Sundry Photography

I maintain two 25-position, equal-weight dividend growth portfolios for my personal investing goals, one with an offensive orientation (my “Ultra High DGI” portfolio) and one with a defensive orientation (my “Defensive DGI” portfolio). Each portfolio has been painstakingly constructed and backtested to maximise risk-adjusted returns and dividend growth based on its respective aim, with the defensive portfolio seeking to minimise drawdowns during difficult periods and thus be as “recession-proof” as possible, and the offensive portfolio seeking to maximise long-term dividend and capital growth.

This article marks the second entry for my Ultra High DGI Portfolio, where I’ll be covering Lowe’s Companies, Inc. (NYSE:LOW) to determine whether it presents a good value for investors at current levels.

LOW: One Of The All-Time Best

In terms of “no-brainer” additions to my Ultra High DGI Portfolio, which primarily aims to maximise quarterly dividend income until retirement (about 20 years for me), LOW was probably the first and easiest choice. Aside from enjoying an effective duopoly in the home improvement market with Home Depot (HD), which tends to be a great situation for the businesses that have it — Mastercard (MA) and Visa (V) come to mind — its dividend growth record is truly second-to-none.

Founded in 1921, LOW has paid a growing dividend for 61 years, making it one of just 48 stocks to achieve this feat. Not only that, but it has maintained an exceptionally high dividend CAGR over that time, with its last two dividend hikes coming in at over 30% each. As a dividend nerd I could go on and on about how impressive LOW’s dividend is, but the easiest way to illustrate it is to look at what this kind of compounding can achieve over time.

