Sundry Photography

When I first wrote about Lowe’s (NYSE:LOW), it was 2016, and I was concerned about a downturn affecting the business. I ended up opening a position within a year, during a dip in 2017, and it has been a fantastic position to hold in my long-term portfolio.

Seeking Alpha

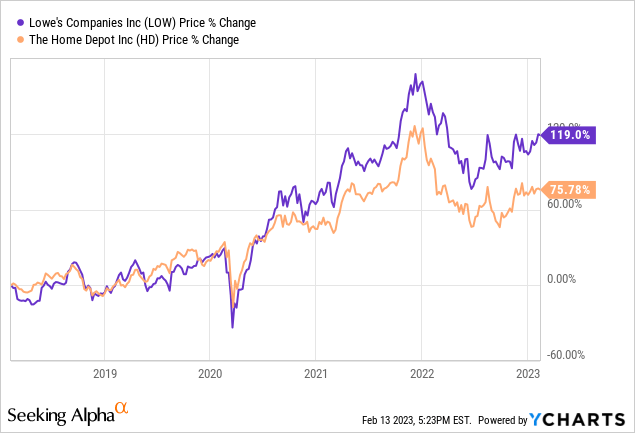

The debate has been well hashed out among investment analysts as to whether to own Home Depot (HD) or LOW over the years. LOW was a perpetual laggard, while HD has had best-in-class metrics. However, LOW has actually outperformed over a shorter time horizon.

The answer to how this happened is LOW had an easier gap to close. HD has continued to execute well, and I wrote on them not long ago. However, LOW was inefficient, and new management in 2018 sunk significant effort into initiatives to modernize the business and improve productivity. This has paid dividends for investors.

Recent Results

In the most recent quarter, results were relatively strong across the board. The company drove 20% earnings growth on an adjusted basis, 3% comparable store comp’s, 54 bps increase in operating margin, and the 10th consecutive quarter of double-digit PRO growth at 16%, which is a key growth vector. Lowe’s.com grew 12%, with about 10% sales penetration, and management is relatively confident on consumer and pro health in the coming quarters. Professional sales is an important metric to monitor for LOW. HD has always maintained a substantial lead with professionals, who are likely to be very loyal to a specific brand that holds their rewards, and drive much higher sales than the average DIY customer.

Management has upped their earnings projection from $13.10-$13.60 per share to $13.65-$13.80 per share for full year 2022 with an operating margin of 13%. This would make the company’s P/E ratio on current year’s earnings about 15.59X, which is well in-line with the company’s historical valuation.

Canadian Operations

As I discussed in my previous article all the way back in 2016, I was concerned about the company’s expansion into Canada with their Rona acquisition. Not long before the Lowe’s announcement, Target had failed pretty spectacularly trying to expand. However, I did think LOW would ultimately be successful in their endeavor and deliver meaningful results from their international expansion. This was partially true. Management has decided to divest itself of all international operations due to the significant expenditures they project would be required to bring them up to par with their home market. Specifically, Canadian stores account for 60 bps of operating margin dilution, and shrank sales by 10.2% in the most recent quarter (with about half of that from the stronger US dollar). The company also incurred a ~$2B impairment charge this quarter. Here’s some additional perspective from the call:

Lowe’s first entered Canada in 2007 and later expanded with the acquisition of RONA in 2016. Over the last few years, we focus on the retail fundamentals of our Canadian operations, which brought the Canadian business to profitability and improved its operating cash flows. However, for this business to achieve the profitability in line with the U.S., significant incremental capital investments would be required to streamline the banners and improve operating margins.

By contrast, we have tremendous opportunity for continued market share and profitable growth in our U.S. home improvement business. This transaction will simplify our business model, improve our operating margins and return on invested capital while enabling us to deliver sustainable value to our shareholders. Brandon will provide details regarding the financial impact of the transaction later on the call.

Risks

Looking at other risks to the company, the housing market and looming highly-discussed recession are likely top of mind for investors. They definitely are for every Wall Street analyst across retail earnings calls. Much like some of the other high-quality retailers I cover, LOW management doesn’t see much to cause concern across the landscape. Here’s some discussion from the earnings call:

And now I’d like to discuss the macro environment and specifically address some misperceptions that I’ve heard about the home improvement market. You’ve heard me talk about this before, but demand drivers for home improvement are distinctly different from those that drive home building. So it’s important not to confuse the two. And as a reminder, at Lowe’s, the three highest correlating factors of home improvement demand are home price appreciation, age of housing stock and disposable personal income.

