Galeanu Mihai/iStock via Getty Images

A Quick Take On LivePerson

LivePerson, Inc. (NASDAQ:LPSN) reported its Q3 2022 financial results on November 7, 2022, beating revenue and missing EPS estimates.

The company provides online messaging and communications technologies to businesses and consumers worldwide.

Although the firm has promise with its conversational, AI-driven technologies, given LPSN’s worsening operating losses and tepid growth, I’m on Hold for LivePerson, Inc. stock until management can show more significant growth while moving quickly toward operating breakeven.

LivePerson Overview

New York-based LivePerson, Inc. was founded in 1995 to provide what it calls conversational commerce software to businesses and consumers.

The firm is headed by founder and Chief Executive Officer Robert LoCascio, who is active in various charity organizations in New York City.

The company’s primary offerings include:

-

Conversational Cloud

-

Voice

-

BELLA Health (being discontinued)

-

GainShare managed contact center.

The firm acquires customers via direct sales and marketing efforts and has customers from smaller mid-market firms to large enterprises.

LivePerson’s Market & Competition

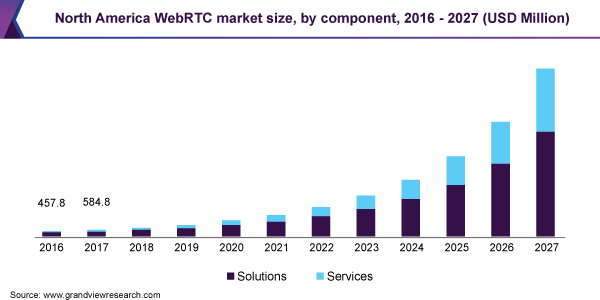

According to a 2020 market research report by Grand View Research, the market for Web real-time communications products was an estimated $2.3 billion in 2019 and is expected to reach $41 billion by 2027.

This represents a forecasted extremely high CAGR of 43.4% from 2020 to 2027.

The main drivers for this expected growth are the need for a better user experience, reduced costs, and an increase in work-from-home employee work environments.

Also, the chart below shows the historical and projected future growth trajectory of the N. America WebRTC market through 2027:

N. America WebRTC Market (Grand View Research)

Major competitive or other industry participants include:

-

Amazon (AMZN)

-

Facebook (META)

-

Cisco (CSCO)

-

Oracle (ORCL)

-

Ribbon (RBBN)

-

Avaya (AVYA)

-

Apidaze

-

Dialogic

-

Plivo

-

Quobois.