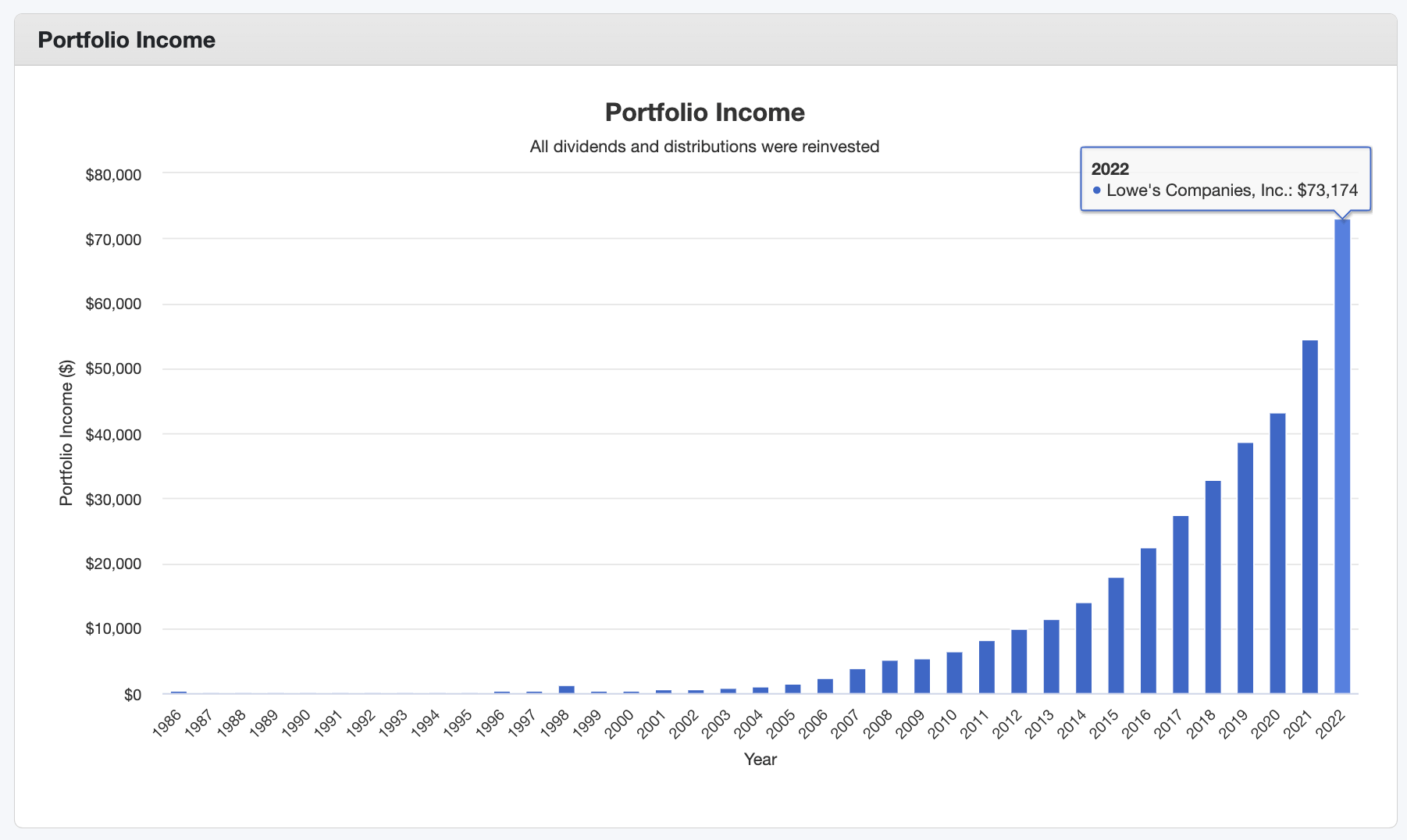

portfoliovisualizer.com

The chart above shows that $10,000 invested in LOW in 1986 with dividends reinvested would currently yield over $70,000 in annual dividend payments. Talk about wealth compounding — from the dividend alone, you’d be receiving the equivalent of a full-time salary and paying more in taxes each year than your entire original investment! And that’s to say nothing of the nearly $4 million total return that $10,000 would have produced. That is one tax bill I think any investor would welcome.

The Current Outlook Is Murkier

For the rest of us mere mortals who are contemplating starting a new position in the company today, the decision might appear a bit more complicated than the chart above suggests. Times have changed, and Lowe’s is now a corporate behemoth with relatively little room for geographic expansion remaining domestically given its own footprint of nearly 1750 stores and that of the larger Home Depot with 2300 stores across the US, Canada, and Mexico.

The macro picture is also bleak, with falling home prices and high interest rates leading builders to postpone new starts and homeowners to postpone renovation projects. Anecdotally, several of my own friends are pushing project start dates back to 2024 in hopes of rates falling, ranging from home improvement to rental developments. As Raymond James analyst Bobby Griffin recently remarked about Home Depot’s declining transactions:

While we are not forecasting a significant correction in earnings, we are concerned that transactions could remain negative in 2023, leading to comparable sales pressure, especially as inflation tailwinds to comps abate some. In addition, any potential decrease in home prices could hinder consumer’s perceived return on investment in their homes following several years of record spend in the category.

Furthermore, like most old, large, slow-growth companies, Lowe’s is now hyper-focused on growing its earnings and expanding its margins, and recently sold its entire Canadian business to private equity group Sycamore Partners for what appears to be almost nothing, in large part because it was a drag on the company’s margins. The murky deal announcement left out details about “performance-based incentives” that will hopefully be revealed with time and left many investors scratching their heads as to why 7% of Lowe’s topline was essentially being written down. Most likely, Lowe’s succumbed to the difficulty and costliness of the Canadian market, and their store network there simply wasn’t profitable enough and/or was actually running at a loss. On top of this, LOW’s revenue growth has completely stalled out in 2022, with comparable sales expected to be down 0-1% YoY.

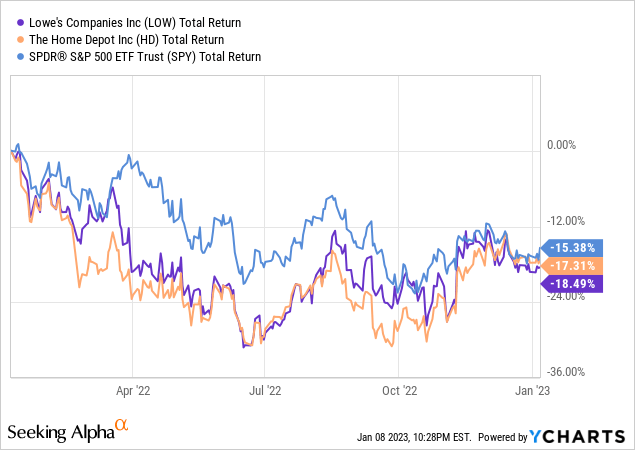

To round out the bad news, LOW’s shares are down 18.5% over the past year, slightly more than both HD and the S&P 500 (SPY), although LOW is still far ahead of both in 3- and 5-year returns.

Despite all of the doom and gloom, Lowe’s delivered a beat-and-raise Q3 earnings report showing 2.4% YoY topline growth and projected 2022 share buybacks of $13B, particularly massive compared to their current $121.5B market cap. Perhaps less surprising given the level of repurchases, 2022 EPS estimates were also raised significantly to between $13.65 and $13.80 versus the analyst consensus estimate of $13.53. Pro Supply revenues continue to be the leading growth area at 19% YoY growth, online sales grew 12%, and US store comps were actually up 3%, lending credence to the idea that divesting its Canadian operations may help sales comps in 2023.

