Bloomberg/Bloomberg via Getty Images

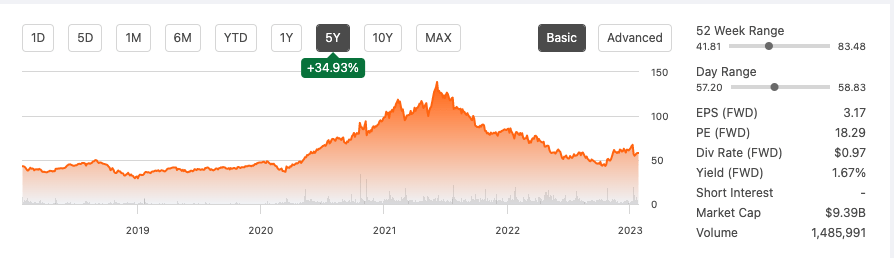

Logitech International S.A. (NASDAQ:LOGI), a gaming and electronic accessories company with a market cap of $9.39 billion, has just released disappointing Q3 2023 results and has cast a negative outlook on its full-year 2023 financials. However, the stock has been a beneficial long-term stock to hold, rewarding investors with returns of 34.93% over the last five years and maintaining a steady and upward dividend. This year the company has been decreasing in sales across all its business segments and all geographic regions.

Five-year stock trend (SeekingAlpha.com)

Consumers and business are reducing their spending, cautious of a recessionary loom. LOGI also takes a reserved cost-cutting stance to maintain a healthy balance sheet. Although it is investing in the booming gaming industry, I do not think it is wise to buy stock in a company with downward trending results, especially if peers are faring better under the conditions in this very competitive market. Therefore I recommend a hold rating.

Company overview

LOGI is a Swiss company founded in 1981 that designs, manufactures and sells hardware and software solutions and accessories sold to consumers and businesses for work, gaming and free time. The brands include Logitech, Logitech G, ASTRO Gaming, Streamlabs, Blue Microphones and Ultimate Ears.

Logitech website (logitech.com)

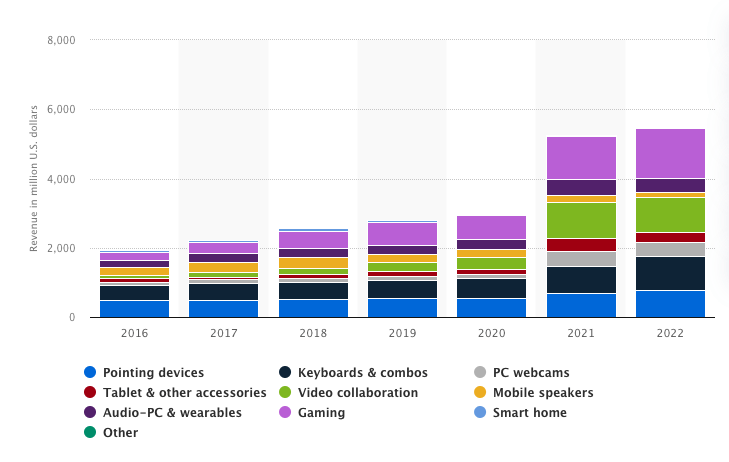

Below we can see the trending data of annual revenue-generating business segments. In FY22, gaming made up 26.5% of total revenue; video game collaboration was at 18.2%, keyboards & combos at 17.6%, pointing devices at 14.3%, PC webcams at 7.4%, audio and wearables at 7.3 %, tablet & other accessories at 5.7%, mobile speakers at 2.7%, bright home has reduced to 2.7$, and other is 0.3%.

Sales by business in Swiss Franc (statista.com)

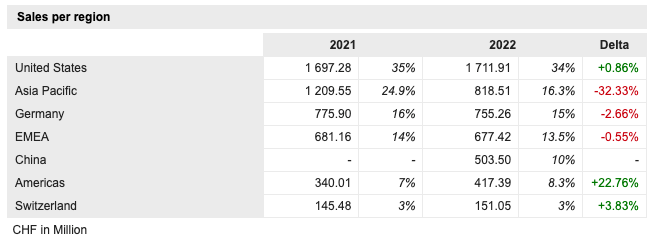

Below we can see that the United States is the largest revenue-generating region, followed by Asia Pacific. China is the company’s second-largest market.