LivePerson’s Recent Financial Performance

-

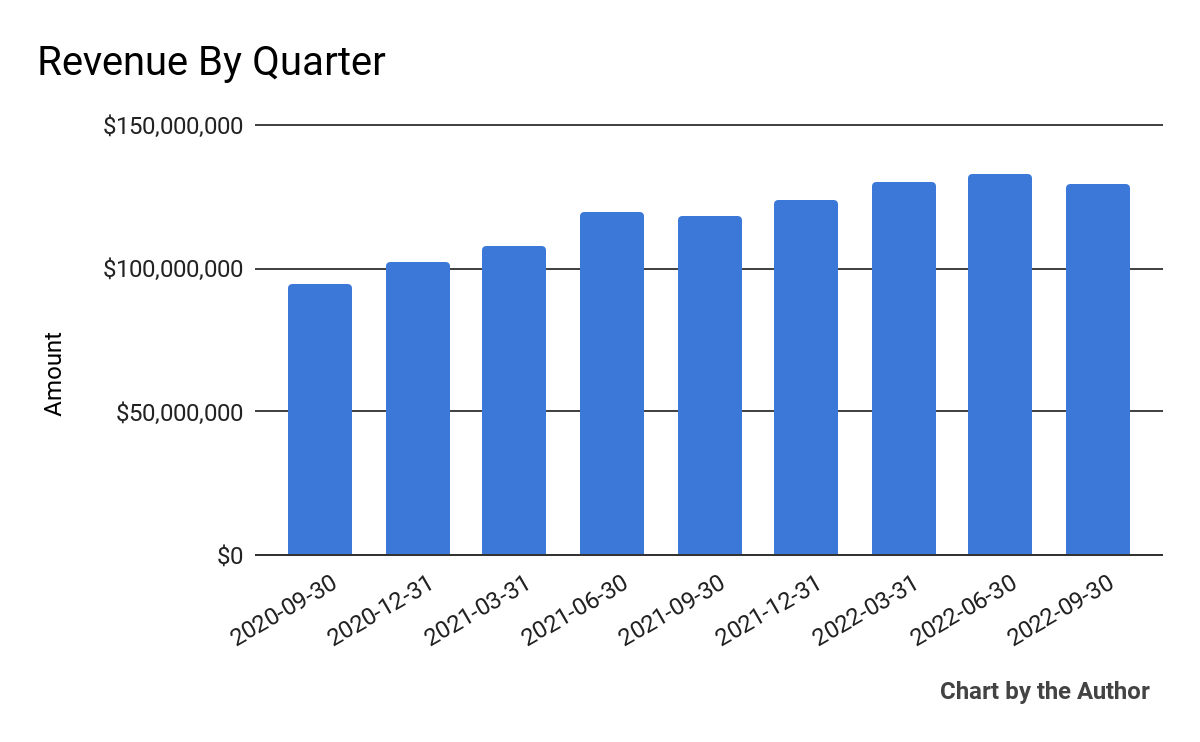

Total revenue by quarter has grown as shown below:

9 Quarter Total Revenue (Financial Modeling Prep)

-

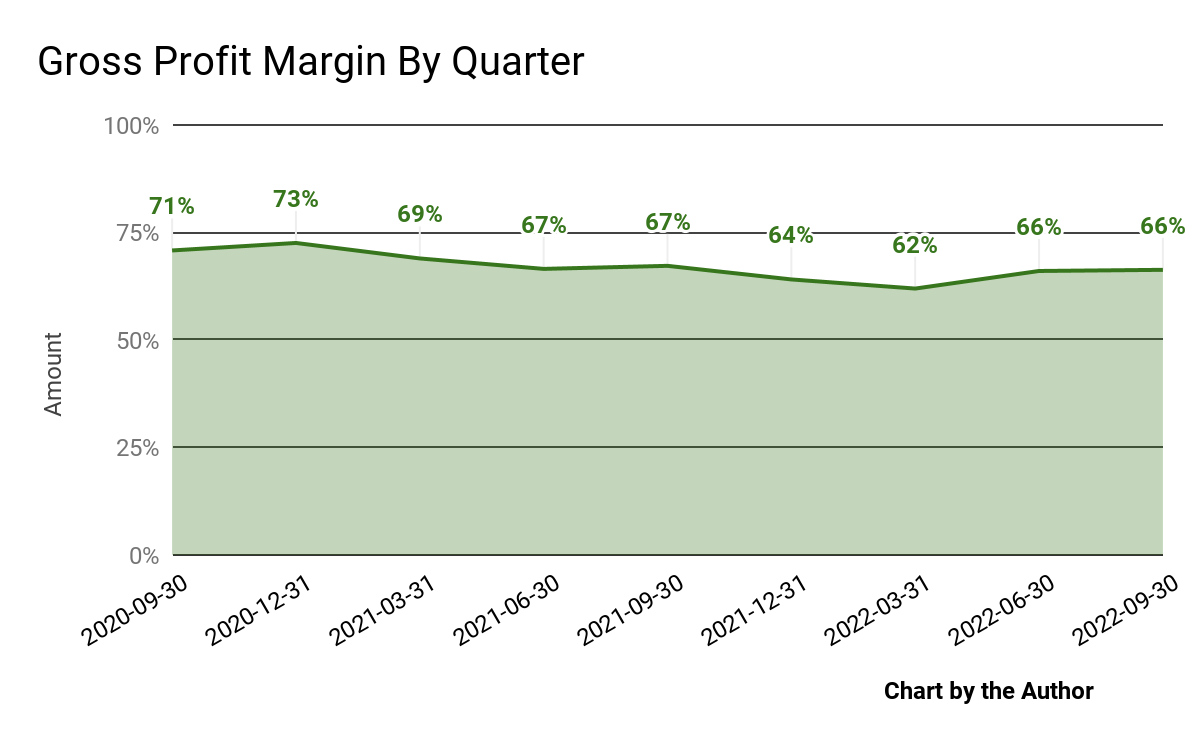

Gross profit margin by quarter has trended lower in recent quarters:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