So let’s start with home price appreciation. Even if there is a broad-based decline in home prices, homeowners currently have a record amount of equity in their homes, nearly $330,000 on average, which remains supportive of home improvement investment. And even in the select U.S. markets where home prices have declined after a particularly steep run-up during the pandemic, we are not seeing any impact to sales; second, the average age of homes in the U.S. is over 40 years old and roughly 3 million more homes built during the housing boom in the mid-2000s, will be entering prime remodeling years by which is a key inflection point for big ticket repairs.

This is one of the key reasons why 2/3 of home improvement spend is nondiscretionary on repair or maintenance projects that cannot be delayed; third, consumer savings are near record highs, while disposable personal income remained strong. And more than 90% of homeowners either own or home or are locked into a low fixed mortgage insulating them from rising rates.

There’s definitely a possibility for a housing market downturn, even a significant one. However, when I’m looking at LOW as a long-term investment, it’s not the first thing I’m worried about. This is definitely something to monitor for the company if you are looking at short-term valuation.

Company Presentation

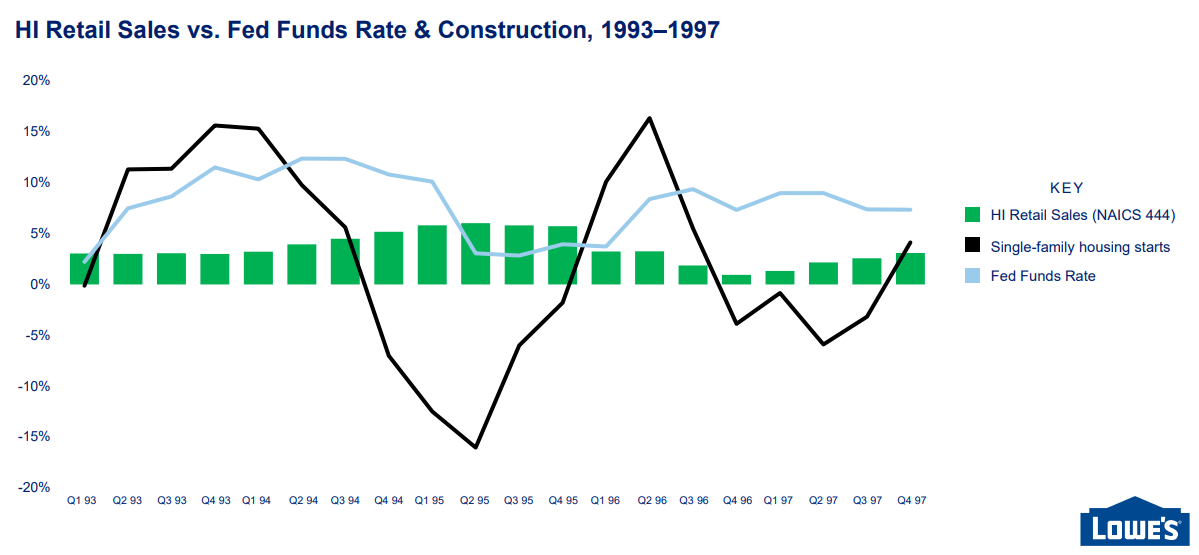

Additionally, I did enjoy this graph from the company’s investor presentation. They are showing the disconnect between new housing starts and home-improvement sales. Note the area in ’95 where sales were much higher during a massive dip in housing.

The housing market has already started to cool, but revenues have remained strong across the retail sector. The risk remains as an overhang, but it’s a short-term concern versus a long-term one.