Sales by region in Swiss Franc (marketscreener.com)

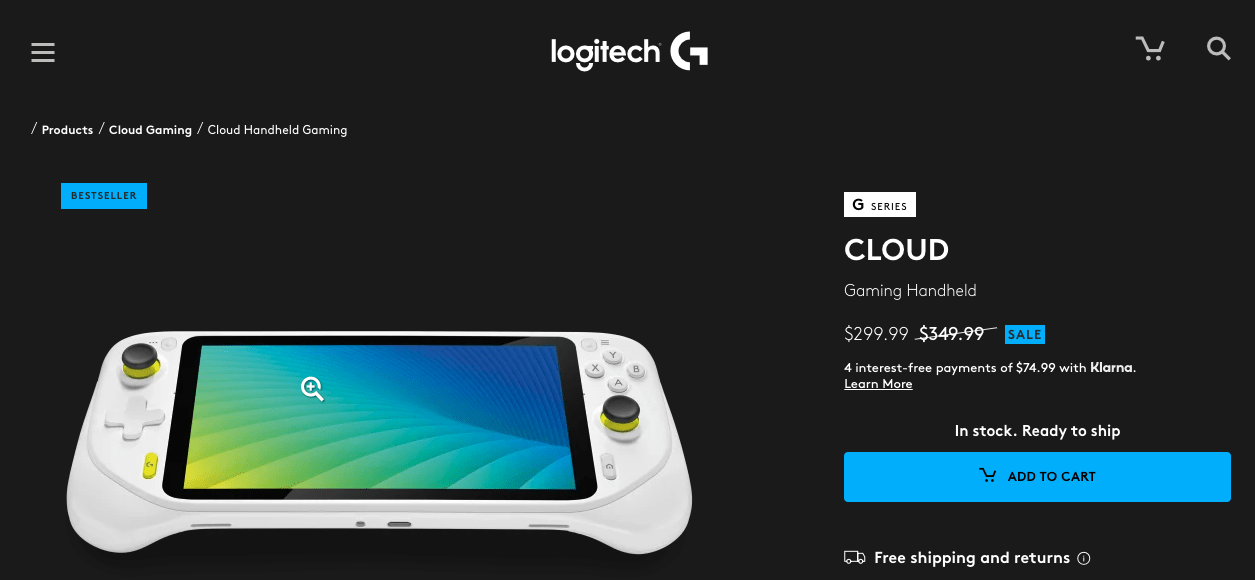

This last quarter sales decreased YoY across all segments and all regions. While sales are down, LOGI is gaining market share in the booming gaming industry. It has recently released G Gloud, its first-ever gaming handheld that requires cloud subscription services and gives instant access to an expansive library of games. It is currently only available in the USA and competes against offerings such as Nintendo Switch and Valve’s Steam Deck.

New product in a new category (logitechg.com)

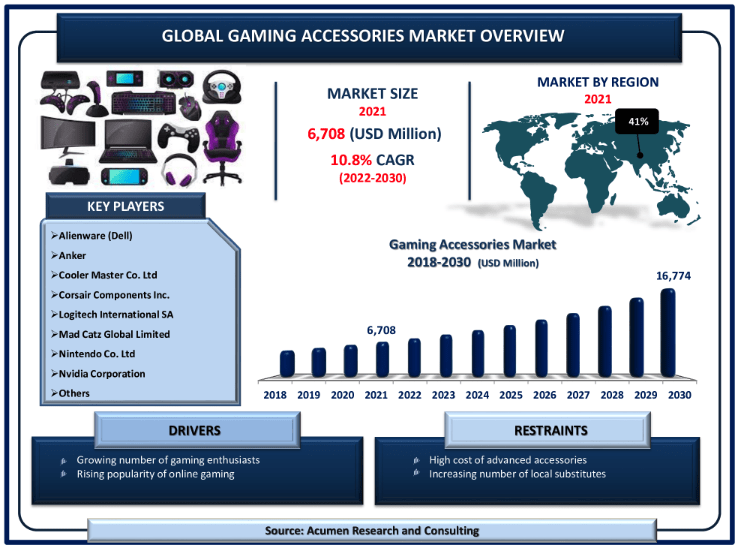

Below we see that the gaming industry has a CAGR of 10.8% and is predicted to reach $16.774 billion by 2030. However, the market is highly competitive and has many strong brand and budget alternatives from global competitors.