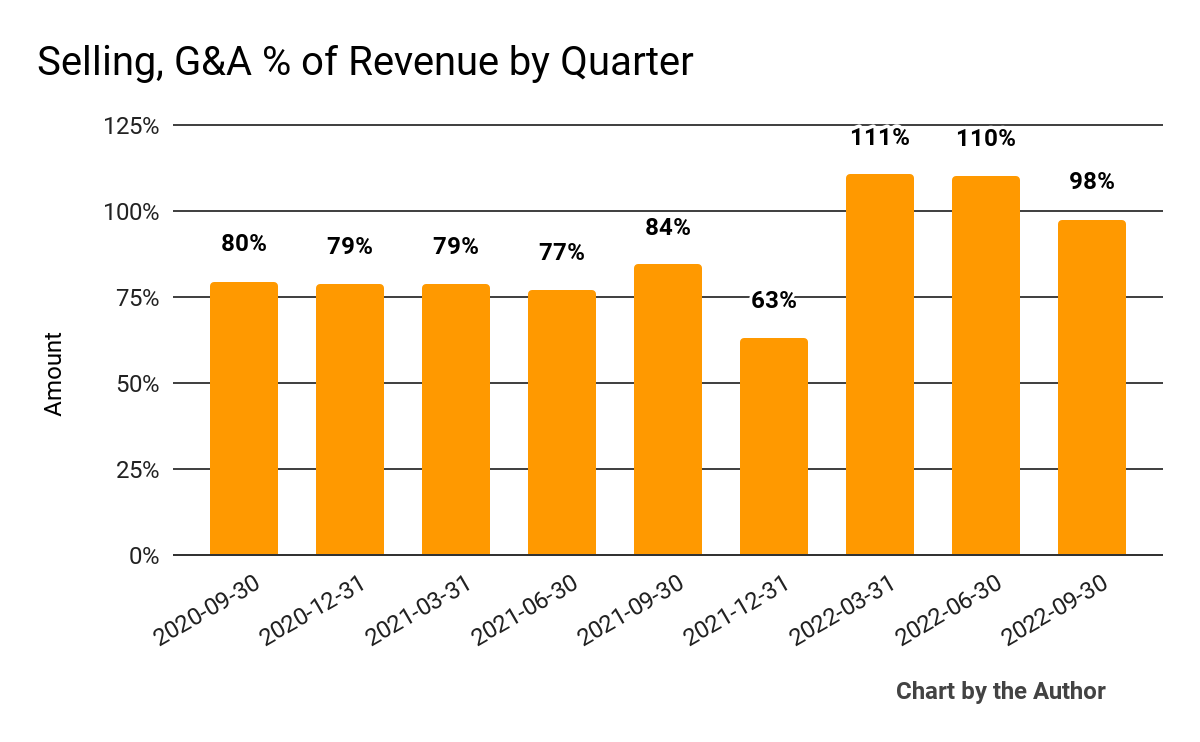

Selling, G&A expenses as a percentage of total revenue by quarter have risen in recent quarterly reporting periods:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