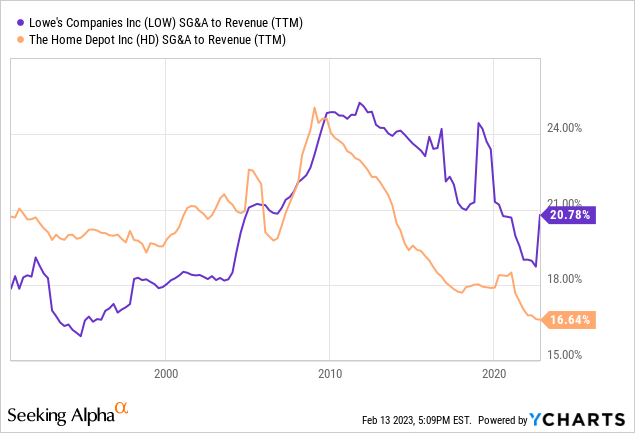

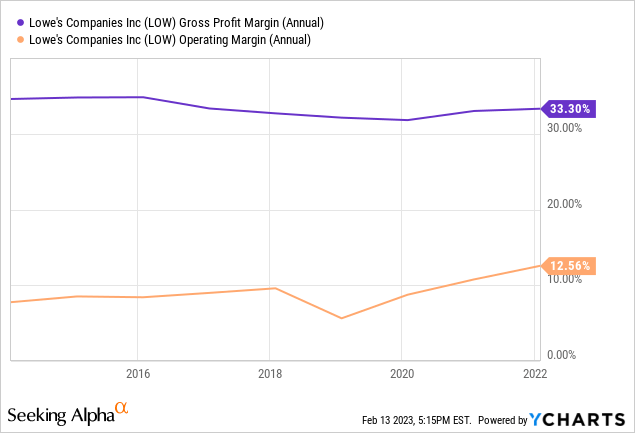

Looking at some numbers for the business, LOW has driven meaningful improvements in its SG&A/revenue metrics over time. The recent blip isn’t on an adjusted basis, and includes one-time charges related to the company’s Canadian write-off. Looking on an adjusted basis, the company is tracking for 18.7% SG&A to revenues. It’s important to look at SG&A expenses as a percentage of sales to track how well a company is maintaining its expenses as it leverages sales growth.

Looking at the comp to HD, it’s obvious why there’s been a valuation gap between the two companies. HD has maintained a lead in this metric, but the gap has closed in recent years.

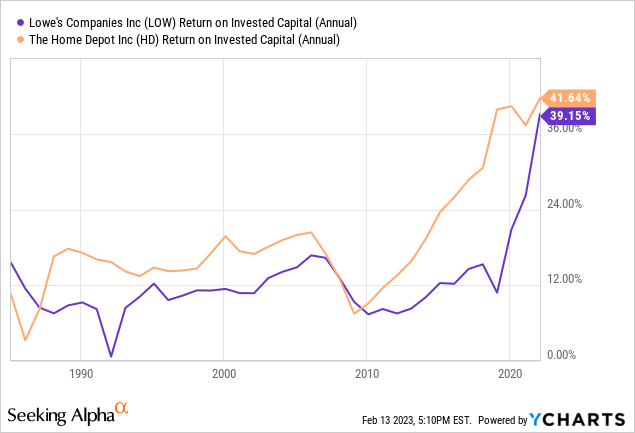

The returns on invested capital are even more markedly different. Note 2019 as an example. The gap between HD and LOW was stark. In the past two years, the company’s initiatives have made up substantial ground, which shows a huge improvement in shareholder value creation and overall profitability. This is absolutely pointed in the right direction and shows excellent execution on management’s cost-saving initiatives.

Looking at margins, gross margin has remained relatively stable over time. The company is projecting an operating margin of 13% in 2022, and international divestitures are projected to drive an incremental 60 bps increase on top of that. Management has invested significant capex in modernizing the company’s tech, right-sizing employee output to improve productivity, and improving the supply chain. These initiatives are bearing fruit, as seen above.

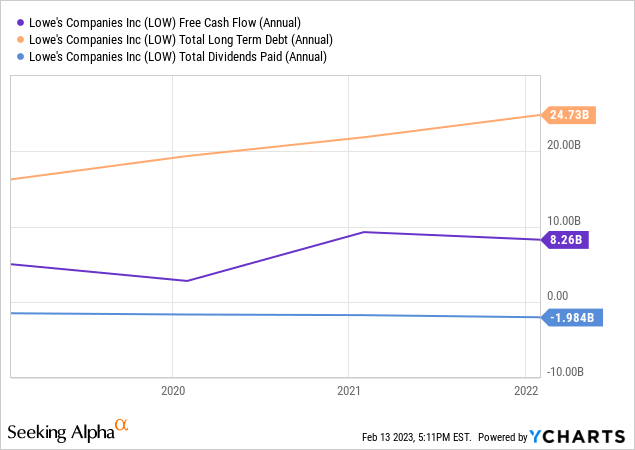

As far as the company’s balance sheet, debt has climbed, but remains manageable. LOW is among the best of the best of dividend growth stocks, and maintains an incredible streak including through the housing crisis. Free cash flow is solid at $8.26B. Management has projected $13B in share repurchases in 2022, and will likely continue to cannibalize the float. It’s not my favorite deployment of capital, but the company is attractively valued today and is driving improvements across all metrics, so I don’t see the repurchases as unnecessarily pulling capital from other needed areas. I don’t project they continue at this rate, however. With free cash flow where it is and the debt load approaching management’s target values, I’d anticipate somewhat more moderate buybacks in the medium term.