Gaming accessories market growth (acumenresearchandconsulting.com)

Third quarter financial overview

The top and bottom lines have continued to be impacted by the weakening macro environment that is not only moving consumer purchases, but the company is seeing enterprises reduce their spending. We noticed sales were $1.27 billion for Q3 2023, a 22% decrease YoY. The gross margin has also decreased to 37.9%

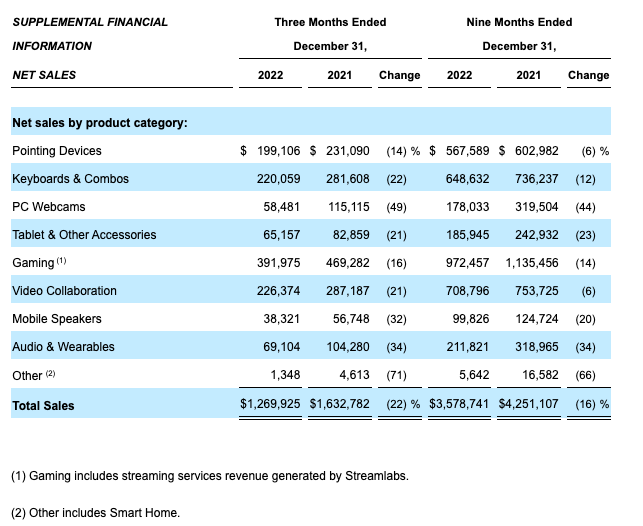

Sales dropped across all segments, as seen in the table below. That over the last three months, every category decreased YoY by double digits, and gaming experienced the least significant decrease at 16%. Over the nine months, we see that video collaborations were least impacted at a 6% decrease YoY. The sales are reflective of the downward turn in enterprise and consumer sales. Most sales were during promotional weeks, which has also cut into the gross profit margin.

Sales by segment Q3 for three and nine months (Investor presentation 2023)

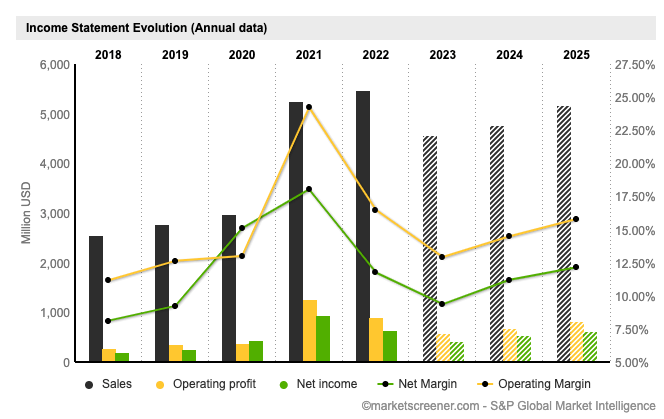

Ignoring the COVID-19 bubble year of FY2021, LOGI has delivered promising upward-trending top and bottom line results since 2018. However, this FY 2023, the management has lowered its net income expectation, and we are likely to see a weaker set of results than the year prior. This past quarter income declined 33% to $177 million.

Financial overview (marketscreener.com)

One of LOGI’s long-term strengths has been its consistent ability to generate positive cash flow. Last financial year, due to increased headwinds, it ended at $17 million and is currently on $196.8 million TTM. Positive cash flow is essential to continue to grow the company, pay off expenses and give back to investors. Year to date, LOGI has returned $486 million via its dividend program and share repurchases, $90 million of which was this quarter. Although the company is cutting down on costs, investing in R&D remains essential, and this past quarter’s investment of $63 million was 50% higher than in Q3 2020. Over the last two years, inventory has more than doubled its historical trends, with a TTM of $797.7 million.

Annual cash flow (SeekingAlpha.com)

Although cash from operations is downward trending, the balance sheet remains healthy, with $1.04 billion in total cash and zero total debt. The business is liquid at a current ratio of 2.20 and a quick ratio of 1.40, meaning it has enough liquid assets to pay off short-term liabilities.