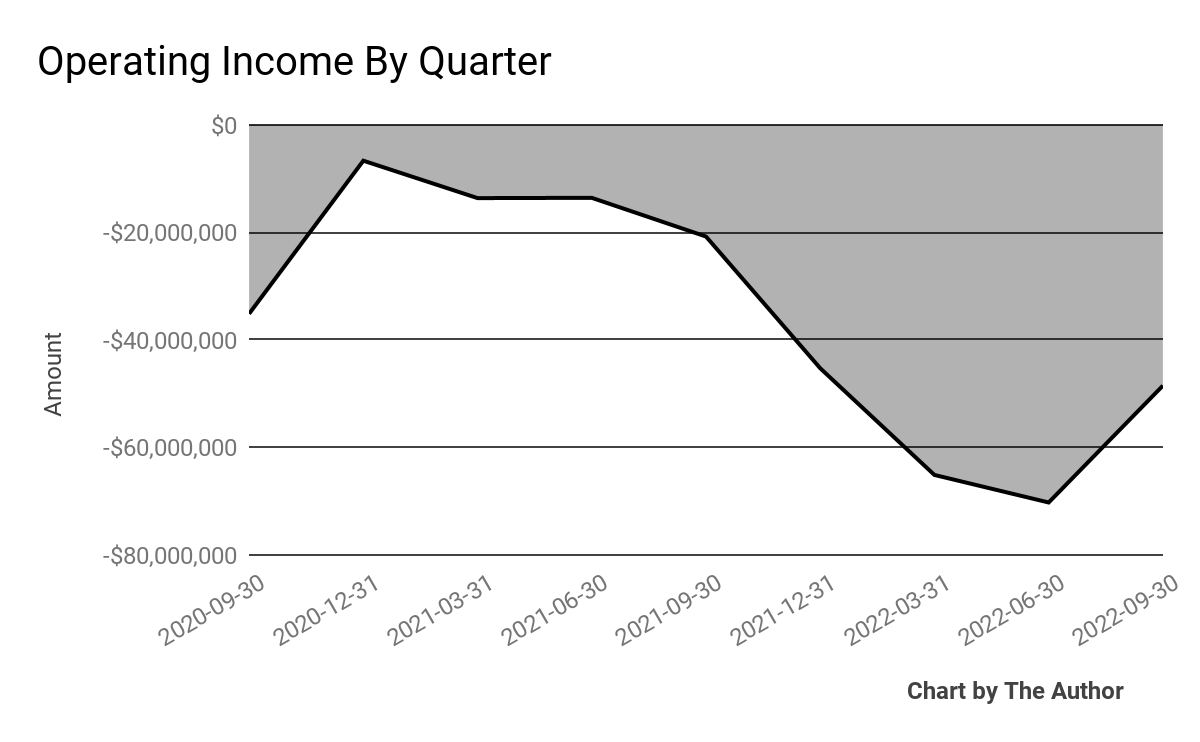

Operating losses by quarter have worsened sharply in recent quarters:

9 Quarter Operating Income (Financial Modeling Prep)

-

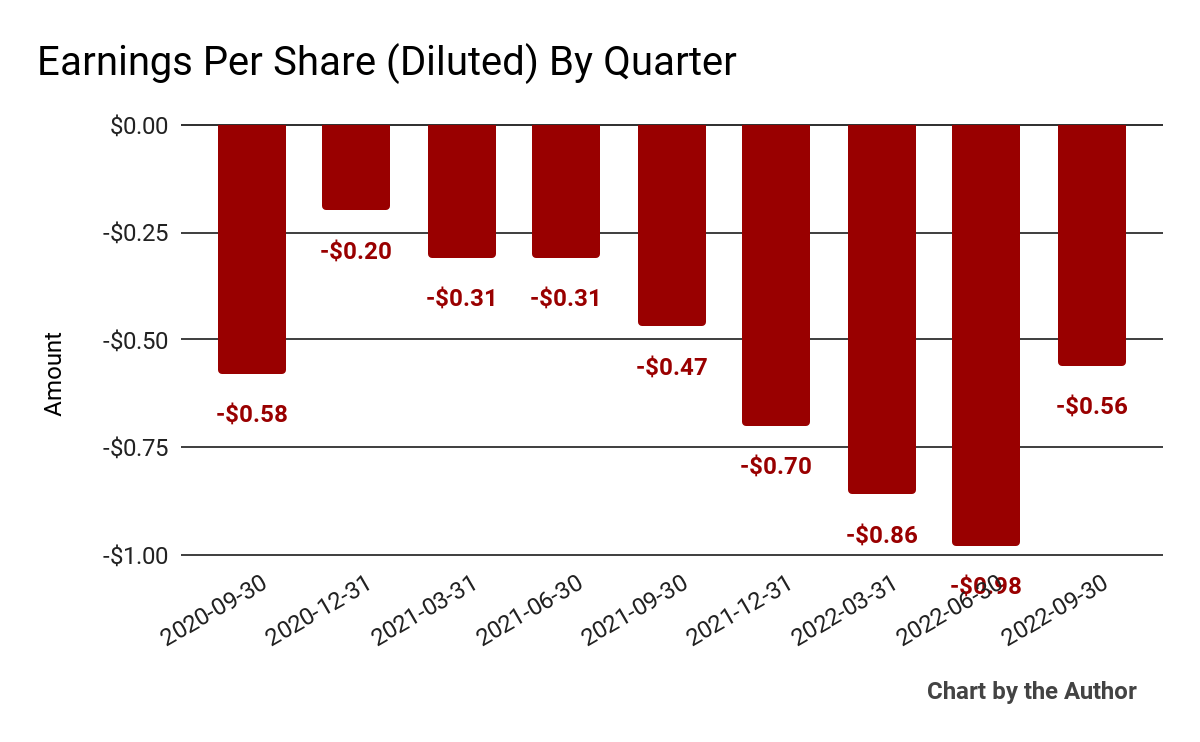

Earnings per share (Diluted) have also deteriorated further into negative territory in recent reporting periods:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP.)