In the most recent quarter, the company spent $4B to repurchase 20.5M shares, so rough back of the napkin math would put that at $195/share, below the current share price. Management still sees plenty of opportunities to deploy capital. Here’s Marvin Ellison on the most recent call:

So as we look at things that we still have to catch up, and I’ll be very transparent, we’re not where we want to be. We still have a supply chain transformation process that’s underway, but we can get all that accomplished and stay within that $2 billion CapEx dollar amount.

We still have significant IT investments that we need to make. We made incredible improvement, but all those things also fall within that current allocation of CapEx. Bill is working to continue to improve merchandising and pricing systems. Again, those things are all mapped out. They’re costed out, and we have a good understanding of it. And we feel like at $2 billion of CapEx will allow us to achieve all of these things.

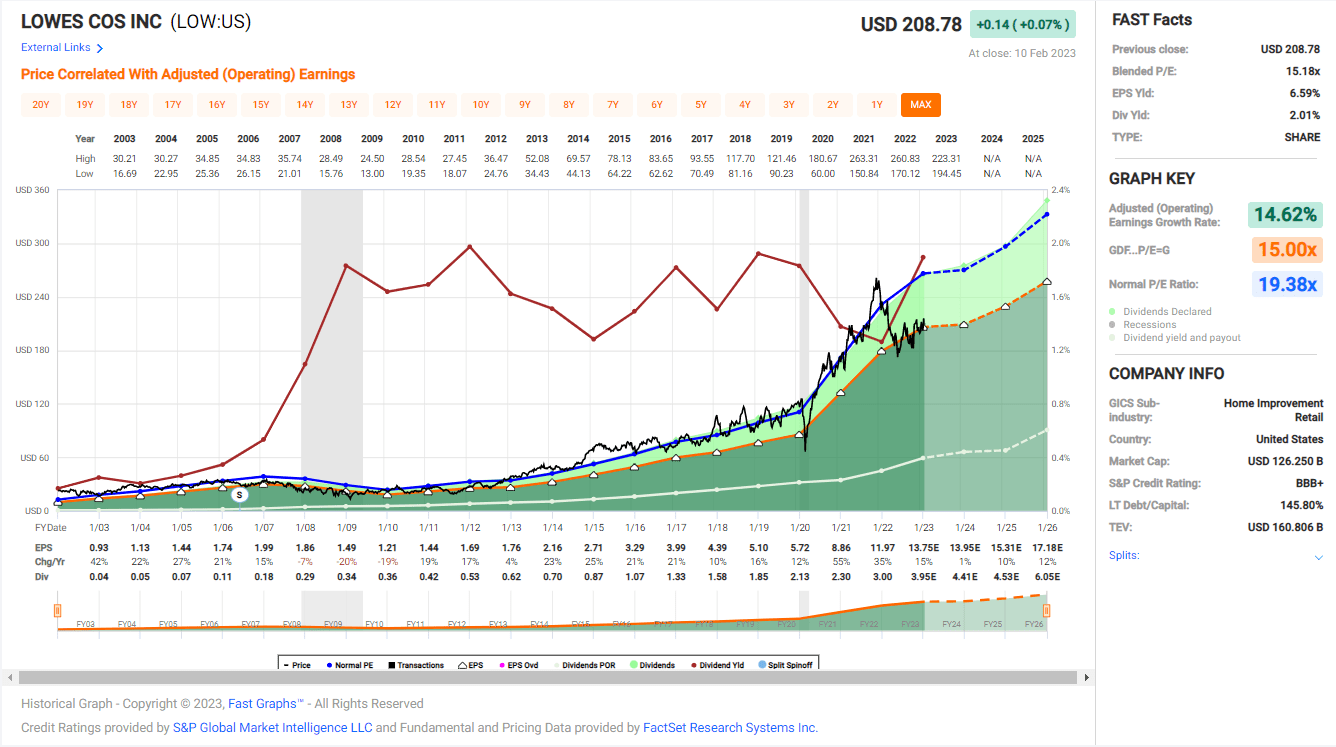

FAST Graphs

The company appears to be attractively valued looking at its long-term history. The company is trading right around 15X earnings, and for right around a 2% dividend yield. Combine that with a normal earnings growth rate of nearly 15% over the long-term, and I think LOW is a very attractive stock currently, even considering the macro short-term risks.