Peer Comparison

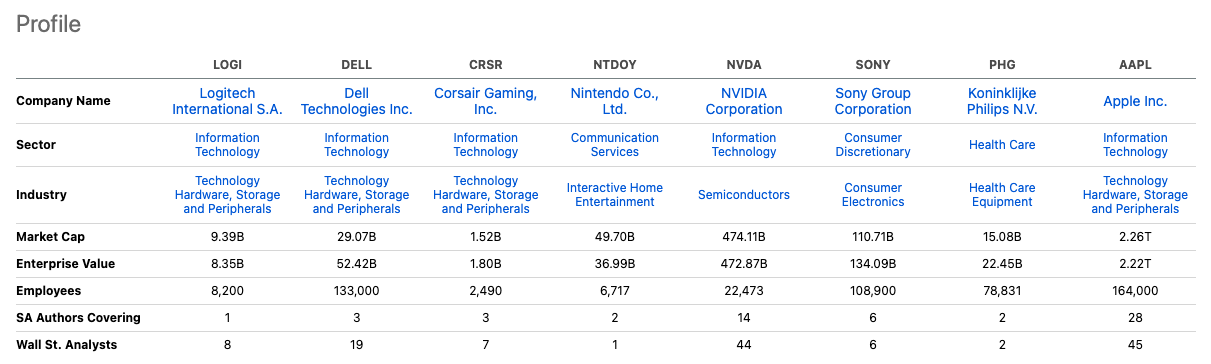

I have compared LOGI to some of its leading gaming and consumer electronic accessories peers. We can see that, apart from Corsair Gaming (CRSR), LOGI is much smaller in terms of enterprise value at $8.35 billion. All stocks, apart from CRSR, are dividend stocks.

Peer comparison (SeekingAlpha.com)

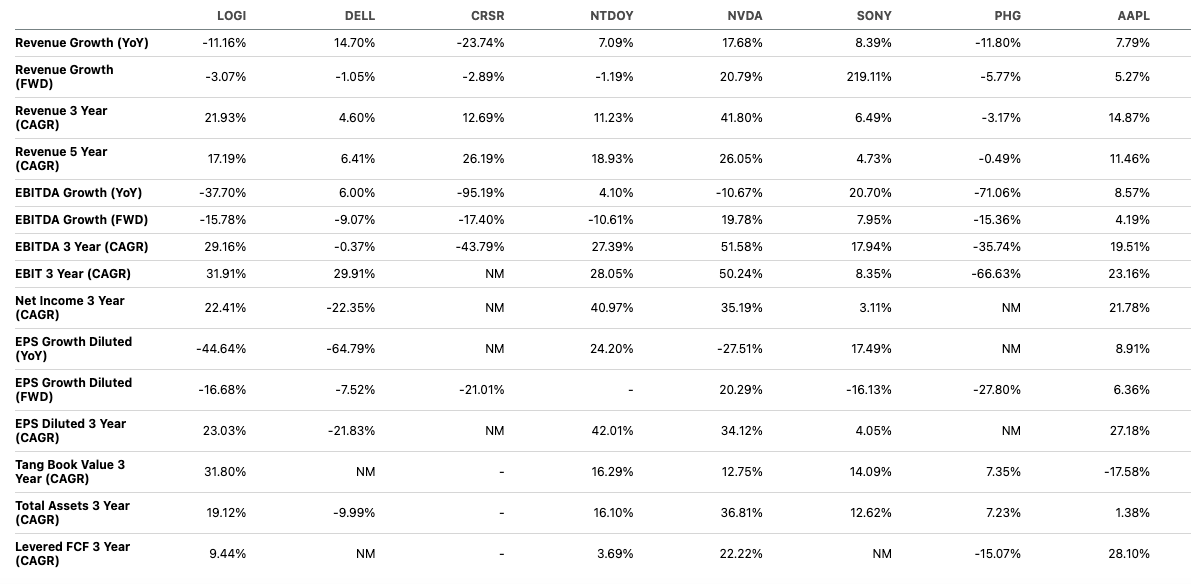

LOGI has put much emphasis on solid headwinds impacting its sales growth. If we look at development across these peers, we see that many are not as significantly affected as LOGI, with a negative YoY growth at 11.16% versus the leader of the pack Dell (DELL), at revenue growth of 14.70%. LOGI has a negative YoY EBITDA decline of 37.70% compared to the leader of the pack Sony Group (SONY), with an EBITDA growth of 20.70%.

Growth comparison (SeekingAlpha.com)

Risks

It has been a more challenging year for LOGI than for some of its competition, although all of them have been hit by economic and geopolitical headwinds. The industry is fiercely competitive, with many global corporations, small and large, with fast-paced technological changes impacting how customers work, play and have free time. LOGI works to attract both consumers and businesses to their solutions. It is crucial to have in-demand offerings, or it could negatively impact the company’s future performance. As an international player, the business has been affected by macro events such as the recent COVID outbreaks in China, impacting supply availability. On the other hand, China has recently opened up again as its second-biggest consumer market. This may be a tailwind for improved performance.

Final thoughts

LOGI has been a rewarding stock for long-term investors. However, the nature of the economic and geopolitical environment pushes the company into a more conservative, cost-focused strategy to withstand the ongoing headwinds. We have seen that some competitors have fared better under the circumstances. Although LOGI has a healthy balance sheet, is continuing to invest in R&D and is focused on benefiting from the booming gaming industry, while the business has been decreasing sales over the last year across all segments and all geographies, I do not recommend buying the stock and give it a hold rating.

Be the first to comment