Dividend Strength

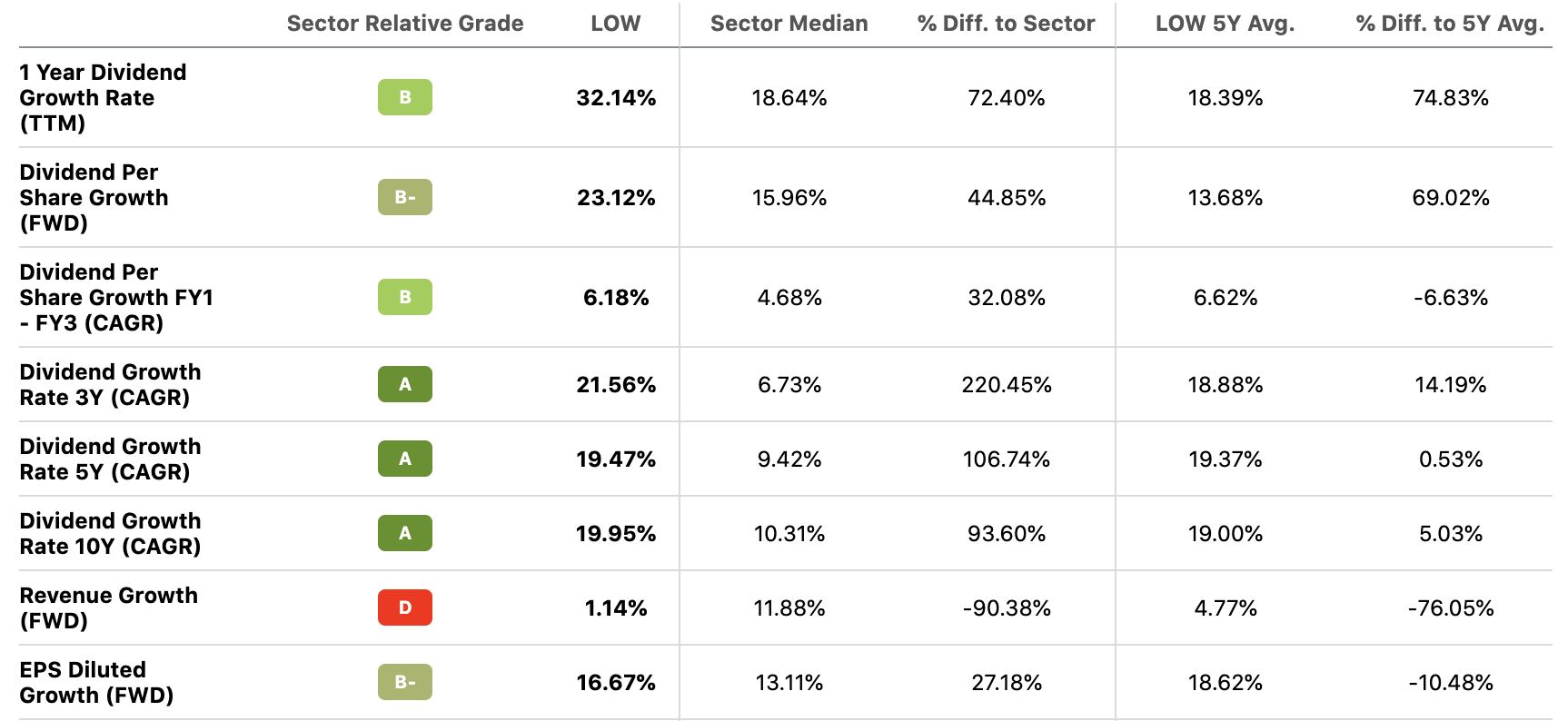

In other good news, Lowe’s dividends continue to be stronger than ever, with the company maintaining a low payout ratio of 36%, slightly less than HD’s payout ratio of 46% even when adjusted for HD’s higher yield of 2.39%, a current yield of 2.09%, which is over 18% higher than its 5-year average yield of 1.77%. Most importantly, unlike other DGI stalwarts that have been engaging in huge buybacks while cutting their dividend growth rate, LOW’s continues to hike their dividend at a 20%+ rate, with a 2-year dividend CAGR of 32% and 3-year CAGR of 21.56% versus their 10-year CAGR of 19.95%.

