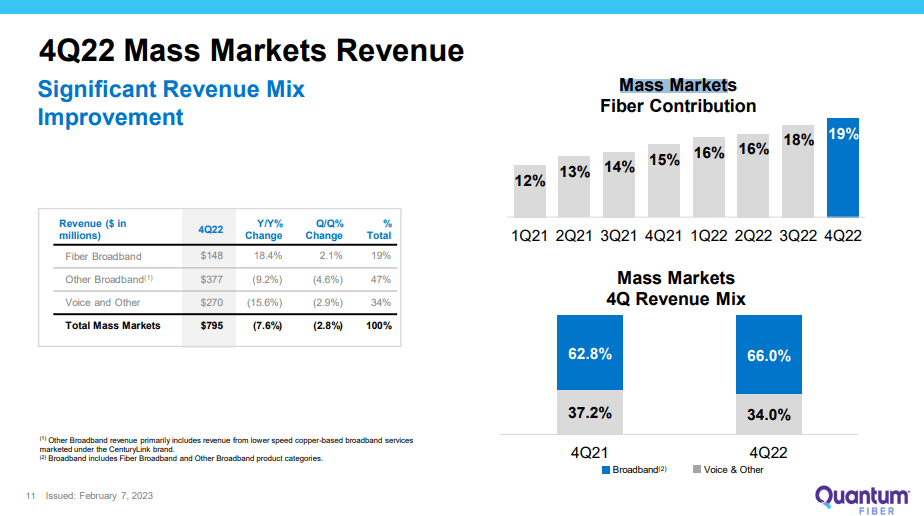

Mass Market (Q4 2022 Pres)

The 16% decline YoY in voice is consistent with what we’ve seen even back in 2019. The declines are compounding at this rate, and these exposures are shrinking in the mix.

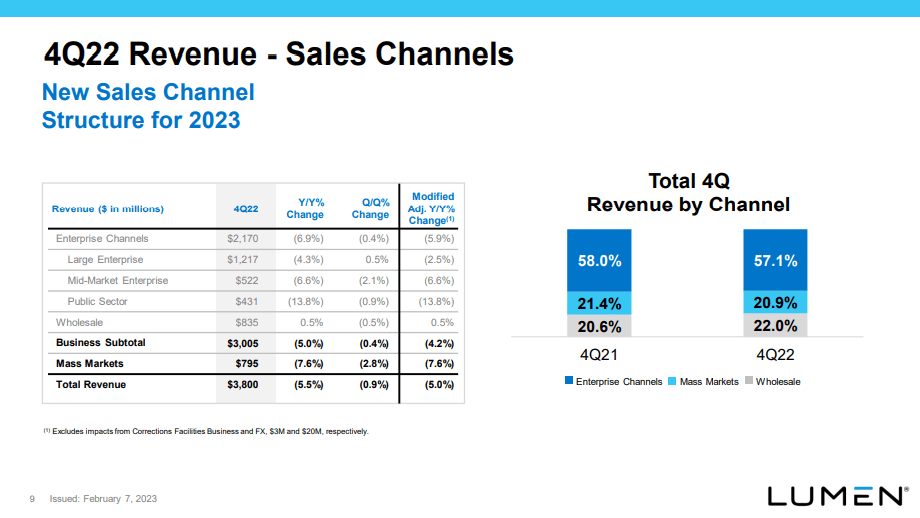

Business + Mass Market Revenues (Q4 2022 Pres)

The same effects can be seen in the enterprise segments, which feature even more voice exposure. The public sector was primarily hit by these declines as well as declines in VPN, although a failure to win a contract renewal did have about a 1.5% impact on the total declines, so more or less 10% of the declines.

The failure to renew the contract, although not a particularly large part of the explanation for the public sector declines, does help illustrate why the market could not have expected a turnaround at this point in time. Lumen sells commodified services. Certainly, IP transit is a commodified service, but even generally the selling of broadband or any kind of connectivity services is going to be competitive, and when customers are analyzing budgets, especially in mid-market enterprise, the competition gets even more ferocious as providers try to keep the cash flows. Some declines, whether in the pricing of connectivity services or in the total number of customers engaged, should be expected.

The Quantum Fiber project apparently saw a bit of a slowdown in rollout as the company maintained discipline. Lumen has been good on making sure it gets IRR on its rollouts, and we think this is more or less positive, however competitors that are less disciplined could just come in and drive down capital costs. This is a structural problem for a marginal players’ fiber rollout, but where working in more regional markets makes them more sensitive to macro pressures, it also reduces these competitive risks. On the FY results, the Quantum Fiber growth created an appreciated offset to declines.