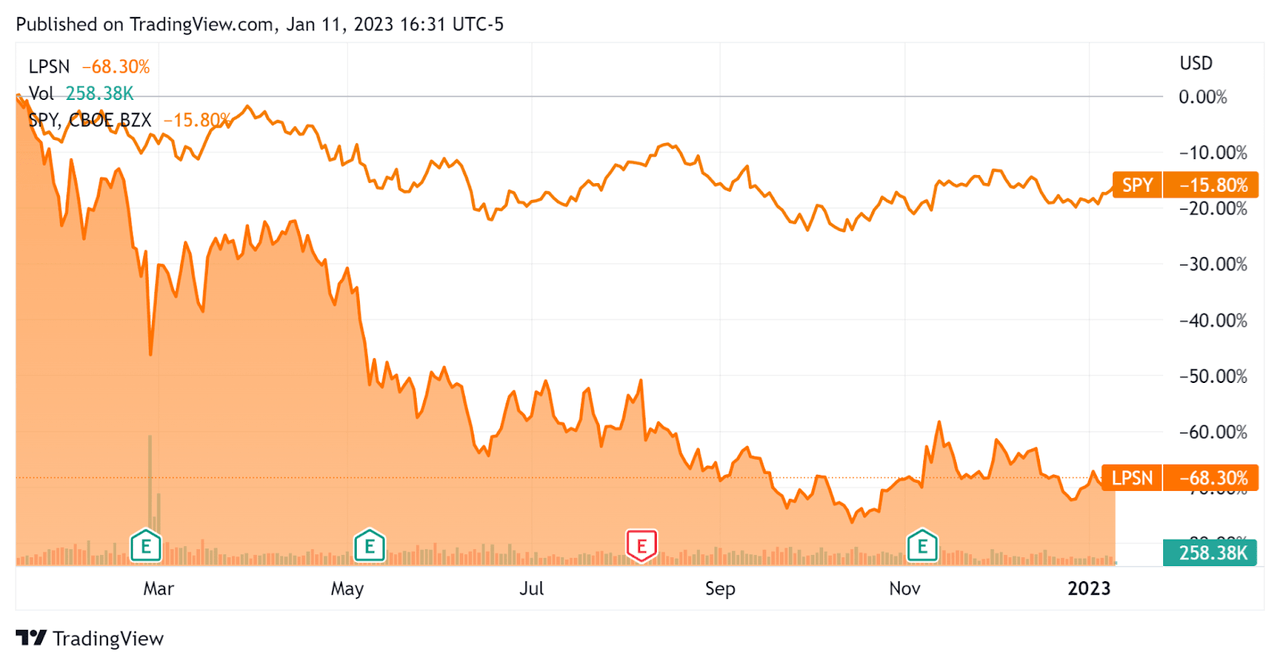

In the past 12 months, LPSN’s stock price has fallen 68.3% vs. the U.S. S&P 500 Index’s (SP500) drop of around 15.8%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For LivePerson

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.3 |

|

Enterprise Value / EBITDA |

-6.5 |

|

Revenue Growth Rate |

15.2% |

|

Net Income Margin |

-45.3% |

|

GAAP EBITDA % |

-35.0% |

|

Market Capitalization |

$798,477,824 |

|

Enterprise Value |

$1,174,990,068 |

|

Operating Cash Flow |

-$111,866,000 |

|

Earnings Per Share (Fully Diluted) |

-$3.10 |

(Source – Financial Modeling Prep.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

LPSN’s most recent GAAP Rule of 40 calculation was negative (19.8%) as of Q3 2022. This means the firm’s performance has worsened substantially over Q1 2022, per the table below:

|

Rule of 40 – GAAP [TTM] |

Calculation |

|

Recent Rev. Growth % |

15.2% |

|

GAAP EBITDA % |

-35.0% |

|

Total |

-19.8% |

(Source – Financial Modeling Prep.)

Commentary On LivePerson

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted customer satisfaction with its products and resulting increase in shifting greater contact volume to the firm’s AI-powered customer engagement tools.

The company closed 86 deals during the quarter as brands seek AI-enhanced digital engagement capabilities.

As to its financial results, total revenue rose 9.5% year-over-year and adjusted EBITDA was $9.1 million.

A bright spot was a 25% year-over-year revenue growth for its B2B segment. By product, conversational cloud messaging grew by 25%, the highest growth of any product line.

The company’s net retention rate “was just below our target range of 105% to 115%.”

The firm’s Rule of 40 results have worsened dramatically into negative territory, with a positive revenue growth result more than offset by a negative operating result, contributing to a poor performance figure for this metric.

SG&A expenses as a percentage of revenue have risen markedly, resulting in worsening operating losses and negative earnings.

For the balance sheet, LivePerson, Inc. finished the quarter with $393.3 million in cash and equivalents and $736.5 million in long-term debt.

Over the trailing twelve months, free cash used was $159 million, of which capital expenditures accounted for $47.1 million. The company paid a very hefty $122 million in stock-based compensation (“SBC”).

Looking ahead, management raised revenue guidance for full-year 2022 to a 10.5% growth rate at the midpoint of the range and reaffirmed its previous guidance for adjusted EBITDA.

Note that adjusted EBITDA typically doesn’t include stock-based compensation, which for LivePerson has been a very high $122 million in the trailing twelve-month period.

Regarding valuation, the market is valuing LPSN at an EV/Sales multiple of around 2.3x.

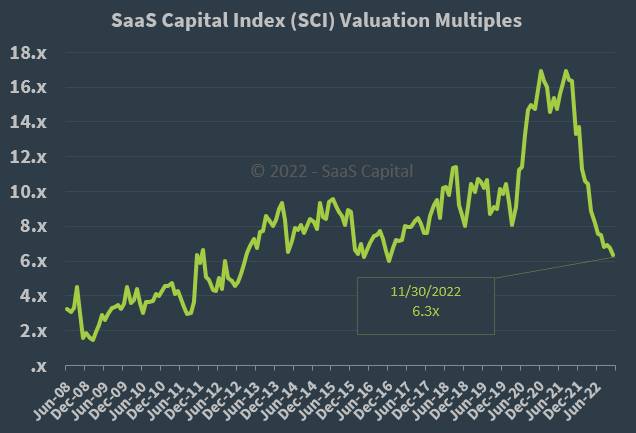

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.3x on November 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, LPSN is now currently valued by the market at an even greater discount to the broader November 30, 2022 SaaS Capital Index than it was as of Q1 2022’s results.

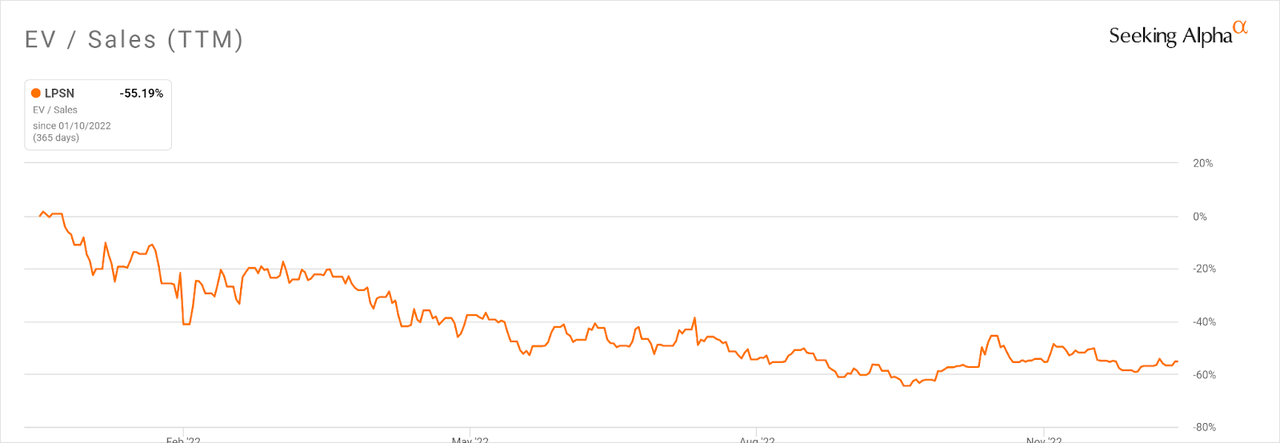

Notably, LPSN’s EV/Sales multiple [TTM] has compressed by over 55% in the past twelve months, as the Seeking Alpha chart shows here:

EV/Sales Multiple History (Seeking Alpha)

A potential upside catalyst for LivePerson, Inc. stock could include a recession that pushes companies faster toward automation efforts that can reduce costs and improve customer retention or acquisition.

Although LivePerson, Inc. has promise with its conversational, AI-driven technologies, given LPSN’s worsening operating losses and tepid growth, I’m on Hold for LivePerson, Inc. stock until management can show more significant growth while moving quickly toward operating breakeven.

Be the first to comment