Seeking Alpha

Top line growth may have stalled, but the company is returning more cash than ever to shareholders. A 2.09% yield may not seem like much on its own, but when combined with LOW’s long-term 20%+ dividend CAGR it has tremendous compounding potential. In fact, LOW shares have only yielded more than 2% a few times in the past 20 years. Based on its yield alone, LOW appears to be a strong buy at current levels.

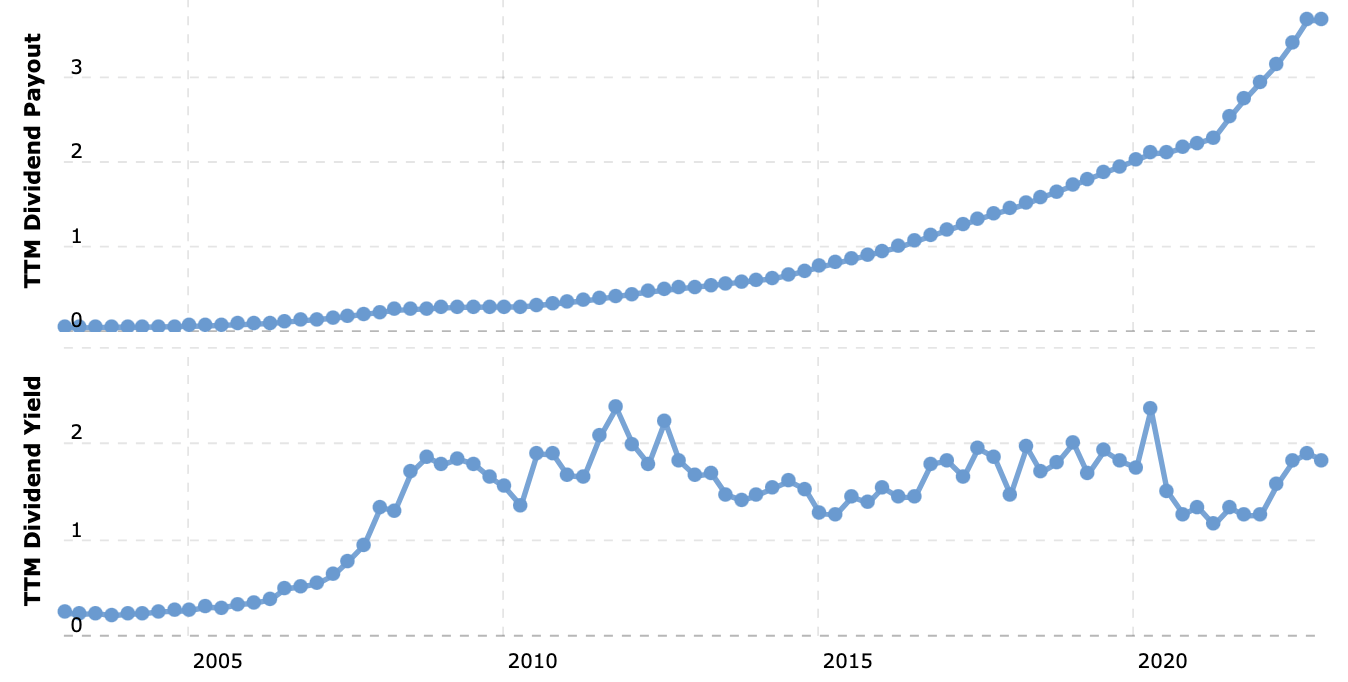

macrotrends.com

Valuation

LOW’s current valuation shows that the stock is trading at a discount to its historical levels as well:

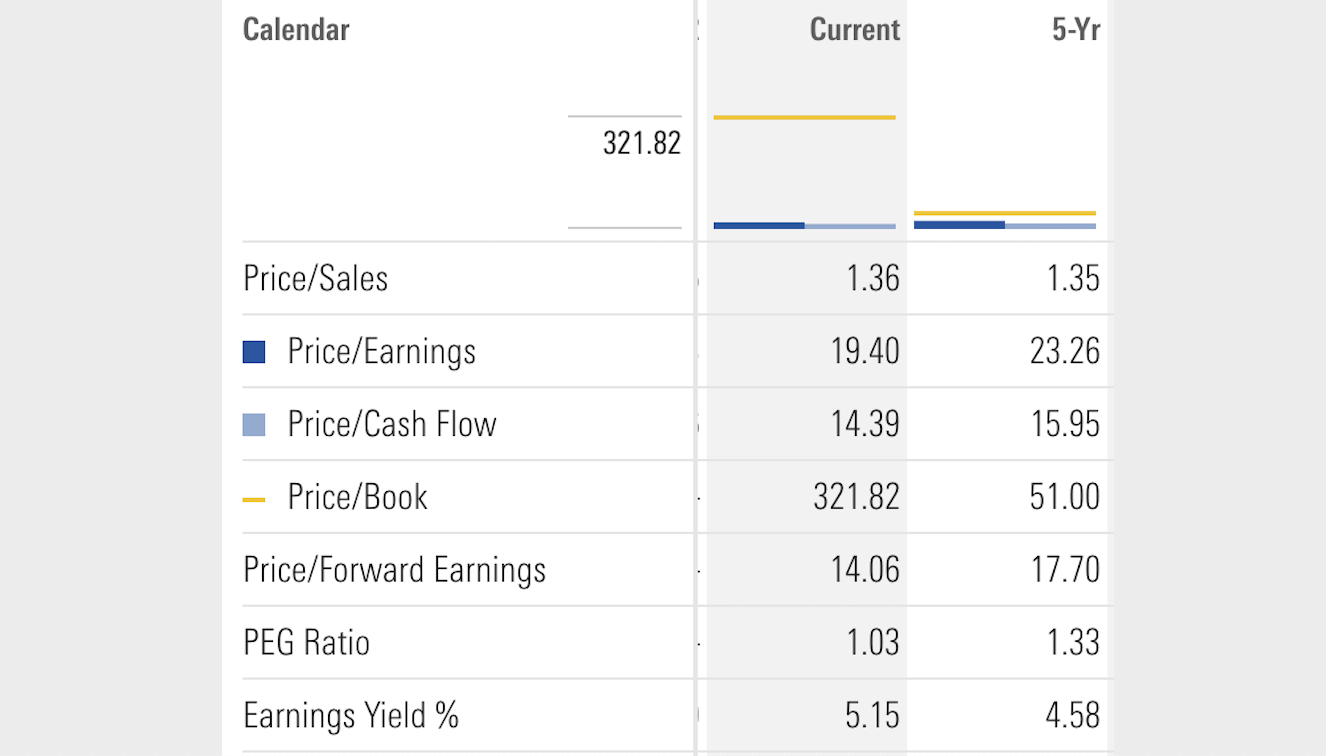

LOW Current vs 5-Yr Valuation (Morningstar)

While its Price to Sales ratio of 1.36 is in line with its 5-year average of 1.35, on an earnings and cash flow basis it appears 10-30% undervalued.

Since we’re in such a different macro environment now than we’ve been in for most of the last five years, with higher rates and a particularly weak housing market outlook, I think we have to assume that a home improvement and building materials retail stock — even one of LOW’s caliber — deserves a lower multiple than it was afforded during the COVID-influenced housing market and home improvement boom from 2020-early 2022.

So although Lowe’s yield is historically high and its earnings-based valuation metrics are historically low, personally I view shares as fairly valued at these levels given the company’s poor short-term outlook. Buybacks have likely helped to support the share price and certainly helped to boost EPS in 2022, but the stock has been punished along with the overall market and now trades at a level that accurately reflects its risks and rewards, about 23% off its all-time high. Fortunately in Lowe’s case, I don’t need it to trade at a huge discount to feel safe adding shares. For the best DGI stocks in the market, often fair value paired with a historically high yield and/or significant share price drop is acceptable for long-term investors.

Conclusion

Excellent dividend growth stocks don’t go on sale when everything is perfect, nor when things are just OK. You’ll only find deals when the outlook is bleak, either for the company itself or for the market as a whole. With LOW shares down only 18.5% in the past year, essentially in-line with the S&P’s performance, it may appear that all of the bad news has not yet been priced in.

I’m typically of the mind that when everyone and their mother is talking about recession, chances are that much of it has already been priced into the stock market, and seasoned fund managers have already begun taking advantage of depressed share prices and elevated yields. Shares of all economically sensitive companies will likely surge on the heels of further declining job and inflation reports, let alone when the Fed eventually announces an end to rate hikes, and I don’t want to miss the bounce when they do.

So while I agree that 2023 may bring disappointing sales due to the macro environment, and I don’t anticipate a swift recovery for LOW or HD stocks to new highs, I’d argue that LOW’s long history suggests that investors would be wise to add shares whenever the yield exceeds 2%, even in a higher-rate environment. Currently trading around $200, I rate LOW a long-term buy on a fair valuation relative to its murky outlook and its likely temporary negative market sentiment.

Be the first to comment