AmnajKhetsamtip/iStock via Getty Images

Overall thesis

I believe that Lifetime Holdings (NYSE:LTH) has used its newly-acquired status as a public company (recently IPOed in October 2021) to finance its expensive management compensation and benefits, slowly pay down debt through equity issuances, and limit cash losses.

Under these assumptions, the company’s cash generation capability is just enough to pay back loans and finance its high capital expenditures needs, and thus I see the outstanding equity value is highly overvalued by at least 40%. This conclusion was reached after an in-depth DCF analysis with assumptions derived from the research process disclosed below.

LTH overview, financials, and quick historical background

Lifetime Holdings is a fitness center operator in the US. They currently manage 154 facilities across 29 different states. Their business model is subscription-based, as their clients pay a fixed membership fee to access the facilities, along with generating revenue through in-center spending for additional services. As of June 30, 2022, they had around 770,000 paying members, which generated around $800 million in subscription revenue in 2021. LTH was formerly known as Lifetime Fitness and has been traded on NYSE since the early 2000s. In 2015, they decided to go private and delisted the shares, in a transaction led by a private equity group that valued the company at more than $4 billion (source: here). In October 2021, after 6 years as a private company, they came back to the public markets.

As one can guess, its business model is capital intensive, levered, and has low EBITDA margin. They also make extensive use of capital and operating leases to operate their facilities. (source: latest 10K, various pages).

In the last 4 years, they never reached positive FCF as capital expenditures caused cash losses well before the pandemic hit, leading them to accumulate as much as $2.2 billion in debt as of Dec 2018. Later on, after the IPO took place in October 2021, they used the proceeds from equity issuance(s) to reduce leverage, now at “only” $1.8 billion in LT debt. While their debt-to-equity ratio is still below 1.0x (about 0.8x), their debt-to-adjusted EBITDA ratio is above 6x even if we use the estimated 2022 EBITDA figures, which should not be impacted by Covid-19. Also, these adjusted numbers add back share-based compensation, which was extremely high in Q1 2022 at $22mm, or 55% of adjusted EBITDA ($40mm).

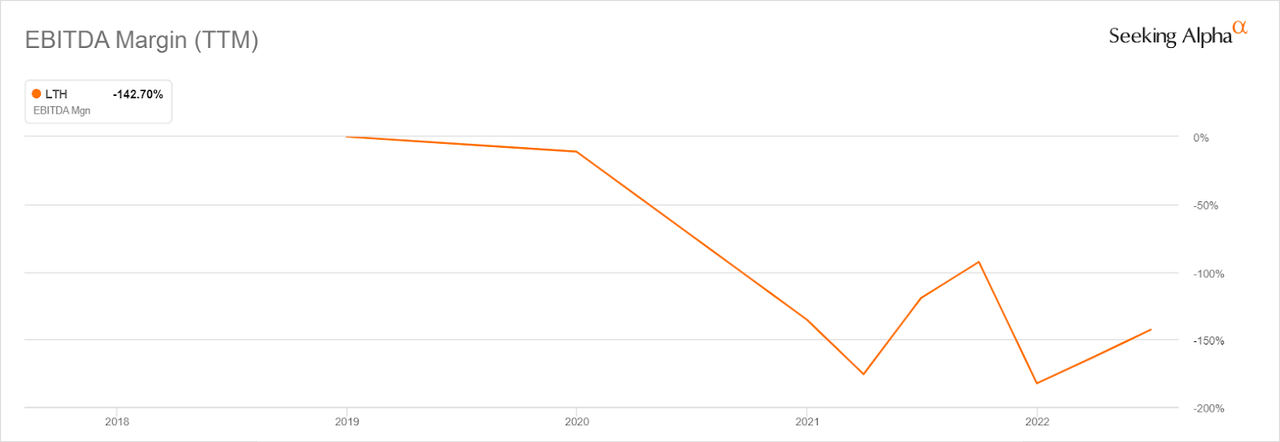

EBITDA Margin (Seeking Alpha Charting)

And the trend of the EBITDA margin in the last years (pre and post-pandemic), is clearly not comforting to the eyes of both bondholders and shareholders.

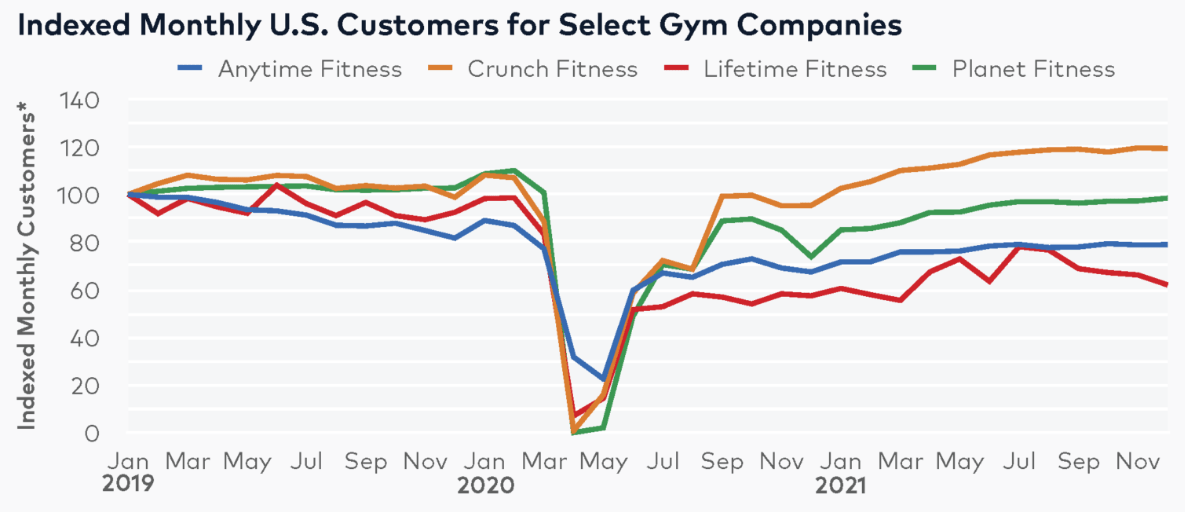

This is what their financial conditions looked like when Q2 2022 closed: $60 million in cash, FCF positive for $3 million (after accounting for one-time gains from sales of RE, of around $175 million), and an astronomical $460 million of short-term liabilities. Their current ratio was below 0.5 and they were barely FCF-positive despite $175 million of one-time gains derived from sale-leaseback transactions closed in the last 2 quarters. In my opinion, this recent pressure may compel management to re-think their capital-intensive approach, meaning that they will likely be heavily selling assets in 2022 to pay down debt, while moving to rented solutions (i.e. expect more volatile margins). (source: Q1 earnings call). Also, according to Bloomberg Second Measure, they are struggling to grow memberships relative to their competitors, and LifeTime Fitness reported the worst recovery performance after the pandemic.

Monthly Customers (Bloomberg Second Measure)

(source: here).

These stats clearly show an underperformance of LTH relative to Crunch Fitness or Planet Fitness (PLNT), which may suggest lower client satisfaction, retention rate after free trials, and lack of competitive advantage (i.e. brand power).

To summarize:

-

$1.8 billion in debt, or 10x 2022 adjusted EBITDA;

-

Lost between $100 million and $280 million per year between 2019 and 2021, with no positive year.

-

Expected continued high Capex requirements above $100 million per year as they are opening around 10 new centers per year for the next 3 years.

-

High pressure on short-term financial conditions may induce them to sell up to $500 million of RE assets in 2022.

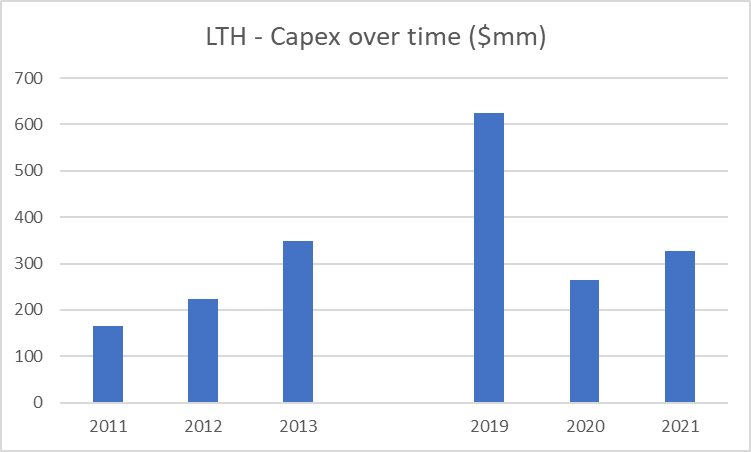

But what was it like before the company went private in 2015? Well, not so different. In the last 10K filed before the transaction, their Capex requirements remained high almost every year before 2015. From 2009 to 2014 they spent an average of $300 million per year on Capex, and before the Great Recession, they were actually spending more than $400 million. Long-term debt doubled during the same period because they were losing money every single year.

Capex over time (Data from historical 10-Ks)

One could argue that that was the recession’s fault. Well, from 2005 to 2008 they were again losing some $150 million per year in FCF, and the company saw its debt grow 4x from 2005 to 2009. Surely the past is not a source of comforting data in the case of LifeTime Holdings (formerly LifeTime Fitness).

Management overview and absurd compensation

As we all know, the management team of a company usually makes a difference, especially in the long term. In the case of this particular short thesis, it matters a lot. Since LifeTime Holdings is a money-losing company with a deeply negative FCF and tons of debt, a CEO that makes $24 million in a year is meaningful, and can’t be ignored.

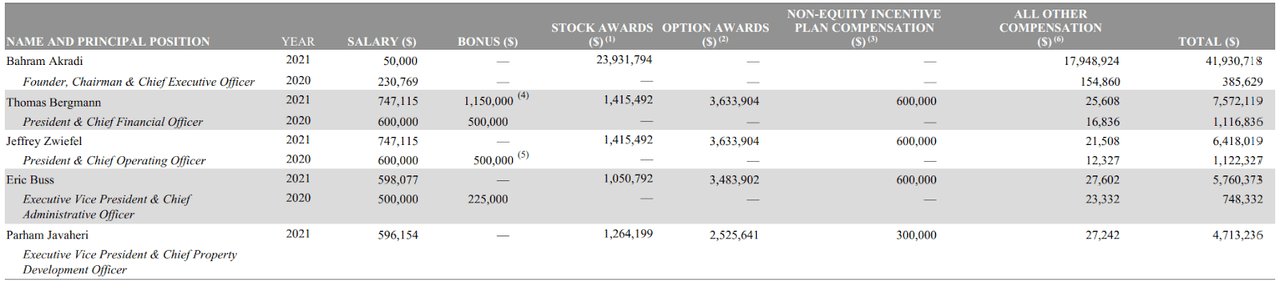

The most significant figure on the board is the CEO, Bahram Akradi, who founded LTH in 1991. He has been a major shareholder for all this time and still owns a 10% stake after the company returned to the public markets in 2021. Compensation at LTH is very generous for executives, as the top 5 directors earned as much as $65 million in 2021, mainly in stock awards (i.e. dilution), while the company reported a cash outflow of $300 million in FCF and revenue was still down 30% from pre-covid levels. The CEO earned only $50,000 in cash but got $24 million in stock awards. In addition to this, the one-time cancelation of a $17 million loan is reported as “other compensation”, for a total of more than $40 million. For comparison, it is more than the CEO of Goldman Sachs, or JP Morgan, or Disney. (source: here).

Management compensation (2021 proxy filing)

(Source: Latest Proxy filing available, page 38, here).

Related party transactions are frequent at LTH

From loans to directors to lease agreements signed with companies owned by related persons (mainly directors) LTH has a long history of entering business with close entities.

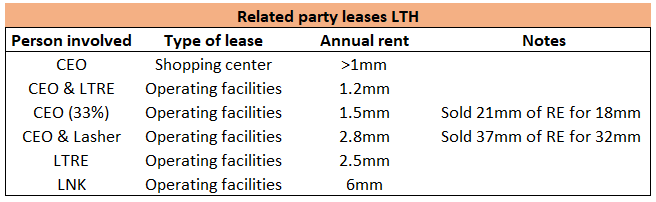

They currently have 4 lease agreements involving the CEO and founder Bahram Akradi, which brings him at least $1.5 million in rent per year, because its interest in other transactions doesn’t seem to be disclosed. He owns one main operational facility of the company located in Woodbury, Minnesota, along with a shopping center he acquired in 2003 and leased to LTH through 2030. The company also entered into 2 different sale-leaseback transactions between 2018 and 2019: in 2018 LTH sold RE valued at $21 million for only $18 million to a private company where the CEO had a 33% interest; and again, in 2019, they sold another $37 million of RE assets for just $32 million, to a company participated by the CEO and Mr. Lasher, a member of the BoD. It is also important to note that this price cutoff is calculated using book value and not market value, which is supposedly much higher. (source: 2022 Proxy filing, pages 56 – 58).

Besides the CEO, Stuart Lasher, a member of the BoD, along with other investors (“LTRE”), entered into a sale-leaseback agreement in which he acquired $35 million of RE assets for $37 million and got a 25 years lease agreement of $2.5 million per year with LTH.

Own made table ((Elaborated) data from proxy filing)

Then we have the loans. In August 2018 the CEO (again), Mr. Akradi, received a $20 million loan from the company, with his LTH stake as collateral (source: proxy filing, page 28, CEO compensation). Such credit agreement was then amended different times to cancel the principal outstanding, first by $5 million (2019) and then the remaining $17 million (2021), with the clause that the CEO is not entitled to severance benefits for 3 years. The company claims it can be also seen as a form of “other cash compensation”, as reported on page 38.

In June 2020 the company also disclosed a $108 million loan granted by some stakeholders to LTH, with a 12% APR and the possibility of converting it into equity. Following its conversion in January 2021, for an estimated fair value of $149 million, the company recorded $41 million in losses. (source: 10K, page 44).

Last but not least, in 2017 LTH decided to contribute half of the expenses sustained by Mr. Bergmann, the CFO, to operate his personal aircraft, in exchange for the possibility of using the plane for corporate purposes (i.e. trips for the CEO and BoD). The CEO spent $160,000 in 2021 in travel expenses accumulated with such aircraft. (source: Proxy filing, page 38).

Risks (of being short): what could go right with this company

The main risk of being short is operating leverage. Like many other capital-intensive businesses, LTH could easily double or triple its CFO in a year or two if demand starts growing consistently. The nature of their costs, which are mainly fixed, would cause their margins to expand a lot and cause a re-rate of the stock, damaging any short seller. Now, for this to happen we would need the company to report historical record new membership subscriptions during a period of (1) rising inflation, (2) increasing pressure on consumers spending capacity, and (3) long-term trends of lower interest for gyms by favoring fitness at-home solutions.

Expected financial results and the impact of a more asset-light business model: finding a fair price for LTH

As I think management decided to move away from high debt, and high PP&E balance sheet, they will likely be moving towards selling the majority of their RE assets, de-leverage, and moving to rent the places they formerly owned. In my view, this will have different outcomes in their financial statements: (1) reduce leverage and interest expense, (2) increase rent expense, and (3) increase margin volatility. Indeed, as they will benefit from lower pressure on their financial position, renting in this particular period of rising rates could prove to be painful to their margins. Also, while contracts are fixed, they could be exposed to increasing rent rates at the time of renewal, which could eventually result in less visibility on their quarterly and annual net income, FCF and EBITDA. From 2019 to 2021, rent rose from $165 million per year to $210 million, while interest expenses also increased from $128 million to $220 million. For 2022, we should expect rent to rise to as much as $255 million, or a 20% increase, while their PP&E should decrease to somewhere between $2.4 and $2.5 billion, also accounting for new club openings.

Still, while they are selling existing clubs, they plan to open an additional 12 ones in 2022, with more planned for subsequent years after 2023 (as stated in the latest call). This means that the Capex requirements will not be zeroed out, and while they may decline substantially from the 2019 peak at $600 million per year, LTH may need to spend at least $100-200 million per year to grow revenues (which is well below the last 10 years average).

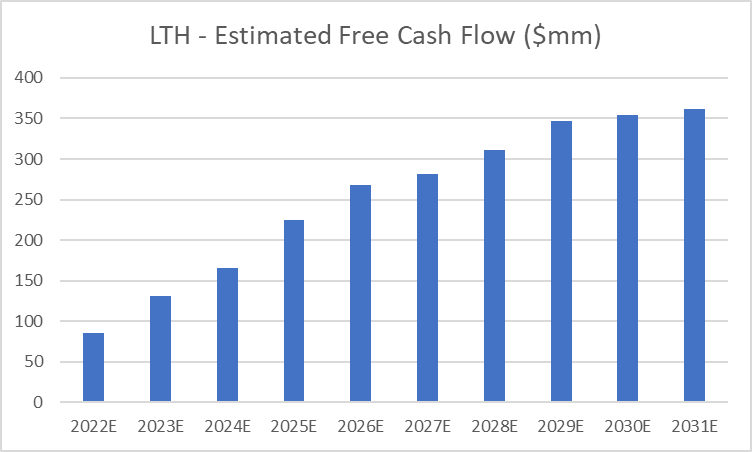

To estimate a fair price for the company, and thus a target price of a possible short position (i.e. how bad this business is and how overvalued by the market), I will be using a DCF model, with estimates derived from the research process above. Capex and EBITDA margins, the key assumptions along with revenue growth, will be used as provided by management. This shows that even if we are overly optimistic, the company is still extremely overvalued and I see a $3 billion equity value as overly rich.

Estimated FCF (Author’s own made DCF model)

Revenue growth? Again, extremely bullish and optimistic despite lower Capex. Indeed, the assumptions for growth are $2.2 billion in 2023 (15% higher than pre-covid) and then growing at 5% per year through 2027). EBITDA margin is the one forecasted by management, between 18% and 20%, an average of 19%. Discount rate is 9%, close to WACC for the company, and the perpetual value formula will be applied to compute terminal value, with a perpetual growth rate of 1%. The results imply a fair EV of $3.4 billion which, after subtracting $1.8 billion in net debt, results in a fair equity value of $1.6 billion, or $8.3 per share. The current share price of $15 then implies an overvaluation of 45%.

Conclusion

I think that LTH is a long-term unsuccessful company. Loaded with debt, it is trying a dangerous, volatile path towards de-leverage. In my opinion, the related party transactions are clearly not adding value and could harm shareholders in the long term. Compensation for the top executives also seems disproportionate, especially if compared with the actual company’s results.

Considering, (1) the precarious financial conditions, (2) poor demand growth and slow recovery, and (3) high execution risk in the debt reduction process and rental of now-owned properties, the stock is a strong sell with a target price below $8.5.

Be the first to comment