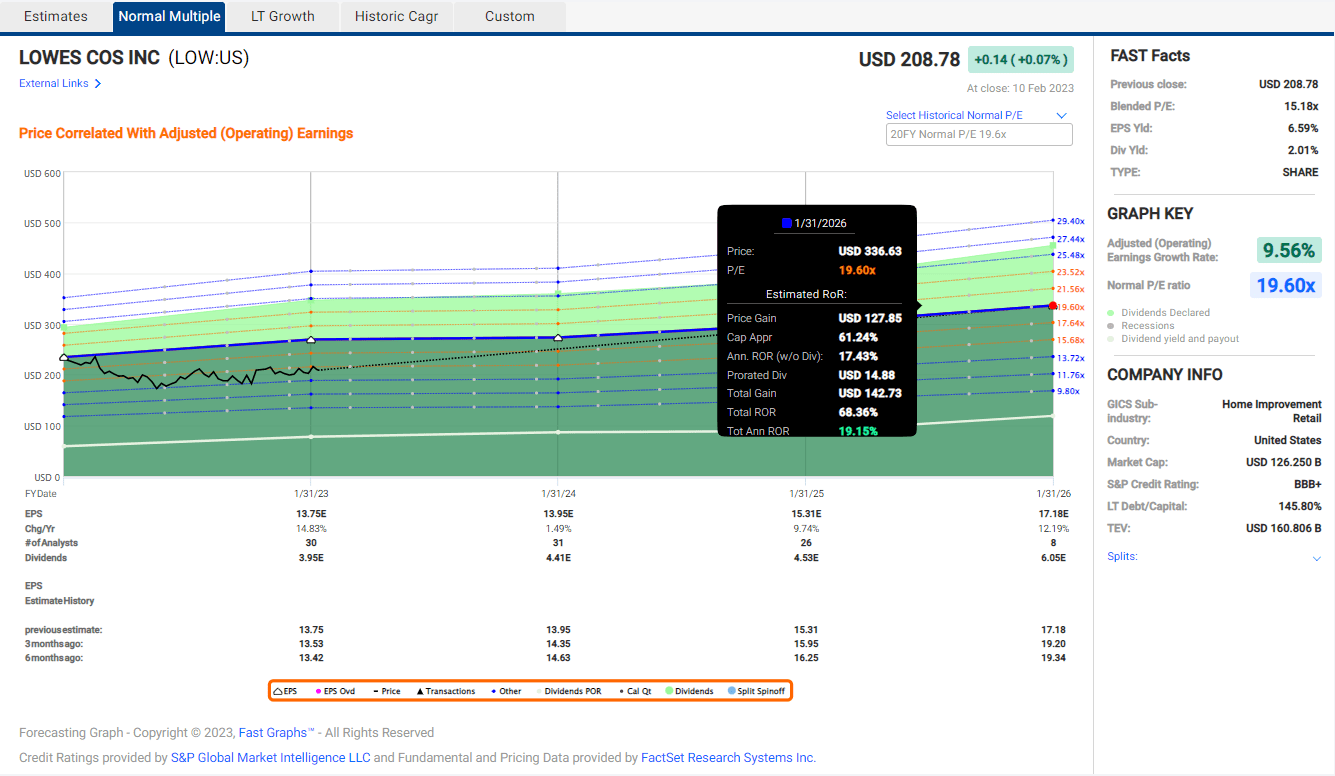

FAST Graphs

Based on analyst projections for earnings growth and a return to the company’s long-term average valuation, and investors could be looking at 18-19% annualized total returns from a purchase today.

Normally, I caution investors to not anchor to that number. However, in LOW’s case, I think there’s actually an argument to be made that they deserve to be trading at a higher multiple than they have historically. Since 2018, management has been highly motivated and lethally effective at turning the business around. Metrics are all pointed in the right direction, the company is closing the gap with HD, and I see a bright future ahead. I’m calling LOW a buy here, and I’ll be adding to my long-term position.

Be the first to comment