The deleveraging continues, and this has always been appreciated by investors especially now that rates are higher.

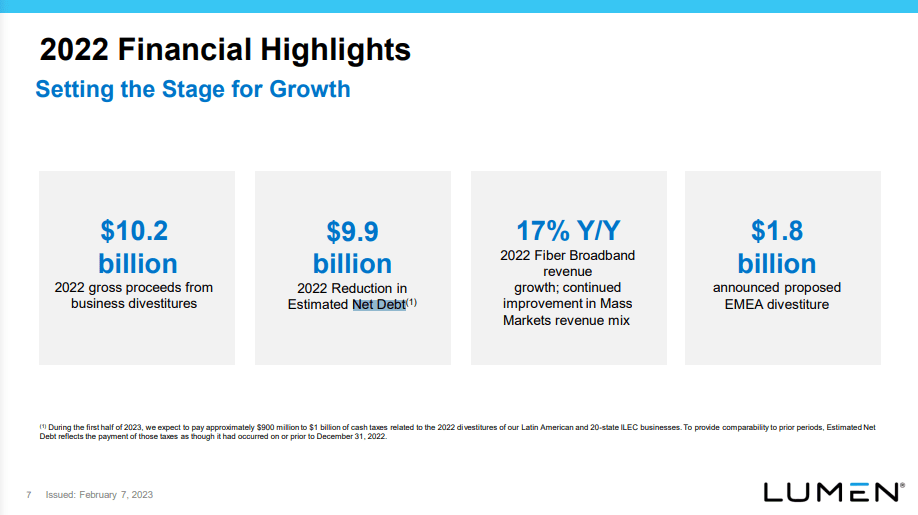

Highlights (Q4 2022 Pres)

Outlook

So far, there’s good explanations for the current performance and the deleveraging is notable, which in the grand scheme of things is positive considering the rate cycle. The problem is that Lumen Technologies, Inc. management is saying things like the following:

As Kate discussed, over the next couple of years, we will be aggressively investing both OpEx and CapEx to position ourselves for long-term sustained success.

And it shows in the CAPEX guidance which is forecast to grow 10% from just new efficiency pushes. CAPEX could end up growing close to 20% in 2023. Finally, there are OPEX increases expected, and those dedicated to optimization alone will shrink EBITDA by 5%. Organic declines have to be expected, but a 5% decline from vague optimization programs are not very appreciated. Moreover, the divestitures are apparently causing profit headwinds in corporate overhead that in management’s words are “not going away,” so these are not one-offs.

Especially regarding the discretionary costs and investments, this is definitely not what investors want to hear, and it reflects on the apparently unwanted direction that management is taking the company starting with the dividend cancellation. Lumen investors would have been enticed by two things: the low multiple and the high dividend. It was simple – we all saw that this was a business that had components that were in decline, but the profits and free cash flow (“FCF”) generation were phenomenal, and the dividend, which would have been around 20% in yield at current prices, was actually a payout that would be sustainable for a while with FCF and EBITDA even after divestitures, where many of their businesses required no CAPEX, not even maintenance CAPEX.

Without the dividend, investors are going to have to bet on success of the current management, whose comments on culture, and vague promises of becoming customer centric and focused give the impression that they believe it is possible to transform Lumen into some sort of comprehensive tech provider, with some CDN and edge technologies here, colocation services there, and of course their wireline and in premises connectivity. Buybacks are not tangible enough of a payout since we still need to bet on the company future for them to payoff.

The sustainable dividend payout rate was absolutely a sufficient mode of return for a business in managed decline. Take a page out of Imperial Brands’ (OTCQX:IMBBY) book, or other businesses in coal which are in inexorable decline. Pay dividends and die slower than the market expects; last that one extra round. At least Lumen had segments that would keep things going longer, and there was even a case for IP transit staving off secular declines, despite being a commodity, that we laid out some years ago. They were comparatively well-positioned compared to businesses facing a government axe.

Remarks

Honestly, Lumen Technologies stock’s multiple remains shockingly low in EV/EBITDA, and the assets are probably undervalued. They have assets that are worth more than those they sold to PE, but the capital return actually mattered here, especially with business confidence being so low. You’d rather not see the earnings reinvested where promised business results were never delivered. Lumen Technologies, Inc. investors would have been fine with a continued caretaker management strategy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment